Morning Briefing Archive (2023)

A Dozen Reasons To Remain Bullish In 2024

December 18 (Monday)

Check out the accompanying pdf and chart collection.

Executive Summary: The bears who still expect a recession base their arguments on historical precedents: At times in the past when economic indicators were flashing the signs they are today, recessions occurred. But we see good reasons not to apply past rules of thumb to the current set of circumstances. Moreover, our Roaring 2020s thesis that widespread adoption of new technologies will set off a productivity boom is unfolding. As a result, we’re bullish on the outlook for the US economy and stock market. Today, we present the bears’ talking points and our rebuttals, including 12 good reasons for optimism as we enter 2024. … Also: Dr. Ed reviews “Archie” (+ +).

YRI Bulletin Board. We have launched our new website. We will be finetuning it in the coming weeks. We appreciate your patience during the transition and welcome your suggestions.

We will be recharging our batteries for the new year from December 19 to January 2. We won’t be publishing the Morning Briefing during that period or broadcasting our usual Monday webcasts. We will keep you connected to our ongoing analysis of economic and market-related events as they happen through our QuickTakes.

Dr. Ed’s next live webcast with Q&A will be at 11:00 a.m. on Monday, January 8. Replays of past weekly webcasts are available here.

Strategy I: Here We Go Again. The Great Debate that started in early 2022 between the stock market’s bulls and the bears continued in 2023 and is set to continue again in 2024. Both sides are marshalling many of the same debating points they have used since early 2022 and a few new ones.

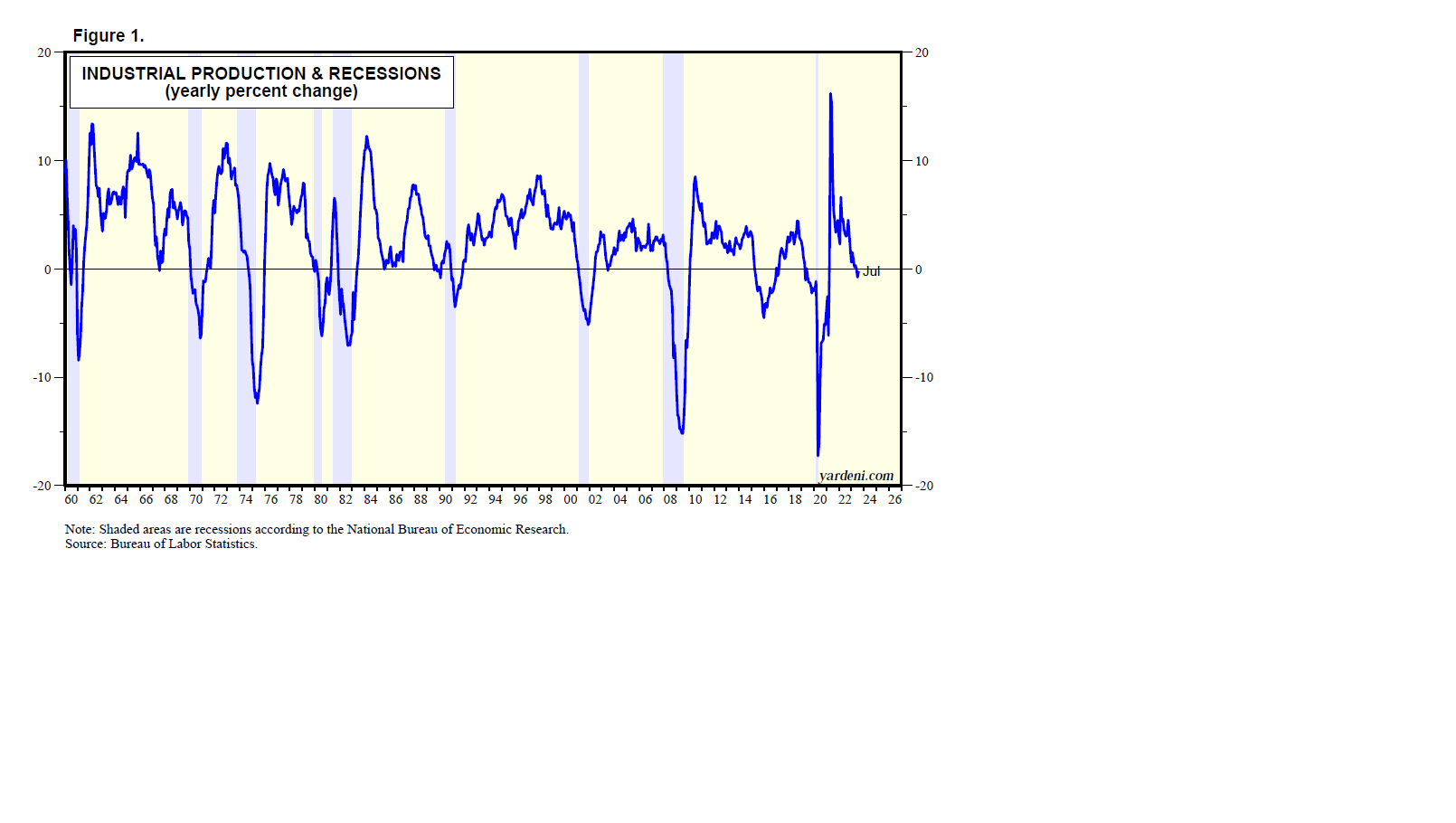

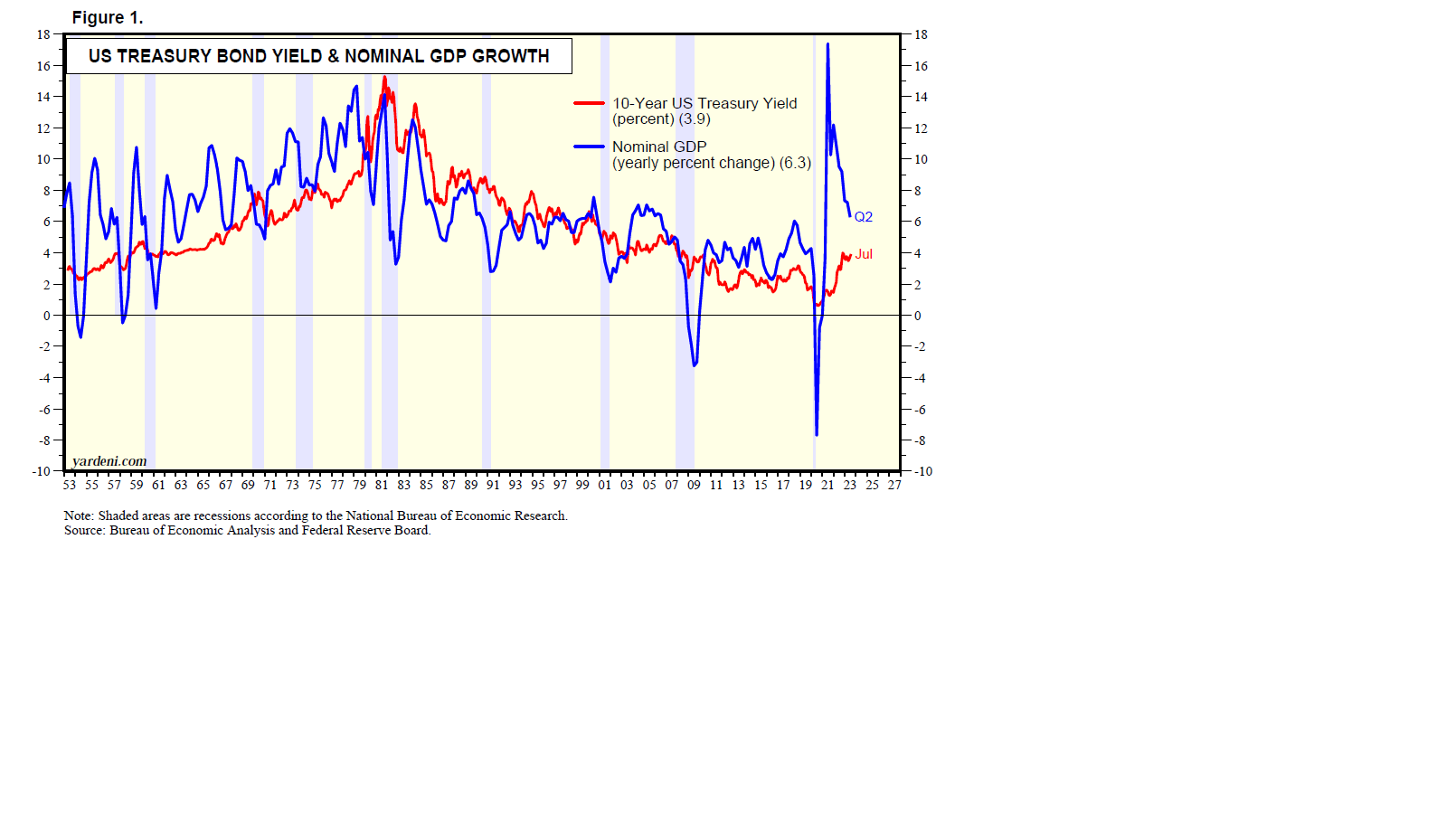

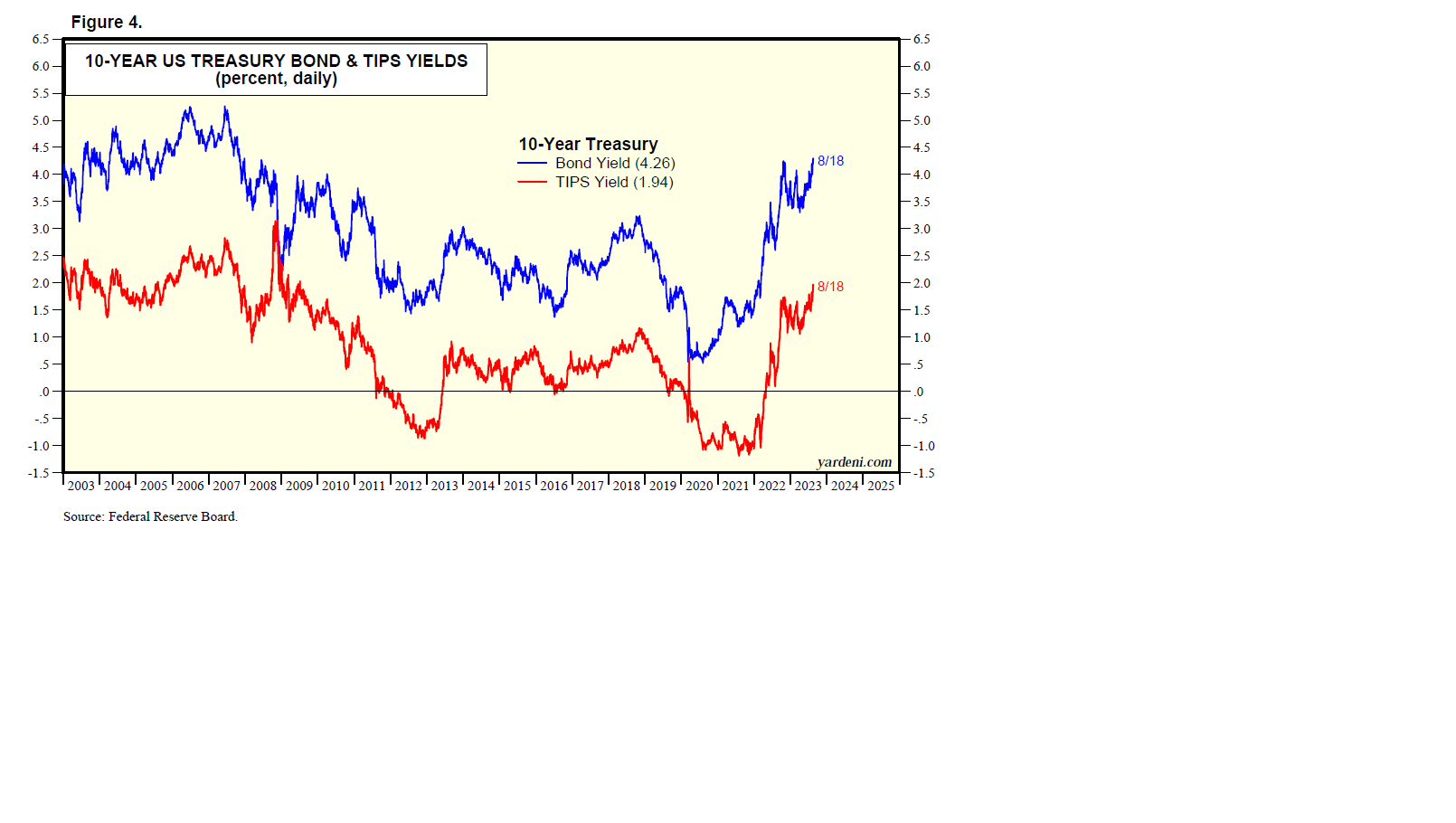

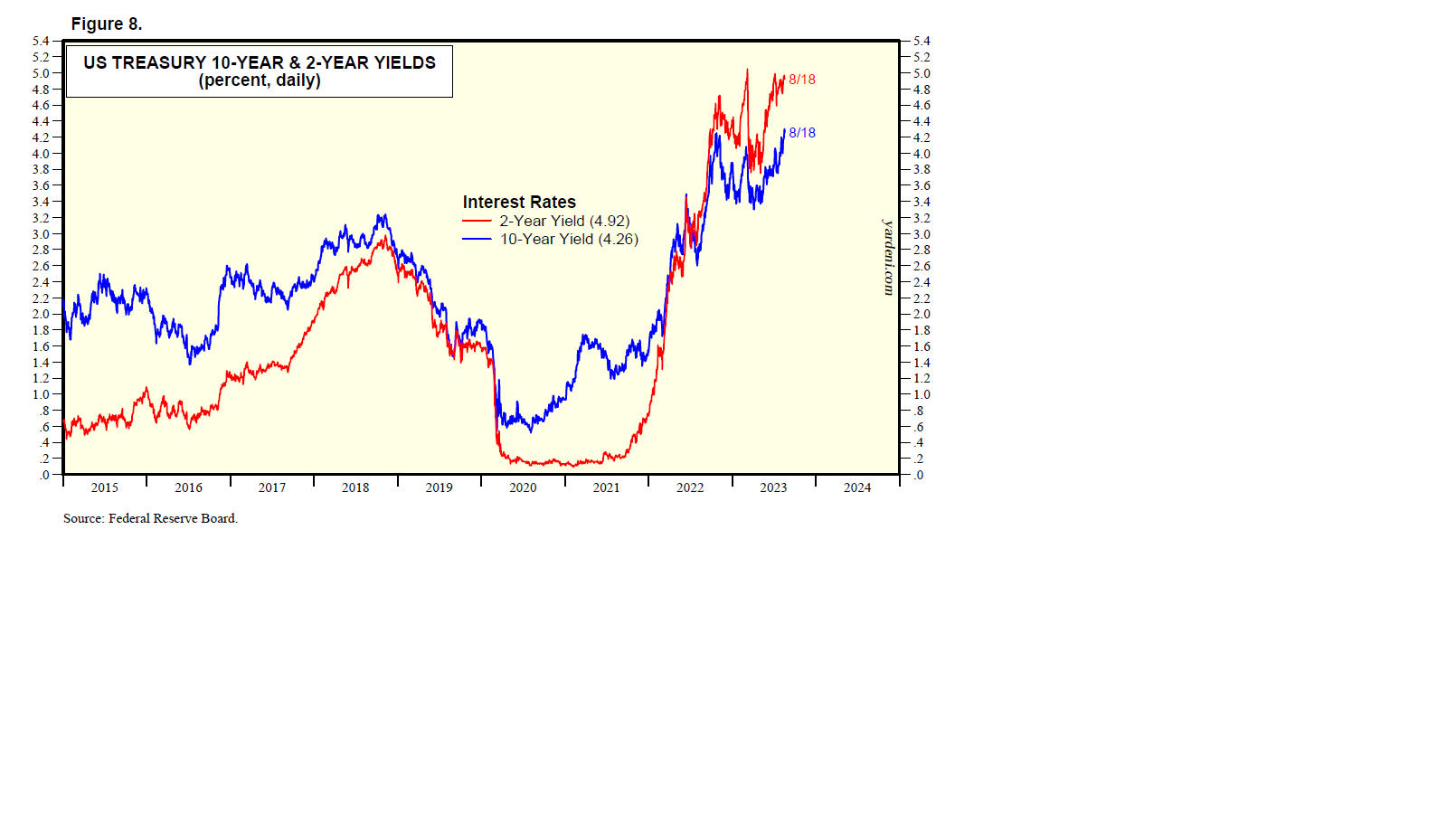

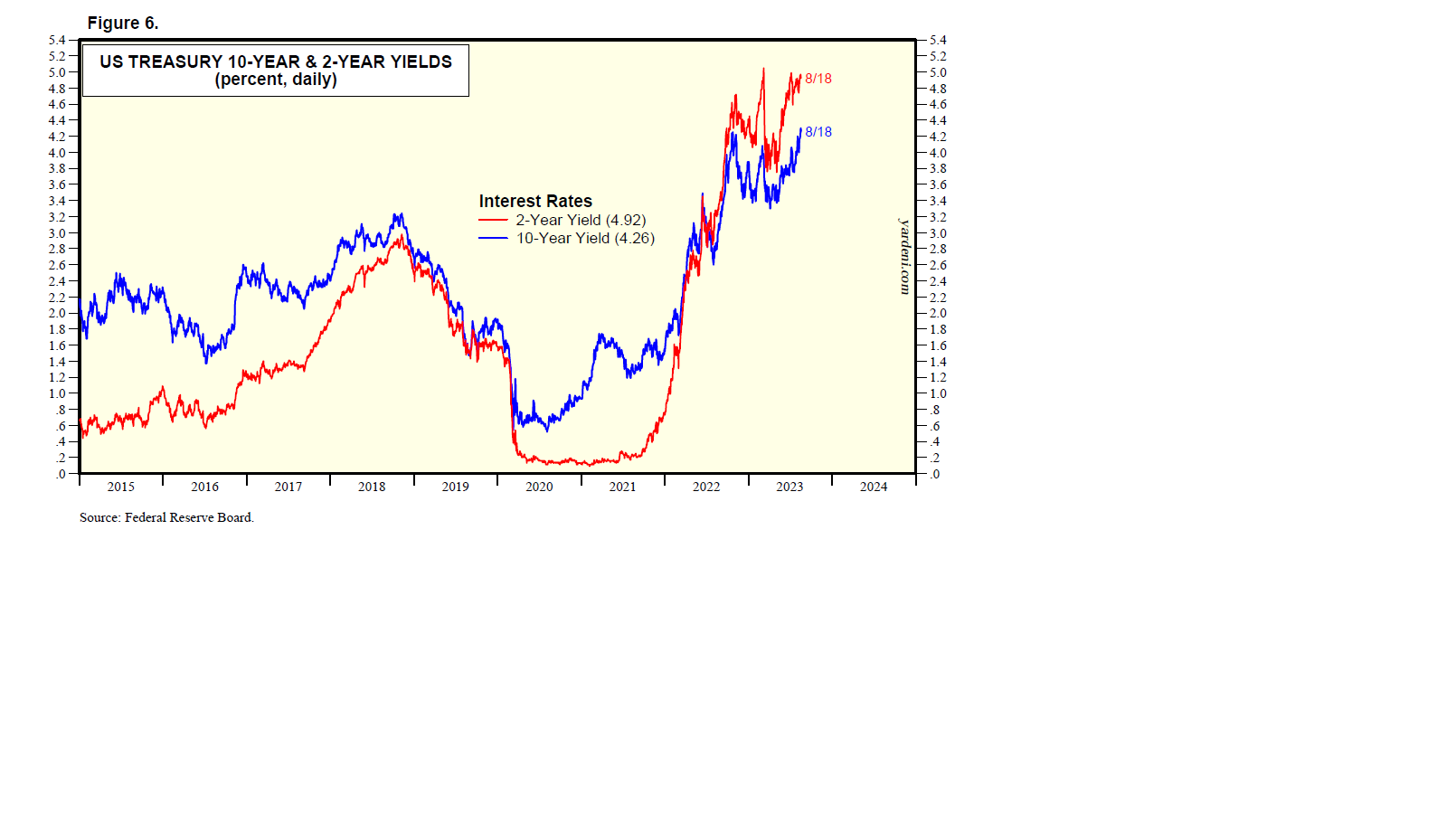

The basic thesis of the bearish debating team is that it isn’t different this time. The Fed raised the federal funds rate by 525bps from March 2020 through August of this year (Fig. 1). That’s the biggest increase since Fed Chair Paul Volcker tightened monetary policy in late 1979. In addition, this time the Fed has been paring the size of its balance sheet through quantitative tightening. This all comes after the Fed provided ultra-easy monetary policies, including ultra-low interest rates and several rounds of quantitative easing, from 2008 through 2021.

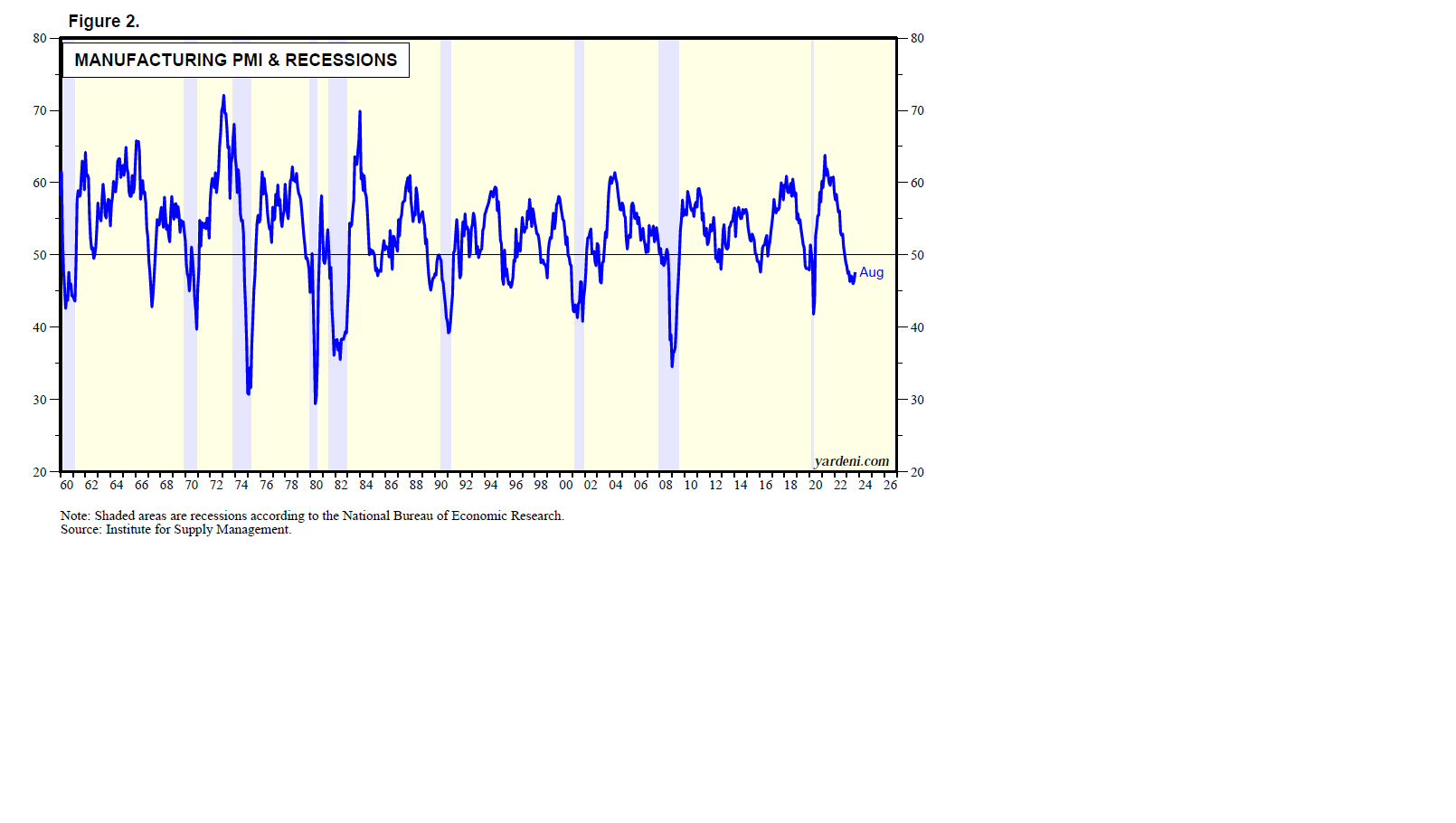

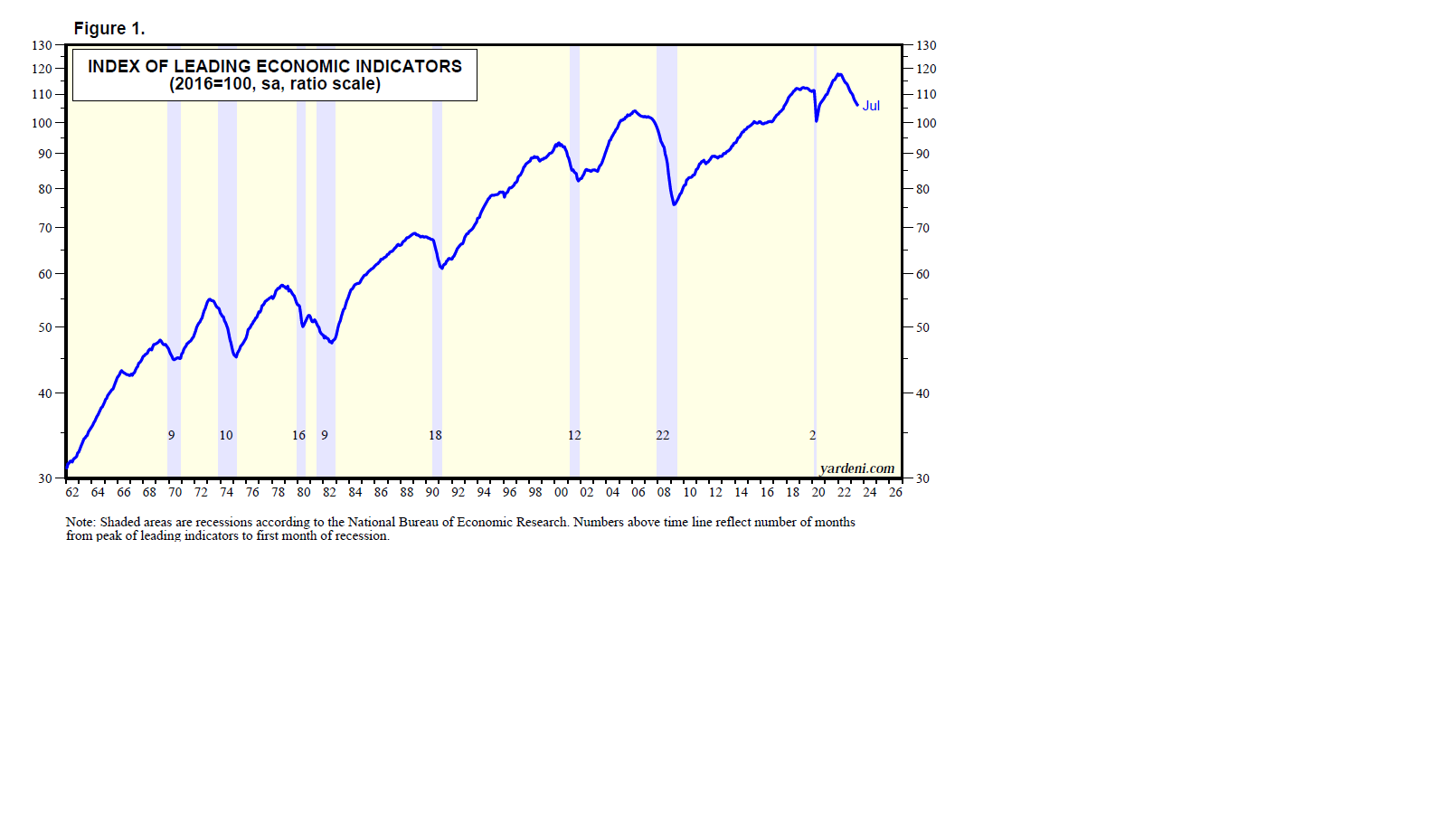

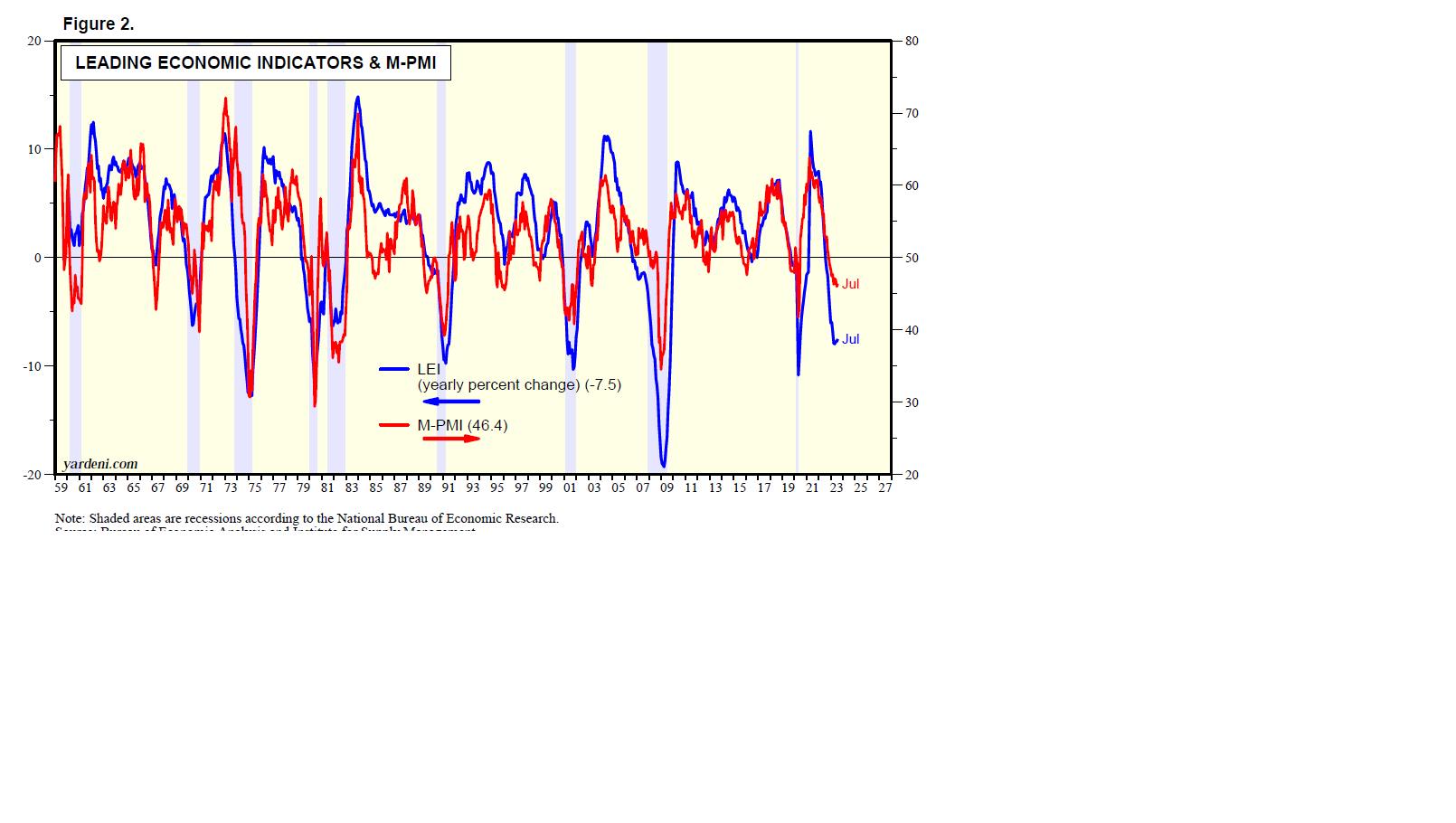

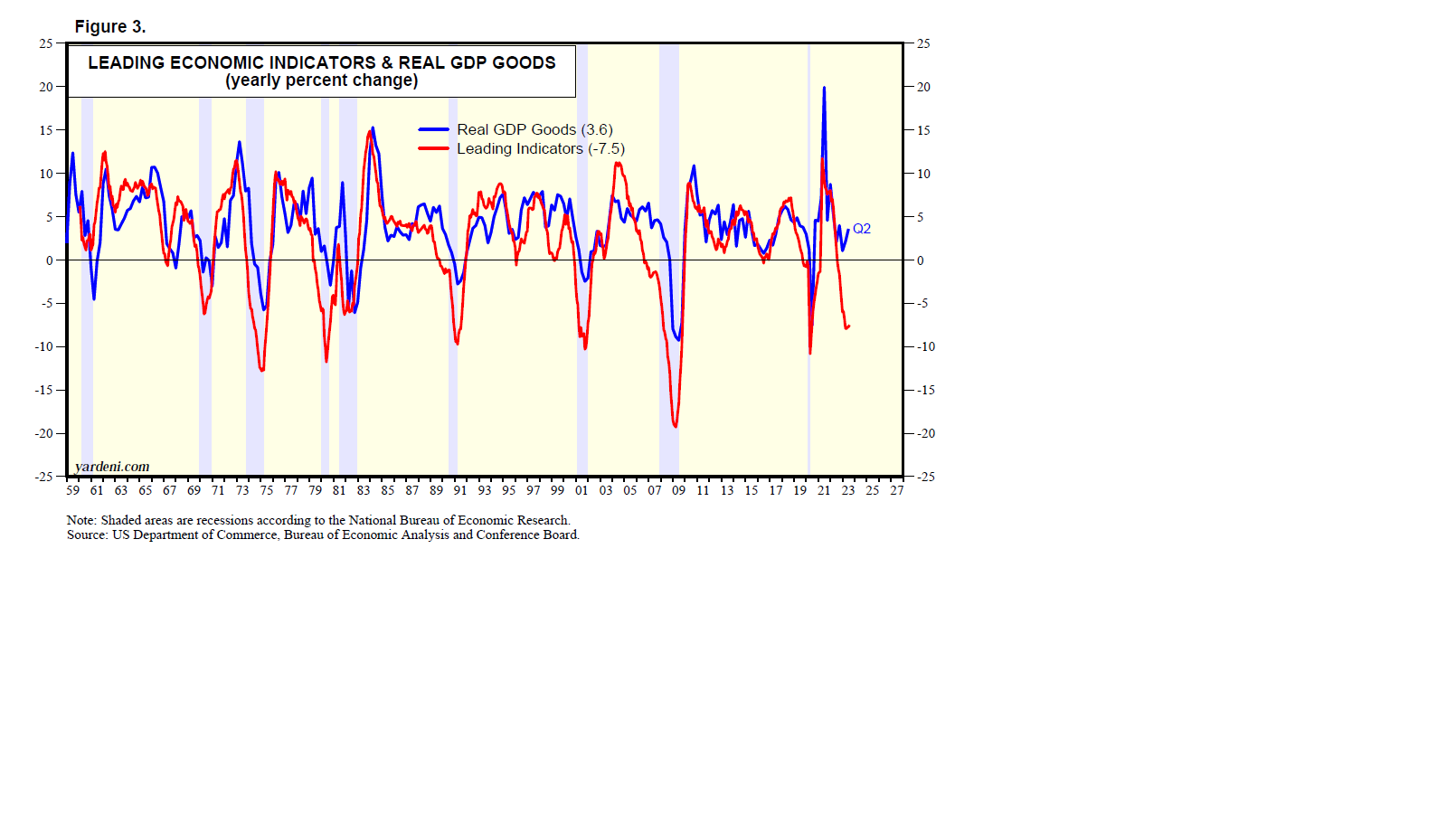

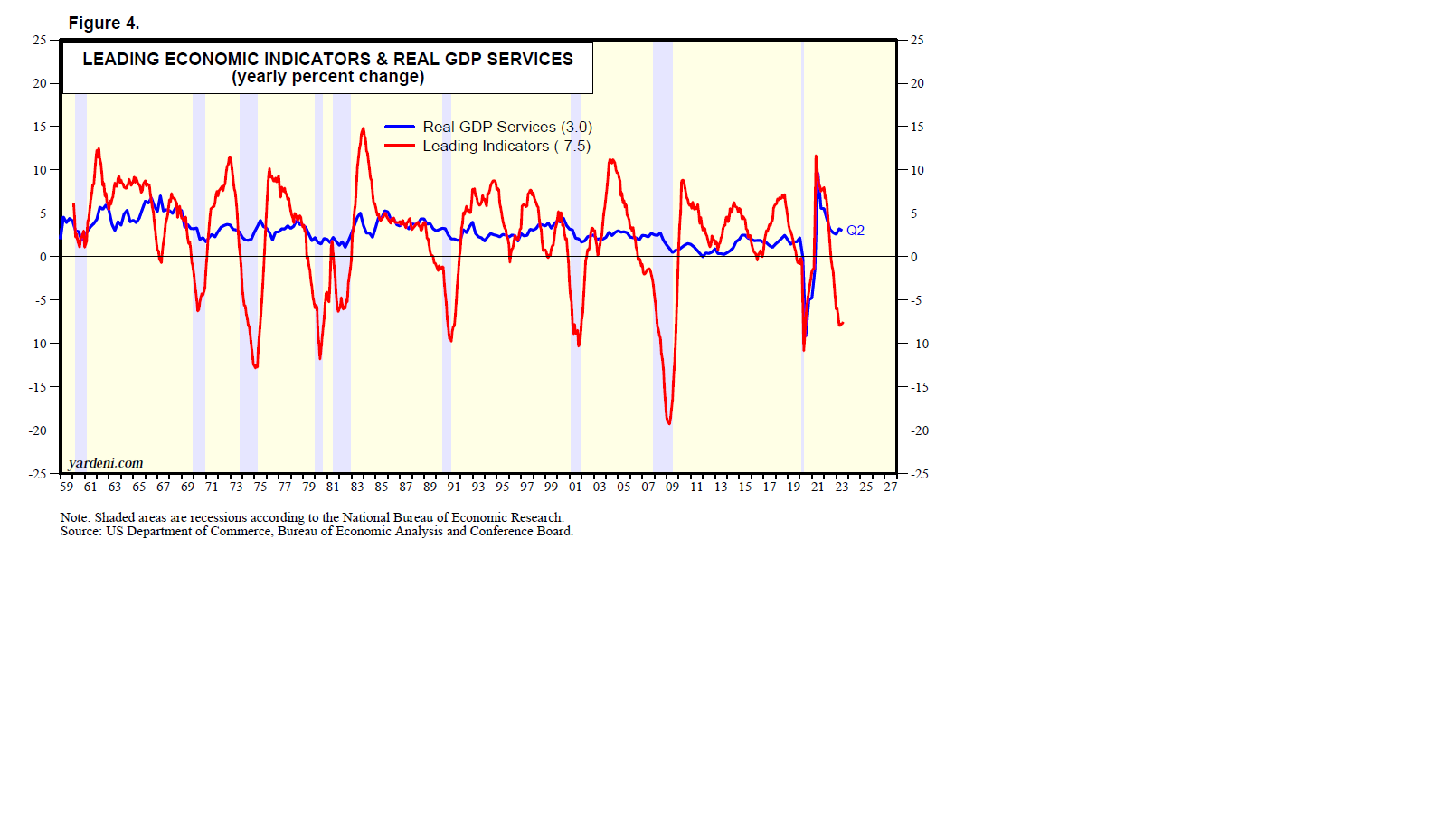

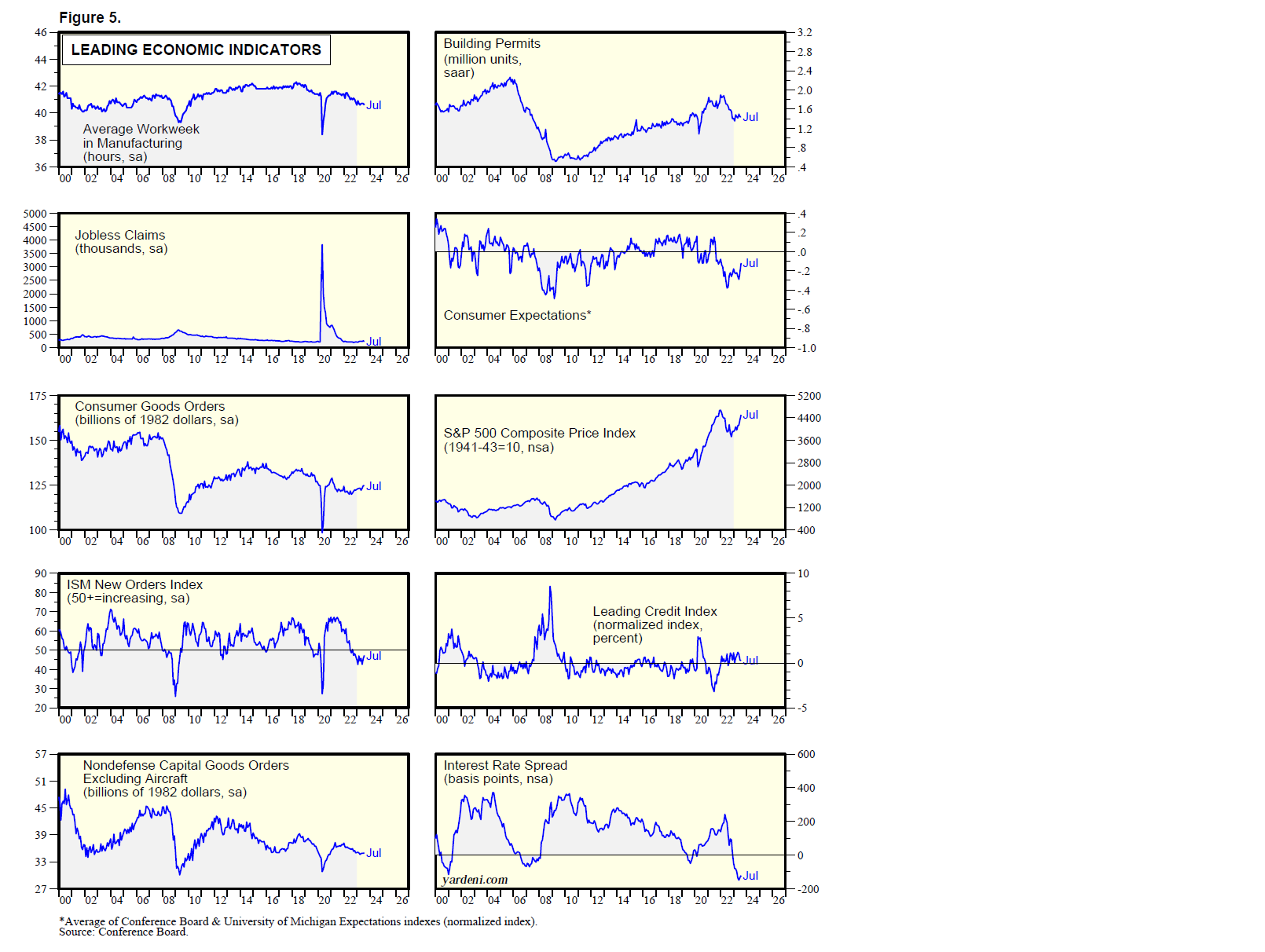

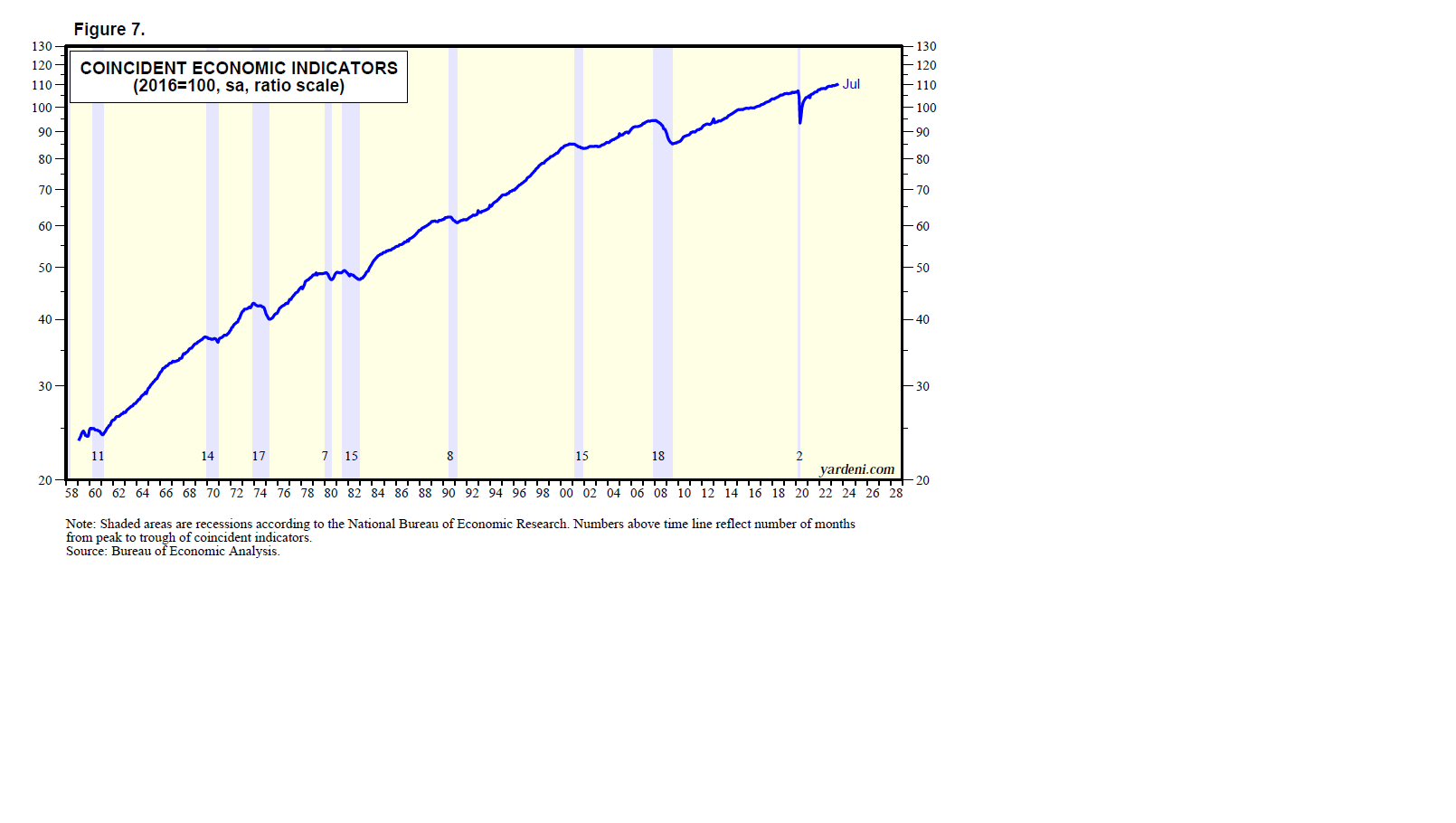

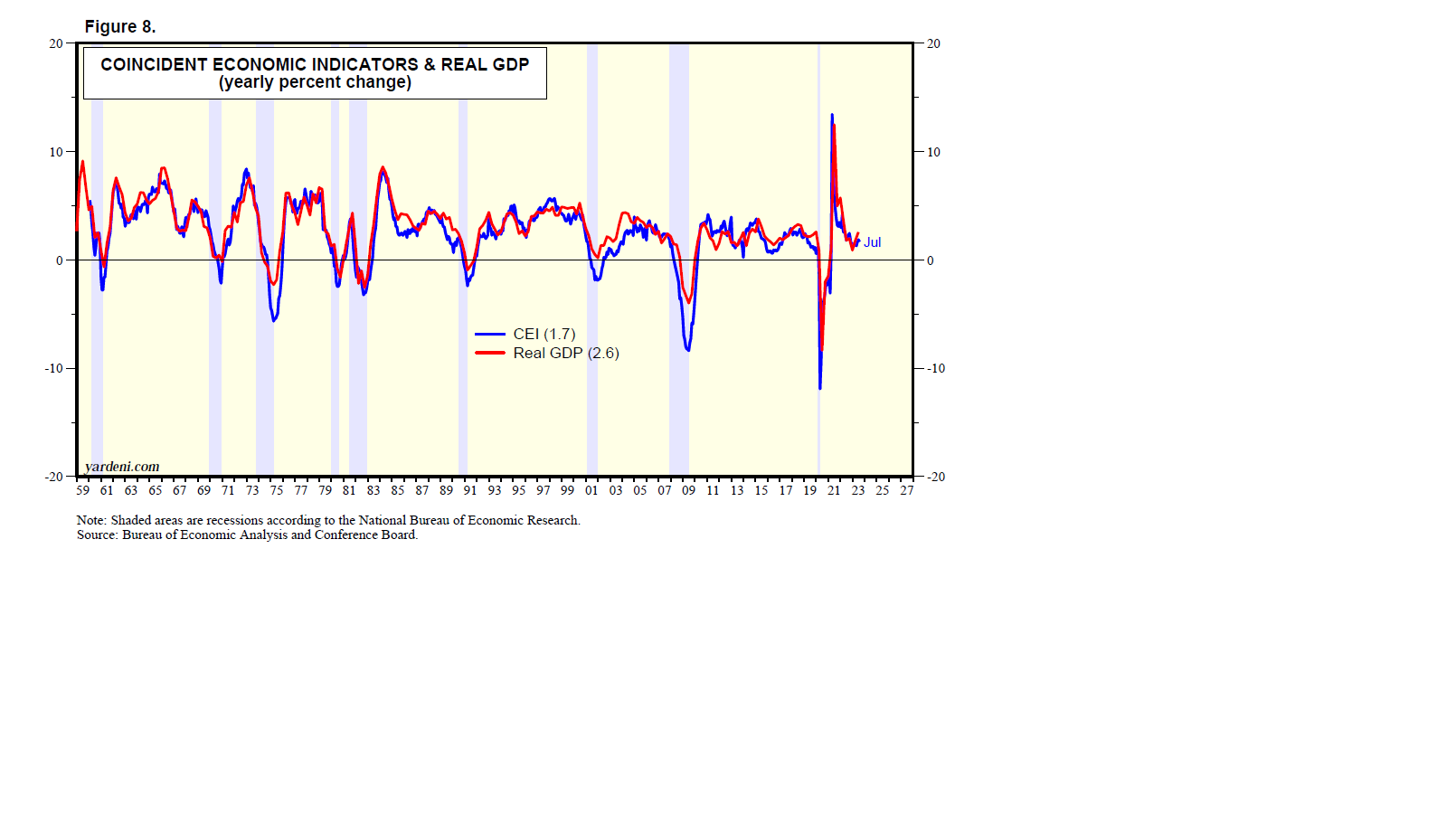

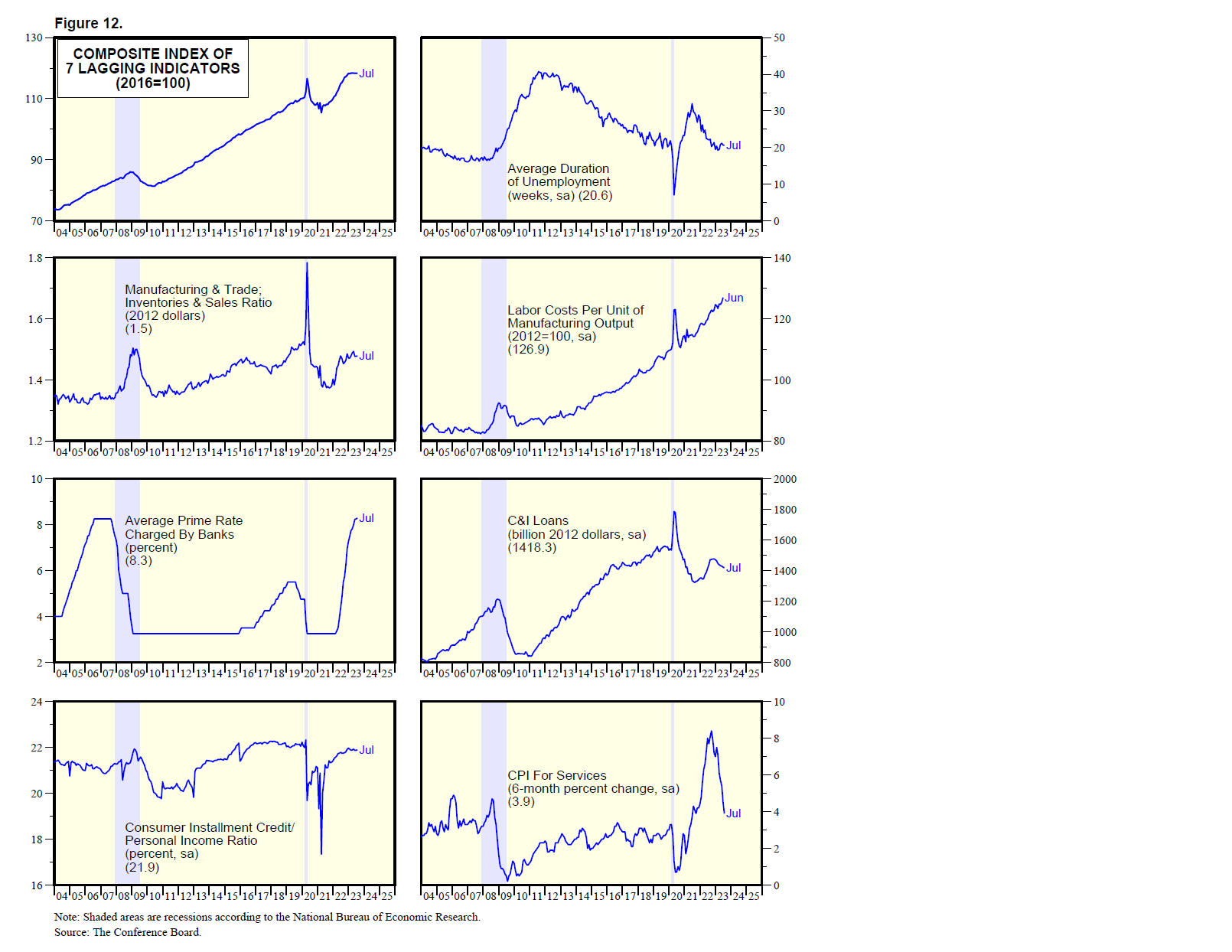

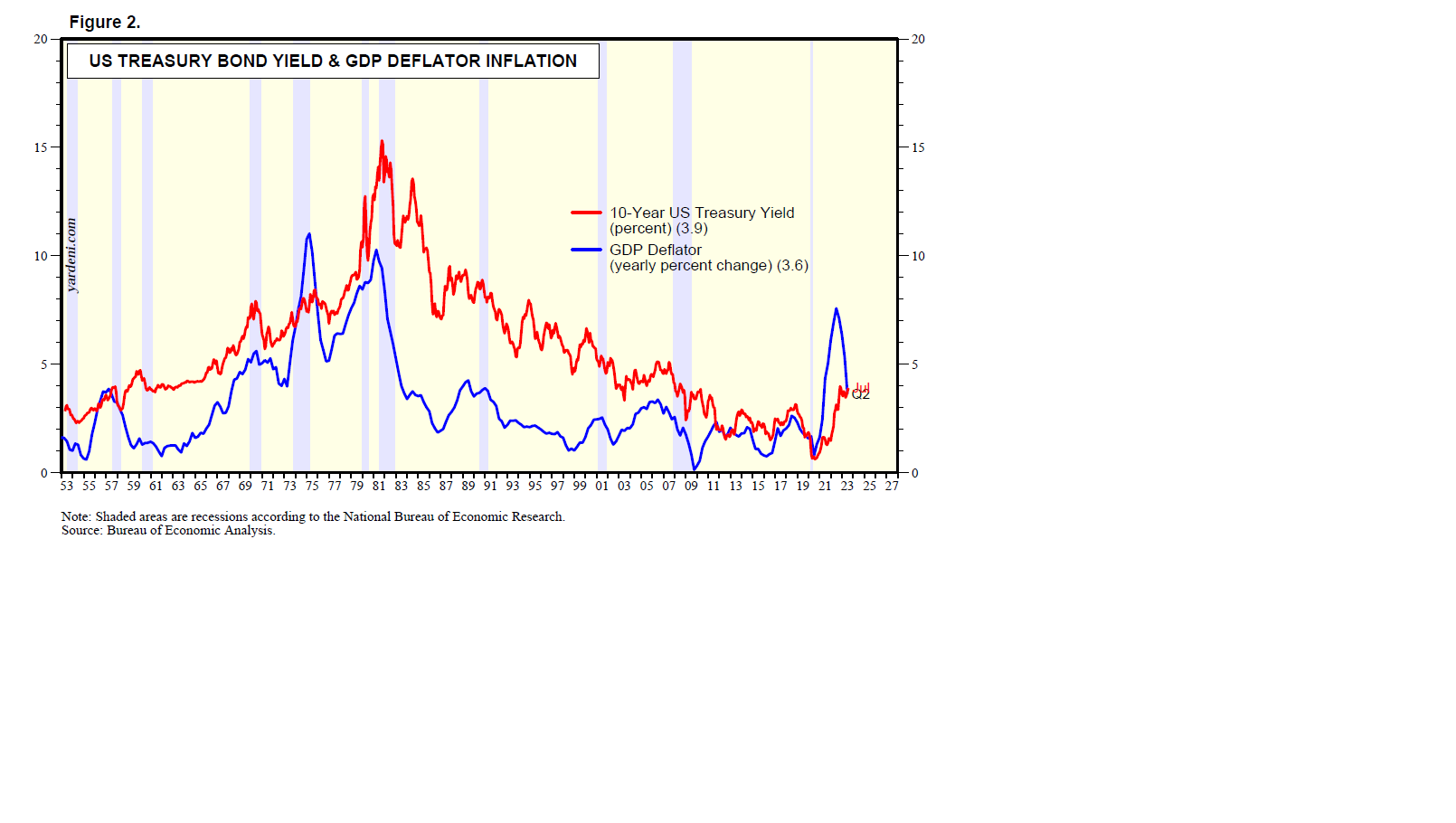

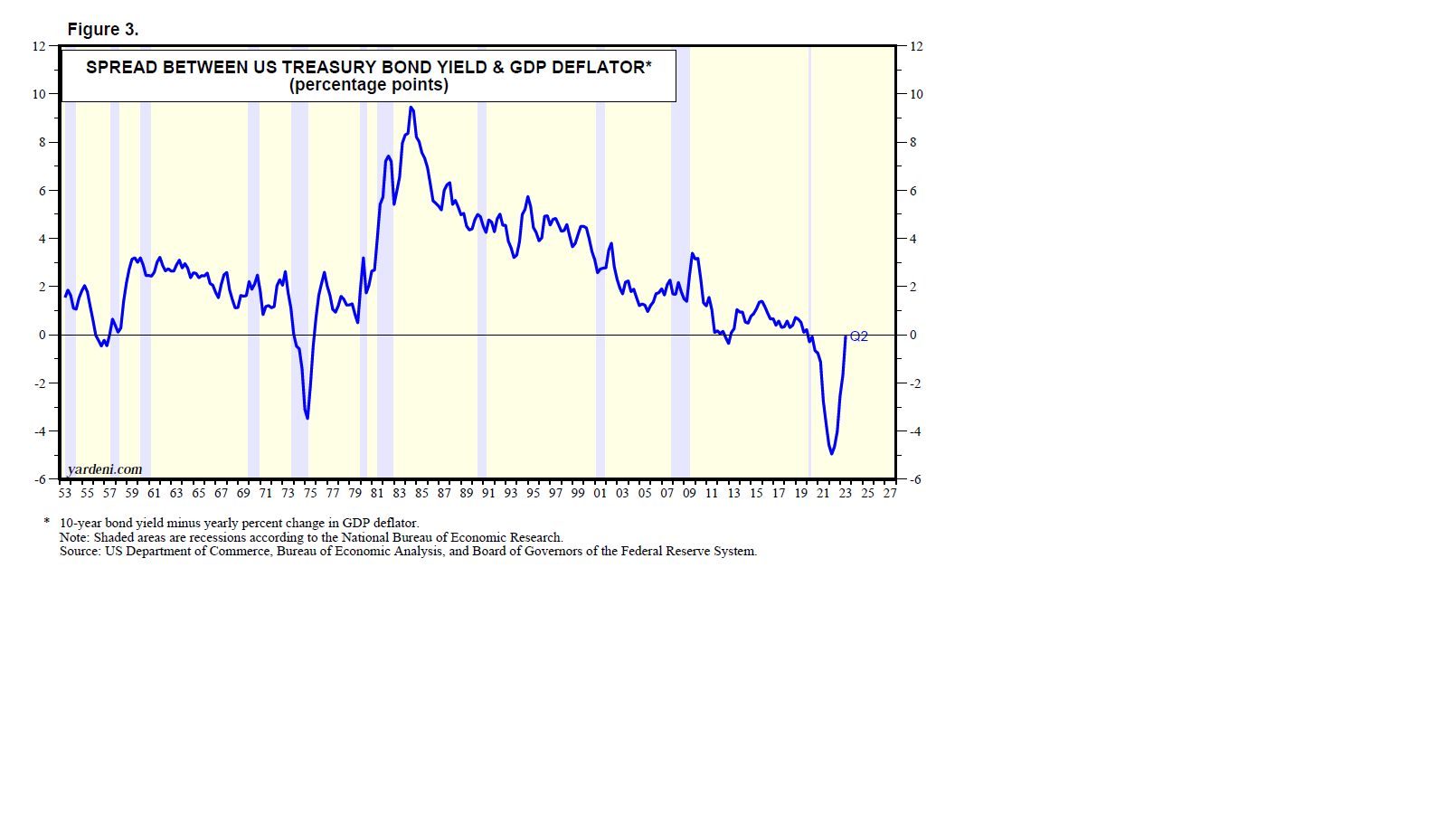

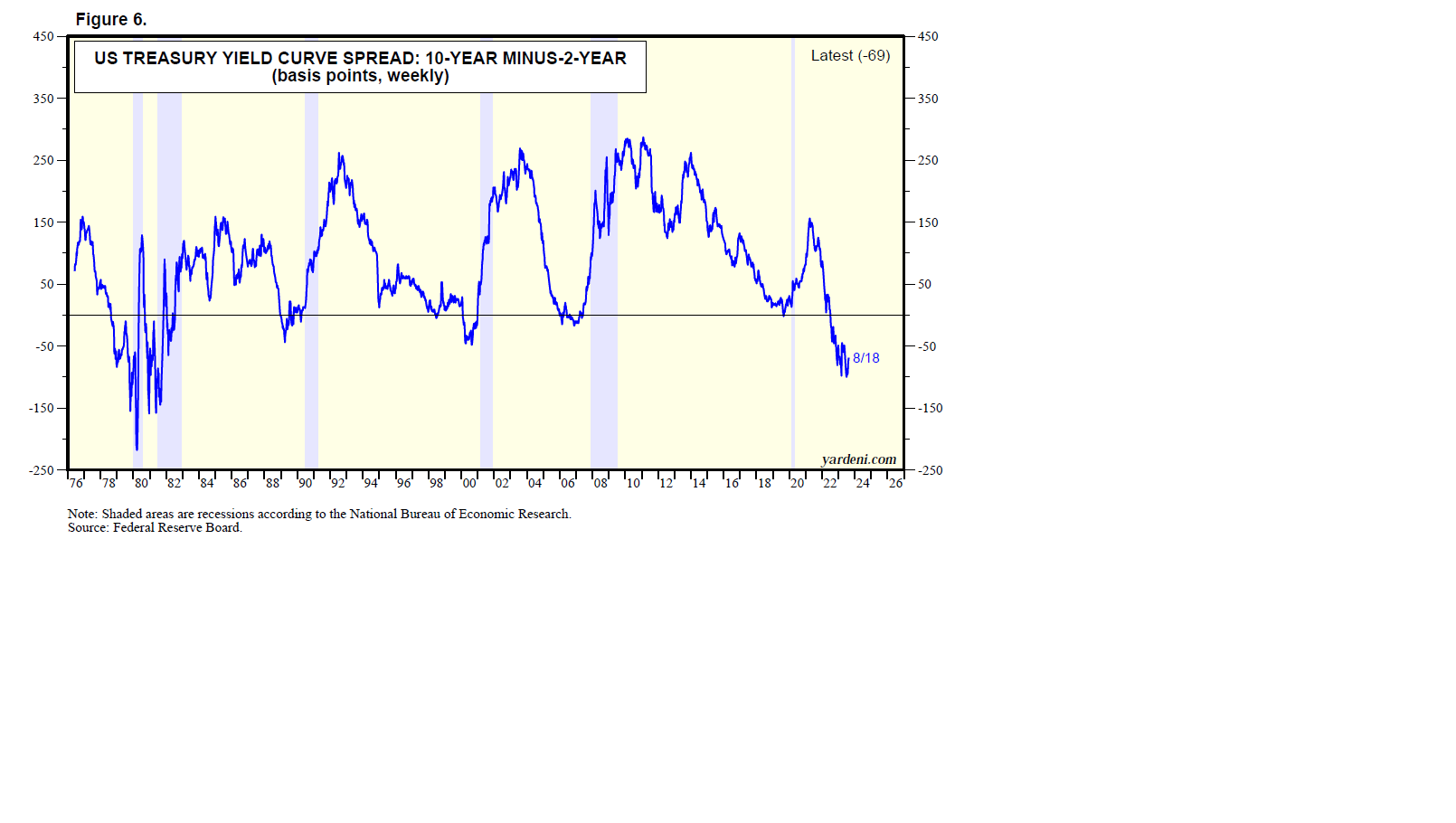

Surely such a massive swing from easy to tight monetary policy must cause a credit crunch and a recession, the thinking goes, and probably a severe one! Monetary policy tightening cycles usually have been followed by recessions (Fig. 2). Indeed, each of the past 10 recessions was preceded by such a cycle. Supporting the recession outlook is the yield curve, which has been inverting since the summer of 2022 (Fig. 3). The yield-curve spread is one of the 10 components of the Index of Leading Economic Indicators (LEI), which has been falling since it hit a record high during December 2021 (Fig. 4). It is down 11.8% since then through October. Granted, the Index of Coincident Economic Indicators rose to a record high in October, but it is bound to fall in 2024, according to the bears. Also, an ominous sign for real GDP growth is that real M2 has been falling on a y/y basis since December 2022 (Fig. 5).

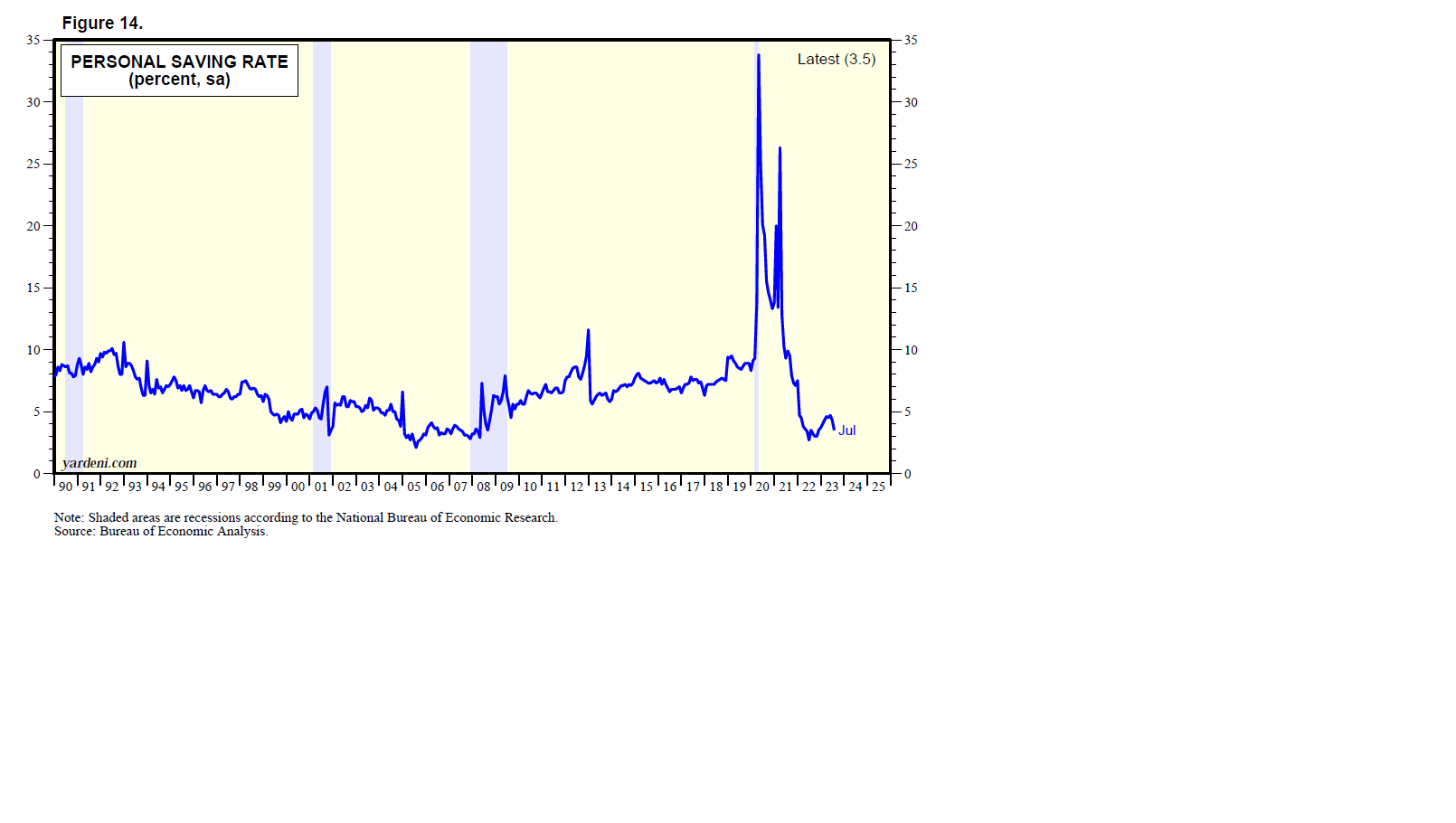

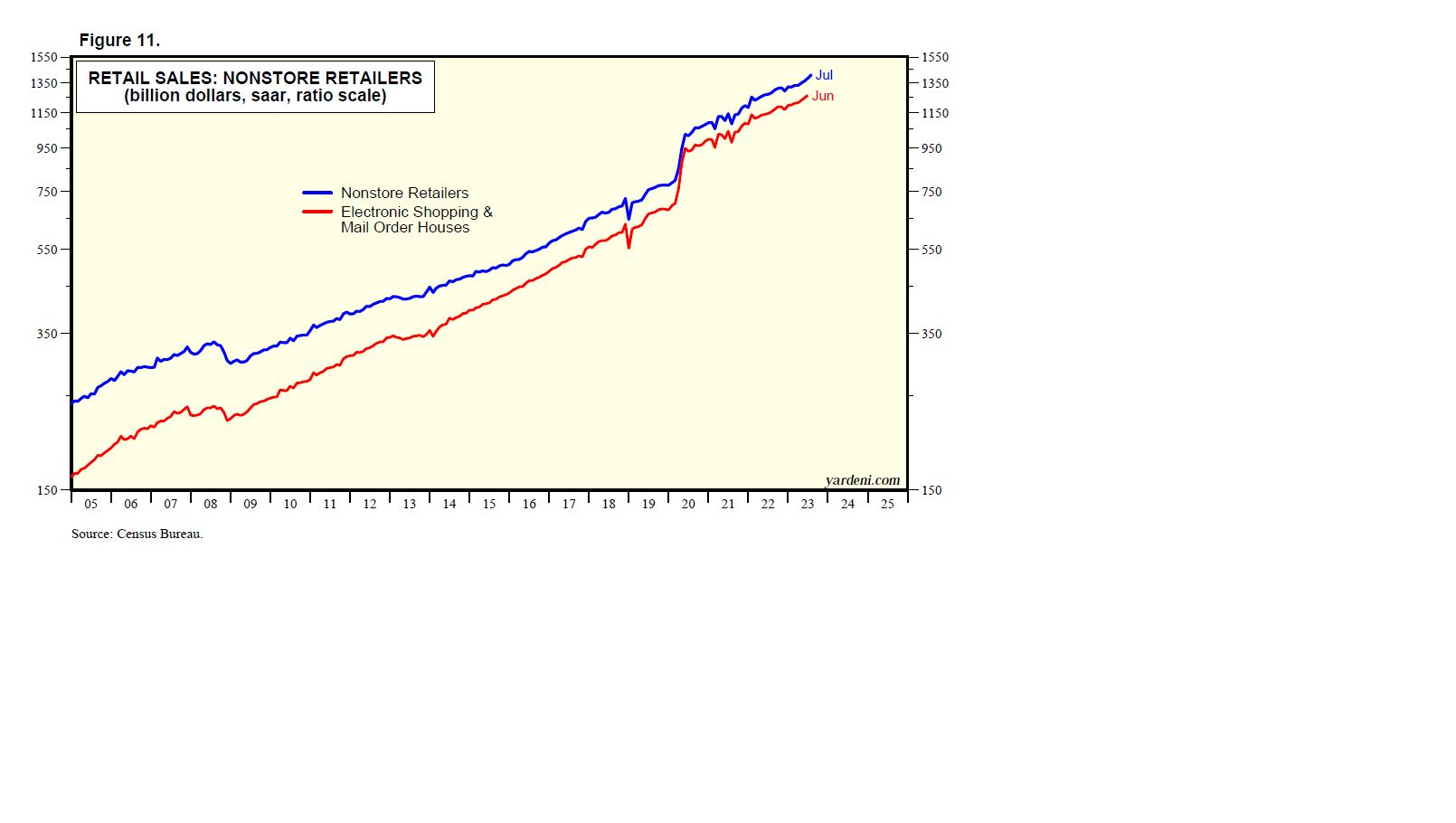

Recognizing that consumer spending currently accounts for 68% of nominal GDP, the bears have been attributing the resilience of consumer spending to “excess saving,” which they had expected to run out by now. So now they say that whatever is left will be spent in the coming months, forcing consumers to retrench next year. Meanwhile, another alarming signal, they say, is that consumer credit rose to a record $5.0 trillion, with revolving credit up to a record $1.3 trillion, during October. They’ve also been warning that the resumption of student loan payments during October would depress consumer spending. However, retail sales were surprisingly strong during November, so that is likely to be dropped as a talking point of the bearish squad.

Before we present our rebuttal to the bears’ arguments, here’s some perspective on our stock market outlook and how it compares to the expectations of other Wall Street strategists.

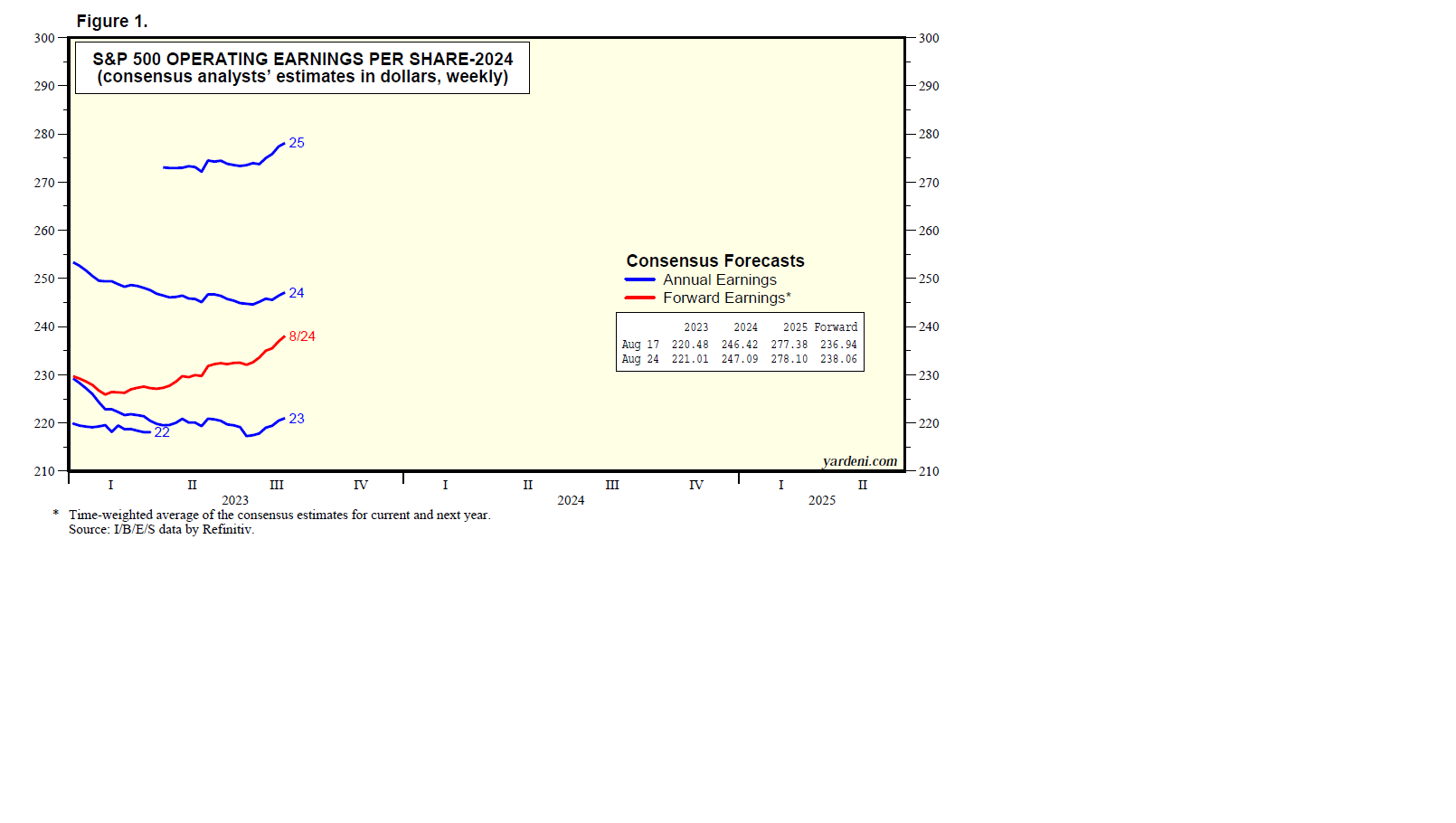

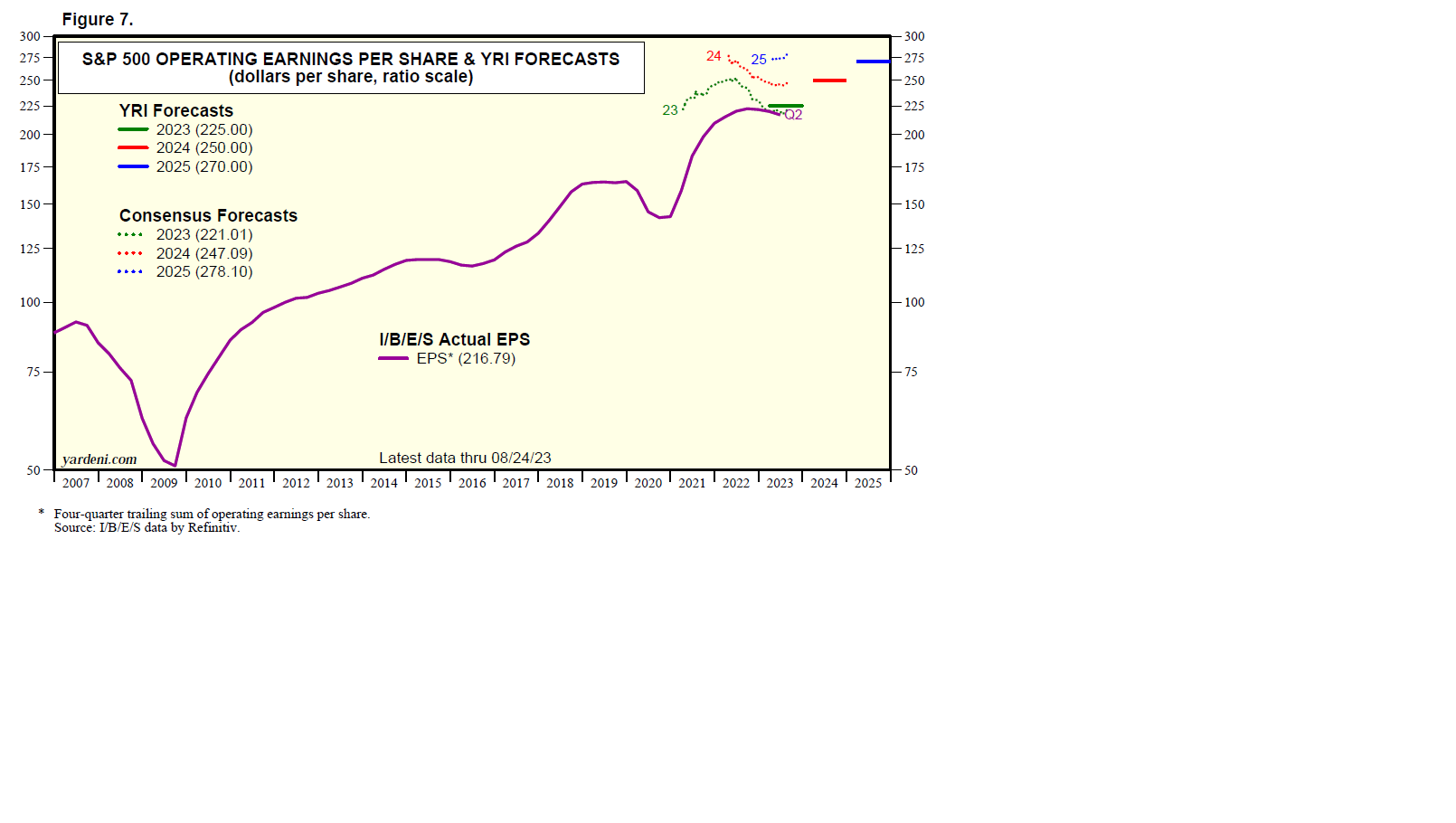

Strategy II: Bullish Targets. The current issue of Barron’s includes the 2024 S&P 500 targets for six investment strategists including yours truly. Our target is the highest at 5400, based on projected S&P 500 earnings per share of $250 next year. Morgan Stanley’s Mike Wilson has the lowest numbers at 4500 for the index’s price target and $229 for earnings per share. In last year’s survey by Barron’s, we had 4800 as our S&P 500 target for last year with earnings at $225. The low comparable readings were 3930 and $199 for 2023.

Along the way, we trimmed our year-end target to a more reasonable 4600. Then, on June 5, we wrote: “Is all the AI euphoria leading the stock market into another ‘MAMU’—‘Mother of All Meltups’? If so, our 4600 target for the S&P 500 by year-end might prove conservative, not controversial.”

On July 19, we wrote: “The S&P 500 is now almost at 4600. It closed at 4556.27 on Tuesday. Rather than raise our year-end target, we are raising our expectations for what the bull market could deliver through the end of 2024 and beyond. We think that 5400 is achievable by the end of next year. If that happens, then 5800 would be our target for the end of 2025. In other words, we think that the bull market has staying power.”

Last week, we raised our 2025 target for the S&P 500 price index to 6000, as our Roaring 2020s scenario is looking not only possible, but also probable.

Strategy III: A Dozen Good Reasons. Now let’s review our talking points on behalf of the bullish team in the Great Debate. Here’s an even dozen:

(1) Interest rates are back to normal. Perhaps the Fed hasn’t been tightening monetary policy so much as normalizing it. Interest rates are back to the Old Normal. They are back to where they were before the New Abnormal period between the Great Financial Crisis and the Great Virus Crisis, during which the Fed pegged interest rates near zero.

The normalization theory implies that the Fed might not lower interest rates next year as much as widely expected. That’s because the economy wouldn’t require as much easing to reverse the tightening. If the economy remains resilient but inflation continues to fall closer to the Fed’s 2.0% target next year—both of which we’re expecting—then the Fed might lower the federal funds rate twice next year, by 25bps each time, instead of four times or more as widely anticipated.

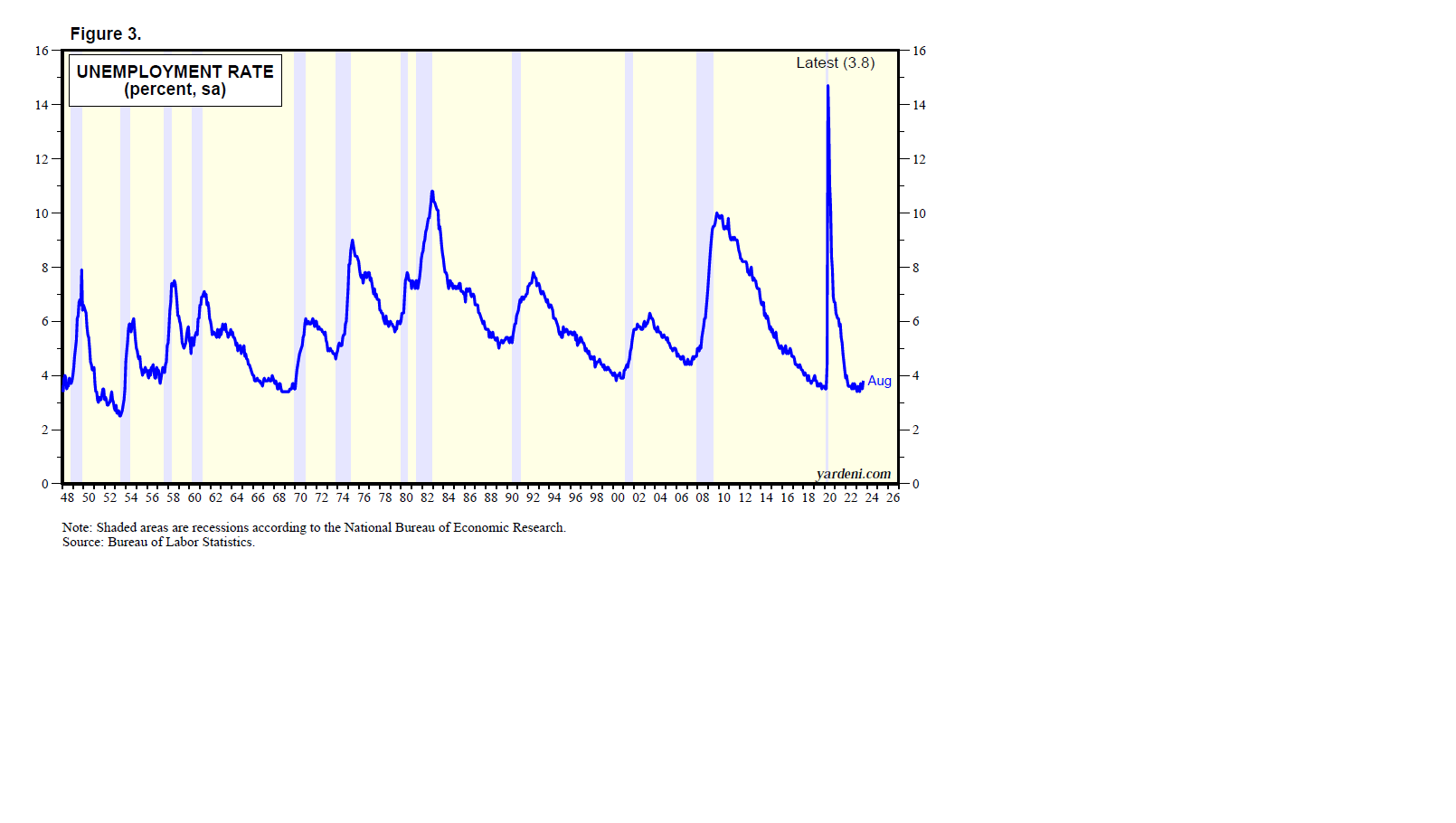

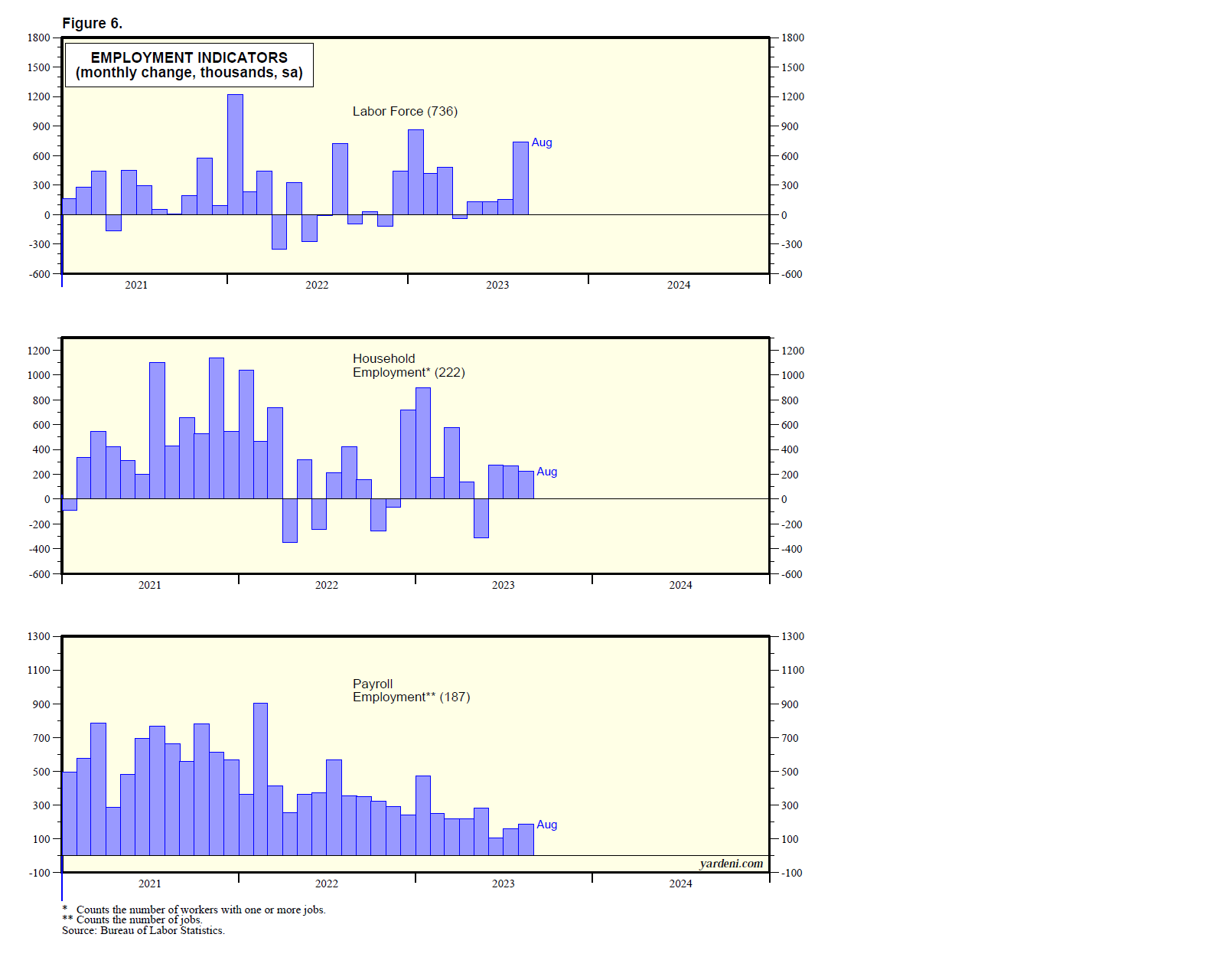

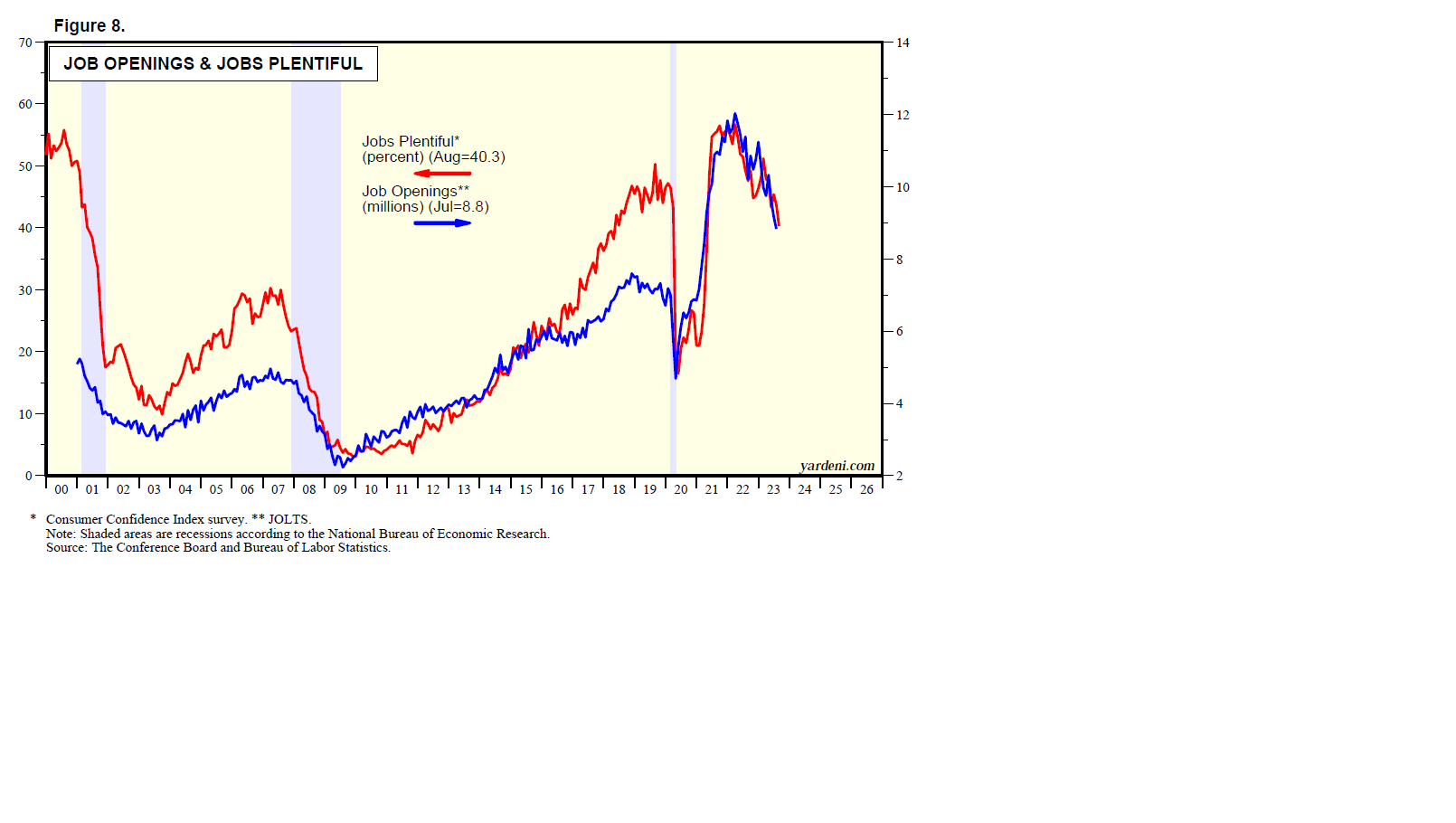

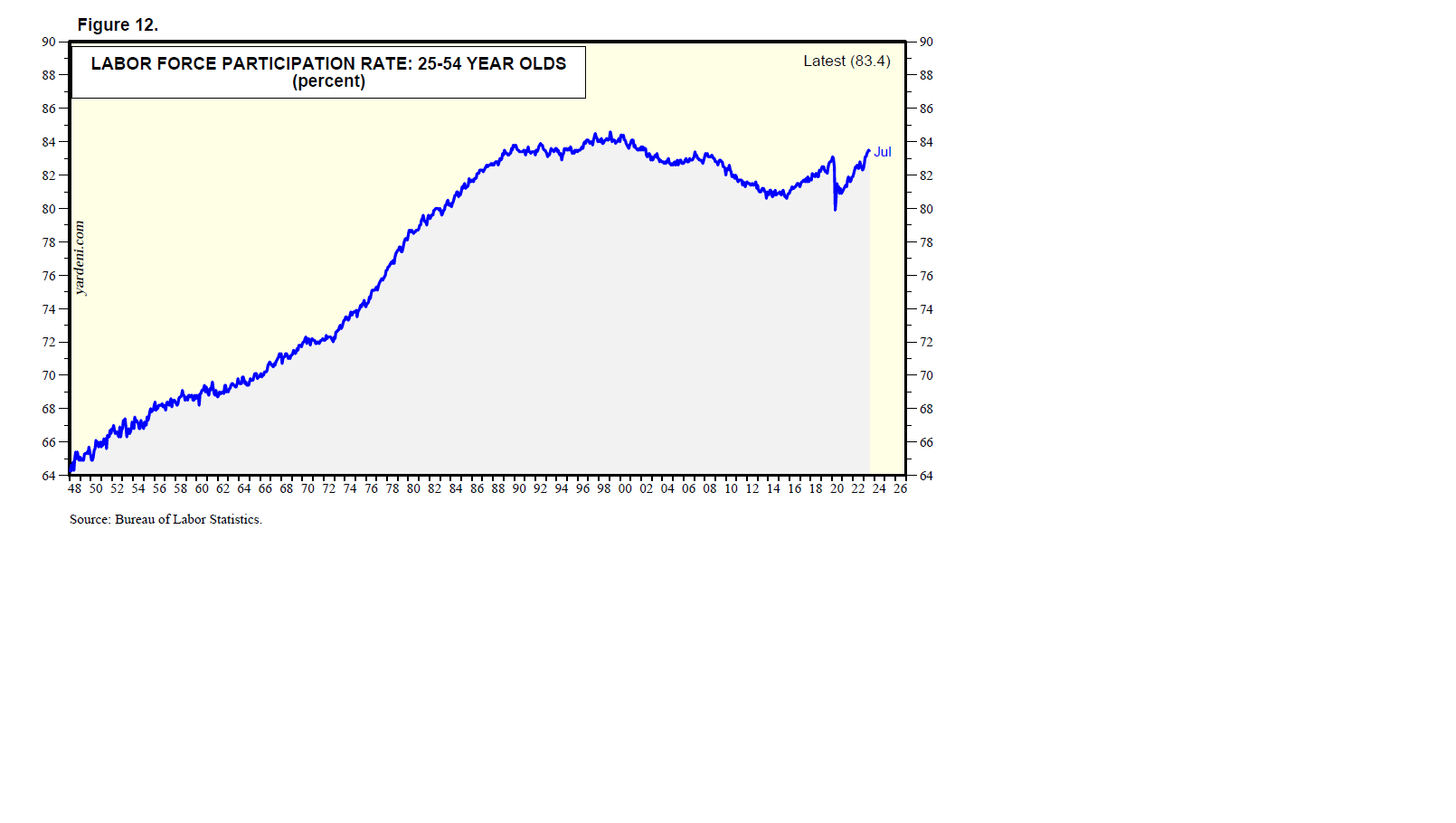

(2) Consumers have purchasing power. Many consumers may soon run out of their excess saving, as the economy’s naysayers are saying. Some consumers could be weighed down by too much consumer debt, especially student loans. Nevertheless, most of them are likely to continue to consume as long as their job security remains high, which it will be as long as there are plenty of job openings and as long as the unemployed and new entrants to the labor force fill those openings. That describes the current state of the labor market.

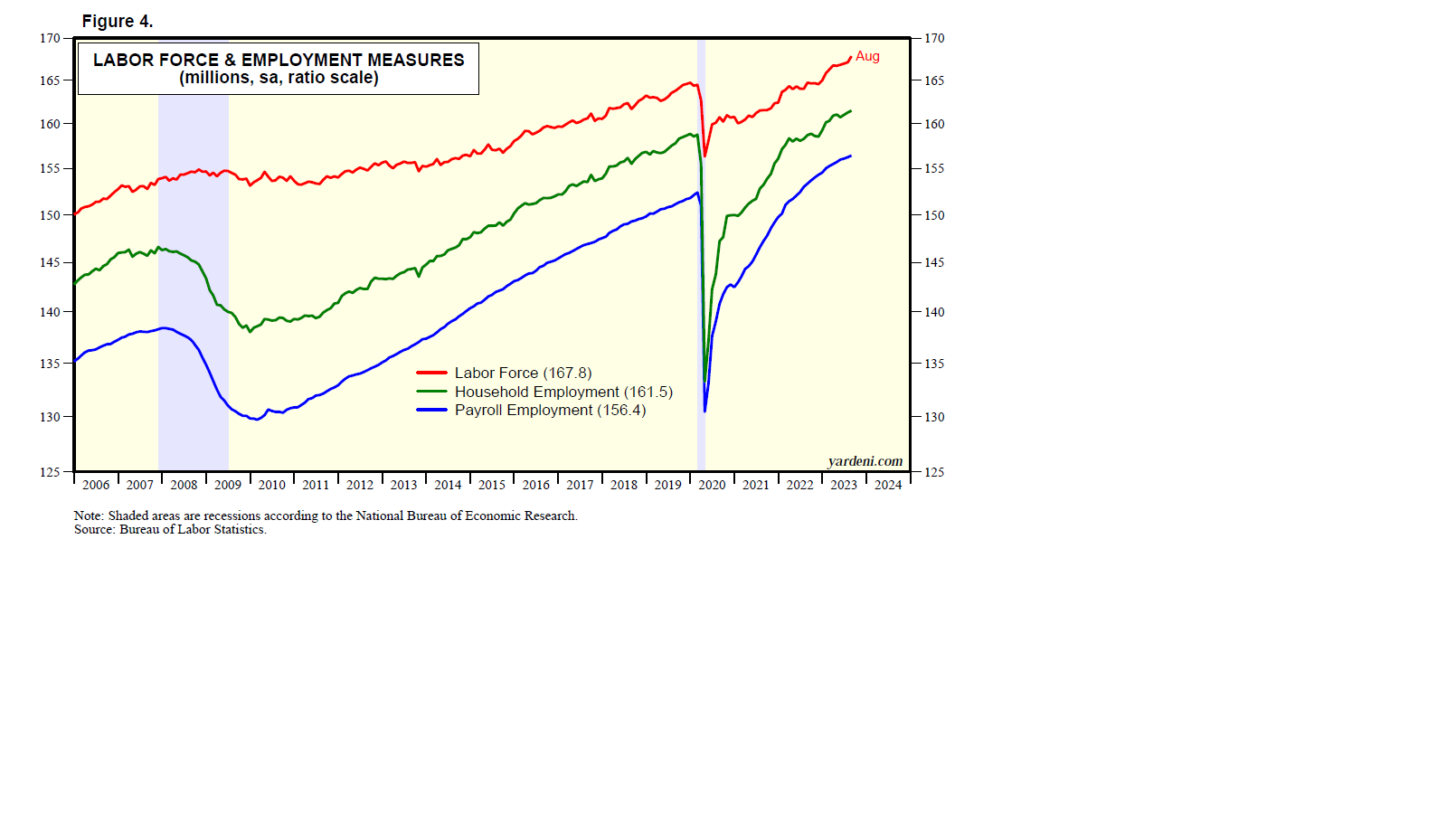

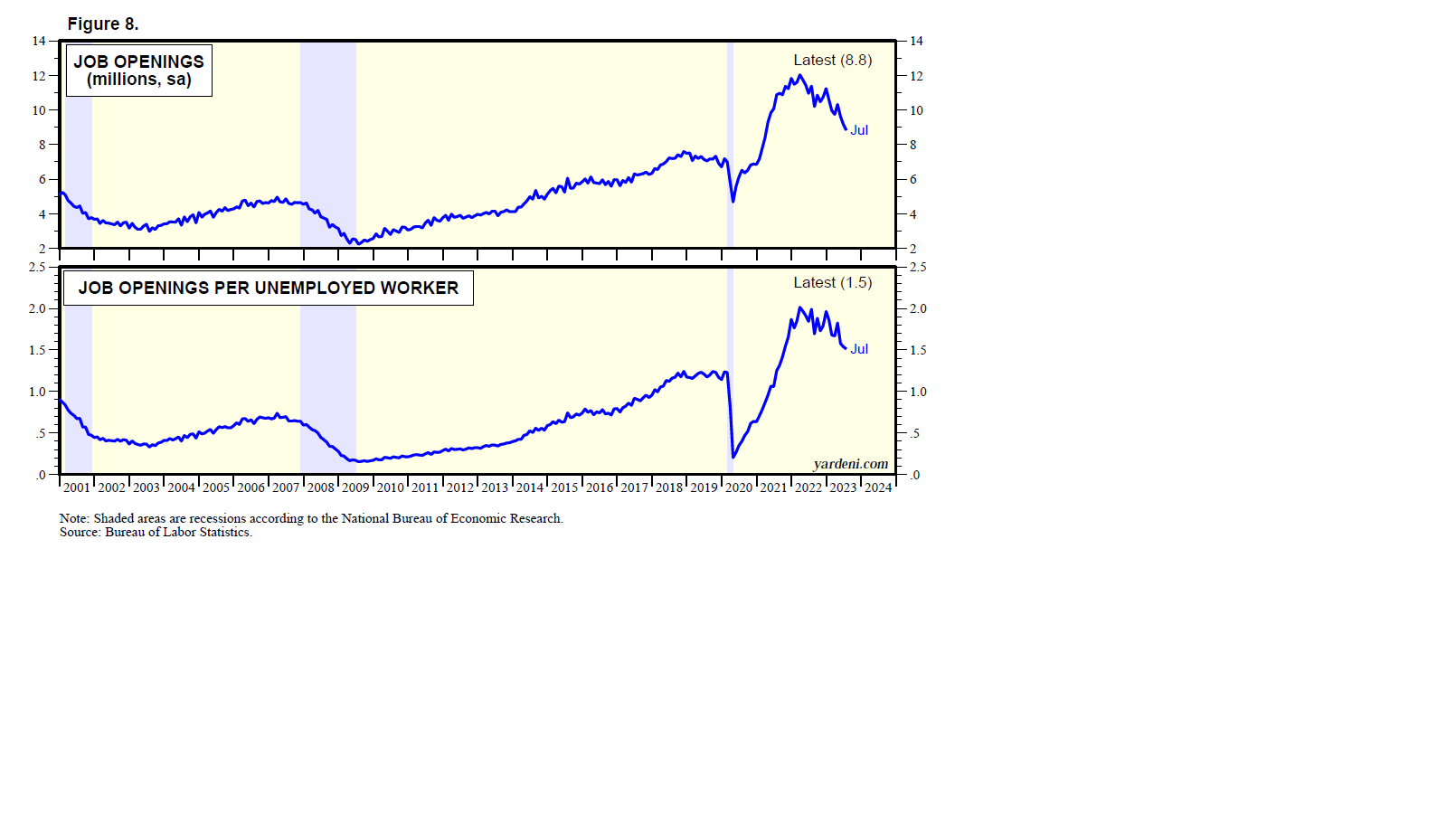

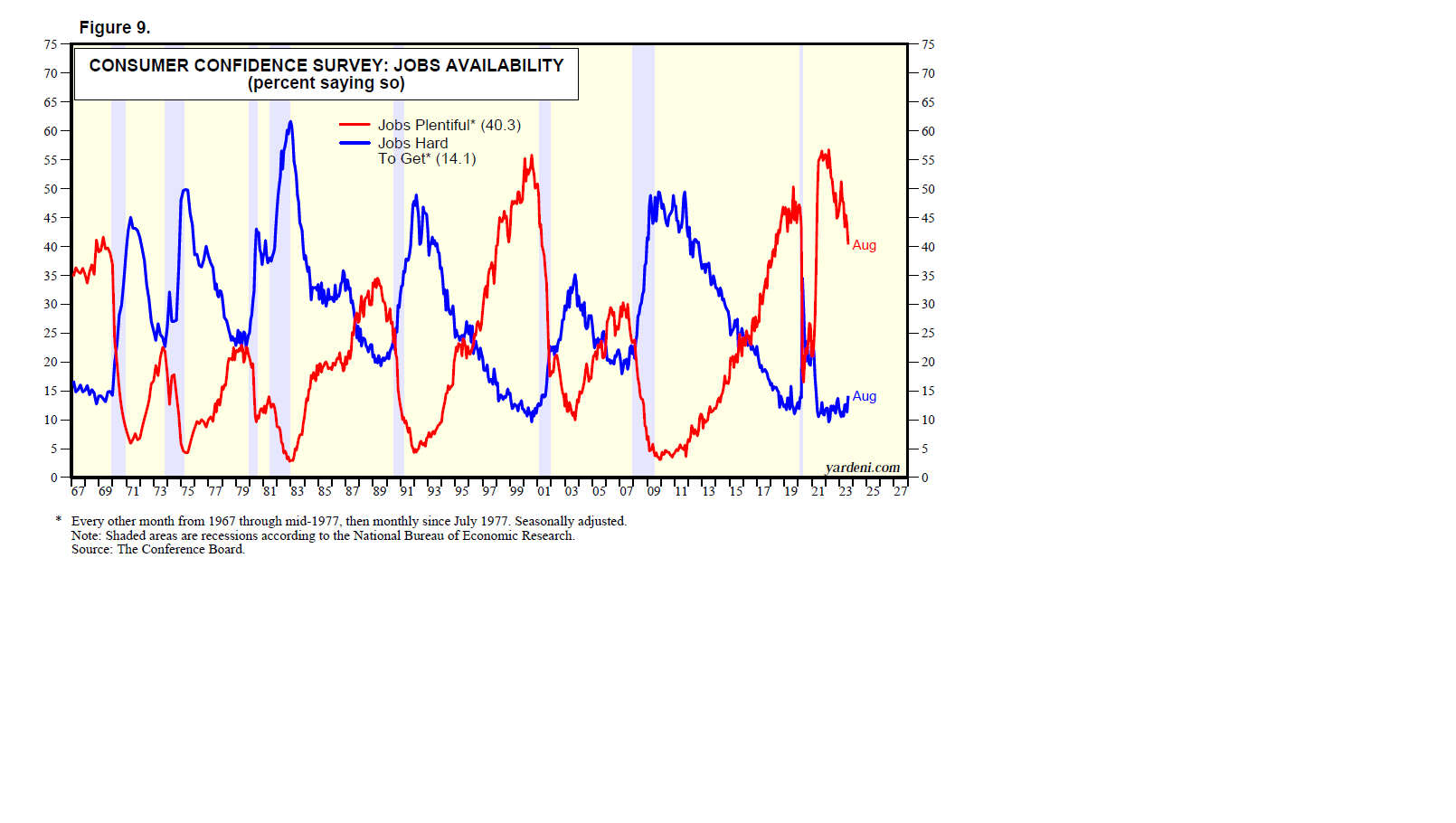

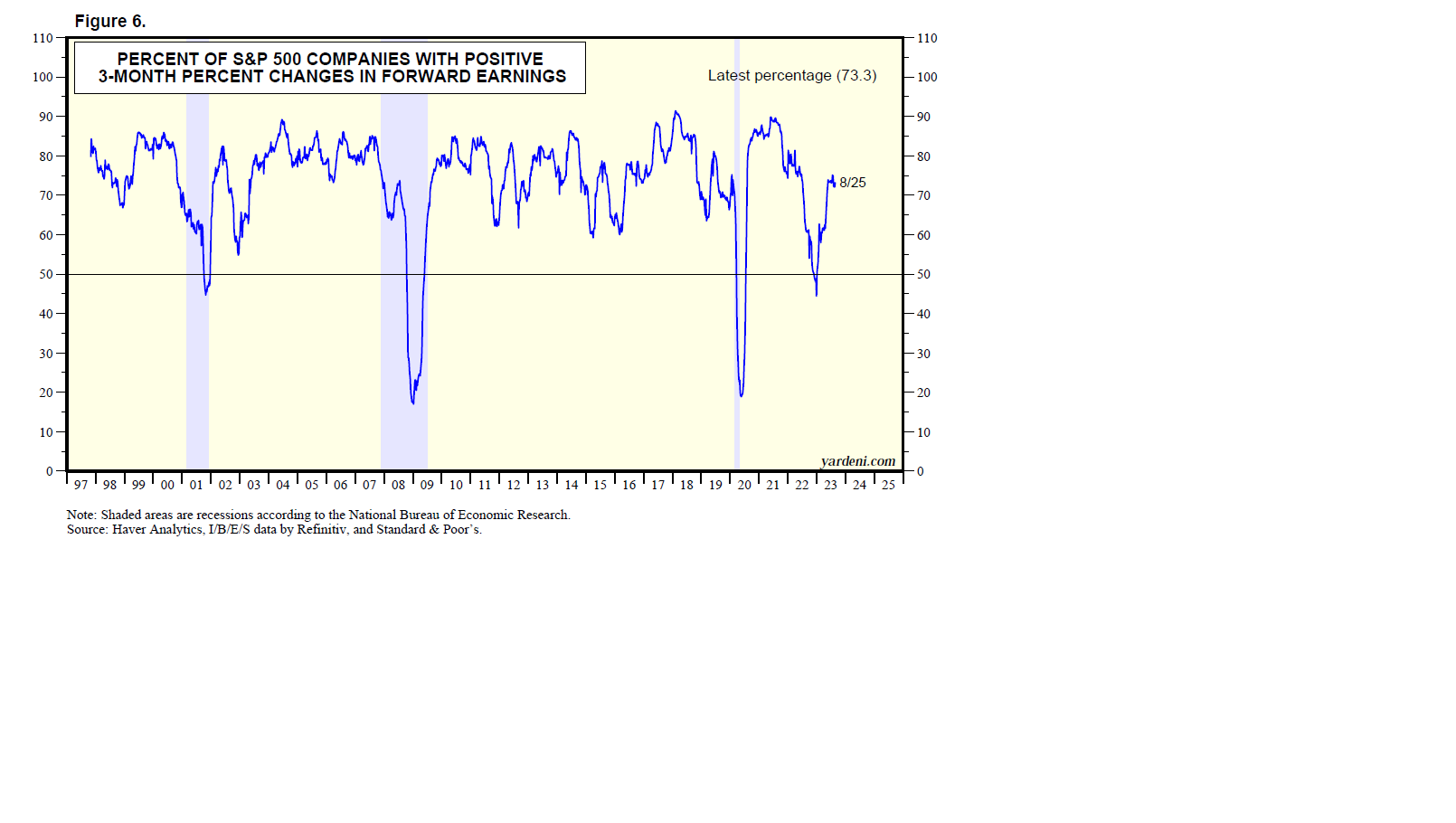

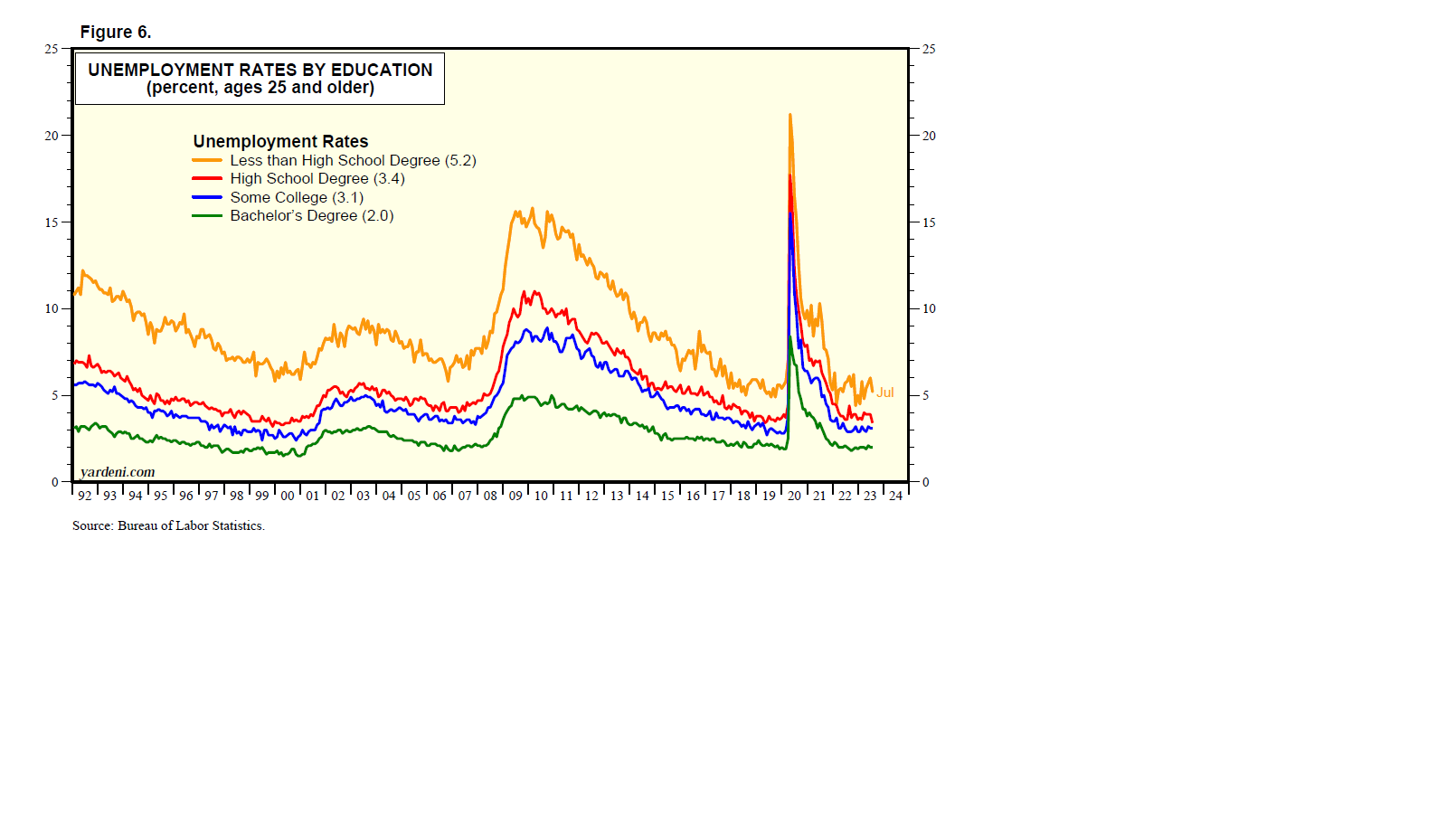

Indeed, during November, 40% of small business owners reported that they have job openings (Fig. 6). During October, there were 8.7 million job openings overall in the labor market versus 6.5 million unemployed that month. The labor force has increased 3.3 million during the first 11 months of this year. The household measure of employment is up 2.7 million over the same period.

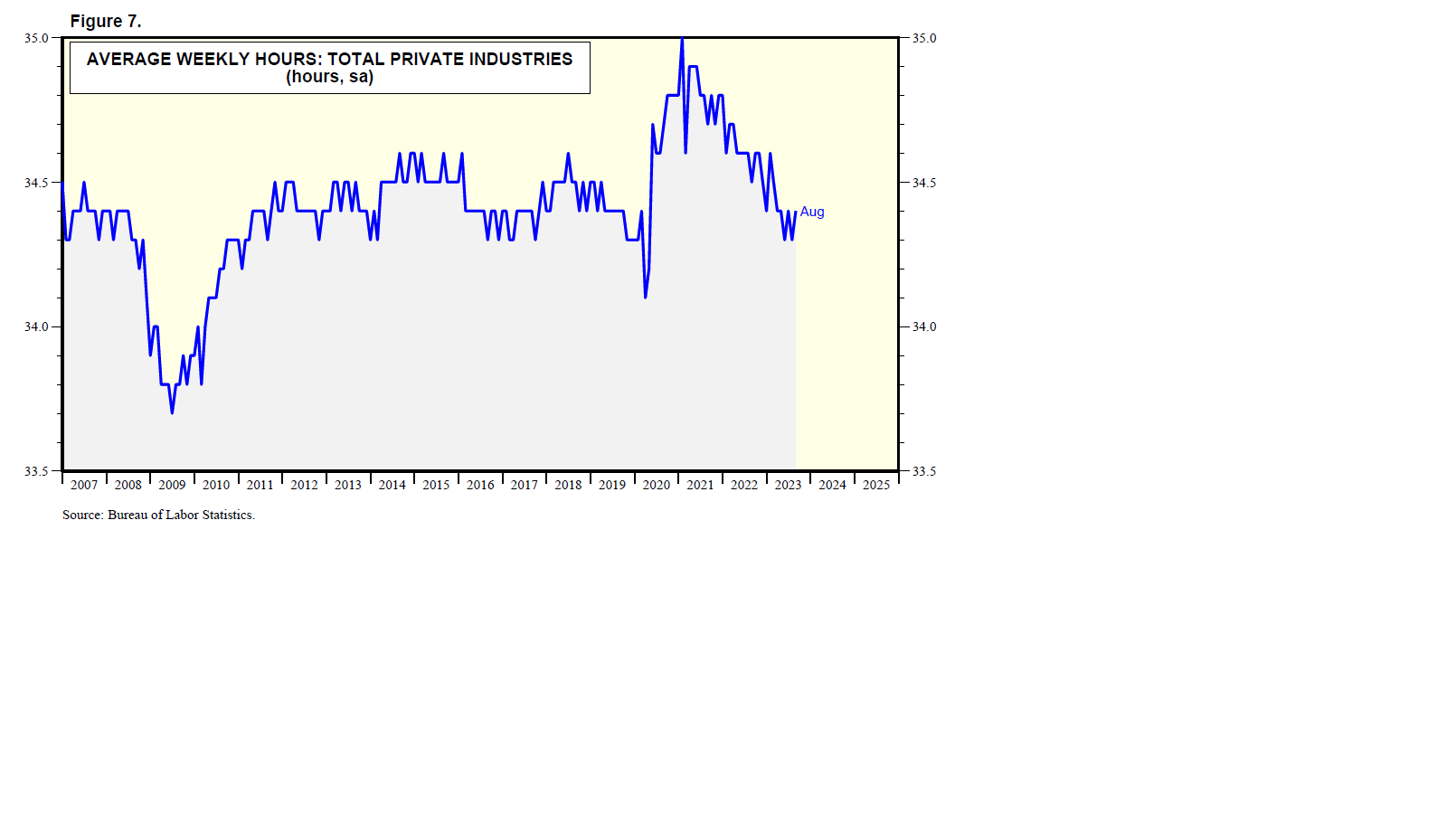

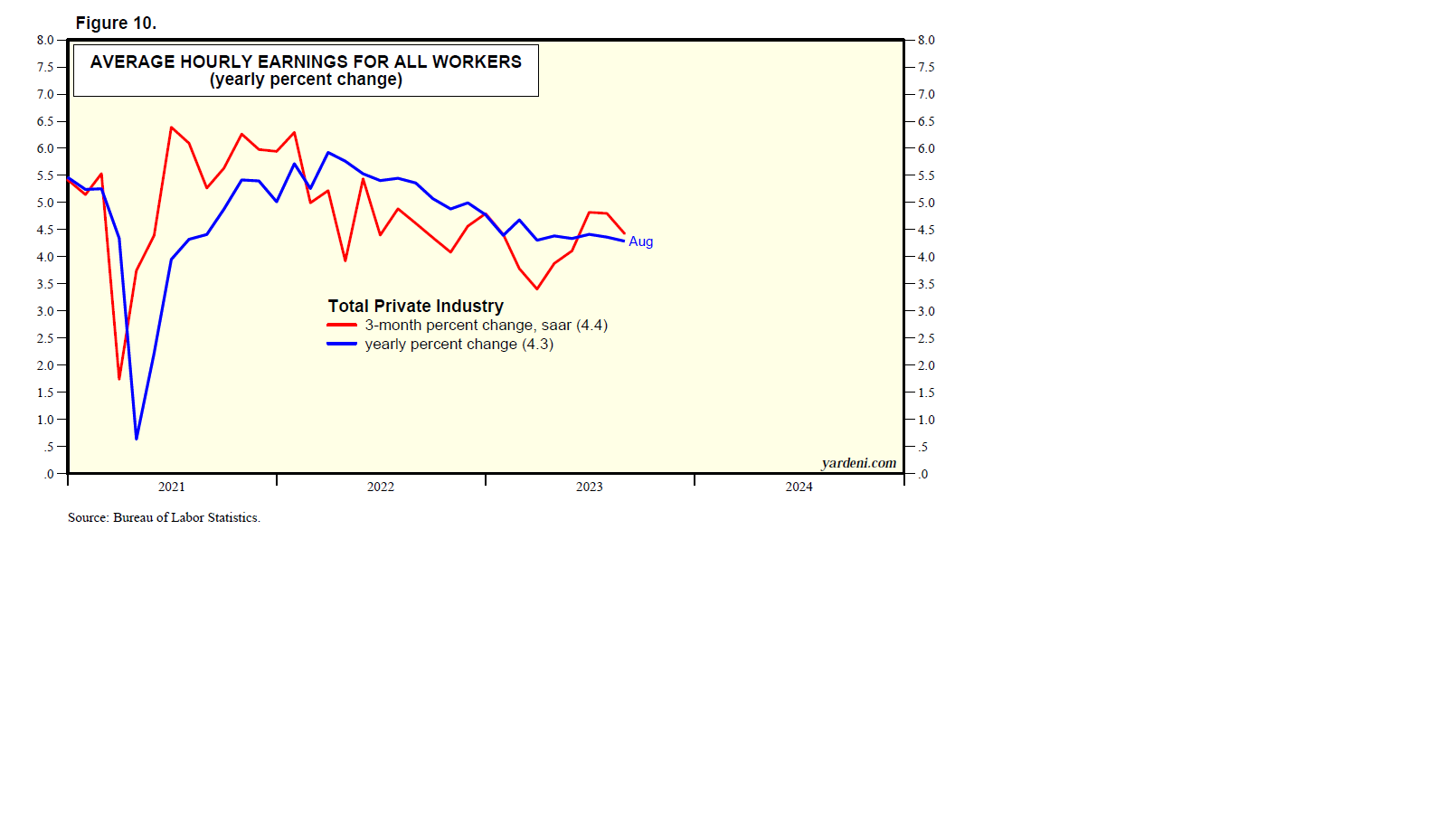

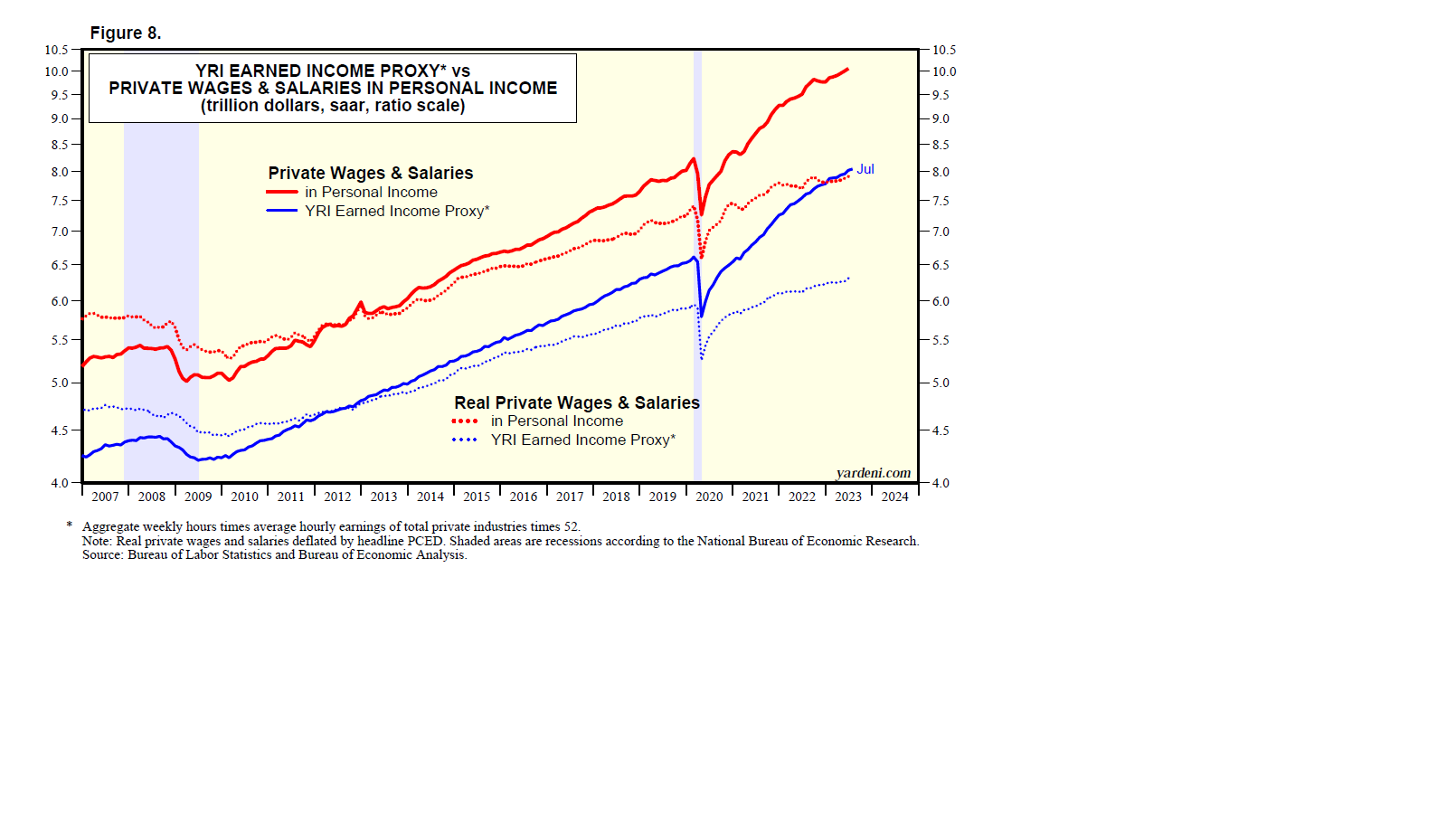

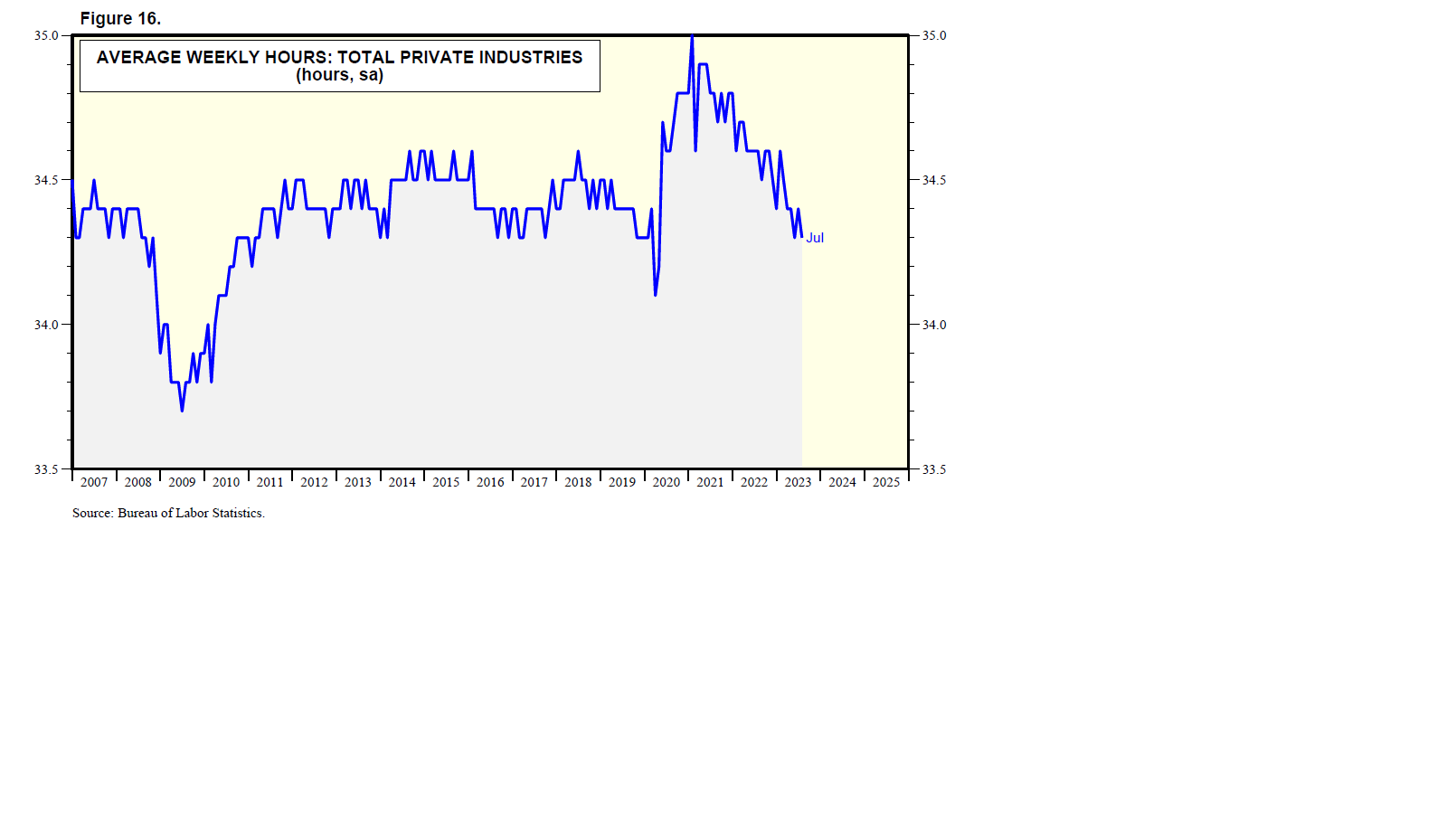

Pandemic-related excess saving certainly helped to boost consumer spending over the previous three years when unemployment was very high and real wages stagnated. But unemployment is low now (i.e., below 4.0% since February 2022), and real average hourly earnings is rising once again along its 1.4% annualized trendline that started in 1993 (Fig. 7).

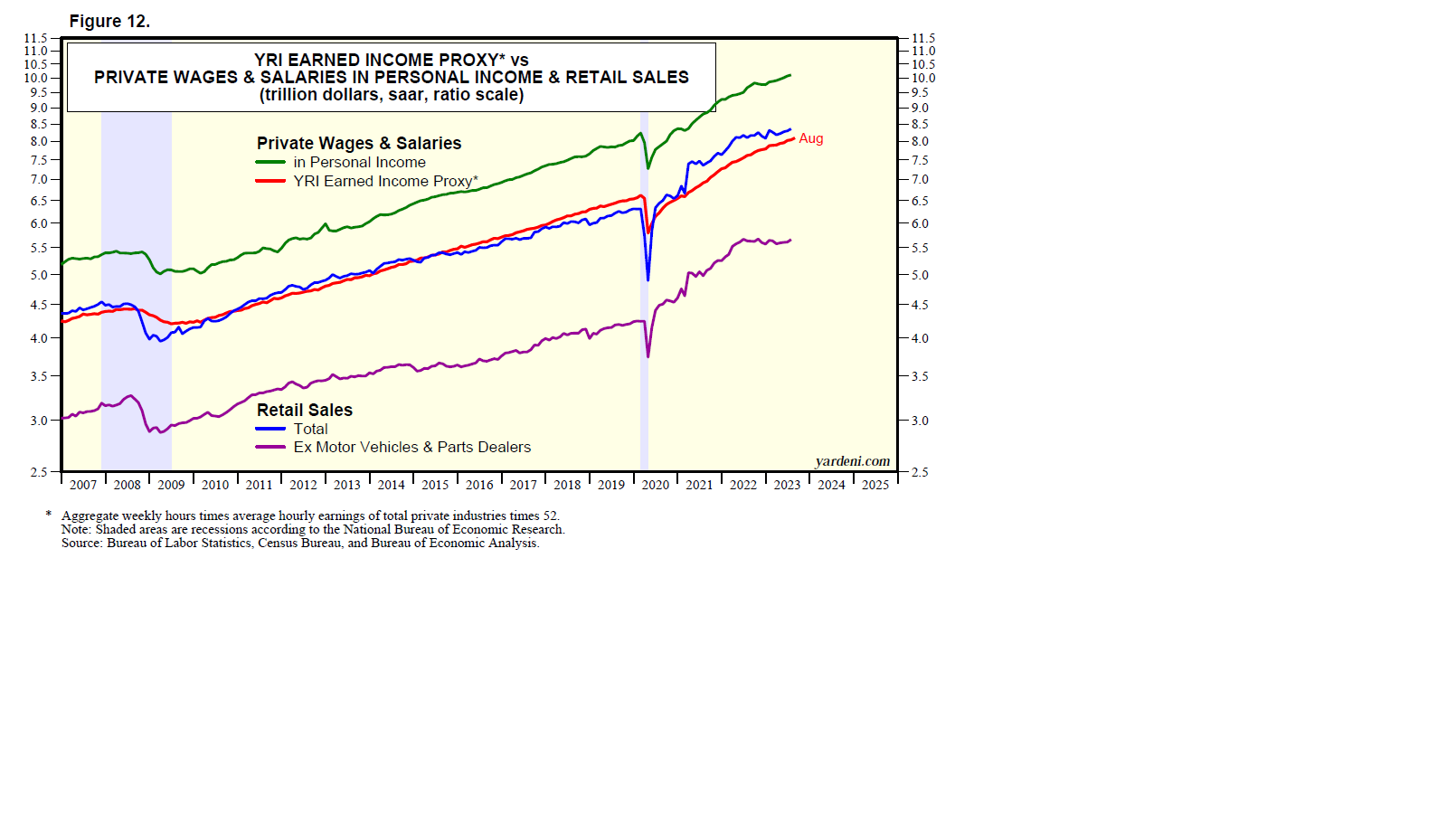

Both nominal and real wages & salaries in personal income and unearned personal income (including interest income, dividends, rents, and proprietors’ income) rose to record highs during October (Fig. 8). They probably did so again in November.

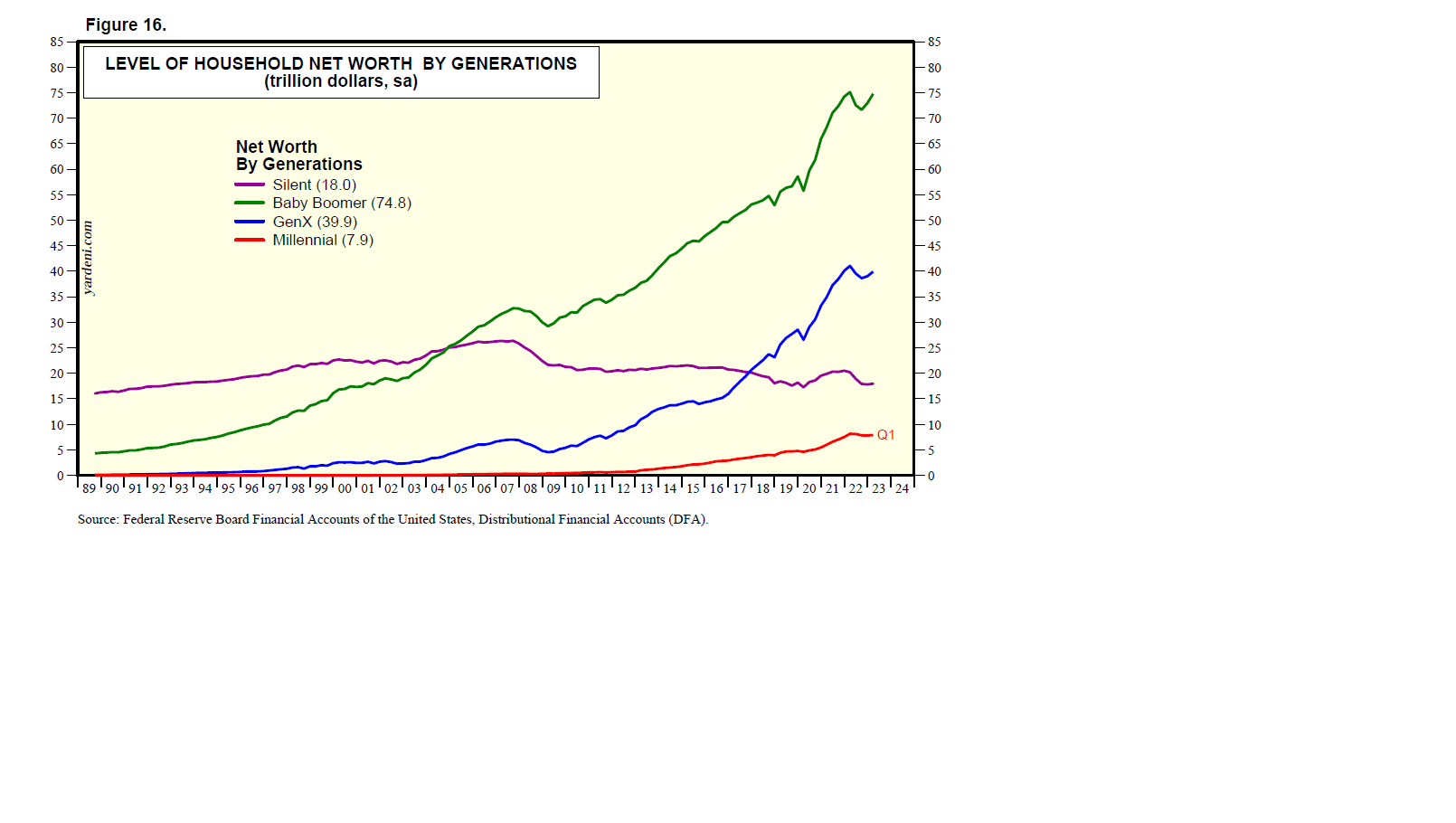

(3) Households are wealthy and liquid. The net worth of American households totaled a staggering record-high $151.0 trillion at the end of Q3-2023 (Fig. 9). Their portfolios are diversified in various asset holdings that all are at or near record highs (Fig. 10). There are certainly lots of liquid assets that might be sold to buy stocks and bonds when the Fed decides to lower short-term interest rates. A record $5.9 trillion is in money market mutual funds (MMMF) with a record $2.3 trillion in retail MMMFs (Fig. 11). Commercial bank deposits in M2 totaled $17.3 trillion during the December 12 week (Fig. 12).

There are 86 million households who own their own homes, and 40% of them have no mortgages. Many of these homeowners likely are Baby Boomers. They have mostly followed the advice of Star Trek’s Spock, who often said, “Live long and prosper.” Collectively, the generation held $73.1 trillion of net worth at the end of Q3. Boomers are likely to be among the main beneficiaries of record unearned income streams.

(4) Demand for labor is strong. From personal experience, we know that some of the Baby Boomers are providing some financial support to their young adult children. The Boomers are also eating at restaurants and traveling more often. They are visiting their health care providers more frequently to make sure that they live long enough to spend some of their retirement nest eggs.

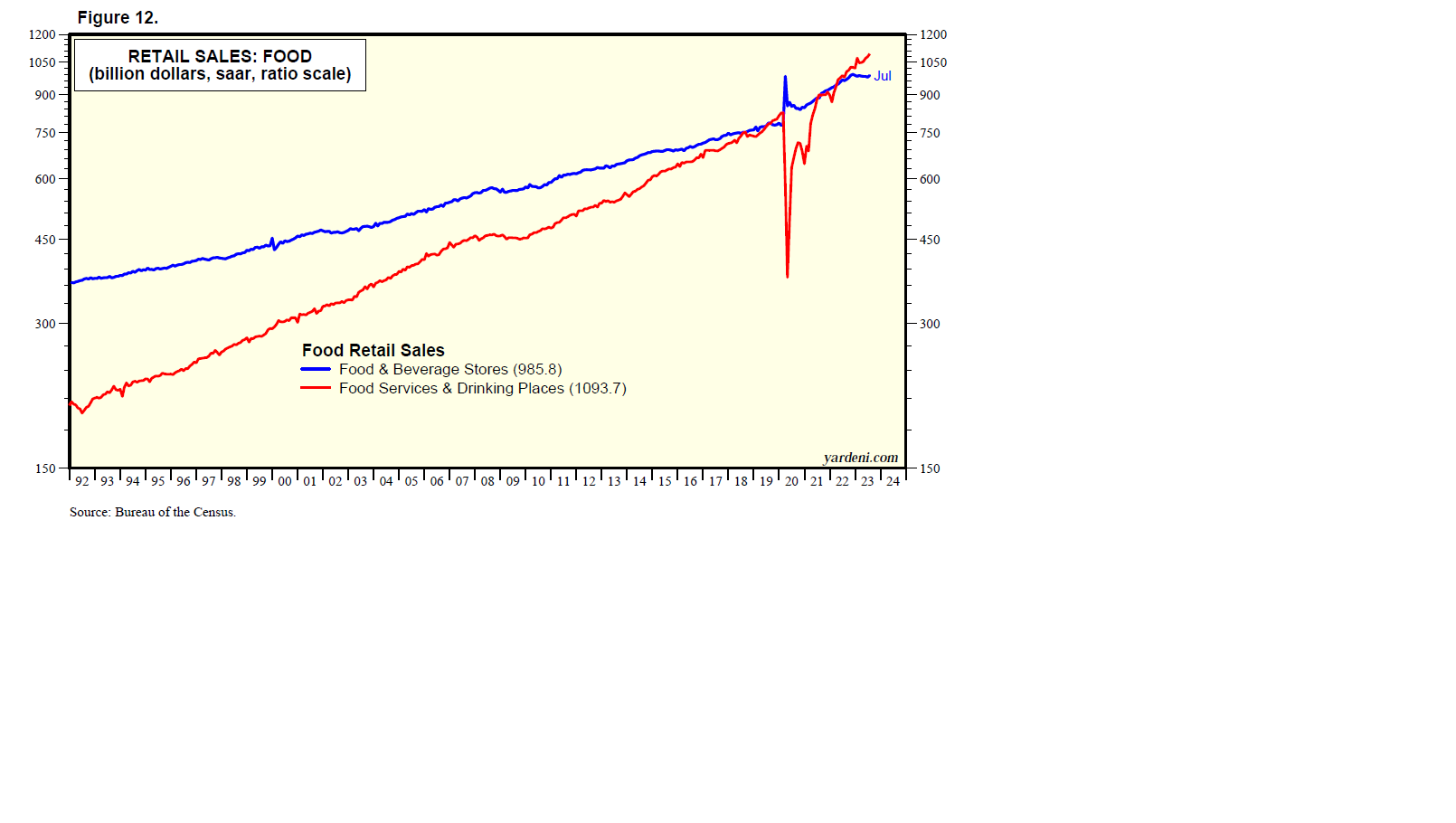

Not surprisingly, November’s better-than-expected retail sales was led by food services, which rose to yet another record high (Fig. 13). Employment continues to soar in the leisure & hospitality industry as well as in the health care sector.

(5) Onshoring boom is boosting capital spending. American and foreign manufacturing companies clearly are onshoring to the US. Supply-chain disruptions during the pandemic and growing geopolitical tensions between the US and China have stimulated the onshoring rush. So has a shortage of workers in China.

The onshoring boom and the federal government’s increased spending on public infrastructure are boosting new orders for construction machinery, which is up 30.5% over the past 24 months through October (Fig. 14). Onshoring and infrastructure investment also explain why construction employment rose to yet another record high of 8.0 million during November despite the recession in single-family housing starts.

Construction spending on manufacturing facilities is soaring because of the increase in onshoring partly owing to federal incentives. In current dollars, it is up a whopping 71.6% and 136.8% on one-year and two-year bases (Fig. 15).

(6) Housing is all set for a recovery. The plunge in mortgage interest rates since early November undoubtedly will boost new and existing home sales. That should give a boost to housing-related retail sales on appliances, furniture, and furnishings. The rolling recessions in housing and housing-related retailing should turn into rolling recoveries for both.

(7) Corporate cash flow is at a record high. The economy’s resilience can also be attributed to the awesome ability of US corporations to generate cash flow. It totaled a record $3.4 trillion (saar) during Q3-2023. That’s despite the pressure on companies’ profit margins coming from high labor costs and higher interest rates over the past couple of years. Corporate cash flow is up 4.1% y/y, with tax-reported depreciation up 6.9% and undistributed profits down 3.3%. The latter has been relatively flat since Q3-2009.

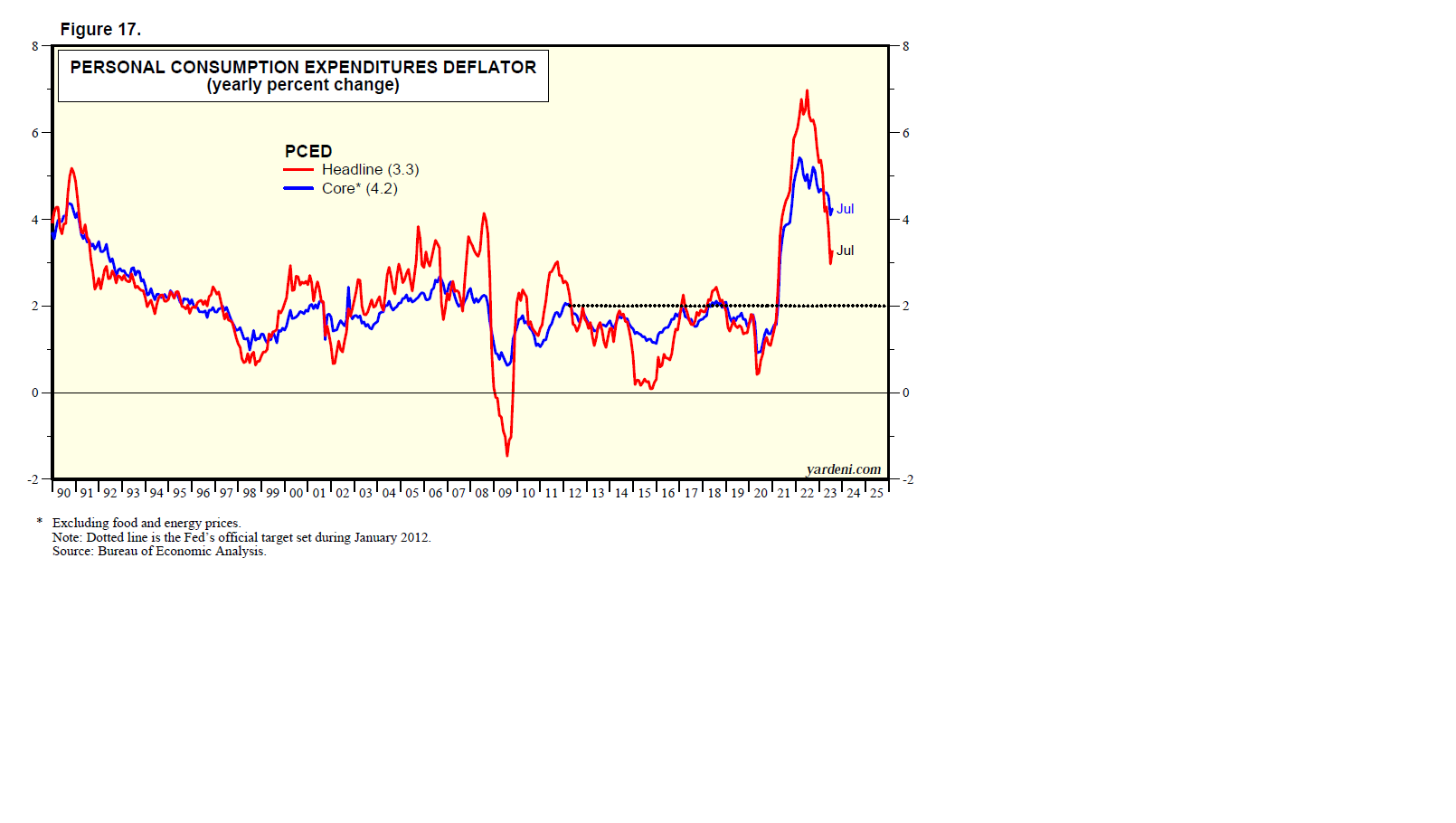

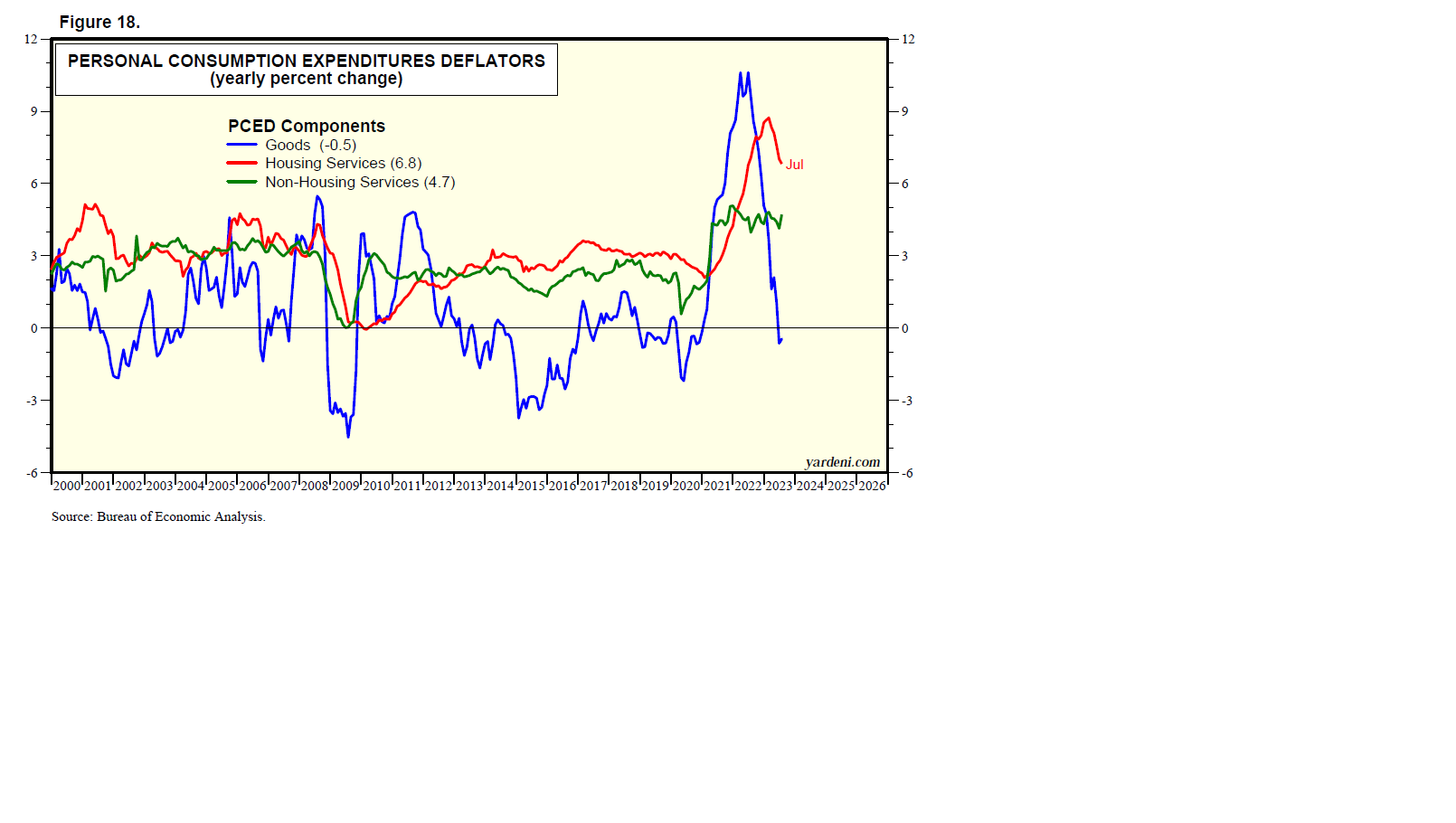

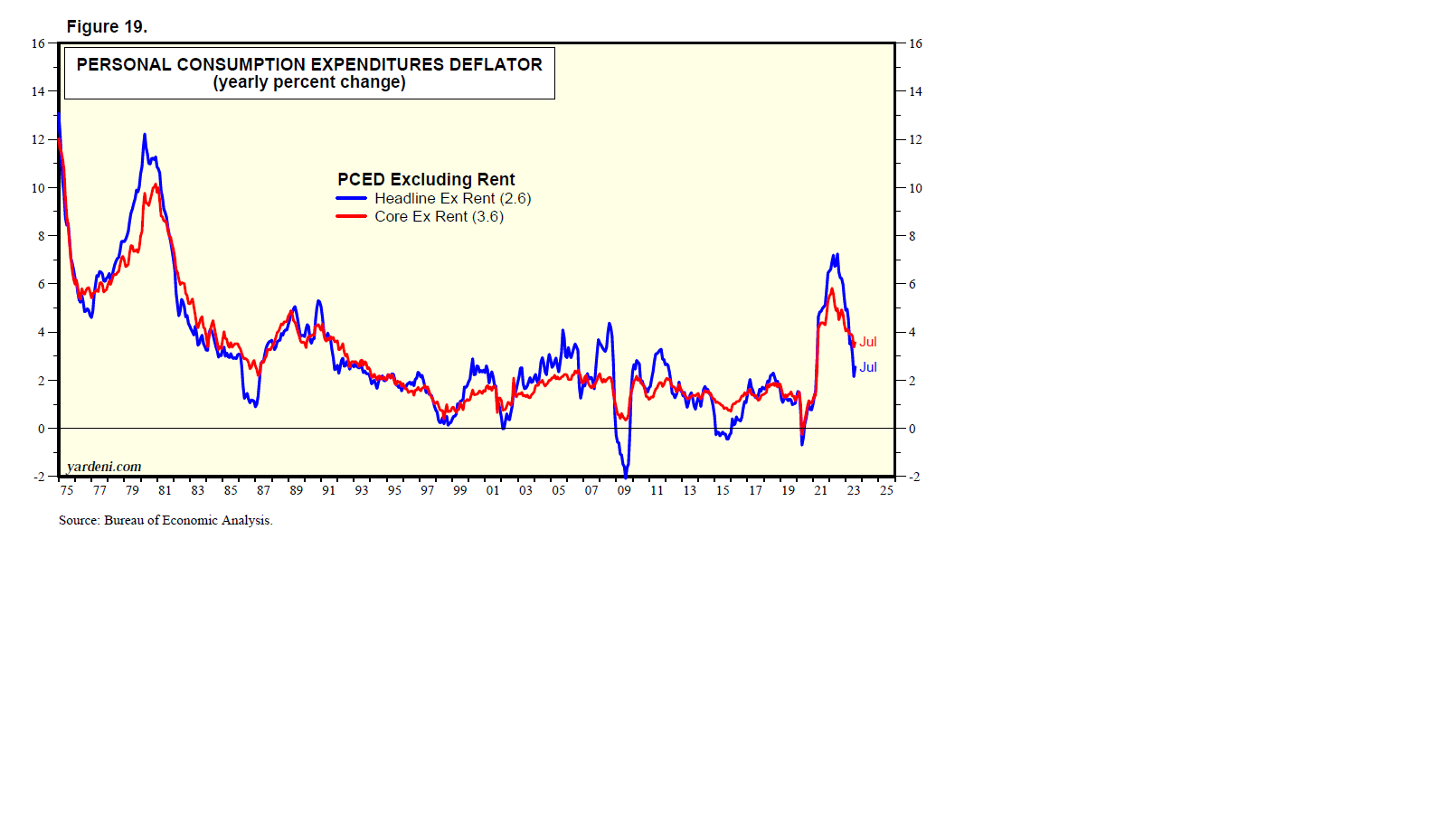

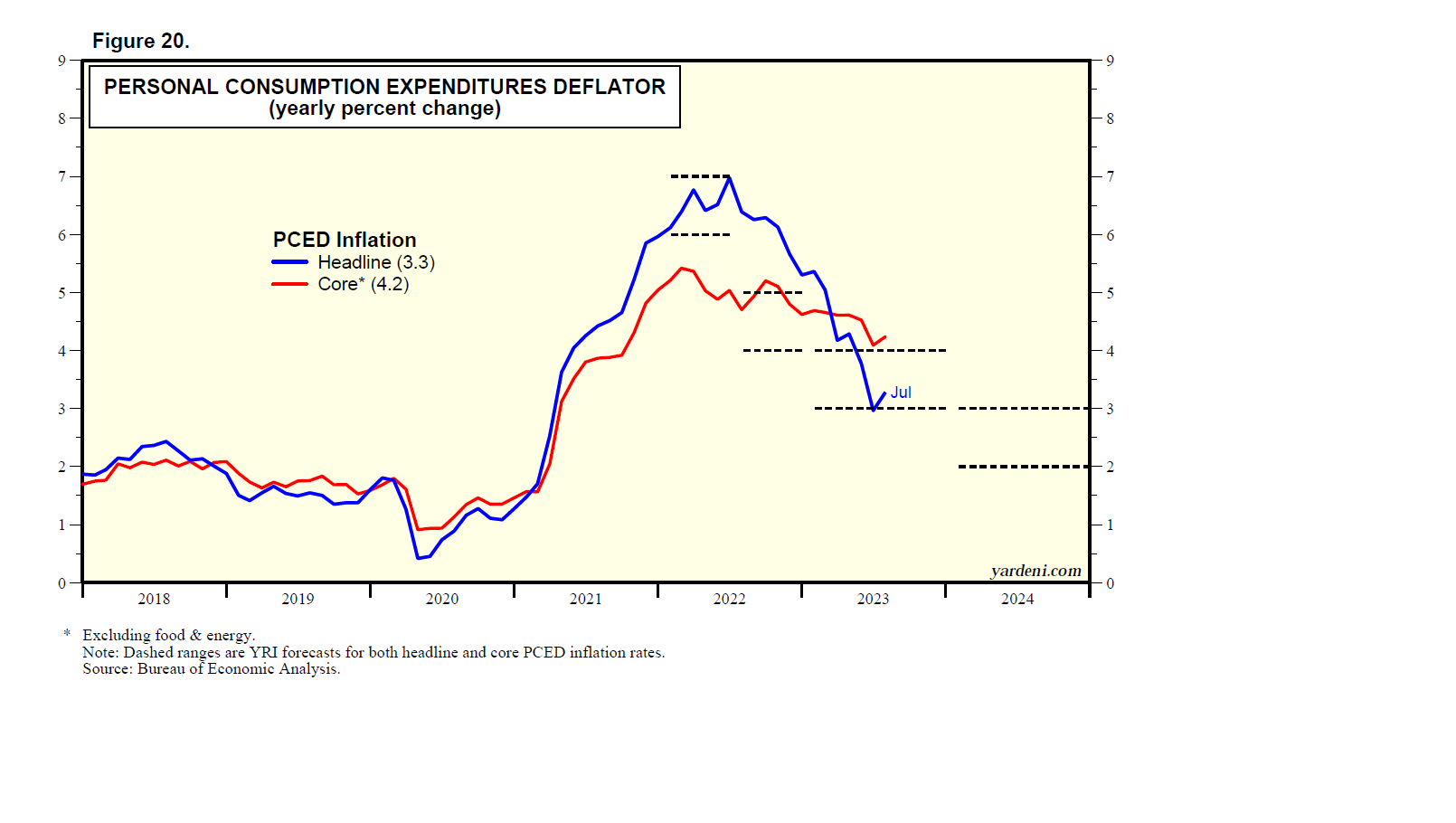

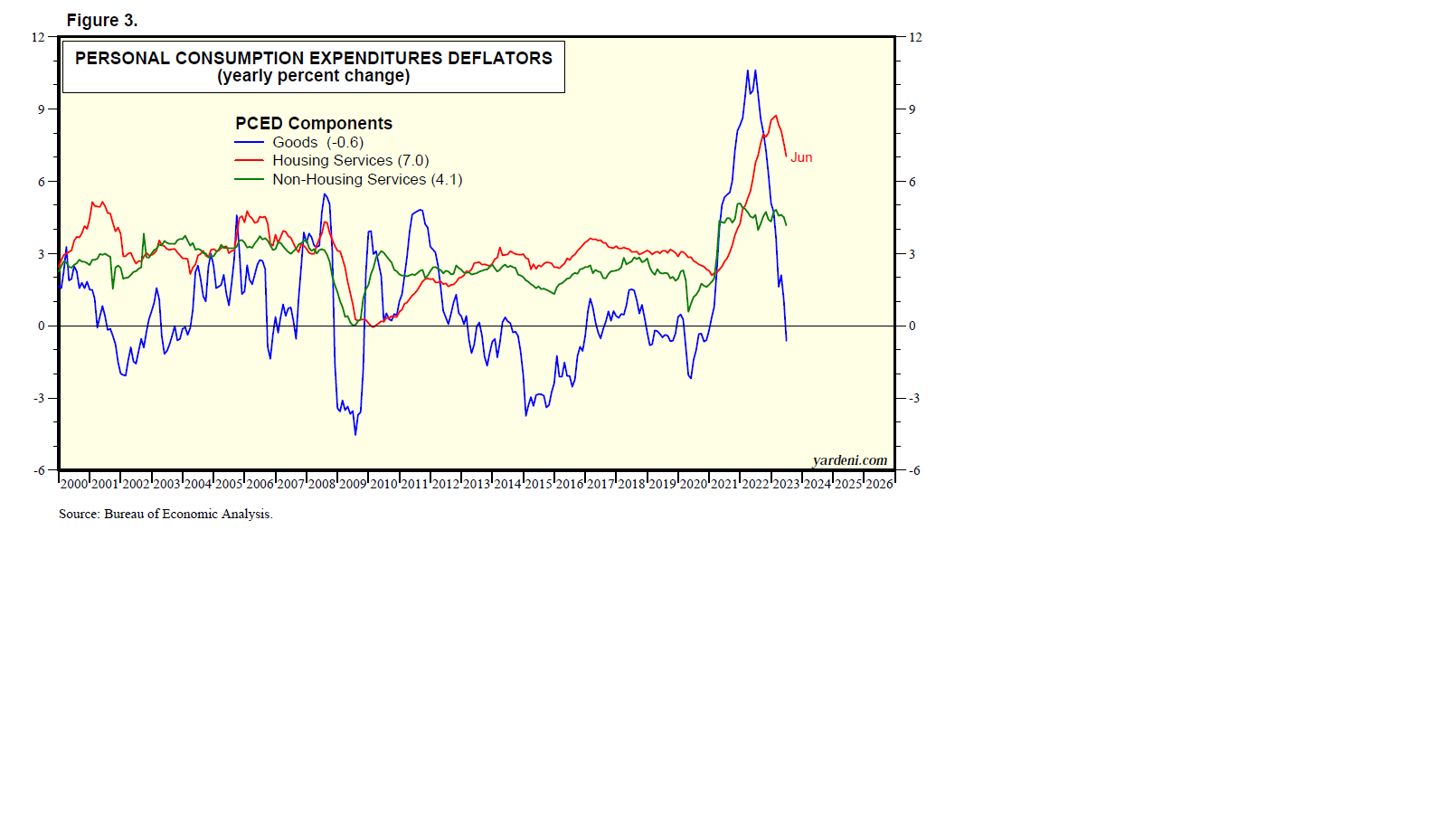

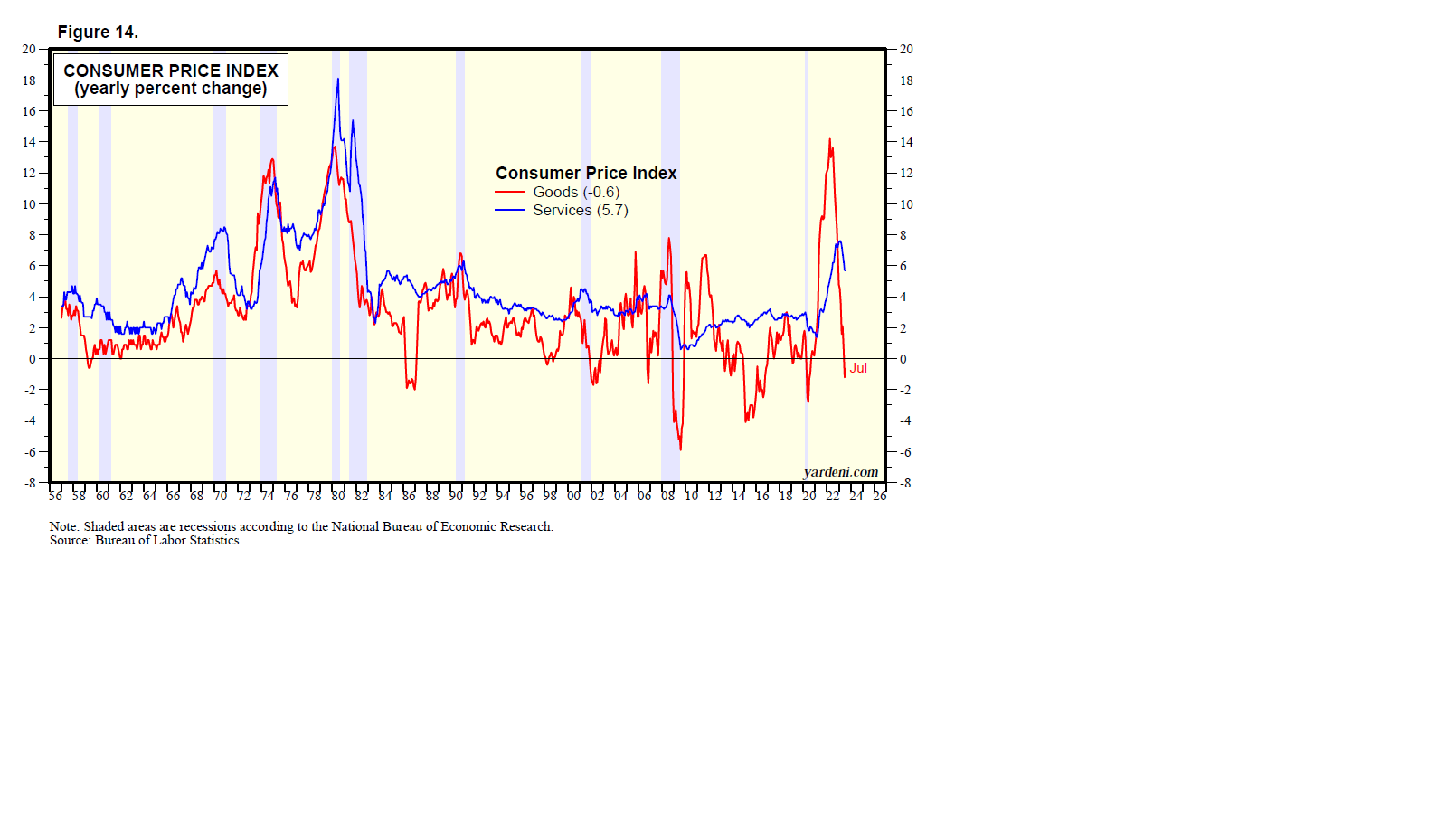

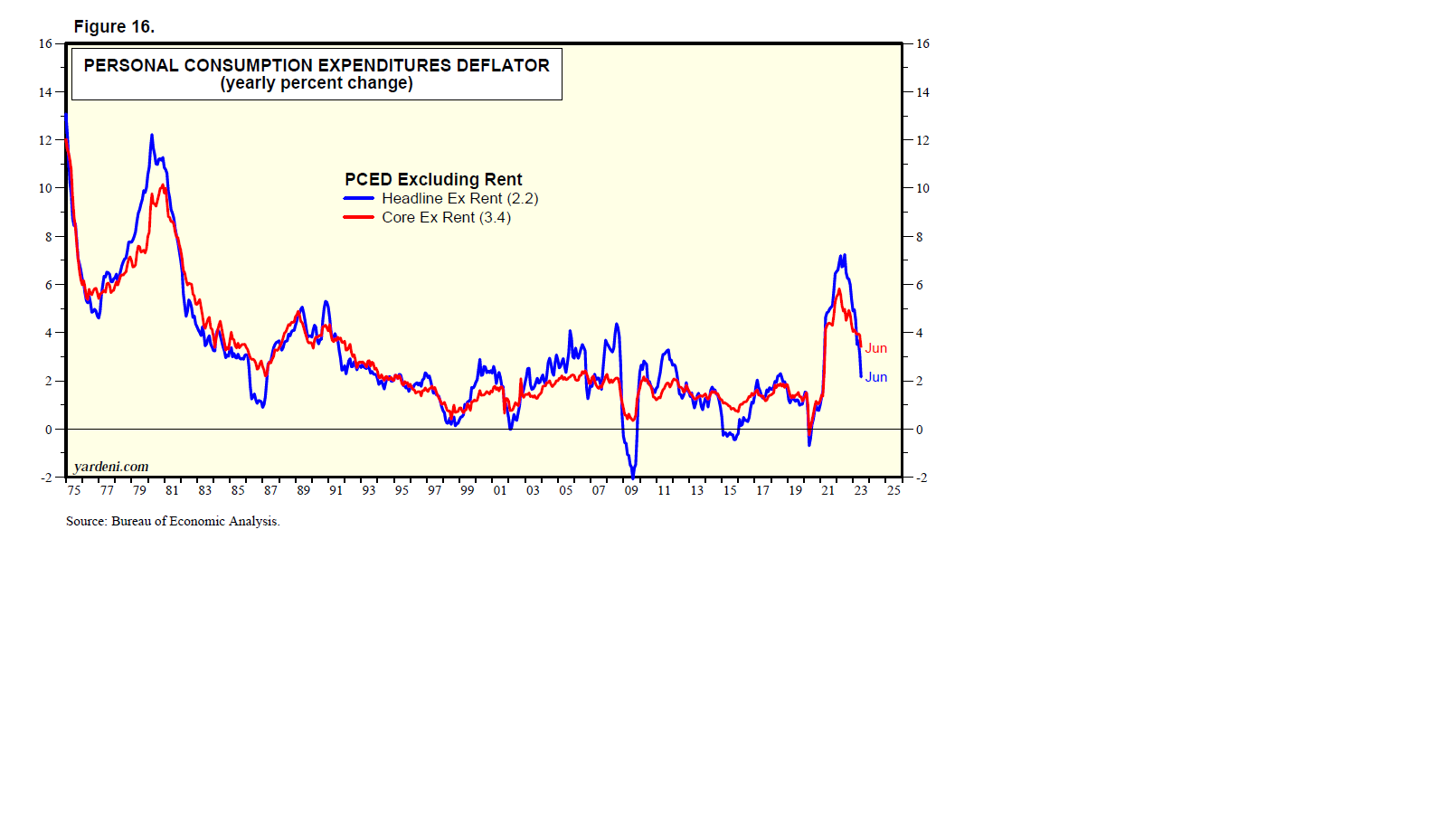

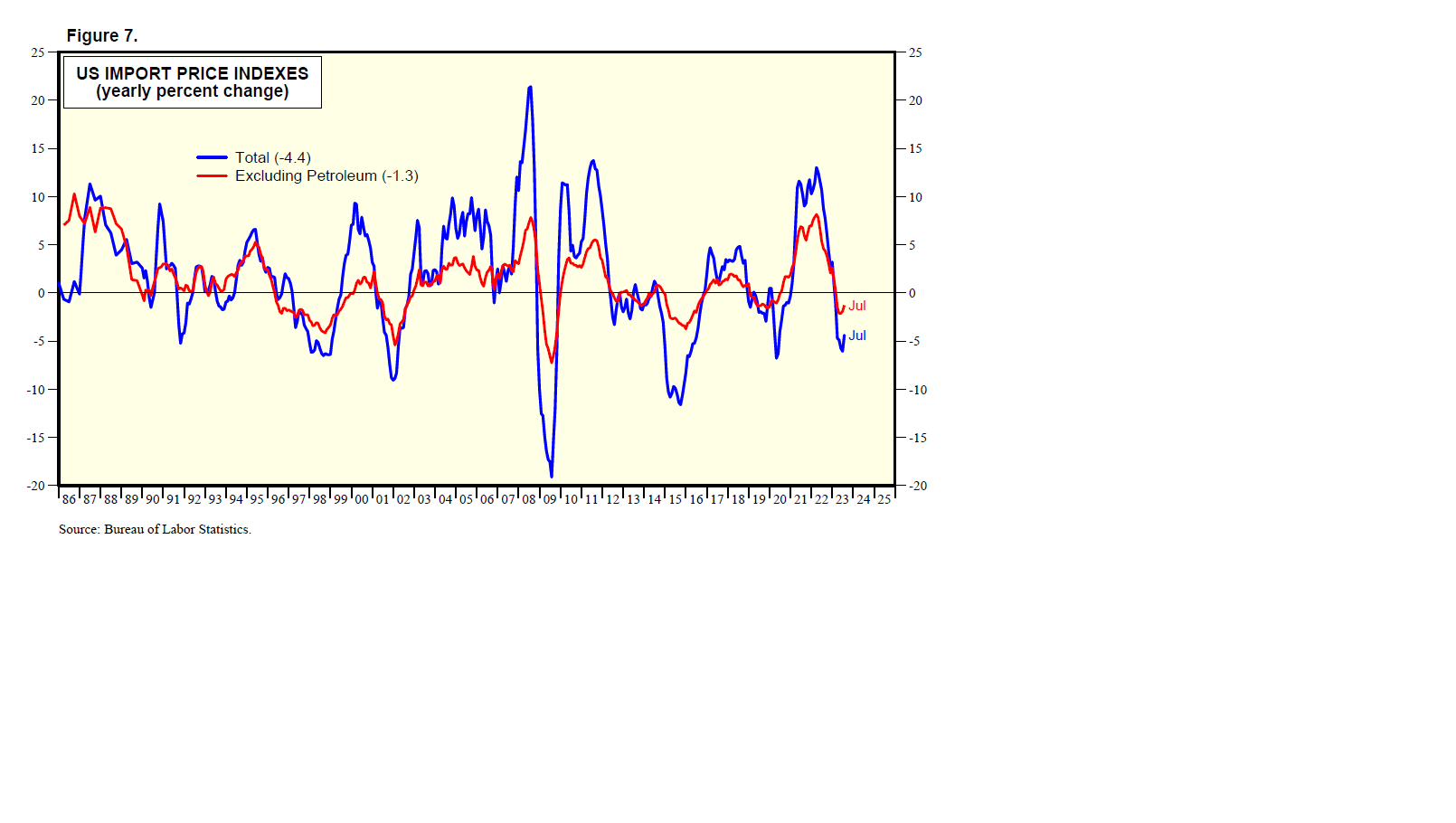

(8) Inflation is turning out to be transitory. There can be no debate about the transitory nature of goods inflation since H2-2020. It was back down to 0.0 y/y during November (Fig. 16). It turned out to be mostly attributable to the shocks and aftershocks of the pandemic, which have been dissipating since the end of the pandemic.

Almost all the inflationary pressures on durable goods and many nondurable goods stemmed from the pandemic-related supply-chain disruptions, which can be seen in the Global Supply Chain Pressure Index compiled by the Federal Reserve Bank of New York. The index jumped from 0.1 in October 2020 to peak at 4.3 in December 2021. It has plunged since then, returning to 0.1 in November (Fig. 17). The PPI inflation rate for transportation & warehousing has followed suit (Fig. 18).

Now that the goods inflation shock is behind us, the services inflation shock is showing signs of dissipating. We expect it will do just that in 2024.

(9) The High-Tech Revolution is boosting productivity. Companies are allocating more of their capital spending budgets to technology hardware and software to boost their productivity in response to chronic labor shortages. As a result, production of high-tech equipment and spending on software are at all-time highs.

We believe that a major cycle in productivity growth started at the end of 2015, when it bottomed at 0.5% (based on the 20-quarter average) and rose to 1.8% during Q3-2023 (Fig. 19). We expect productivity growth will peak around 4.0% by the end of the decade.

(10) Leading indicators are mostly misleading. What about all those leading indicators that have been signaling an impending recession since last year? We’ve often explained why they are misleading. For example, inverted yield curves in the past have anticipated that the Fed’s tightening would break something in the financial system, causing a credit crunch and a recession, that’s not always the case. There was a mini-banking crisis in March of this year. But it was contained by the Fed so had few systemic ripple effects.

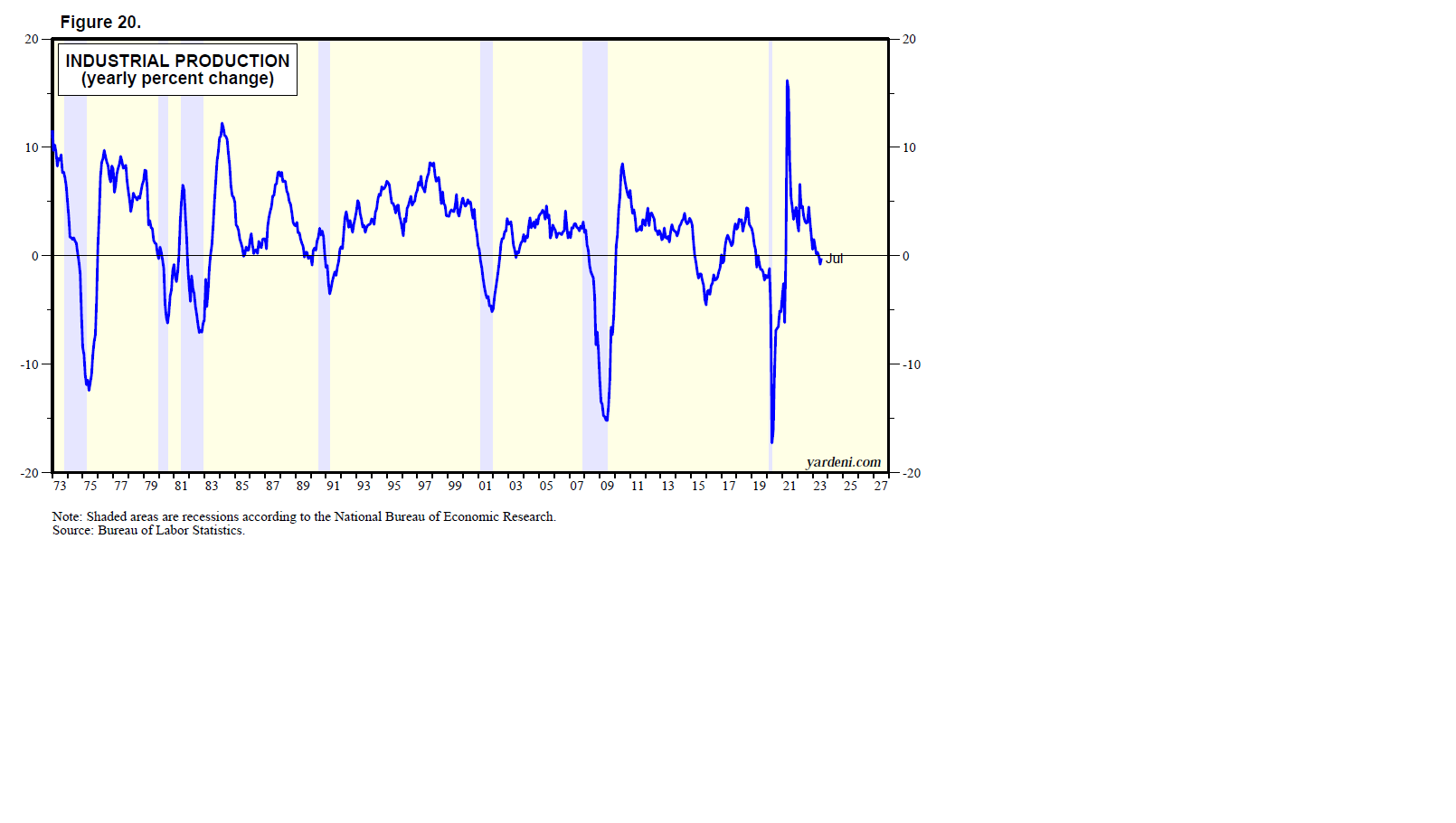

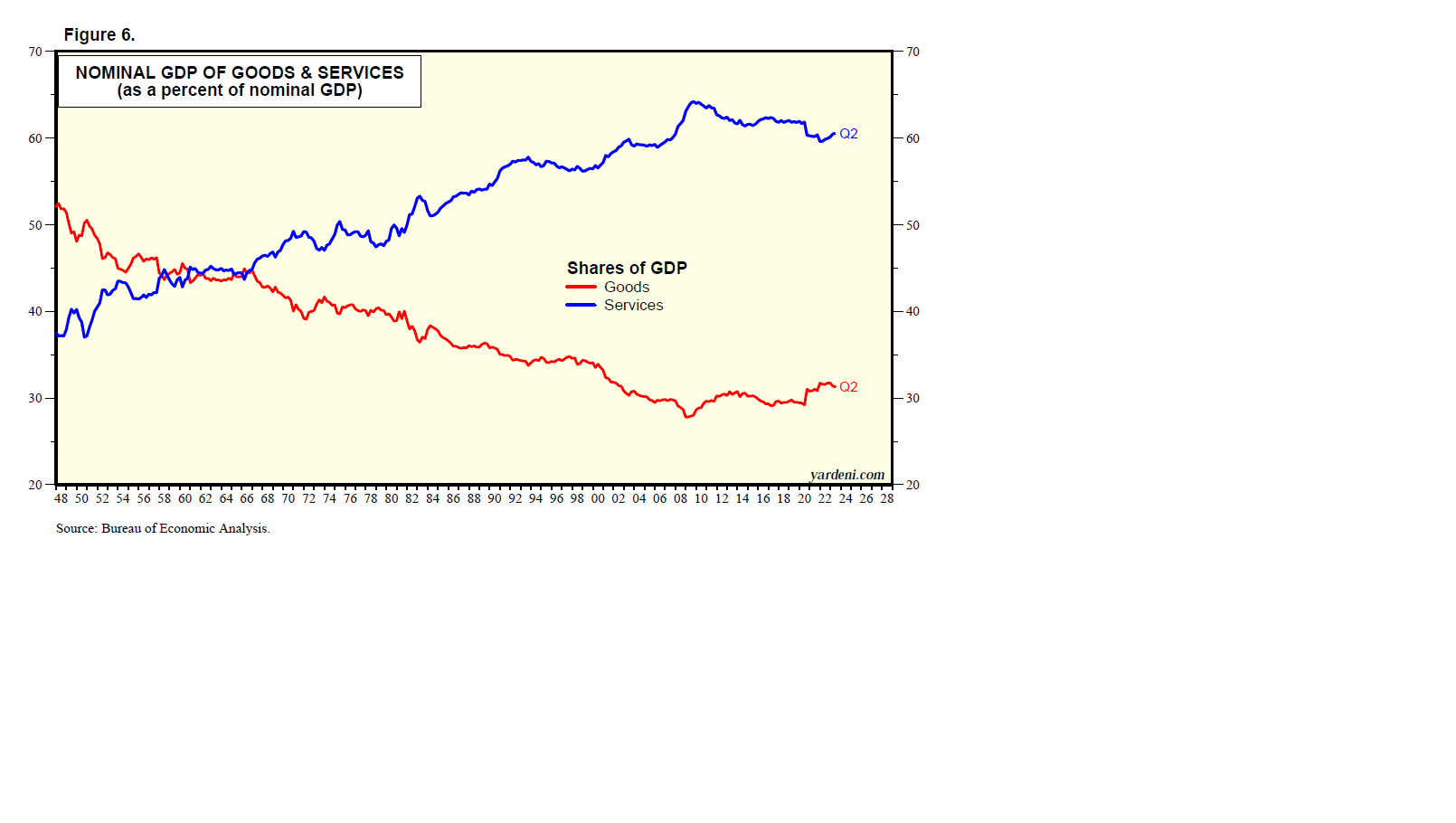

The LEI has misfired its recession signals because its composition is biased toward predicting the goods sector more than the services sector of the economy. There has been a rolling recession in the goods sector, but it has been more than offset by strength in services, nonresidential private and public construction, and high-tech capital spending.

(11) The rest of the world’s challenges should remain contained. Also booming is industrial production of defense, which is likely to continue rising to new record highs given the geopolitical turmoil around the world. The wars between Russia and Ukraine and between Israel and Gaza should remain contained regionally. China’s economic woes reduce the chances that China will invade Taiwan. Nevertheless, these geopolitical hot spots will boost defense spending among the NATO members.

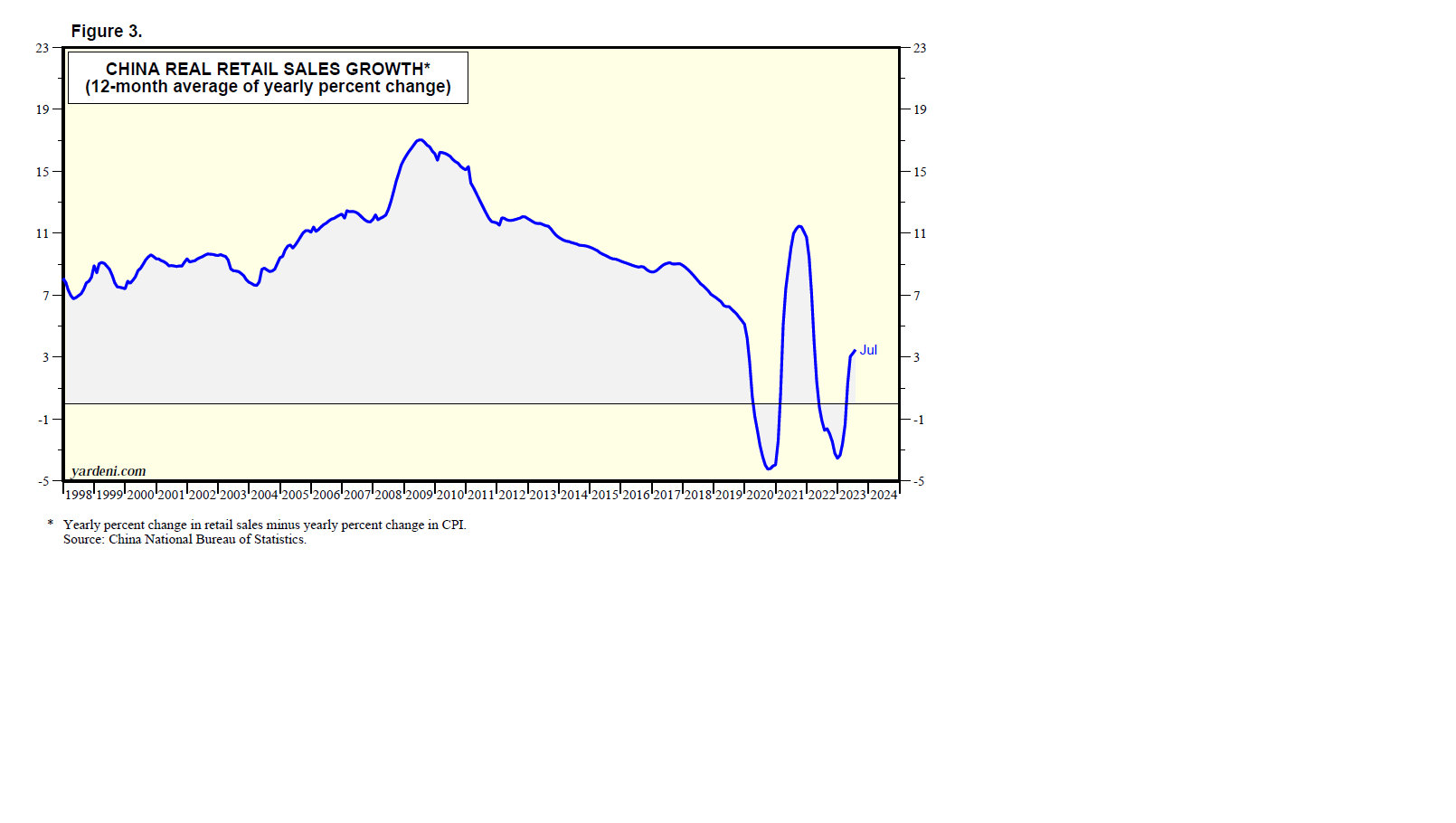

The bursting of China’s property bubble should continue to weigh on global economic growth and commodity prices. China will remain a major source of global deflationary pressures. Europe is in a shallow recession and should recover next year as the European Central Bank lowers interest rates.

(12) The Roaring 2020s will broaden the bull market. At last week’s FOMC meeting, Fed Chair Jerome Powell and his colleagues pivoted toward the soft-landing scenario, which is also known as “immaculate disinflation.” In their Summary of Economic Projections (SEP), they projected three 25bps cuts in the federal funds rate next year, up from September’s two rate cuts. They are starting to recognize that inflation can subside without a recession. We think this is happening because China is having a recession and effectively exporting goods deflation to the US. In addition, technology-driven productivity growth is making a comeback, in our opinion.

The current bull market started on October 12, 2023. It received a big boost when AI-related stocks took off late last year. OpenAI launched ChatGPT on November 30, 2022. We believe that date is when the stock market first started to discount our Roaring 2020s scenario. At first, the bull market was narrowly based, but it since has been broadening to include more sectors and industries. We believe that reflects investors’ realization that the beneficiaries of the Roaring 2020s theme aren’t just the companies that make technology but also those that use it to boost their productivity—i.e., companies generally whatever their industry may be.

Strategy IV: How About All That Government Debt? The bears’ latest and most compelling talking point is that federal government deficits are out of control. Federal government spending is growing rapidly, led by outlays on net interest paid. They totaled a record $716.7 billion over the past 12 months through November. That’s an unsettling development, for sure.

However, keep in mind the flip side of high interest rates: They represent a big windfall for households that receive interest income, which has increased significantly. In addition, the spending bills passed by Congress last year will continue to boost construction spending on public infrastructure, which is at a record high, and continue to stimulate onshore construction of manufacturing facilities. Better-than-expected productivity-led growth would certainly help to reduce the mounting burden of the federal debt.

Nevertheless, the federal government’s need to finance the huge deficit could cause an oversupply of Treasury bonds relative to demand, which could set off a debt crisis. And that certainly could trip up the Roaring 2020s scenario. However, investors realize that nothing will be done to fix the problem in 2024 because it is an election year. Meanwhile, inflation is falling, the Fed is pivoting toward lowering interest rates, and the economy remains resilient.

Movie. “Archie” (+ +) (link) is a British television drama series about actor Cary Grant. He was born into poverty in Bristol in 1904 as Archibald Leach before becoming a star in Hollywood with the new stage name. He was very successful as an actor, playing lead roles in several hit movies. However, his personal life was a mess, as evidenced by his five marriages and four divorces. He suffered greatly from the emotional pain of his childhood. He recognized that he was trapped in the past but couldn’t escape it. However, near the end of his life, he had a baby girl with his fourth wife, Dyan Cannon; it was then that he finally found peace and great satisfaction in the role of good dad.

Drugs, China & AI

December 14 (Thursday)

Check out the accompanying pdf and chart collection.

Executive Summary: The S&P 500 sector with the brightest 2024 earnings growth outlook is none other than Health Care, with a share price index that’s a deep underperformer this year, Jackie reports. One of its component industries accounts for much of both this year’s stock price pain and next year’s projected earnings gains—pharmaceuticals. Three drug makers in particular appear bound for standout earnings next year. … Also: China’s government is not doing what it takes to overcome its formidable economic challenges. … And in today’s Disruptive Technologies segment: one tech veteran’s advice for working with AI, warts and all.

Health Care: Hoping for a 2024 Recovery. The S&P 500 Health Care sector stock price index has been sickly all year, posting negative ytd performance through Tuesday’s close. Tough y/y comparisons to Covid-boosted-earnings in 2022 hurt some drug companies. Others fell off patent cliffs. Pharmacy benefit managers have come under pressure from new competition from the online pharmacy services being offered by Amazon and billionaire entrepreneur Mark Cuban. The makers of weight-loss drugs were among the few pharmaceutical manufacturers to have a banner year.

As the new year begins, analysts are optimistic about the 2024 earnings prospects for companies in the Health Care sector. In fact, the sector’s earnings growth next year is expected to trump that of any other S&P 500 sector—including Technology.

Let’s dive into what hurt Health Care names this year and what stands to help the sector in the year ahead:

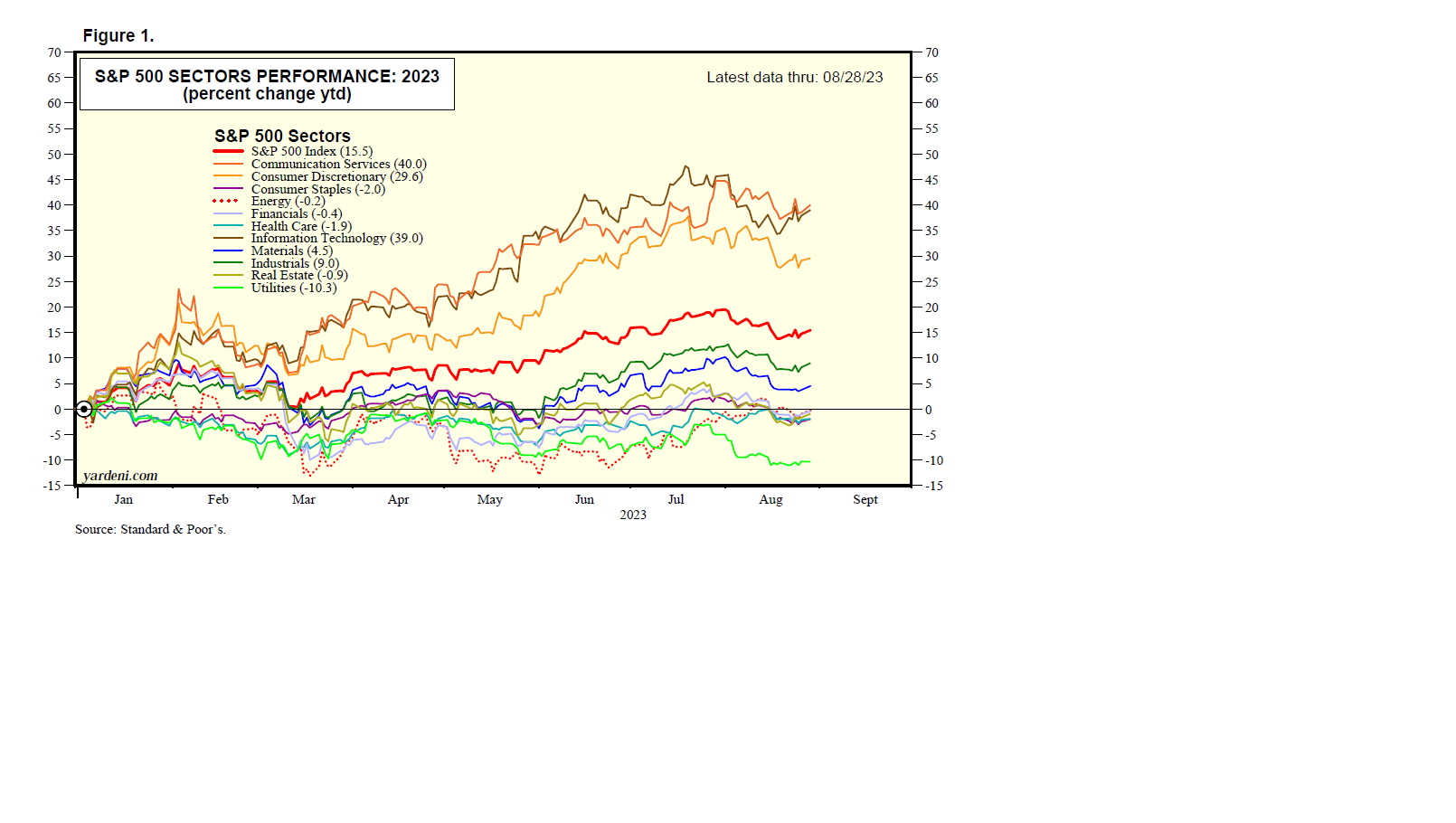

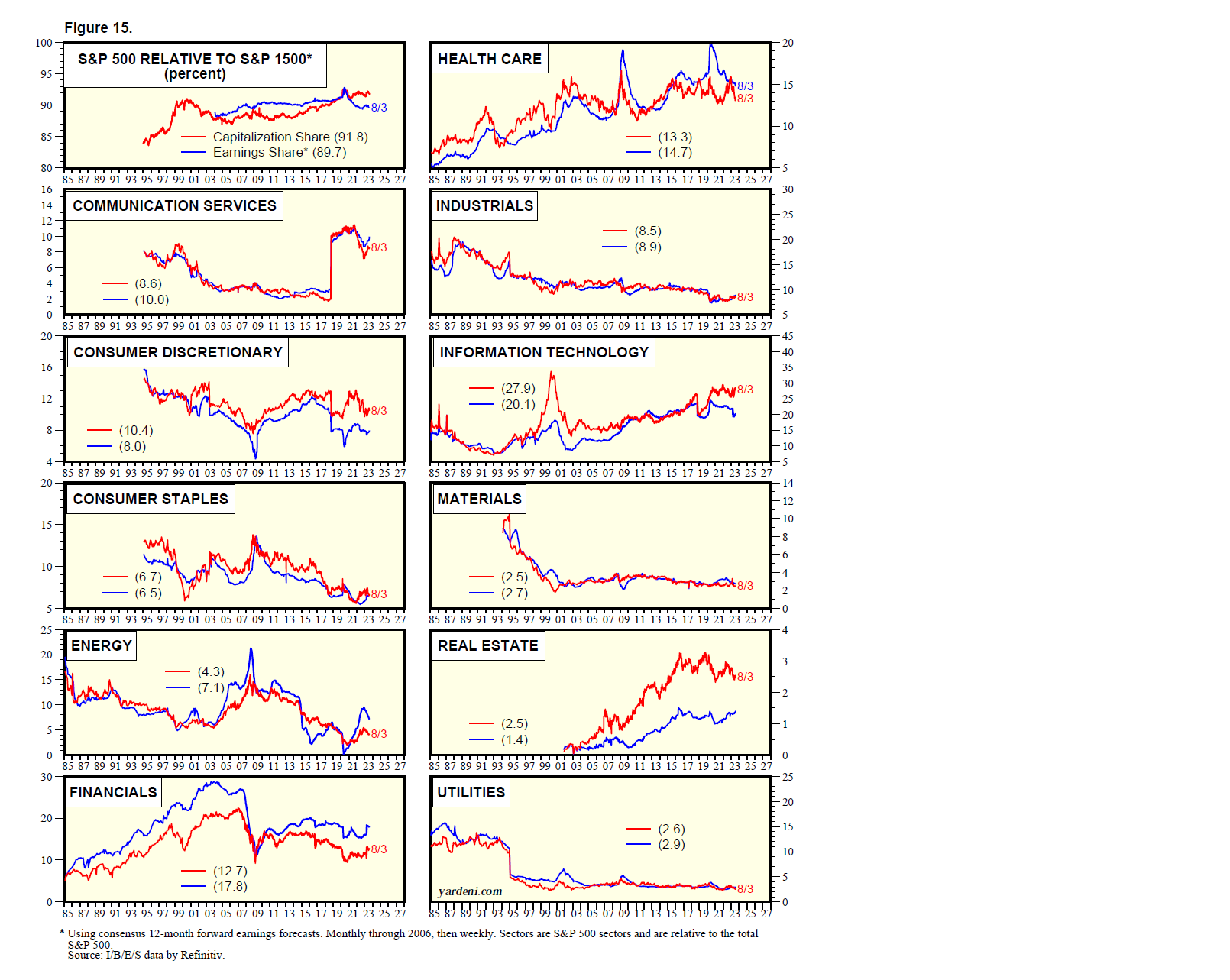

(1) A tough 2023. The S&P 500 Health Care sector’s stock price index is one of only four among the 11 S&P 500 sectors to fall this year. Here’s the performance derby for the S&P 500 and its sectors ytd through Tuesday’s close: Information Technology (54.0%), Communication Services (47.8), Consumer Discretionary (36.9), S&P 500 (20.9), Industrials (12.0), Financials (6.6), Materials (6.3), Real Estate (2.3), Health Care (-2.1), Consumer Staples (-4.1), Energy (-8.4), and Utilities (-10.6) (Fig. 1).

The stock price indexes of all but one of the industries within the S&P 500 Health Care sector severely lagged the S&P 500 ytd through Tuesday’s close: Health Care Distributors (23.1%), Health Care Facilities (8.6), Health Care Equipment (3.9), Health Care Supplies (2.7), Managed Health Care (0.4), Biotechnology (-2.9), Pharmaceuticals (-3.7), Life Sciences Tools and Services (-9.9), and Health Care Services (-12.9) (Fig. 2).

(2) Strong earnings growth expected in ’24. Ironically, given the 2023 underperformance of Health Care’s stock price index, this is the S&P 500 sector that analysts see bound for the strongest earnings growth in 2024—of 19.5%, representing a sharp about-face from the sector’s projected earnings drop this year of 20.2%.

Note how much faster the S&P 500 Health Care sector’s earnings are forecast to grow in 2024 relative to the other S&P 500 sectors: Health Care (19.5%), Communication Services (15.9), Information Technology (14.7), Consumer Discretionary (11.7), Industrials (11.1), S&P 500 (11.0), Utilities (8.1), Financials (5.9), Consumer Staples (5.2), Energy (3.7), Materials (2.9), and Real Estate (-0.5).

The Health Care sector’s healthier earnings growth next year owes much to the rebound in the Pharmaceuticals industry’s earnings. In 2022, pharma earnings were boosted by the pandemic, particularly for companies that sold vaccines or needed supplies. This year, earnings for those companies fell sharply as memories of the pandemic faded. Next year, more normal earnings growth is expected to return.

The Pharmaceuticals industry had 18.0% earnings growth in 2022, followed by a projected 41.9% decline in earnings this year; it’s expected to grow earnings by 51.1% in 2024. As a result, the Pharmaceuticals industry’s earnings are expected to be the second fastest growing in the S&P 500 next year, behind only Movies & Entertainment. Notably, though, the Pharmaceutical industry’s earnings estimates will likely be trimmed over the next week as analysts factor in the sharply lower 2024 earnings guidance that Pfizer announced yesterday.

Here are the 2024 earnings growth estimates for the S&P 500 Health Care sector and its component industries: Pharmaceuticals (51.5%), Health Care sector (19.6), Health Care Distributors (13.0), Managed Health Care (11.0), Health Care Supplies (10.7), Biotechnology (9.1), Health Care Facilities (8.2), Health Care Equipment (8.1), Health Care Services (5.1), and Life Sciences Tools & Services (1.0).

(3) Thank Merck, Pfizer & Lilly. Three pharma stocks are expected to post standout earnings growth next year: Eli Lilly, Merck, and Pfizer. Lilly’s results should get a boost from Mounjaro, a diabetes drug that’s now being used for weight loss. A recent analysis of health records and other data showed that those taking Mounjaro lost weight faster than those taking Novo Nordisk’s competing Wegovy and Ozempic drugs, a November 27 Reuters article reported. Lilly’s earnings are expected to rise 86.2% next year, and its shares have climbed 59.8% ytd.

Merck’s earnings growth will jump next year because this year’s earnings are depressed. The drugmaker is facing the patent expiration of blockbuster cancer drug Keytruda later this decade. In preparation for the expiration, Merck has been doing deals to boost its drug pipeline, including a recently announced joint venture with Daiichi Sankyo to commercialize three antibody-drug conjugates that fight cancer. While an upfront payment of $5.5 billion related to the Daiichi joint venture depressed Merck’s earnings this year, it will make Merck earnings growth in 2024 look impressive: 455.6%. Merck’s shares are 5.9% lower ytd.

Pfizer is also facing drug patent expirations and tough comparisons to Covid-boosted earnings in 2022. To help fill its drug pipeline, Pfizer recently announced the acquisition of Seagen, another antibody drug conjugate for fighting cancer. In October, Pfizer slashed its 2023 sales guidance for Paxlovid (a drug to treat Covid) to $1 billion from $8 billion, announcing that the US government returned roughly a third of the Paxlovid doses it had bought from the company.

On Wednesday, Pfizer announced its 2024 earnings estimate of $2.05-$2.25 a share, far below analysts’ consensus forecast of $3.18 a share. Results will be lower than expected because revenue from Covid-related products are forecast to come in well below what analysts had penciled in. Pfizer’s earnings are still expected to bungie from the $5.47 a share it earned in 2022 down to $1.73 this year, then up 24.4% to $2.15 in 2024, using the midpoint of the earnings range the company gave. But the rebound was far lower than expected; that sent the shares tumbling roughly 7% yesterday, bringing its ytd decline to almost 50%.

China: Is Xi Fiddling? It’s been more than two years since China’s most indebted property developer, Evergrande, defaulted on more than $300 billion of debt. Over that time, no restructuring plan has been agreed to, leaving creditors and an estimated 1.5 million retail homebuyers in limbo. Evergrande isn’t alone. Oher Chinese property developers have defaulted as well, and debt restructurings—the kind that really flush out the system and allow it to grow again—are mostly nonexistent. A few developers have restructured their dollar-denominated debt, but they’ve yet to reduce the amount of local debt outstanding.

The status quo has left consumers who purchased apartments in the developers’ unfinished properties unsure of what will happen to their investments and likely wary of spending much on other goods. Most developers aren’t moving forward with new projects, so they’re not buying new parcels of land from municipalities. That’s leaving local municipal coffers low on funds and staring up a mountain of debt.

Earlier this week, the Chinese Communist Party (CCP) held its annual economic conference, but it concluded without news of any large, splashy spending program to save the day. Meanwhile, more signs of deflation have appeared in China’s economy, an ominous development given the amount of debt the country needs to repay. We wouldn’t be surprised to see a cartoon of President Xi fiddling, as Nero purportedly did while Rome burned (though fiddles didn’t exist in the time of Nero).

Let’s take a closer look at these recent developments:

(1) Many goals, no instructions. The CCP aims to promote “high-quality development” and focus on scientific and technological innovation, according to a government statement published by Xinhua News Agency. The government aims to “vigorously promote” new industrialization, develop the digital economy, and accelerate the development of artificial intelligence. The party is targeting the development of industries that include biomanufacturing, commercial aerospace, quantum, and life sciences, while strengthening applied and cutting-edge research and encouraging both entrepreneurial and equity investments. The government also aims to stimulate consumption and expand investments that have proven profitable.

The statement did acknowledge the real estate problem China faces: “It is necessary to coordinate and resolve risks in real estate, local debt, small and medium-sized financial institutions, etc., severely crack down on illegal financial activities, and resolutely maintain the bottom line of preventing systemic risks.” But no solutions to the problem were given.

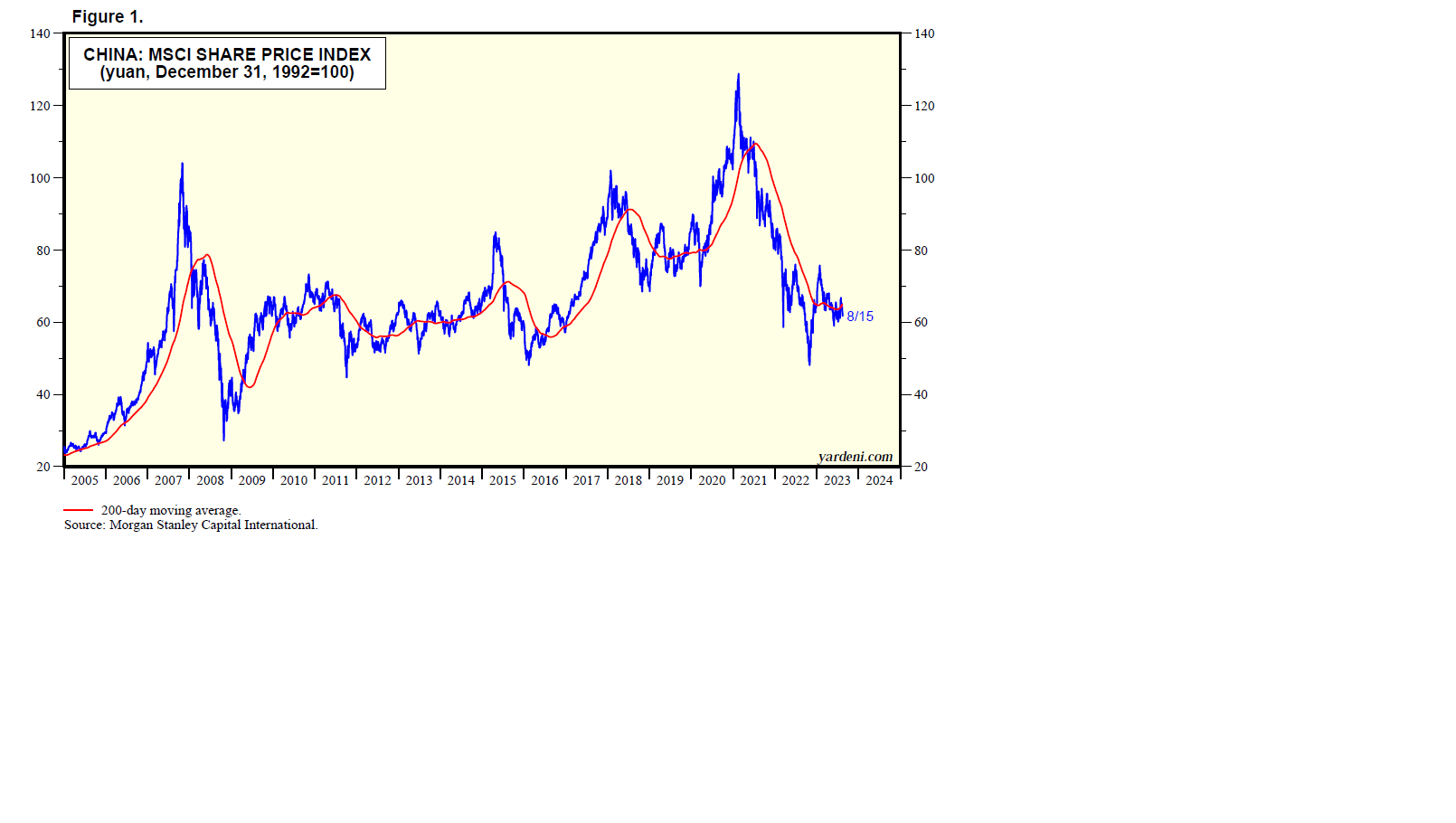

Chinese shares have fallen sharply this year, with the China MSCI index closing at a 13-month low on Monday and down 13.9% ytd through Tuesday’s close. The broader Shanghai Shenzhen CSI 300 closed at a 58-month low on Wednesday and is down 13.0% ytd (Fig. 3).

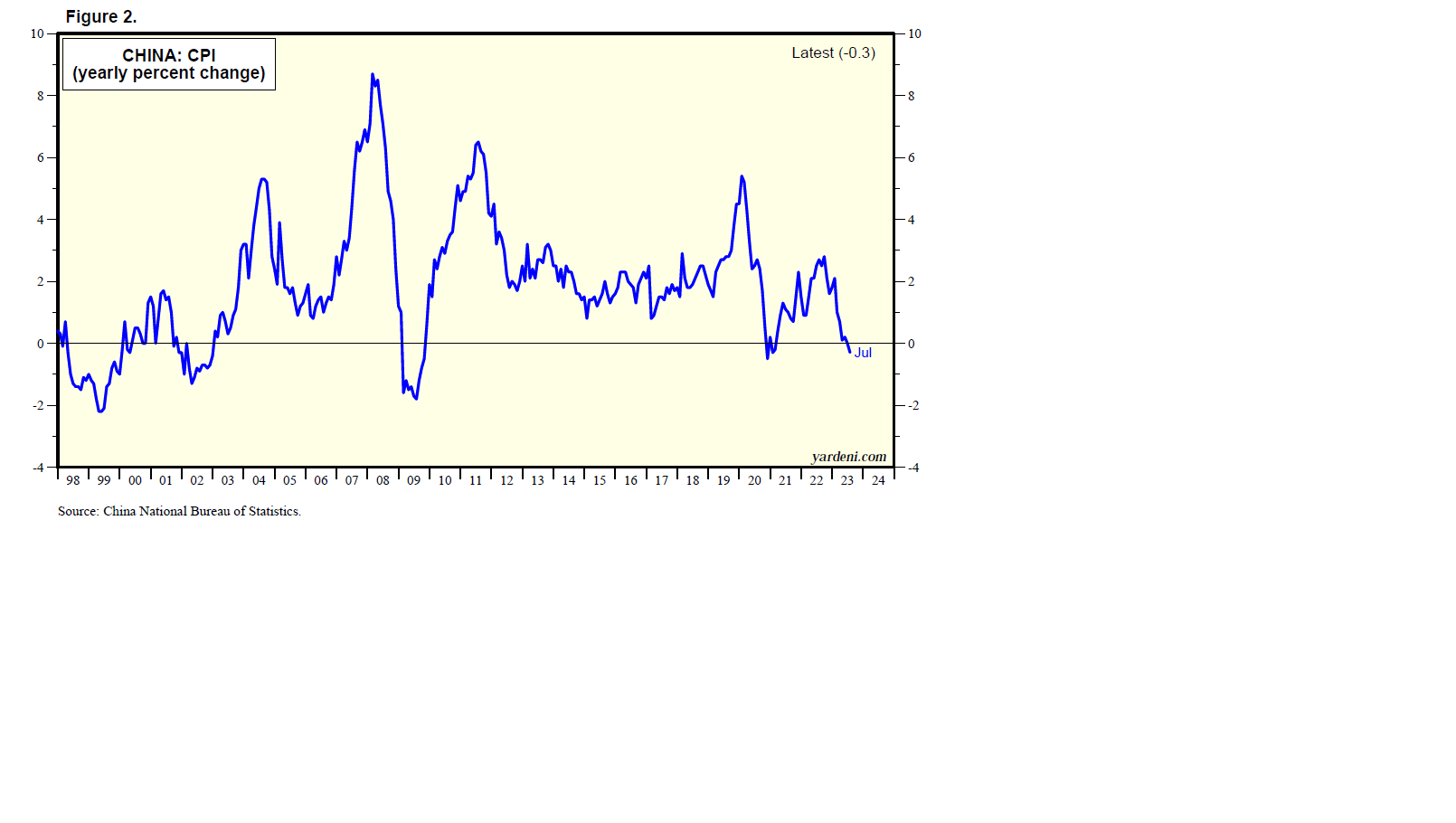

(2) Daunting deflation. Both consumer and producer prices have fallen y/y several months this year, indicating that deflation may be on the verge of becoming entrenched. China’s consumer price index (CPI) fell 0.5% y/y in November, its third month of declines. CPI was negative by 0.2% in October and 0.3% in July and unchanged in June and September. China’s core CPI fell 0.6% y/y in June and was flat in May and July. It was at 0.4% y/y in November.

Producer prices have also been in negative territory since last October and most recently fell by 3.0% in November (Fig. 4).

The specter of deflation should keep Chinese central bankers up at night. It certainly worried former Fed Chair Ben Bernanke when deflation was a problem in the US; he once said that if deflation became serious enough, it could warrant dropping money from a helicopter to resolve it. While he wasn’t serious, the implication is that central bankers should do whatever is possible to steer economies clear of or out of deflationary environments.

(3) Lots of can kicking. Since the start of 2020, at least 60 Chinese property developers with more than $140 billion of dollar-denominated bonds collectively have defaulted, according to a December 8 FT article. That doesn’t include the hundreds of billions of dollars of domestic debt these property developers owe.

While it seems clear that debt restructurings are needed, investors continue to let the heavily leveraged property developers off the hook—for now. In the handful of restructurings that have been proposed, it’s the dollar-denominated offshore debt that’s being restructured, while the local debt remains outstanding.

Just this week, most investors in Country Garden Holdings’ yuan-denominated bonds agreed not to exercise a put option that would require the bond be repaid now, before it matures next year. And they were rewarded. Country Garden announced on Wednesday that it repaid the bond in full. Meanwhile, the builder already defaulted on a dollar-denominated bond in October, and its sales fell 77% in November, a December 12 Bloomberg article reported.

Chinese property developer Shimao Group has proposed a restructuring plan that would reduce its $14 billion of offshore debt by as much as half. Some of the debt would be exchanged for new nine-year loans, new senior secured debt, and equity-linked instruments. The company’s $25 billion of local debt does not seem to be impacted by the restructuring proposal. The company has been selling assets to reduce its debt, but it still had to roll over about CNY18.9 billion of local debt during H1-2023 when it posted a net loss that rose 23% to CNY12.1 billion, a December 8 Yicai Global article reported.

Developer Sunac won court approval to restructure about $10 billion of offshore debt, in part by issuing creditors new notes and convertible bonds. The company did not say whether or how its Rmb1trillion of debt would be affected, an October 5 FT article reported.

Bucking this trend are Evergrande’s offshore creditors, who have petitioned a Hong Kong court to liquidate the company. However, the judge in the case postponed a hearing until January to give the property developer more time to propose a restructuring plan, a December 4 FT article reported.

Disruptive Technologies: Riding the AI Wave. Artificial intelligence (AI) definitely captured the public’s attention this year. All of a sudden, ChatGPT and other AI programs were available to the ordinary Joe for free, firing the imaginations of everyone from 13-year-olds with homework to do (or not?) to CEOs focused on using the technology to increase productivity.

Long-time tech watcher and former Andreessen Horowitz partner Benedict Evans made AI the subject of his annual presentation on macro and strategic trends in the tech industry. It’s worth a look, as is the video of a presentation he gave a year ago on the subject.

In the video, he suggests thinking about AI as an intern. If you employed 50 or 100 interns, what would you ask them to do to make work easier, faster, and more efficient? As with many interns, AI’s output needs to be checked given its proclivity to hallucinate, but that won’t eliminate the technology’s usefulness and ability to increase productivity.

In his presentation, Evans quotes Bill Gates: “In my lifetime, I’ve seen two demonstrations of technology that struck me as revolutionary … the [graphic user interface] and ChatGPT.” Graphic user interfaces (GUI) are the symbols on computer screens that allow you to do things, like open email or cut and paste copy, with the click of a mouse instead of having to write lines of code. GUIs made computers accessible to the everyman, eliminating the need for users to have a programing degree.

Now the question is: What will ChatGPT empower the ordinary Joe to do that once required specialized skills? Our kids know ChatGPT can turn them into writers, artists, and videographers. Companies seem to be harnessing the technology in their marketing departments and in chatbots to improve communication with customers. We’re sure that smart folks will continuously think of novel uses, giving us plenty to write about in 2024.

Earnings: Yesterday, Today & Tomorrow

December 13 (Wednesday)

Check out the accompanying pdf and chart collection.

Executive Summary: S&P 500 companies collectively outperformed industry analysts’ Q3 expectations, posting record-high revenues and earnings per share. The profit margin was the highest in four quarters, suggesting that the cost-push inflation pressures that had weighed on margins are easing. … Analysts’ consensus estimates for 2024 and 2025 suggest accelerating growth for both revenues and earnings and rising profit margins. … The earnings outlook together with our projected valuation ranges result in our price targets for the S&P 500 of 4600 by the end of this year, 5400 by the end of next, and 6000 by year-end 2025.

Earnings I: The Past. The Q3 earnings season is over, and the final numbers for S&P 500 companies are in. The results in aggregate were better than analysts had expected, which isn’t surprising when the economy is growing. Worse-than-expected results tend to occur when the economy is falling into a recession. Widespread concerns earlier this year that the economy would fall into a recession—which was not our outlook, as you know—have been largely alleviated.

Today, let’s do some time traveling. We’ll review the recent past—i.e., the Q3 results—then go back to the future by revisiting our forecasts for S&P 500 revenues per share, earnings per share, and the profit margin for 2023, 2024, and 2025. Then let’s conclude with a discussion of the outlook for the S&P 500’s forward earnings per share, forward P/E, and stock price index—including our newly announced S&P 500 target of 6000 for year-end 2025.

Here we go:

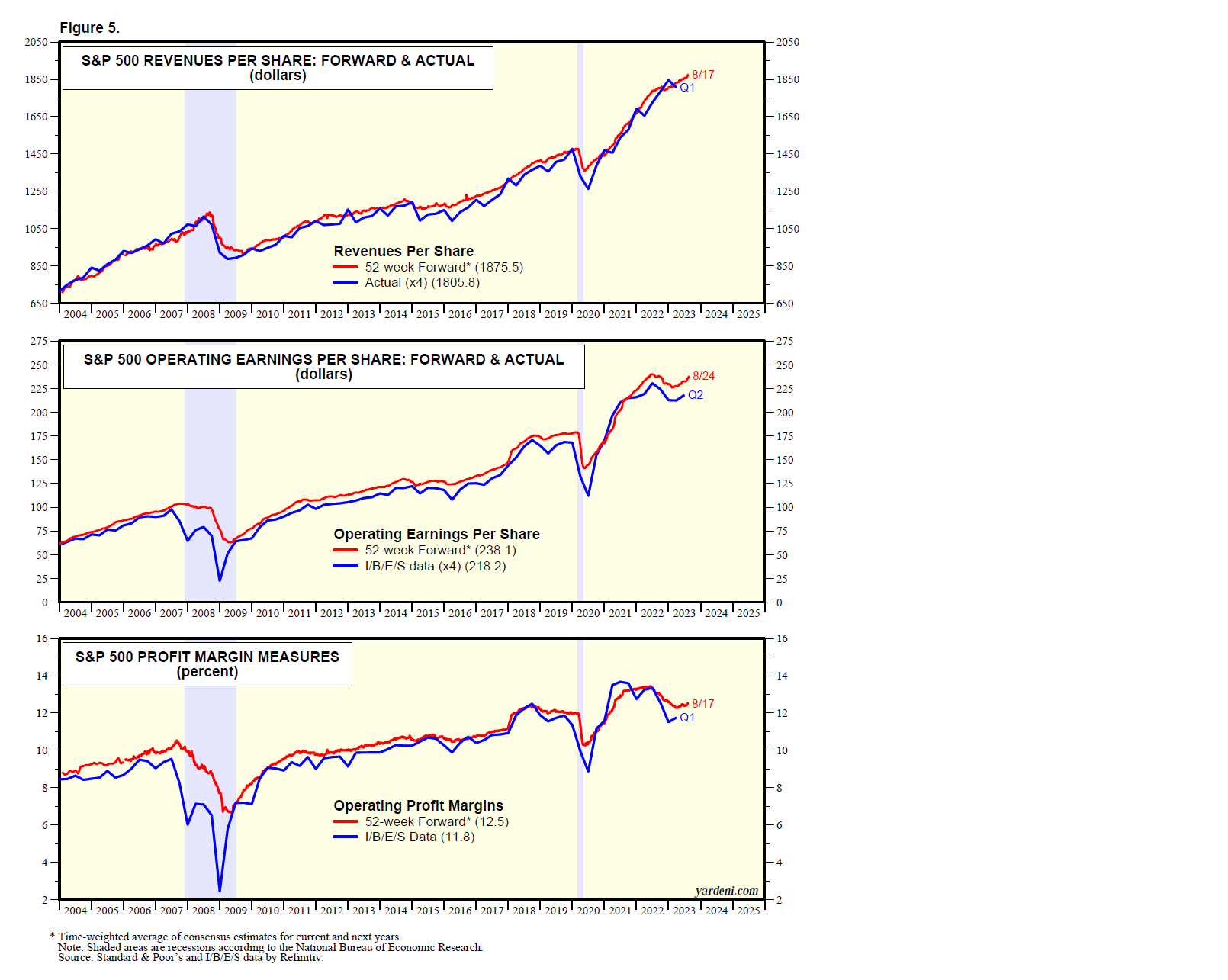

(1) Revenues. S&P 500 companies’ collective revenues per share rose to a record high for a second straight quarter in Q3 after dipping in Q1 from Q4-2022’s record, but the y/y gain slowed to an 11-quarter low of 5.0% from 7.1% in Q2 (Fig. 1 and Fig. 2). Inflation continued to boost the growth rate, but less so than in Q2—as the GDP price deflator rose only 1.7% in Q3 compared to 3.5% in Q2—but the inflation-adjusted revenues increase was still a solid gain.

(2) Earnings. S&P 500 earnings per share also rose to a record high in Q3, for the first time since Q2-2022, and its 4.6% y/y increase was its first y/y gain in four quarters (Fig. 3 and Fig. 4).

(3) Profit margin. We can calculate the S&P 500’s profit margin by dividing the index’s earnings by revenues (Fig. 5 and Fig. 6). The margin rose 0.8ppts q/q to a four-quarter high of 12.5%, which is up from 11.5% during Q4-2020. But it was still down from the record high of 13.7% during Q2-2021.

The just-ended earnings recession was very mild, with three back-to-back quarters of modest single-digit percentage declines on a y/y basis. There was no revenues recession. The earnings weakness of recent quarters has been entirely attributable to the decline in the profit margin due to cost-push inflation, and productivity has been weak because of unusually high turnover in the labor market, with record-high quits and job openings earlier in the year. However, the improvement in the profit margin during Q3 suggests those pressures are abating now.

Earnings II: The Present. The S&P 500 companies’ actual Q3 earnings per share turned out to be up 4.6% y/y, which was better than the 0.2% decline expected by industry analysts collectively at the start of the earnings season (Fig. 7).

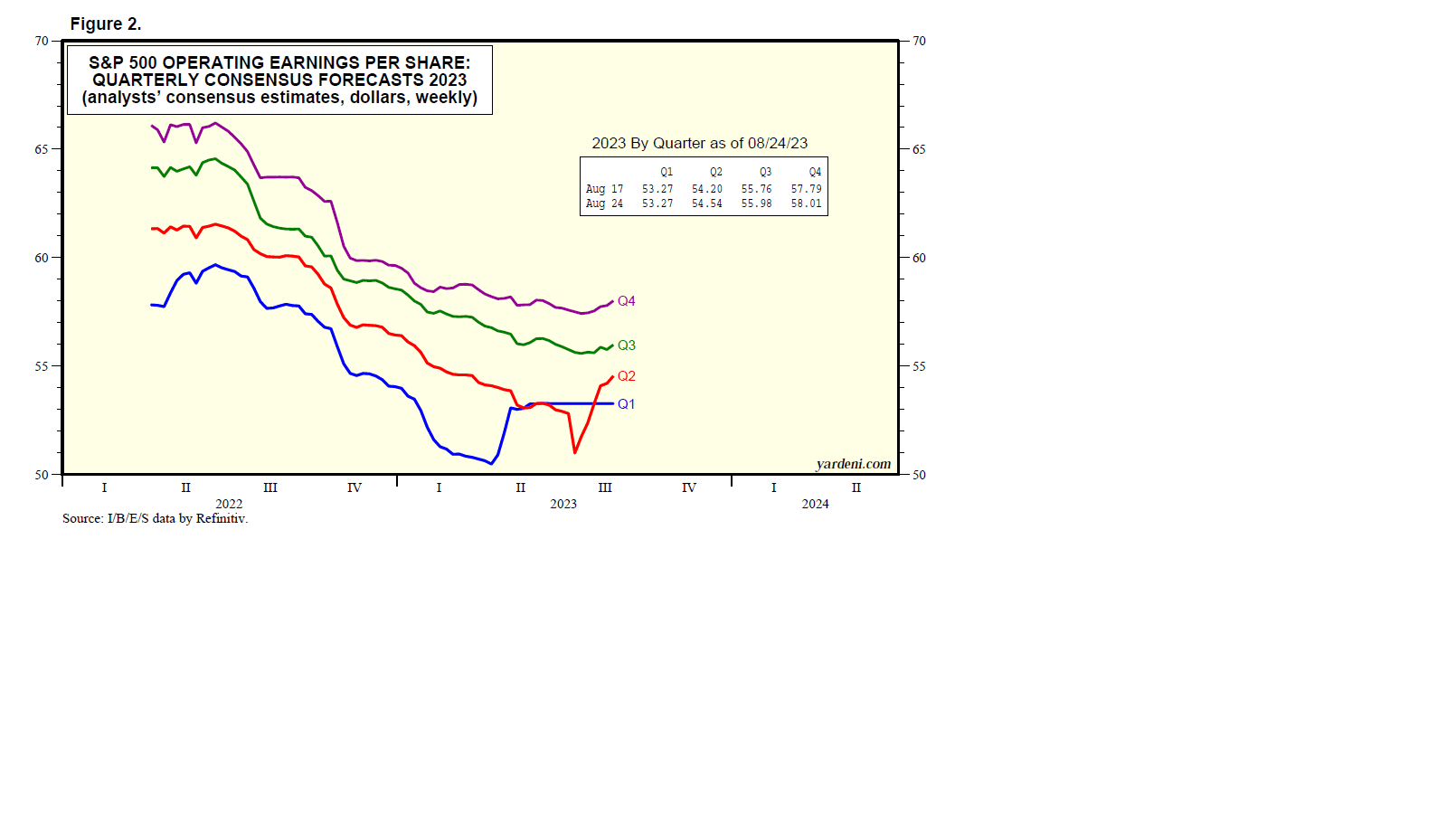

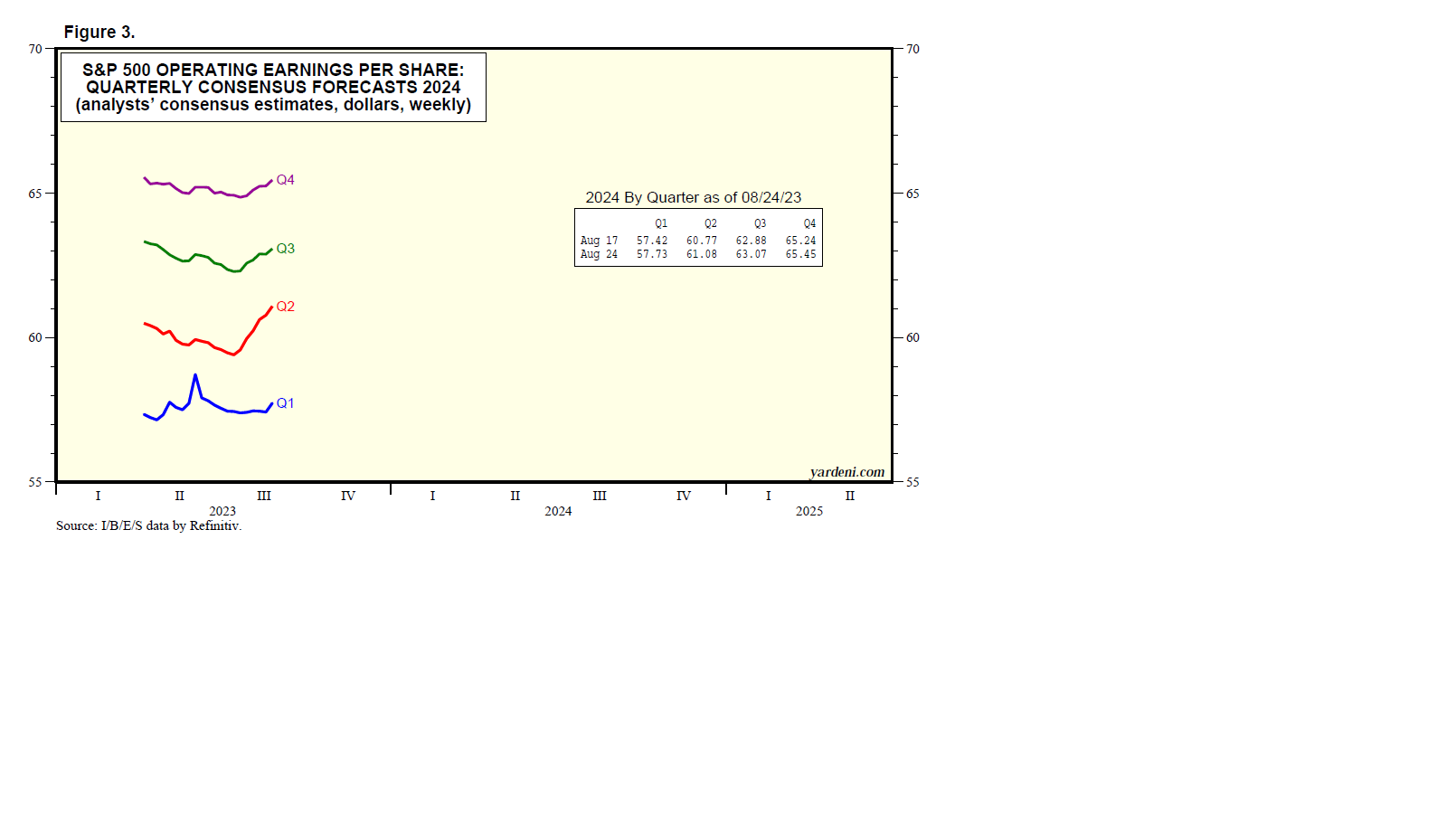

Currently (as of the December 7 week), industry analysts project that S&P 500 earnings will be up 3.5% y/y during Q4, followed by quarterly gains in 2024 of 7.0% (Q1), 11.2% (Q2), 9.3% (Q3), and 17.8% (Q4) (Fig. 8). At the start of Q4, analysts had been expecting a 9.4% gain in Q4-2023 earnings. Since then, expectations were mostly cut at the drugmakers, auto manufacturers, and commodity-related industries in the S&P 500 Materials sector.

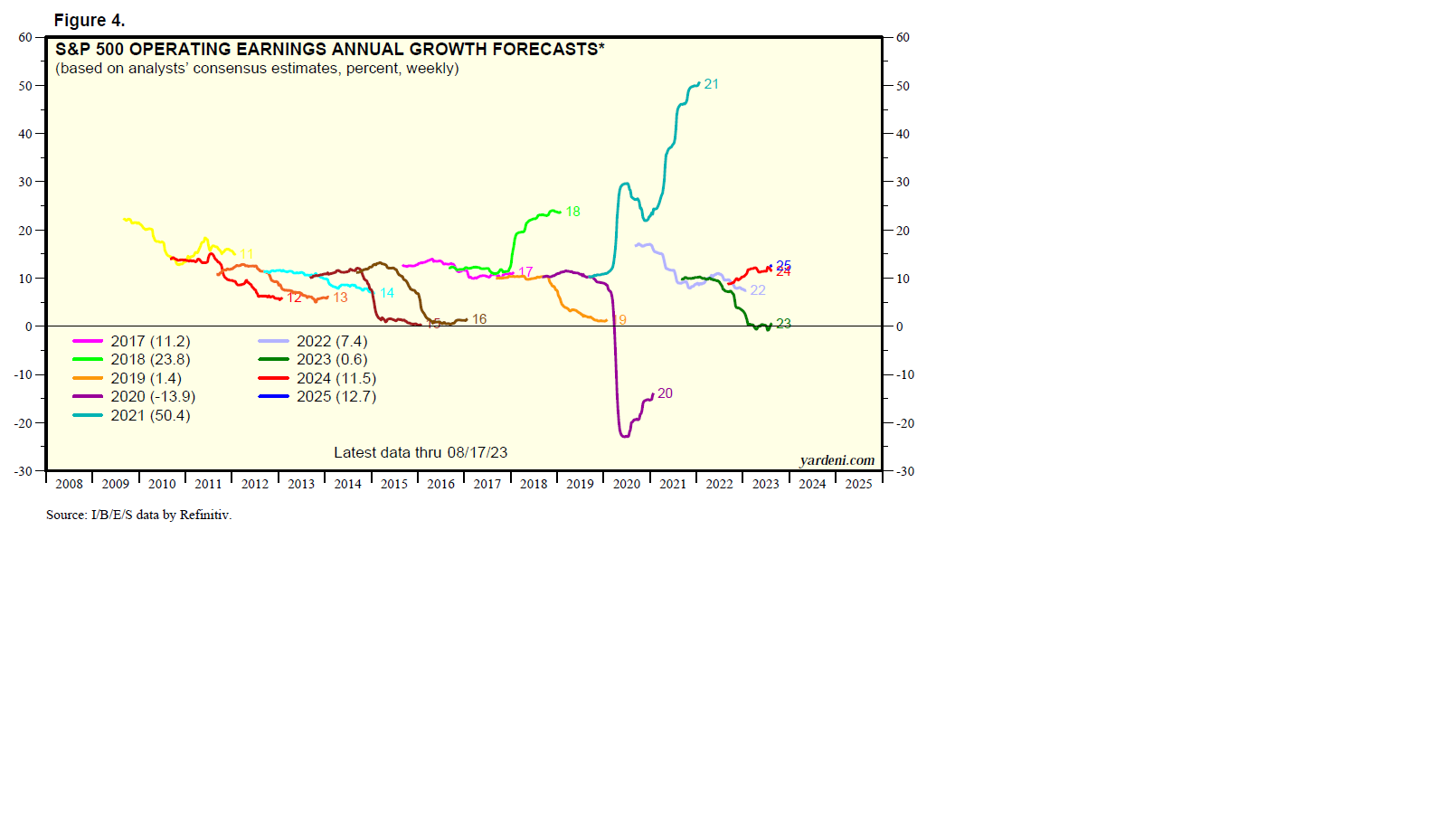

Like the economy, revenues and earnings have been experiencing a soft landing so far, and industry analysts as a group have not been slashing their forecasts. Currently, the analysts’ consensus estimates imply the following y/y revenues and earnings growth rates: for 2023 (2.1%, 0.7%), for 2024 (4.9%,11.2%), and for 2025 (5.4%, 12.4%) (Fig. 9 and Fig. 10).

The S&P 500 profit margin forecasts implied by analysts’ revenues and earnings estimates for 2023, 2024, and 2025 are stabilizing now after dropping at the start of this year. The latest readings for the three years are at 11.8%, 12.5%, and 13.4%. The bottoming of industry analysts’ implied margin estimates suggests they believe that the mini recession in earnings attributable to weakening profit margins is over. They may be right, with margins rising again.

As you know, Joe and I are big fans of weekly S&P 500 forward revenues per share and forward earnings per share as great coincident indicators of the actual quarterly series for S&P 500 revenues per share and earnings per share (Fig. 11 and Fig. 12). (Forward revenues and earnings are the time-weighted average of analysts’ estimates for the current year and the coming year.)

During the November 30 week (the latest data available), forward revenues was just 0.2% below its record high, hit during the November 2 week. But forward earnings has been hitting record highs regularly since the September 14 week—the longest string of successive weekly record highs since the June 16, 2022 week. The forward profit margin edged up during the December 7 week to a 13-month high of 12.7% (Fig. 13).

Earnings III: The Future. Now let’s turn to an update of our outlook for the S&P 500 companies’ collective revenues, earnings, and profit margin.

Since earnings have had a soft landing so far, rather than a hard one, we are expecting a U-shaped, rather than a V-shaped, earnings recovery. If we are surprised, then it’s likely to be because the recovery is more robust than we are projecting. If so, that would be attributable to higher profit margins, boosted by technology-driven productivity gains. Let’s think ahead:

(1) Revenues. We are projecting that revenues per share will increase 4.0% this year to $1,823, 4.0% in 2024 to $1,896, and 4.0% in 2025 to $1,970 (Fig. 14).

(2) Earnings. We project earnings per share will be $225 this year, $245 next year, and $270 in 2025 (Fig. 15). That’s been our forecast since summer 2022. (The final tally for 2022 was $218. We had been projecting $220.) We are now forecasting $300 in 2026.

(3) Profit margin. Our projections imply that the profit margin will fall from 12.4% in 2022 to 12.3% in 2023 and rise back to 13.2% in 2024 and 13.7% in 2025 (Fig. 16).

(4) Forward earnings. We are projecting that S&P 500 forward earnings per share will be $245 at the end of this year (currently $244), $270 at the end of next year and $300 at the end of 2025 (Fig. 17). Those are what we expect the analysts’ consensus earnings expectations then will be for 2024, 2025, and 2026. (At year-ends, forward earnings match the analysts’ projections for the upcoming year.)

(5) Valuation & S&P 500 ranges. Now let’s apply forward P/E ranges of 16.0-20.0 to our forward earnings projections to derive target ranges for the S&P 500 (Fig. 18). The range for 2024 is 4320-5400, and the range for 2025 is 4800-6000 (Fig. 19). Our year-end point estimates are 4600 by the end of this year, 5400 by the end of 2024, and 6000 by year-end 2025.

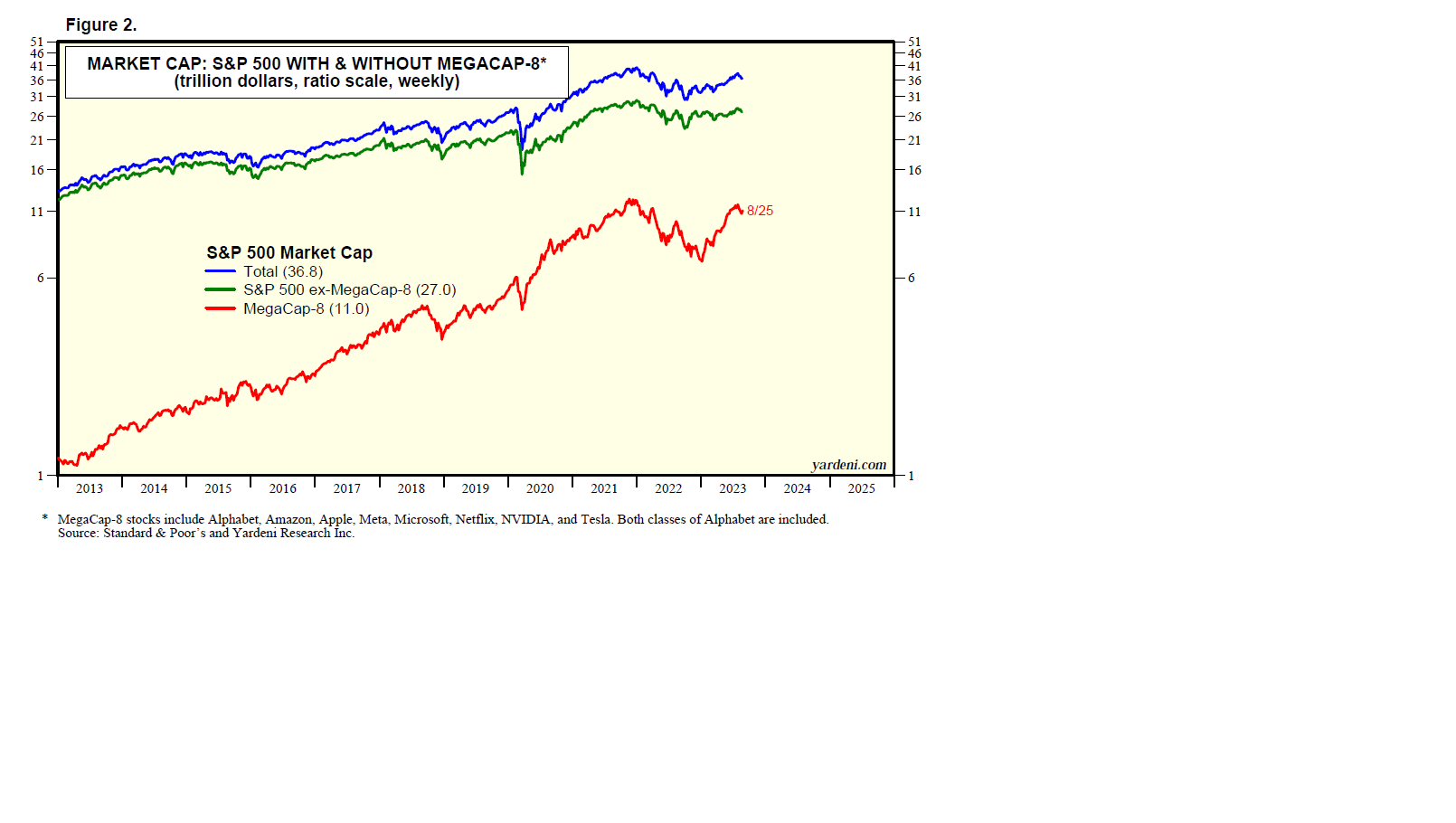

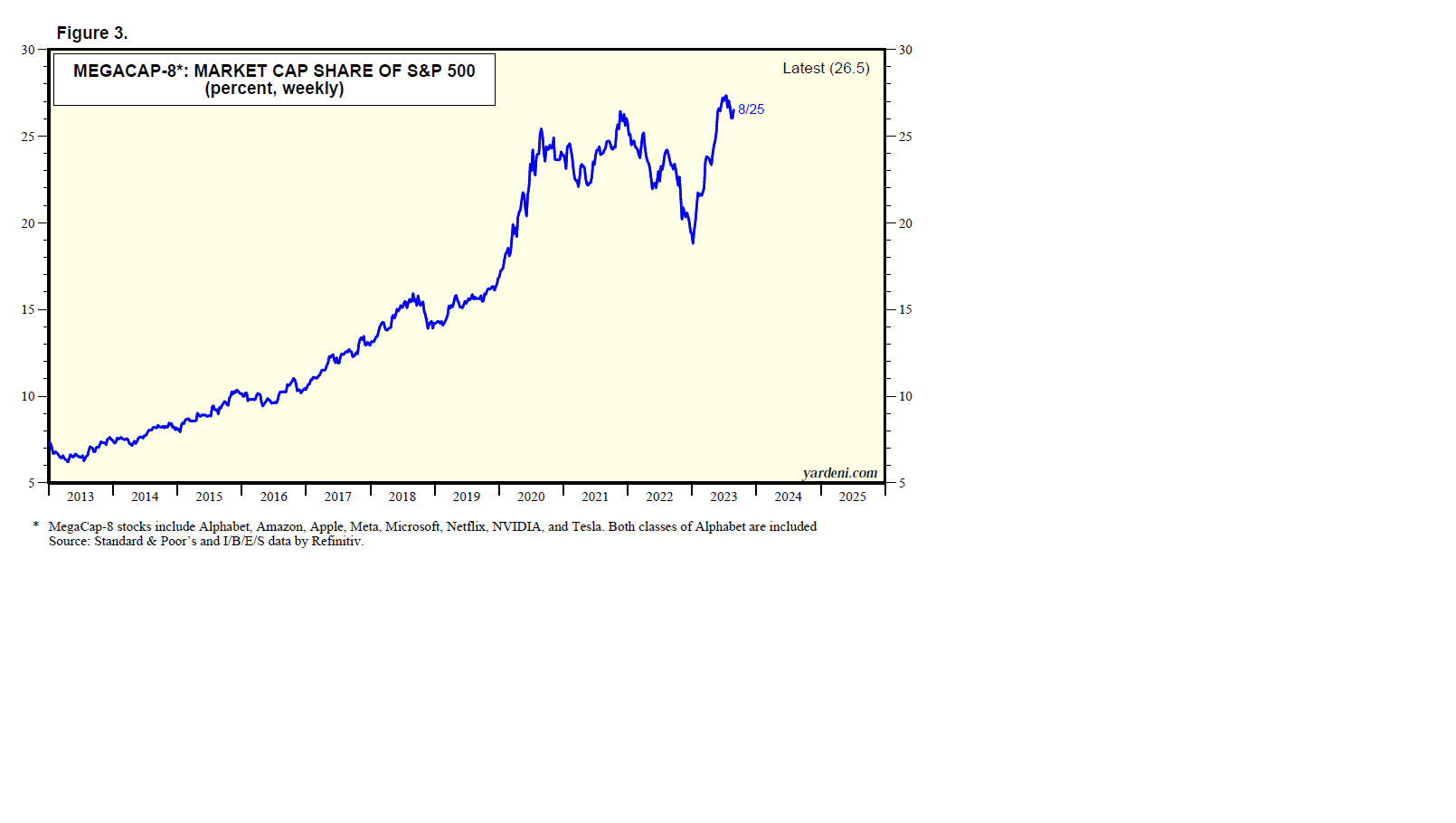

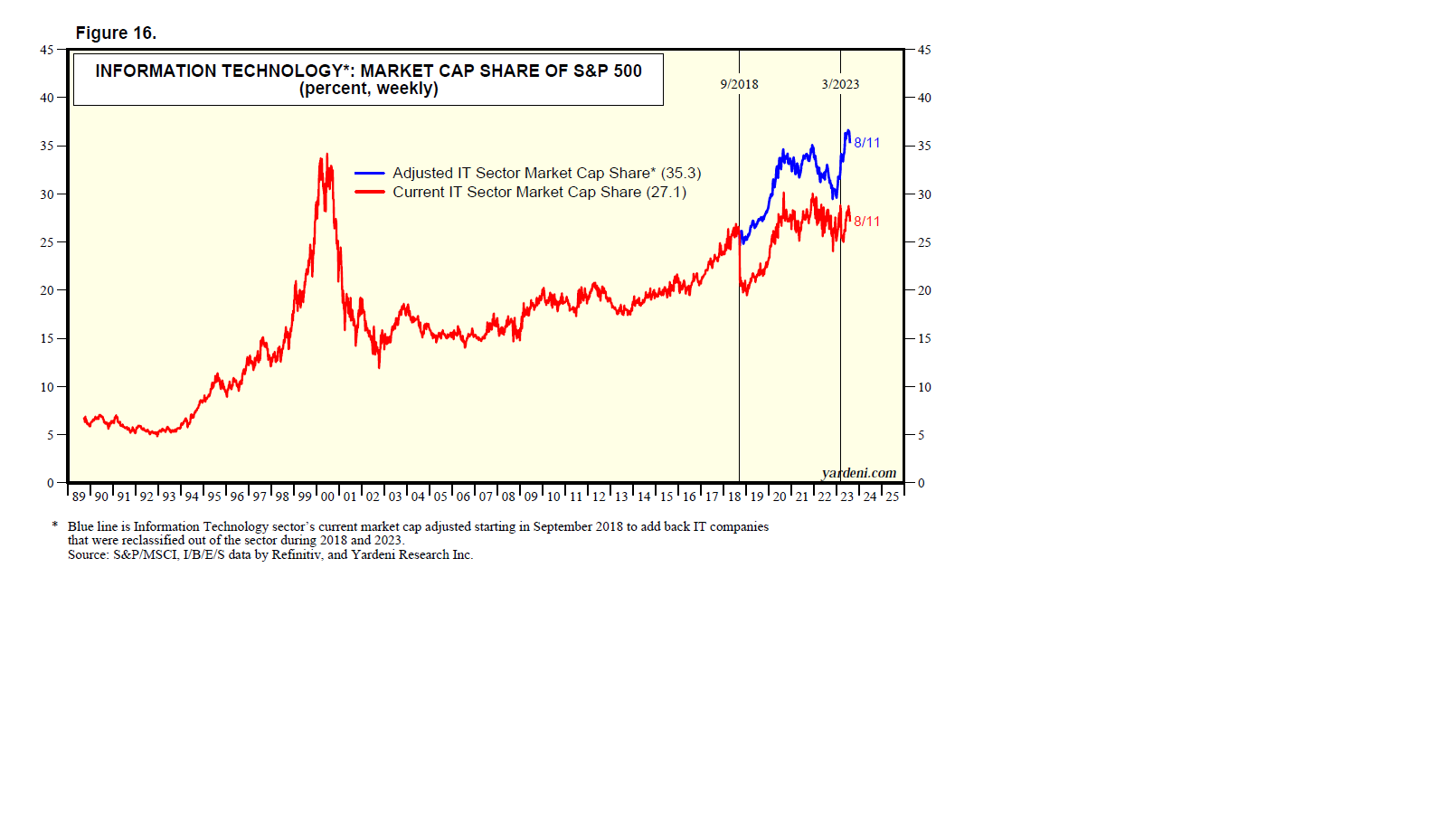

We acknowledge that our valuation multiple ranges are high historically. However, they reflect our expectations that the MegaCap-8 stocks (i.e., Alphabet, Amazon, Apple, Meta, Microsoft, Netflix, Nvidia, and Tesla) will continue to account for a significant portion of the market cap of the S&P 500, and that they will continue to be highly prized by investors.

We are also seeing more reasons to believe in our Roaring 2020s scenario—the theory that productivity growth will stage a comeback, driven by widely implemented technological solutions to address the US’s chronic labor shortages, and rising productivity will propel economic growth to surprising heights.

Global Economy Still In A Funk

December 12 (Tuesday)

Check out the accompanying pdf and chart collection.

Executive Summary: Recent global indicators show economic growth at a crawl, commodity prices remaining weak, and inflation moderating. Weighing on the pace of growth have been recessions in China and Europe. China’s economic malaise is secular in nature and likely to last for a while given the challenges facing that country. But we expect the ECB to ease in the spring as inflation moderates, and the Eurozone’s shallow recession to lift. US economic growth has been slowing from Q3’s rapid pace, but a comeback in productivity growth could recharge it. … We continue to advise overweighting US stocks in global equity portfolios.

Weekly Webcast. If you missed Monday’s live webcast, you can view a replay here.

Global Economy: Secular or Cyclical Weakness? The global economy is growing, but at a slow pace. Much of the weakness is attributable to the recessions in China and Europe. US economic growth is slowing from Q3’s rapid pace. Much of the weakness is structural in China but cyclical in the US and Europe.

In 2024, China’s economic weakness is likely to persist and weigh on the global economy. But Europe should start to recover, as Melissa and I discussed last Wednesday. The US economy should continue to grow slowly, though we are inclined to anticipate upside surprises if productivity growth continues to make a comeback, as it did during Q2 and Q3 of this year. In our scenario, global inflation should continue to moderate. It might even fall to the 2.0% y/y rate targeted by the Fed for the US and the European Central Bank (ECB) for the Eurozone by the end of next year.

Yesterday, Debbie and I discussed the prospects for the economy over here. Today, let’s look at the outlook over there:

(1) Global growth indicators crawling. According to the Netherlands Bureau for Economic Policy Analysis, global industrial production rose 0.5% y/y through September. However, it has been basically flat since early 2022, though at a record high (Fig. 1). That’s when China was still imposing pandemic lockdowns, Europe’s economy was hit by the shocks from Russia’s invasion of Ukraine, and US consumers pivoted from buying goods to purchasing services. The volume of global exports has also been flat since early 2022, but also at a record high.

Since December 2021, industrial production and the volume of exports among advancing economies are down 1.3% and 1.2% (through September of this year, the latest data available) (Fig. 2). Both have been essentially flat. Over this same period, the production and exports of emerging economies are up 4.9% and only 0.1%. The industrial production index for the members of the Organization for Economic Co-operation and Development (OECD) has also been flat since the end of 2021 (Fig. 3).

(The OECD, with 38 member countries, was founded in 1961 to stimulate economic progress and world trade. The OECD includes the following countries: Australia, Austria, Belgium, Canada, Chile, Colombia, Costa Rica, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Israel, Italy, Japan, South Korea, Latvia, Lithuania, Luxembourg, Mexico, Netherland, New Zealand, Norway, Poland, Portugal, Slovak Republic, Slovenia, Spain, Sweden, Switzerland, Turkey, United Kingdom, and the United States.)

The weakness in both production and exports during 2022 can be attributed largely to global supply-chain disruptions. The New York Fed’s Global Supply Chain Pressure Index soared from 0.11 during October 2020 to 4.33 during December 2021 (Fig. 4). It was back down to 0.11 during October, the first reading above zero since January. Jammed ports and overwhelmed trucking systems depressed global production and exports during 2022. Inbound container traffic soared in US West Coast ports from mid-2020 through mid-2022 to new record highs (Fig. 5). It then dropped sharply during H2-2022 to pandemic lockdown levels. It has started to recover in recent months.

(2) Commodity prices remain weak. Commodity prices, especially those of industrial commodities and crude oil, have been weak, confirming that the global economy is weak. The price of a barrel of Brent crude oil has dropped 20% from September 27 through December 8 (Fig. 6). That’s despite output cuts by Saudi Arabia and Russia since the summer and despite the mounting tensions between the US and Iran because of the Gaza war.

The CRB raw industrials spot price index is down 21% from its most recent peak of 689.0 on April 4, 2022 to 541.4 on December 8, near its lowest level since February 8, 2021. The spot price of copper is included in the CRB index, and it is down 10.5% since January 26 on mounting evidence that China’s property crisis is worsening and weighing on Chinese growth. The price of copper is highly correlated with the China MSCI stock price index, which is down a whopping 56.7% since February 17, 2021 (Fig. 7).

(3) Global inflation moderating. Headline and core inflation rates peaked last October for the 38 member countries of the OECD at 10.7% and 7.8%, respectively (Fig. 8). They were down to 5.6% and 6.5% in October. Energy and food inflation among the OECD, which peaked last year at 40.8% and 16.1%, fell to -4.8% and 7.4% during October (Fig. 9). The headline and core CPI inflation rates for the G-7 countries peaked last summer at 7.8% and 5.5%; they were down to 3.4% and 3.9% in October.

Experience suggests that recessions are necessary to bring down inflation. Yet that’s not necessarily true, as inflation has fallen significantly in the US without a recession. However, inflation is a global phenomenon, especially the recent experience, which was largely triggered by the demand shock that overwhelmed goods markets around the world and their supply chains. That explains why goods inflation has dropped so quickly as soon as the buying binge for goods abated and the supply chains were normalized. Services inflation rates have been stickier, but they also are trending down.

Arguably, the US didn’t need a recession to bring inflation down because the recessions in China and Europe have done that job for it. Let’s turn to those two economies.

(4) China’s challenges. Jackie and I often have discussed the downsides of investing in China. The country prospered from the 1980s through 2013. That was the year that Xi Jinping became the president of China. A few years after assuming office, Xi turned increasingly hostile to the free market entrepreneurial spirit that his predecessors had embraced to stimulate widespread prosperity. The Chinese Communist Party (CCP) took back control of the economy. The problem is that the economy had spun out of control, particularly in the real estate sector.

Provincial governments raised revenues for infrastructure spending by selling land to developers who built ghost cities of empty apartments that were purchased by individuals as investments. The Chinese have a high saving rate and purchased stakes in trusts that are exposed to real estate. They also invested in the stock market. Recently, we’ve noted the significant negative wealth effect that China’s consumers are experiencing. As noted above, the China MSCI stock price index is down 56.7% since February 17, 2021. Apartment prices are falling in an illiquid market for such properties.

Just as China’s property market engine has stalled, so too has its export engine. The CCP’s hostile domestic policies toward entrepreneurs and belligerent foreign policies toward democracies have depressed foreign investments in China and China’s exports. The country is no longer viewed as a dependable business partner nor as a reliable source of goods, especially vital parts.

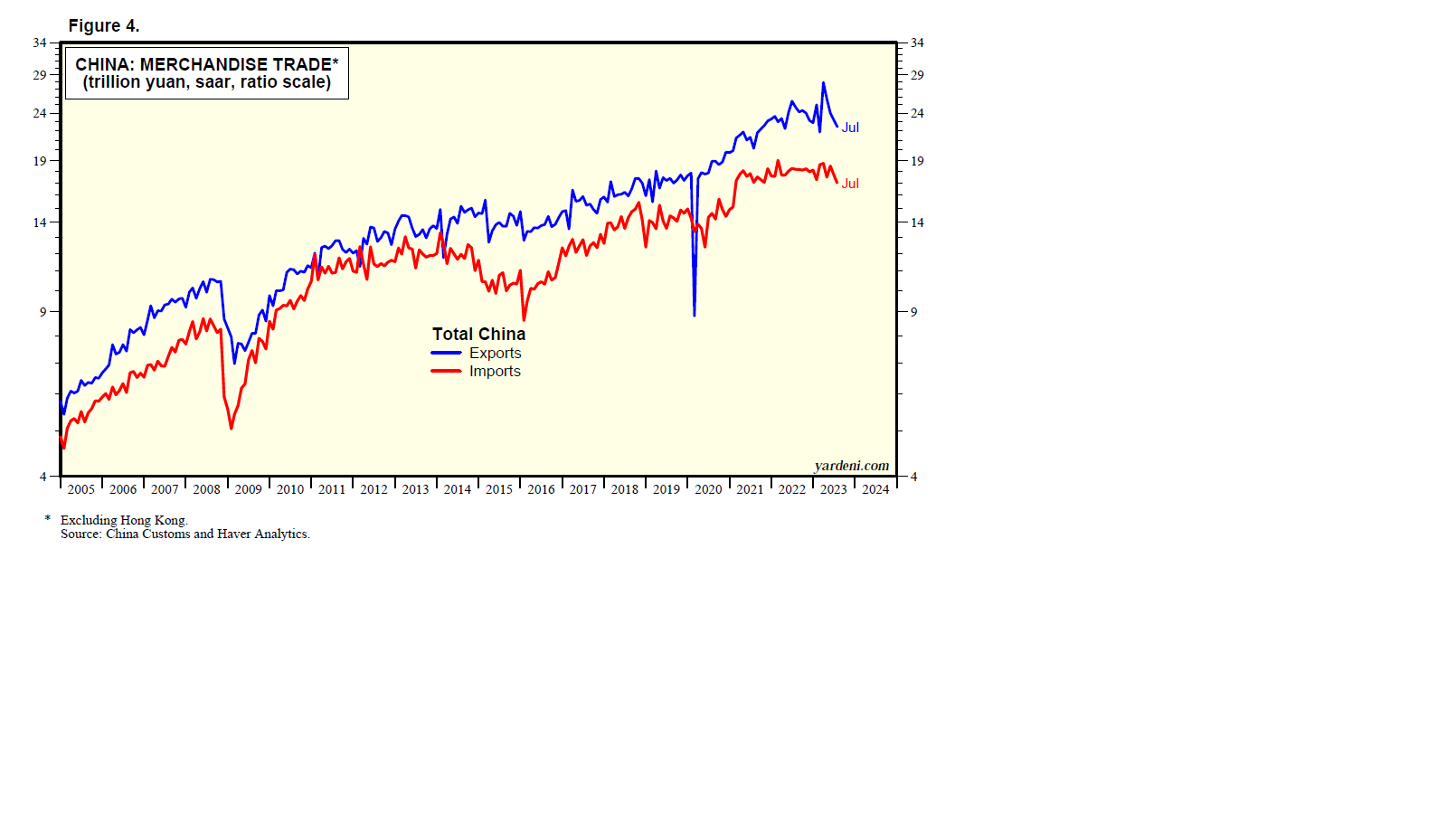

China’s exports have been flat since December 2021 through November of this year (Fig. 10). That partly reflects slower global economic growth. Imports have also been flat since March 2021. That undoubtedly reflects a weaker domestic Chinese economy.

(5) Europe’s shallow recession. Last week, Melissa and I reviewed the economic outlook for the Eurozone. It’s quite bleak currently, but we expect that more secure sources of energy, lower inflation, and lower interest rates will revive economic growth during H2-2024. The latest data suggest that the region is in a shallow recession currently. Real GDP fell 0.4% (q/q saar) during Q3 (Fig. 11).

The Eurozone’s Economic Sentiment Indicator suggests that GDP might be falling again during Q4. So does the volume of retail sales there, which has been falling since November 2021 (Fig. 12).

Also weighing on the region’s economic growth is the weakness in Germany’s manufacturing sector. Manufacturing orders fell 3.7% m/m and 7.3% y/y during October (Fig. 13). New orders were down in major sectors, including fabricated metal products, electrical equipment, and the key automotive industry. Machinery and equipment manufacturing orders dove 13.5% in October. Manufacturing production fell 0.4% m/m and 3.5% y/y.

As we wrote last week, we are expecting that the ECB will start easing its monetary policy next spring as inflation continues to moderate in the Eurozone. Both the 2-year and 10-year German government note yields dropped sharply in recent days to 2.80% and 2.27%, well below the ECB’s 4.00% deposit rate (Fig. 14).

Global Strategy: Go Home or Go Global? Joe and I continue to recommend overweighting the US in global portfolios. Europe should also be overweighted. We would remain underweighted in the emerging market economies—especially China, even though its stocks look relatively cheap at the current valuation of the China MSCI. On the other hand, India’s MSCI stock price index is at a record high partly because it is a primary beneficiary of China’s woes (Fig. 15). Here are a few related observations:

(1) The Stay-Home versus Go-Global MSCI stock price index ratios in dollars and in local currencies have been trending higher since 2010 (Fig. 16). Both are at or near their record highs during the 2021-22 period.

(2) Contributing to the outperformance of the US MSCI have been the various country indexes’ forward earnings (Fig. 17). The one for the US is up 264.3% since March 9, 2009, to a record high. Meanwhile, the other major market indexes’ forward earnings are up less than 100% over this period and have stalled below their record highs for the past two years. The US tends to have the highest forward profit margin of the major markets around the world (Fig. 18).

(3) The forward P/E of the US MSCI tends to be much higher than those of the other major MSCI markets (Fig. 19). That’s mostly because there are more growth stocks with higher valuation multiples in the former than in the latter. The forward P/E of the All Country World ex-US MSCI tends to track that of the S&P 500 Value index quite closely (Fig. 20). The two have diverged more than usual after the pandemic.

(4) The Emerging Market MSCI (in local currency) is highly correlated with the CRB raw industrials spot price index (in dollars) (Fig. 21). Given the lackluster outlook for global economic activity, industrial commodity prices are likely to remain depressed, suggesting not much upside for the Emerging Markets MSCI.

(5) The EMU MSCI, for the European Monetary Union, has been showing some relative strength in recent days as investors seem to believe that the ECB will be lowering interest rates before the Fed does so in 2024.

Hard Luck For Hard Landers

December 11 (Monday)

Check out the accompanying pdf and chart collection.

Executive Summary: The economy has proven resilient, defying all the reasons it shouldn’t be, to which diehard hard landers still cling. We expect that it will remain resilient and that inflation will continue to fall to the Fed’s target (a.k.a. “immaculate disinflation”). In this scenario, the Fed won’t be rushing to ease and won’t ease by much. The Fed’s policy stance is perhaps better cast as “normalizing” than tightening that requires undoing. … Labor market supply and demand are coming into better balance, as the Fed would like, though November employment data attest to the labor market’s continued strength. … Also: What to make of the fact that GDI is weaker than GDP. … And: Dr. Ed reviews “Reptile” (+).

YRI Bulletin Board. We are planning on launching our new website at the end of this week on December 15. You might have noticed that we already have cut over to a new design for our charts. We think they are more user-friendly and sharper looking.

We will be recharging our batteries for the new year from December 19 to January 2. We won’t be publishing the Morning Briefing during that period, nor will there be Monday webcasts. We do intend to stay connected with our QuickTakes.

Join Dr. Ed’s live webcast with Q&A on Mondays at 11 a.m. EST. You will receive an email with the link one hour before showtime. Replays of the weekly webcasts are available here.

The Fed: Tightening or Merely Normalizing? Based on November’s employment report released on Friday, Debbie and I can safely conclude that there is still no sign of an impending recession. The Godot recession is still a no-show. Our soft-landing (a.k.a. rolling recession) scenario remains intact, as it has since early last year. The diehard hard landers are still expecting a recession, as they have been since the Fed started to tighten in early 2022. But they now expect it in 2024 and mostly think that it will be a shallow recession.

The widely anticipated recession scenario has been based on a very simple and logical premise: The Fed started raising interest rates aggressively last year during May. Short-term and long-term rates have increased by at least 500bps through the summer (Fig. 1). That shocking pivot, following a very long period of ultra-easy monetary policy, must be a terrible shock for the economy, the thinking goes. While the “long and variable lags in monetary policy” have turned out to be longer and more variable this time, a recession will surely occur in 2024, the hard landers figure.

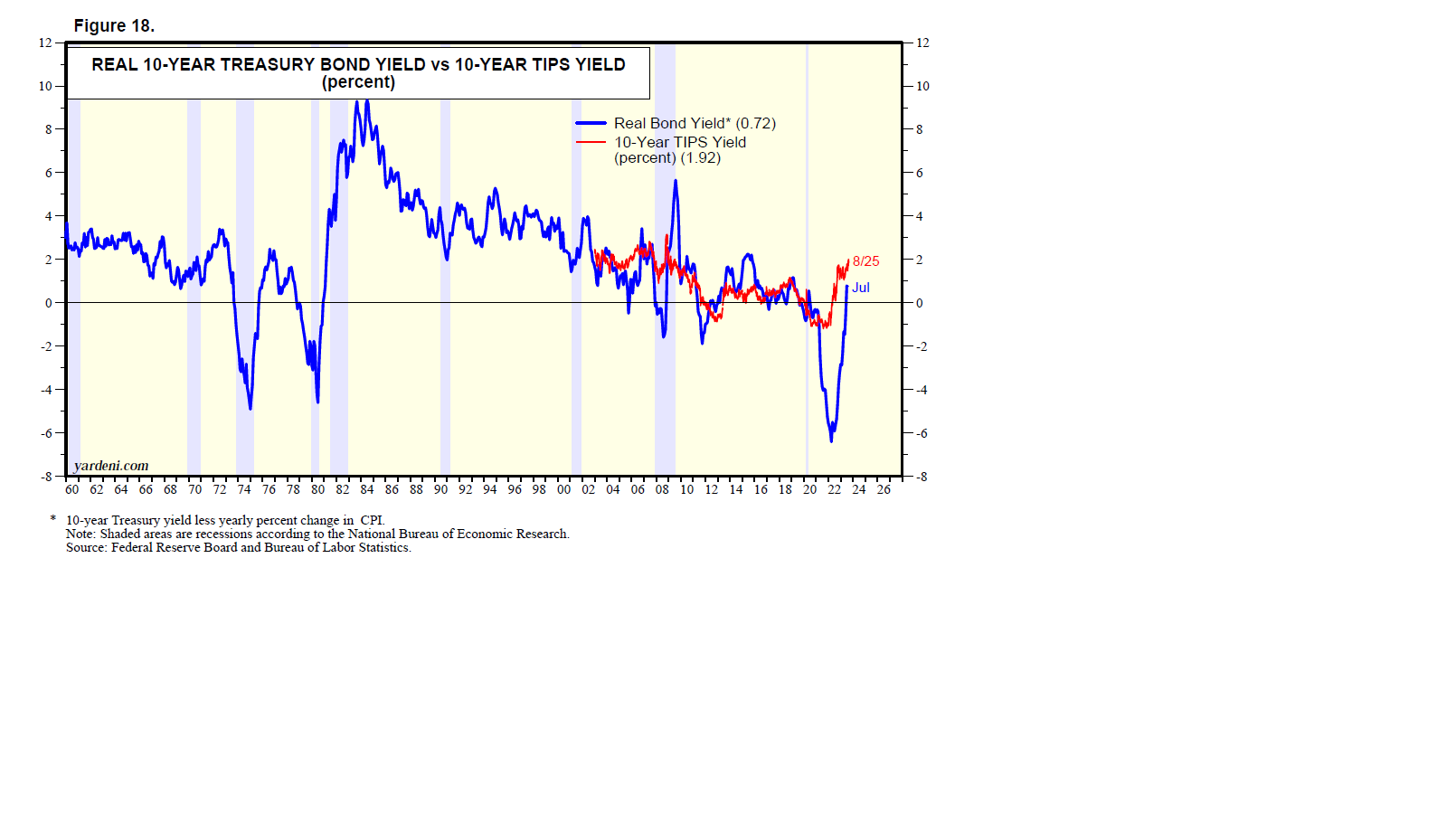

Additionally, the hard landers point out: The yield curve has been inverted since the summer of 2022 (Fig. 2). The Index of Leading Economic Indicators has been falling since it peaked at a record high during December 2021 (Fig. 3). The y/y growth rate of real M2 has been negative since May 2022 (Fig. 4). The real federal funds rate has soared from -8.46% during March 2022 to 2.09% during October (Fig. 5). All of them have been mostly accurate leading indicators of recessions in the past.

Yet contrary to this plausible argument, the economy has remained resilient and avoided a recession so far. Here we are in December 2023, and the unemployment rate remains below 4.0%. Full-time employment is at a record high (Fig. 6). So is payroll employment, which is one of the four components of the Index of Coincident Economic indicators (CEI). It is the first to come out every month and suggests that the CEI rose to yet another new record high in November, confounding the LEI’s followers (Fig. 7).

In recent months, we’ve provided several explanations for why the hard landers and their indicators have been wrong so far. (See, for example, “Captain America,” title of our November 8, 2023 Morning Briefing.) Here’s a new one: Perhaps the Fed hasn’t been tightening monetary policy so much as normalizing it. Interest rates are back to the Old Normal. They are back to where they were before the New Abnormal period between the Great Financial Crisis and the Great Virus Crisis, during which the Fed pegged interest rates near zero.

The normalization theory implies that the Fed might not lower interest rates next year as much as widely expected. That’s because the economy wouldn’t require as much easing to reverse the tightening after the tightening has done its job of bringing down inflation. If the economy remains resilient but inflation continues to fall closer to the Fed’s 2.0% target next year—both of which we’re expecting—then the Fed might lower the federal funds rate twice next year, by 25bps each time, instead of four times or more as widely anticipated. After Friday’s employment report, this was less widely anticipated.

US Labor Market I: Working for a Living. Friday’s employment report was bullish for November’s real personal income, real retail sales, and CEI. Each month when the report is released, Debbie and I calculate our Earned Income Proxy (EIP) for private-sector wages and salaries in personal income. All three of its components registered gains: Payroll employment in the private sector rose 0.1%, average weekly hours increased 0.3%, and average hourly earnings gained 0.4%.

So our EIP rose 0.8% m/m during November (Fig. 8). That undoubtedly well exceeded the month’s inflation rate, boosting the purchasing power of consumers. That should be reflected in a solid increase in the month’s retail sales and CEI.

Here are some other signs of labor market strength in November’s employment report:

(1) The household measure of employment also rose to a record high last month. In fact, it jumped by 747,000 to 162.0 million. Its full-employment component rose 347,000 to a record-high 134.8 million.

(2) The increase in household employment exceeded the 532,000 increase in the labor force. So the number of unemployed workers fell by 215,000 last month to 6.3 million (Fig. 9). The average duration of unemployment fell 10.2% to 19.4 weeks (Fig. 10).

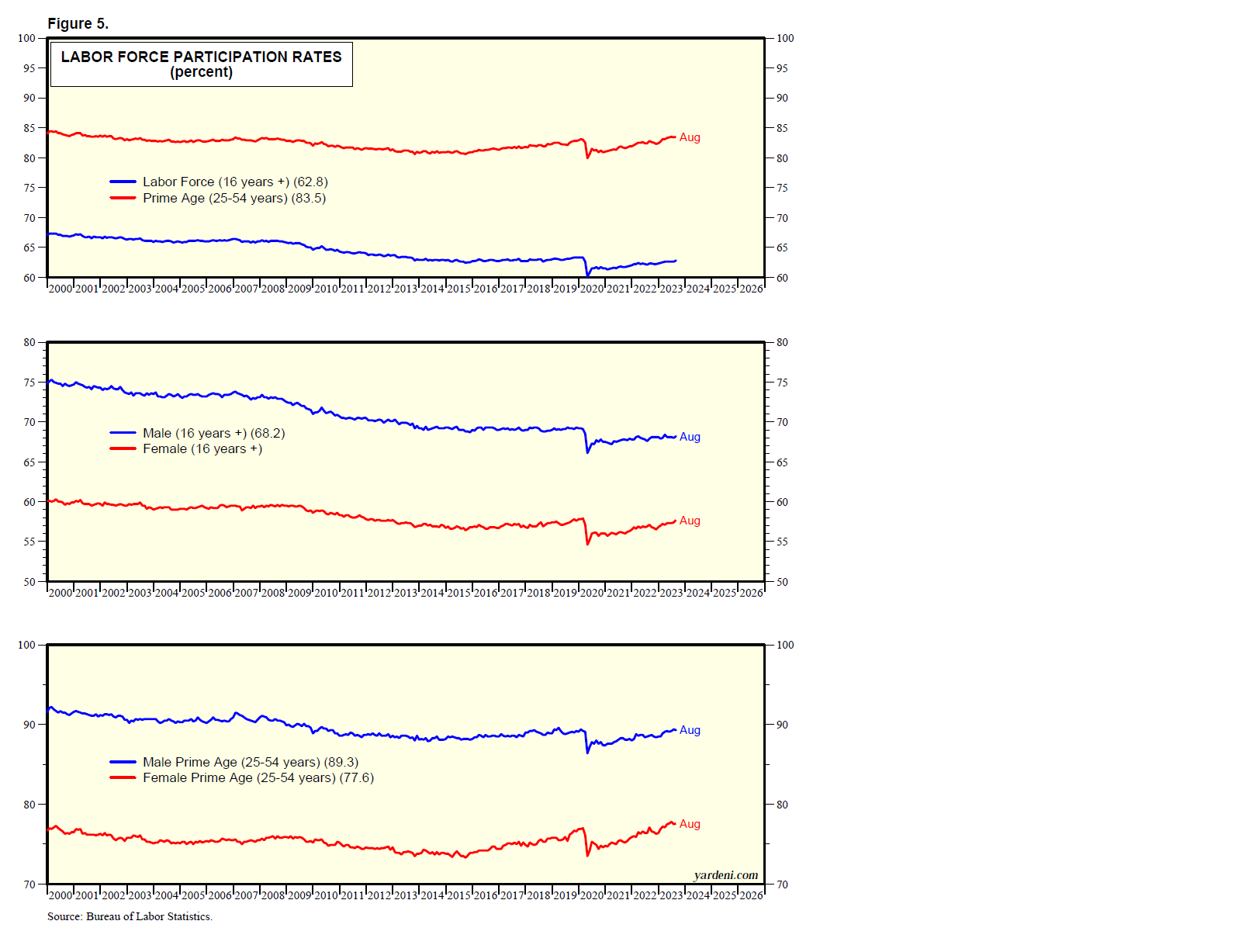

(3) The labor force participation rate rose to 62.8%, matching its highest readings since February 2020 (Fig. 11). Despite the sharp increase in the labor force, the unemployment rate fell to 3.7%. It was down to just 3.4% for adults (Fig. 12).

(4) A closer look at the payroll measure of employment shows that lots of industries reported record payrolls along with the total measure. Particularly strong gains continue to be reported by private education & health services (99,000) and leisure & hospitality (40,000) (Fig. 13). On the other hand, the retail trade payroll count was particularly weak during November (-38,400).

US Labor Market II: Real Pay Gains. In the past, Fed Chair Jerome Powell has indicated that wage inflation would probably have to slow to 3.0% (from 4.0%-5.0% currently) to get to the Fed’s 2.0% target for price inflation. He addressed this issue in a November 30, 2022 speech titled “Inflation and the Labor Market.” Powell observed: “In the labor market, demand for workers far exceeds the supply of available workers, and nominal wages have been growing at a pace well above what would be consistent with 2 percent inflation over time. Thus, another condition we are looking for is the restoration of balance between supply and demand in the labor market.”

That seems to be happening. Consider the following:

(1) Supply and demand. In his speech at the end of last year, Powell presented a clever chart showing the supply of labor as the labor force, and the demand for labor as the sum of employment plus job openings (with the latter pushed ahead by one month) (Fig. 14). It is showing that the demand for labor is down 700,000 since the start of the year, while the supply has increased by 2.5 million. Demand still exceeds supply by 2.4 million workers, but that’s down from a peak of 6.1 million during April 2022.

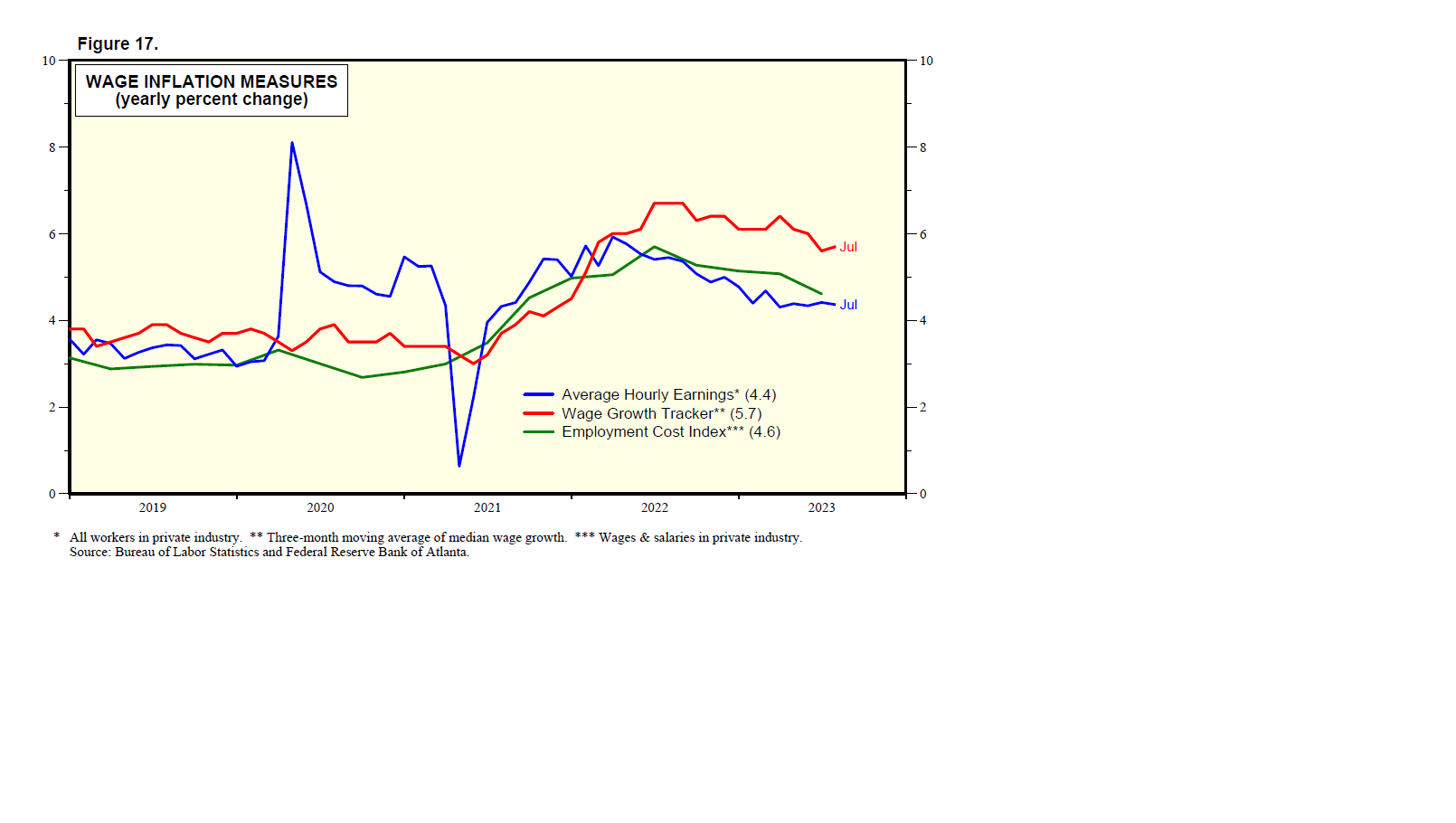

(2) Wages. Average hourly earnings (AHE) continued to moderate in November. It was down to 4.0% and 4.3% for all private-sector workers and for production and nonsupervisory workers (lower-wage workers), who account for about 80% of payroll employment. The AHE of higher-wage workers has been bouncing around 3.0% y/y since early 2022 (Fig. 15).

US Economy: GDP vs GDI. Then again: USA TODAY Economics and Jobs Reporter Paul Davidson observed in a December 1 story that while Q3’s real GDP was revised up to an annual rate of 5.2%, real gross domestic income (GDI) is up just 1.5%. It “has grown feebly over the past year even while GDP has advanced solidly. Over the past four quarters, GDP has increased 3% while GDI has fallen 0.16%.” Davidson concluded that maybe the economy “isn’t so resilient after all.”

In theory, GDP should equal GDI since the former measures the demand for goods and services, while the latter measures the income available for purchasing those very same goods and services. In practice, there is always a statistical discrepancy. During Q3, real GDP was 2.6% higher than real GDI, the highest discrepancy since 1993 (Fig. 16).

The discrepancy is even greater between nonfarm business output (NFBO), which jumped 6.1% (saar) during Q3, and GDI. The former is the series used to measure productivity.

(Business sector output is a chain-type, current-weighted index constructed after excluding from GDP the following outputs: general government, nonprofit institutions, and households [including owner-occupied housing]. Nonfarm business, which excludes farming, accounted for about 76% of GDP in 2022.)

So which is it? Are the economy and productivity as resilient and strong as suggested by NFBO and GDP, or are they both as weak as suggested by GDI? Economists tend to pick data that support their story. The hard landers love the GDI story. We are prone to that bias, but we do our best to be balanced and tell you both sides of the story, as we are doing now. Some economists simply take the average of GDP and GDI. For now, we see plenty of evidence to stick with our views that the economy is resilient and productivity growth is making a comeback. The stock market seems to agree with us.

Movie. “Reptile” (+) (link) stars Benicio Monserrate Rafael del Toro Sánchez in this crime drama, which is almost as long as his name. The plot is interesting but is a bit too slow paced. Then again, Del Toro is always fun to watch. His understated intensity is ever-present in the roles he plays. This movie is about a murder, real estate agents, drugs, and cops. Alicia Silverstone and Justin Timberlake have parts, but they don’t add much to the movie.

Onshoring, Acquisitions & Octopus

December 07 (Thursday)

Check out the accompanying pdf and chart collection.

Executive Summary: Federal incentives promoting the onshoring of manufacturing plants have certainly hit their mark in Arizona and New York. Both states are sprouting new regional semiconductor manufacturing ecosystems, Jackie reports, dramatically boosting local economic development. … Also: Financial firms with investment banking operations report a pickup in M&A, a trend that should only accelerate when the interest-rate environment stabilizes. … And our Disruptive Technologies focus today is on Octopus Energy, a British company with an innovative business model that rewards green electricity consumption.

Industrials: Onshoring’s Ripple Effects. In phase one of the onshoring wave, many large companies announced plans to take advantage of tax breaks and open new manufacturing facilities in the US. Manufacturers in the solar, semiconductor, and chemical industries have been among the most aggressive in taking advantage of so-called Bidenbucks, the dollars and tax breaks available through the CHIPS and Science Act, the Inflation Reduction Act, and the Infrastructure Investment and Jobs Act.

Now comes phase two. Suppliers are following their large customers and building new manufacturing plants in the US of A as well. The process is well underway in Arizona, where Taiwan Semiconductor Manufacturing is spending $40 billion to build two massive plants, the first of which is expected to open in 2025. In upstate New York, where Micron Technologies has committed to building four plants, the green shoots are visible as well.

The development of these new semiconductor ecosystems as well as manufacturing plants in other industries has contributed to the surge in spending on manufacturing structures. It was up 66.4% y/y during Q3 to a record high; in the first three quarters of 2023, such spending rose 43.3% y/y (Fig. 1). That strength has boosted new orders for construction equipment, which rose 6.7% y/y during October to the fourth highest reading on record (Fig. 2).

All this building has led to more jobs. The number of Americans working in manufacturing has risen to 13.0 million as of October, according to the Labor Department. That’s higher than the prior peak in 2019 and brings manufacturing employment back to a level last seen in 2008 (Fig. 3). Likewise, record numbers of folks are working in heavy and civil engineering construction, 1.1 million in October, and in construction, 8.0 million as of October (Fig. 4 and Fig. 5).

Here’s a look at some of the companies building the semiconductor ecosystems in Arizona and New York:

(1) Arizona’s success story. Taiwan Semiconductor first announced plans to build a $12 billion semiconductor plant in Arizona in 2020. Two years later, it doubled down, expanding that project to two plants costing $40 billion. The project hit some bumps this summer, with squabbles erupting over workers being brought in from Taiwan and the opening pushed back a year to 2025; but otherwise, it’s progressing. Intel is also in the process of building two fabs in Arizona with a $20 billion price tag.

These huge commitments have given suppliers confidence to move to Arizona as well. Since the Taiwan Semi news, 27 semiconductor industry-related companies have announced plans to move to the Phoenix area or have bought or leased property there, a September 10 article on azcentral.com reported. The new businesses have attracted new residents, and builders are building new apartment units to house them.

One semi supplier is Solvay, which announced plans last year to invest in a new facility to produce electronic-grade hydrogen peroxide that cleans silicon wafers, a July 26, 2022 company press release stated. The company, which has other factories in the US, purchased 25 acres of land in Arizona and planned to begin construction this year. Taiwan-based Chang Chun also announced plans in 2022 to produce in Arizona electronic-grade hydrogen peroxide and other solutions for the semiconductor industry. Its first US manufacturing facility is expected to cost $300 million and create 200 jobs.

Yield Engineering Systems develops and manufactures thermal, deposition, and wet process equipment used in semiconductor, life sciences, and display manufacturing. It leased a 123,000-square-foot facility in Arizona in May 2022 to house operations that cater to the semiconductor industry, a May 2022 press release from the local municipality states. The ribbon-cutting was in July 2023.

KPCT Advanced Chemicals, a joint venture between Taiwan-based Kanto Group and Chemtrade Logistics in the US, is building an electronic-grade sulphuric acid manufacturing plant in Arizona over 10 acres. It too will supply the semiconductor industry and is expected to be operational by 2025, a November 2022 press release from the Arizona Commerce Authority states.

Many other industries are building new factories in the state as well. Arizona boasts a $675 million plant being built by Nestle USA to produce creamers. Virgin Galactic is building a manufacturing facility to produce as many as six Delta-class spaceships per year. Proctor & Gamble is building a $500 million manufacturing plant to support its fabric care business by 2025, a January 10 article in Engineering News Record.

(2) Upstate NY bets on semis. Manufacturers like General Electric, Kodak, and Carrier have exited or sharply reduced their operations in the upstate New York area in recent decades, forcing many folks relocate if they want to make a decent living. So it was big news when Micron Technology announced in October 2022 that it would spend $100 billion over the next 20 years to build semiconductor plants in Clay, New York, just north of Syracuse. Construction is expected to begin in 2024 on the first of four plants that should be operational by 2030 and employ 3,000 people directly.

Micron anticipates hiring 9,000 people eventually, when all the fabs are constructed, and 41,000 additional jobs are expected to be created by other businesses supplying the company and its employees with everything from materials to maintenance and restaurants, a July 6 MIT Technology Review article reported.

A handful of other semiconductor businesses have cropped up in upstate New York as well. In November 2022, Edwards Vacuum, a UK-based manufacturer of vacuum and abatement equipment for the semiconductor industry, announced plans to develop a $319 million dry pump manufacturing facility in Genesee County, about two hours west of Clay. That follows the April 2022 opening of Wolfspeed’s $1 billion silicon carbide chip plant north of Utica. The chips initially will be used in electric vehicles (EVs) produced by Lucid and General Motors, a May 2, 2022 article in the Utica Observer-Dispatch reported.

New York State is hopeful that more semi suppliers will brave the New York winters. Governor Kathy Hochul announced $40 million in grants to develop shovel-ready tracks of land on which semiconductor suppliers could build plants. “Employers want to know that the permits are in place, the infrastructure is right, and work can begin almost immediately because time is money," Hochul said according to an August 15 article on WXXI News.

To help meet the region’s future need for qualified labor, Syracuse University plans to expand funding for its College of Engineering and Computer Science by 50% over the next five years or so. Onondaga Community College is also creating two new degree programs.

Time will tell whether New York is as successful as Arizona.

(3) Industrials benefit. All this manufacturing activity has helped boost the S&P 500 Industrial sector’s stock price index by 9.6% ytd through Tuesday’s close. Here’s how Industrials’ ytd performance stacks up against that of the S&P 500 and its other sectors: Information Technology (50.2%), Communication Services (45.3), Consumer Discretionary (34.5), S&P 500 (19.0), Industrials (9.6), Financials (4.7), Materials (4.1), Real Estate (2.5), Health Care (-3.3), Consumer Staples (-4.8), Energy (-6.2), and Utilities (-11.7) (Fig. 6).

The Industrials sector would have performed even more admirably had it not been dragged down by some of the defense contractors, airlines, and air freight & logistics industries. Here’s how some of the best performing industries within Industrials have fared ytd through Tuesday’s close: Industrial Machinery (16.0%), Electrical Components & Equipment (15.9), Industrial Conglomerates (14.1), Construction Machinery & Heavy Trucks (11.5), and Aerospace & Defense (0.4) (Fig. 7).

The S&P 500 Industrials sector is expected to grow revenue by 4.3% this year and 4.8% in 2024, while earnings for the sector are projected to increase 14.2% in 2023 and 11.1% next year (Fig. 8 and Fig. 9). The sector’s forward P/E, at 18.4, is toward the upper end of its range of 11 to 26 over the last decade (Fig. 10).

Financials: A Glimmer of Hope. In recent days and weeks, we’ve noticed that reports of large mergers and acquisitions (M&A) seem to have picked up. Executives at some of the largest banks, while still couching their comments, sounded just a touch more optimistic about the M&A deal environment as well.

“M&A deals are coming a little faster," Bank of America CEO Brian Moynihan told a Goldman Sachs conference, a Reuters article reported on Tuesday. As the interest-rate environment stabilizes, there will be more scope for dealmaking, he added. The bank’s investment banking fees of about $1 billion in the current quarter will be down y/y at percentages in the low single digits but are still expected to outperform the industry average.

Goldman Sachs CFO Denis Coleman said that a lot of clients have appetites for strategic deals but that the high cost of funding has kept private equity firms cautious about undertaking them, Reuters reported.

Here are some of the deals that caught our attention in a wide array of industries:

(1) Health care. Cigna is in merger talks with Humana to create a $140 billion giant that combines a huge pharmacy benefit management operation with the second largest Medicare Advantage business. Roche agreed earlier this month to buy Carmot Therapeutics, an obesity drug developer, for $2.7 billion. Meanwhile, AbbVie is paying $10.1 billion in cash to buy ImmuoGen, which has an antibody drug that fights ovarian cancer.

(2) Oil patch. Occidental Petroleum is reportedly in talks to buy shale company CrownRock. Meanwhile, ExxonMobil has offered to acquire Pioneer Natural Resources for $59.5 billion in stock, but the deal could face a bumpy road if the Federal Trade Commission’s recent request for additional information is any indication.

(3) Airlines. Alaska Air Group has offered $1.9 billion to acquire Hawaiian Airlines. The offer was made even as the Justice Department sued to block JetBlue Airways’ $3.8 billion offer to buy Spirit Airlines. The parties are awaiting a judge’s decision.

(4) Odds ’n ends. Steel manufacturer Cleveland-Cliffs is in negotiations to buy US Steel, while Neiman Marcus has turned down Saks Fifth Avenue’s $3 billion acquisition offer after months of negotiations. Talks between the two retailers reportedly continue.

Disruptive Technologies: Introducing Octopus. Windmills always seem to be painted white, so pictures of several purple and hot pink windmills towering outside of the Dubai venue of the big international climate change conference COP28 demanded further attention. They were installed by Octopus Energy, a privately held British company that’s trying to turn the electric industry on its head. It’s attempting to manage the intermittency of solar and wind energy by deploying storage solutions, incentivizing consumers to use electricity when renewable energy is at peak production, and rolling out smart software to manage it all.

The company has its tentacles in many different areas. Here’s a quick look at some of them:

(1) Green production. Octopus owns wind and solar projects in 15 countries, including the UK, France, Finland, Sweeden, and Australia. On Monday, it announced an agreement to develop up to five wind turbines and solar panels with batteries in Sierra Leone in partnership with actor Idris Elba and Siaka Steven’s development company, Sherbro Alliance Partners.

(2) Electricity provider. Octopus sells electricity to consumers and to businesses. It installs heat pumps, EV chargers, smart meters, and other hardware in residential homes. Consumers get the opportunity to invest in that local green energy generation; and if they live near a wind turbine, consumers can receive a 20% discount on electricity used when the wind is blowing most actively. The same goes for solar. The model incentivizes consumers to use electricity when it’s the most available and cheapest for Octopus to provide it.

The company is working with British property developers, telling them how many solar panels to put on a home and what sizes of battery, heat pump, and water heater are necessary to install. The company provides homeowners with a license to consume the solar energy provided and guarantees that they won’t receive an electric bill for 10 years.

(3) EV lessor. Another program Octopus offers gets EVs into consumers’ driveways. Companies can lease EVs from Octopus to offer as employee perks; employees can buy the EVs they’re using over time with a portion of their gross salary. As part of the deal, they receive a free home charger, insurance, car maintenance, and free home charging on the first 4,000 miles driven. The payroll deductions allow employees to save on National Insurance (the UK’s social security system) and income tax, the company’s website explains.

(4) Software manages it all. Perhaps Octopus’ most valuable arm is Kraken Technologies. It offers a software operating system that utilities use to manage and optimize energy production and consumption. Its software also manages customer information, billing, meter data management and offers AI-powered communication and automation.

Intelligent Octopus is a Kraken-powered retail offering that helps British customers max out their renewable electricity use when power is abundant and cheap. “Speaking on a panel at COP28, [Octopus Energy’s founder and CEO Greg Jackson] said that the previous day more than half a million Octopus customers were paid to use less electricity at peak times, which was ‘the equivalent of turning off the entire energy consumption of two cities,’” according to a December 4 article in the Australian Financial Review. As a result, Octopus doesn’t have to buy expensive coal-generated electricity during peak periods. It creates a “virtual power plant” that’s growing 24% m/m in the UK.

The company is selling the Kraken software internationally. On Tuesday, Octopus announced a trial with Abu Dhabi National Energy Company; and last June, the company struck its first US deal with Tenaska Power Services.

Over There & Over Here

December 06 (Wednesday)

Check out the accompanying pdf and chart collection.