Morning Briefing Archive (2021)

Santa vs the Two Grinches, Again

December 20 (Monday)

Check out the accompanying pdf and chart collection.

(1) Santa runs into turbulence. (2) The attack of the two variants. (3) Omicron is fast spreading, but less dangerous, especially to the vaccinated. (4) Will herd immunity be the outcome? (5) New cases soaring in Europe, but not hospitalizations, so far. (6) China faces the Omicron challenge. (7) The hawkish variant of the FOMC. (8) Levitating dot plot. (9) Waller says March is a “live meeting.” (10) Pivots and rotations. (11) A slimmed-down variant of Biden’s BBB likely to pass in early 2022. (12) People are disappearing in China, and so is retail sales growth. (13) Will China’s property bubble burst or just deflate? (14) Movie review: “Spencer” (+).

YRI Monday Webinar. There won’t be a webinar today, but please join Dr. Ed’s live Q&A webinar on most Mondays at 11 a.m. EST. You will receive an email with the link to the webinar one hour before showtime. Replays are available here.

Strategy I: The Two Grinches. Late last week, the Santa Claus rally ran into some turbulence as investors turned more risk averse. They were clearly spooked again by the two Grinches—the Omicron variant of Covid-19 and the hawkish variant of the FOMC. Consider the following developments:

(1) Fast-spreading Omicron variant. Might Santa be an asymptomatic carrier of the Omicron variant of Covid-19? That’s unlikely since he never gets sick this time of year. Others aren’t so lucky: In recent conversations with friends, we have been hearing that quite a few have contracted the variant but have either no symptoms or minor ones. And, yes, a few of them have been fully vaccinated, including with booster shots.

The media is onto the story, with lots of ominous headlines. Rarely mentioned is that Omicron seems to hit hardest mostly the unvaccinated and that it may be spreading herd immunity. If so, it may bring the pandemic to an end sooner rather than later. We know that the variant is spreading like wildfire. Initial reports were that it is far less dangerous than previous variants of the virus, especially to people who have been vaccinated. Recent accounts have raised some doubts about that conclusion. In other words, we don’t know very much about where the virus is taking us.

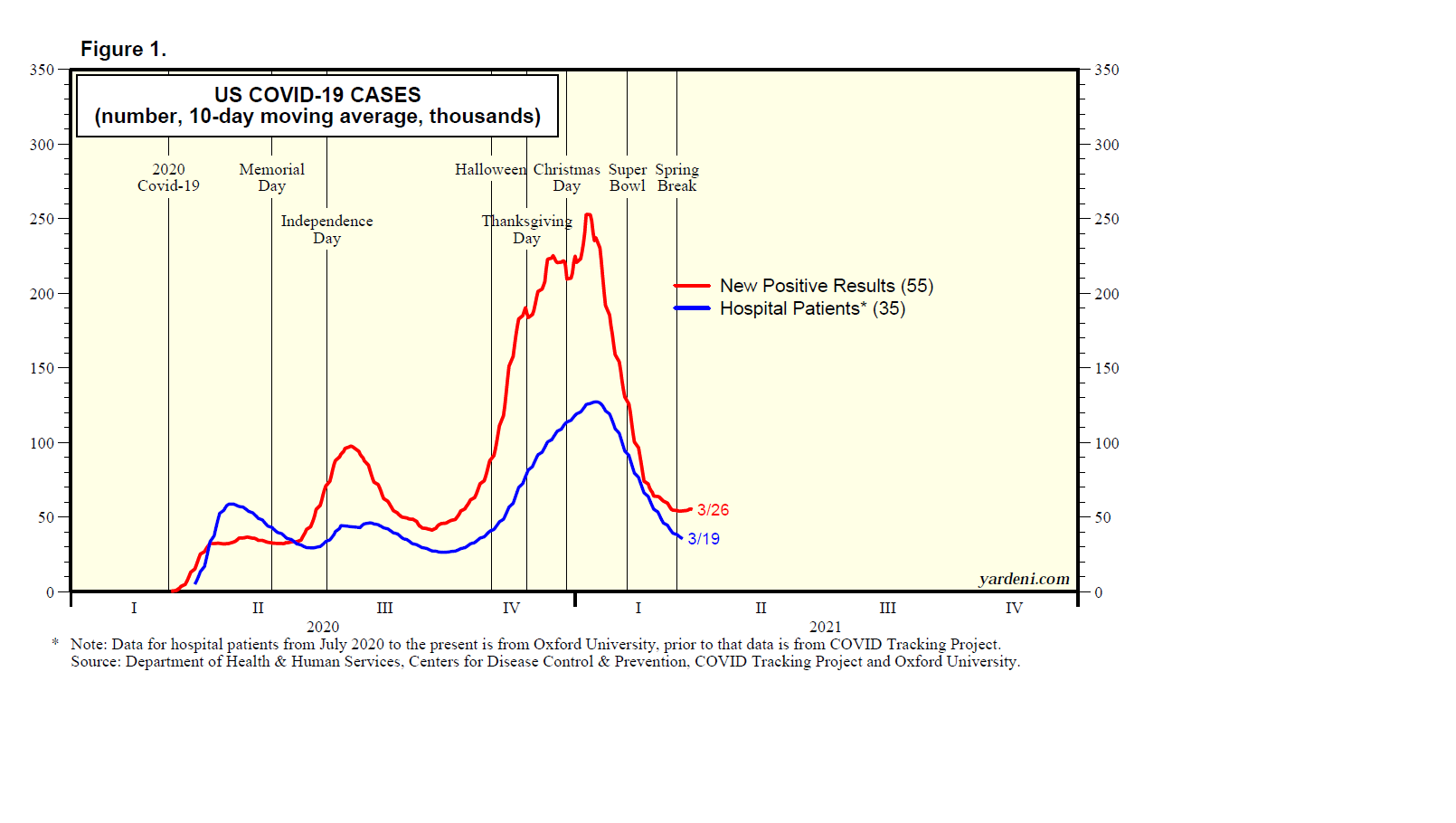

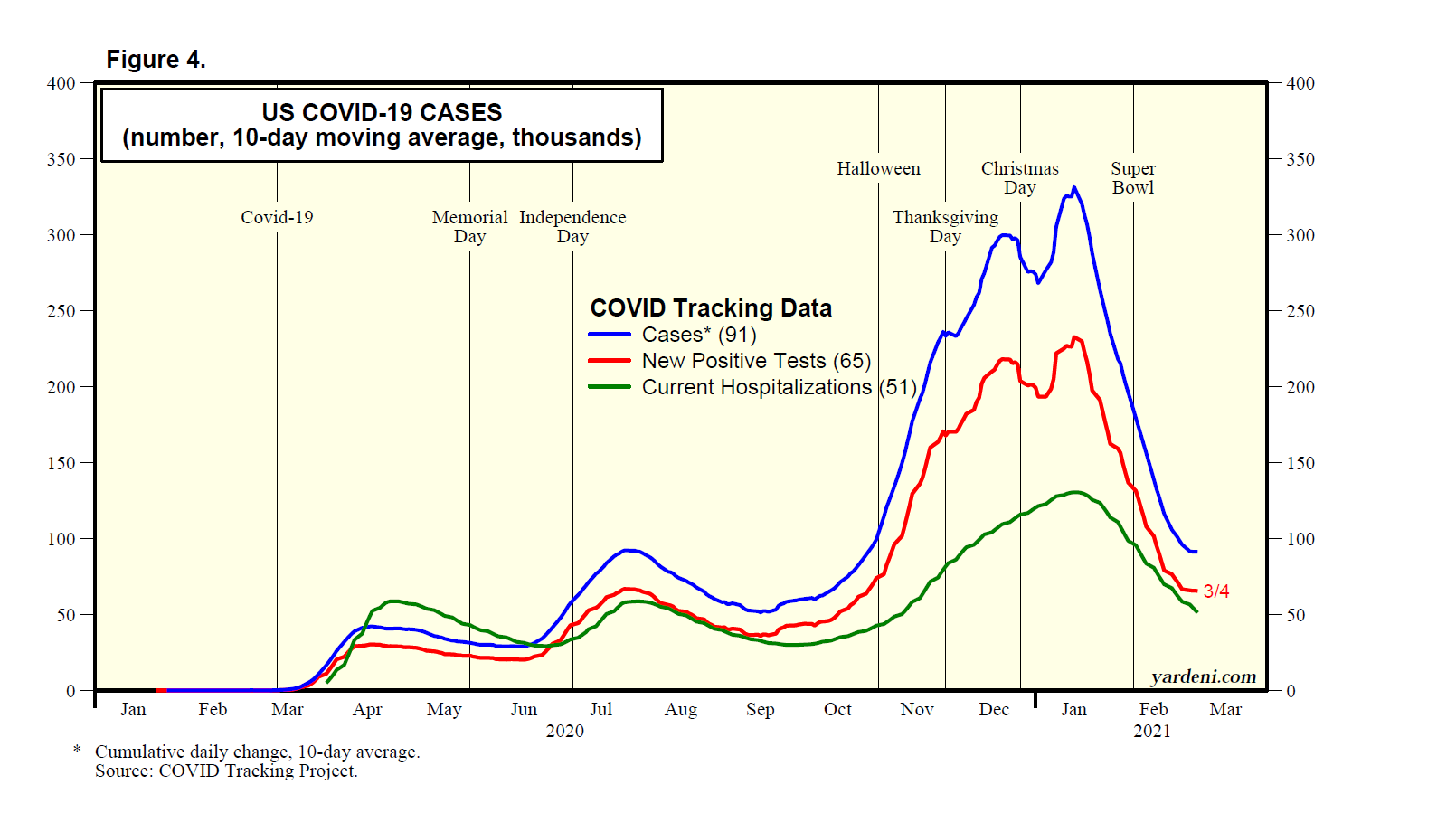

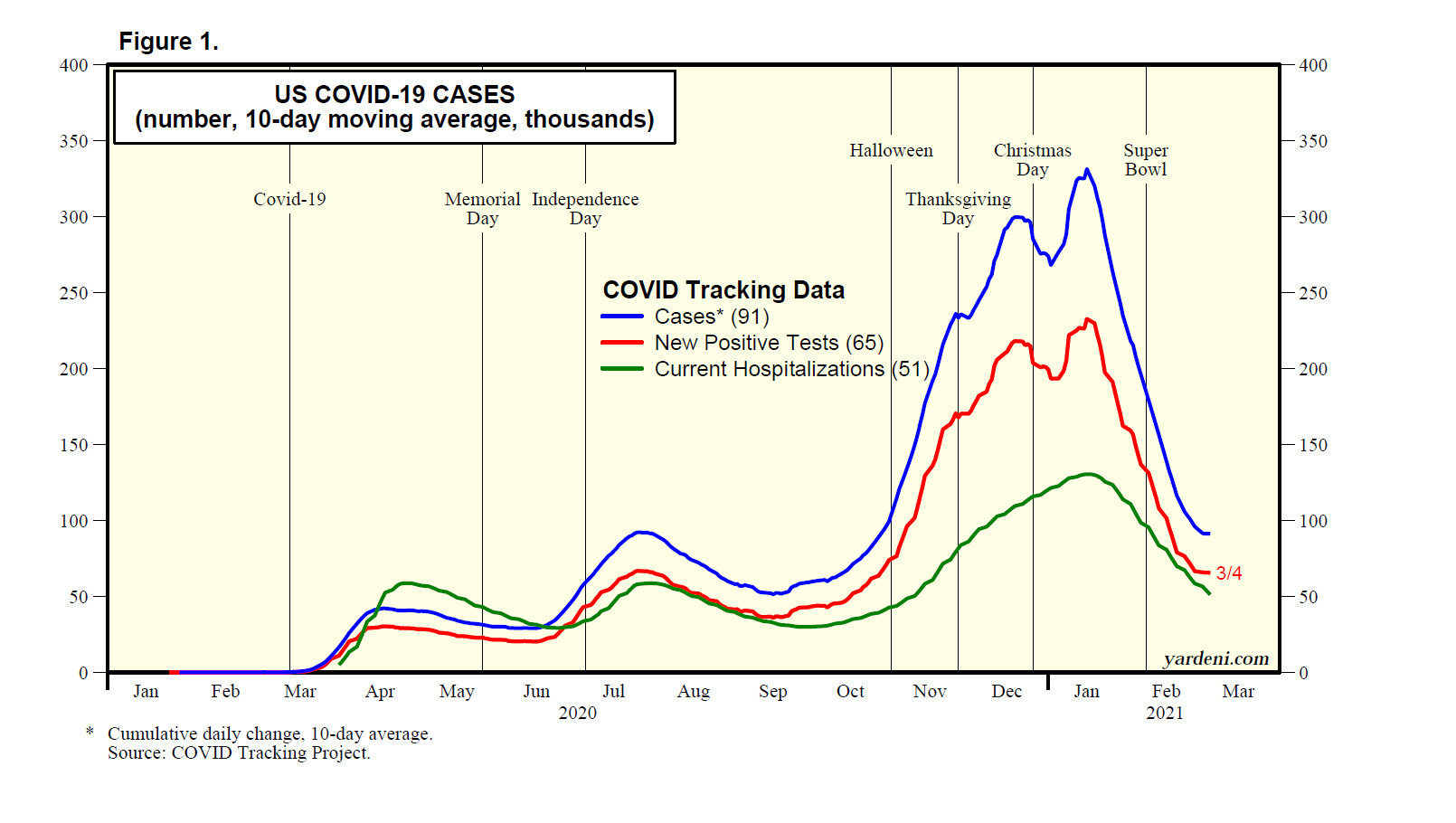

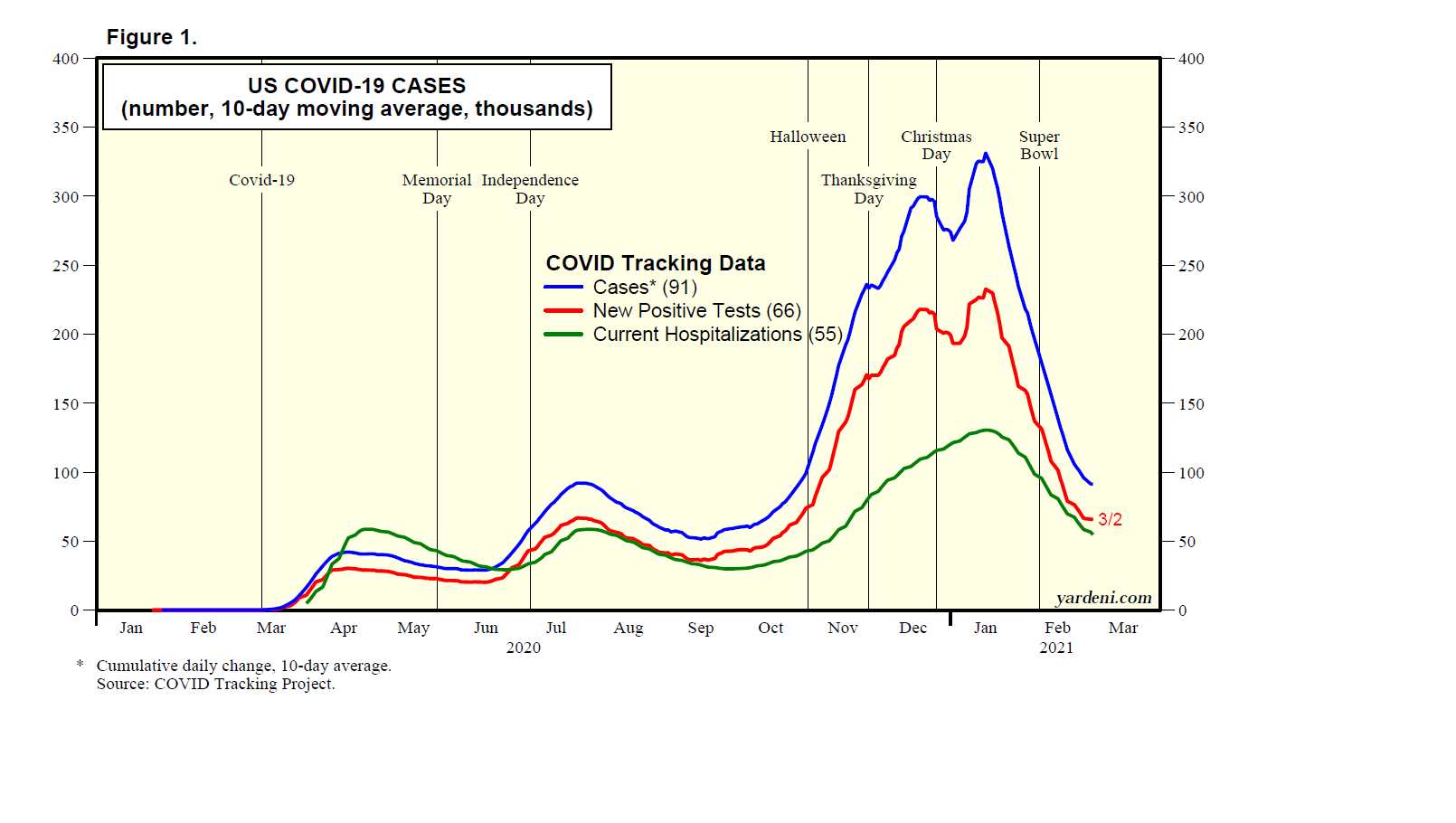

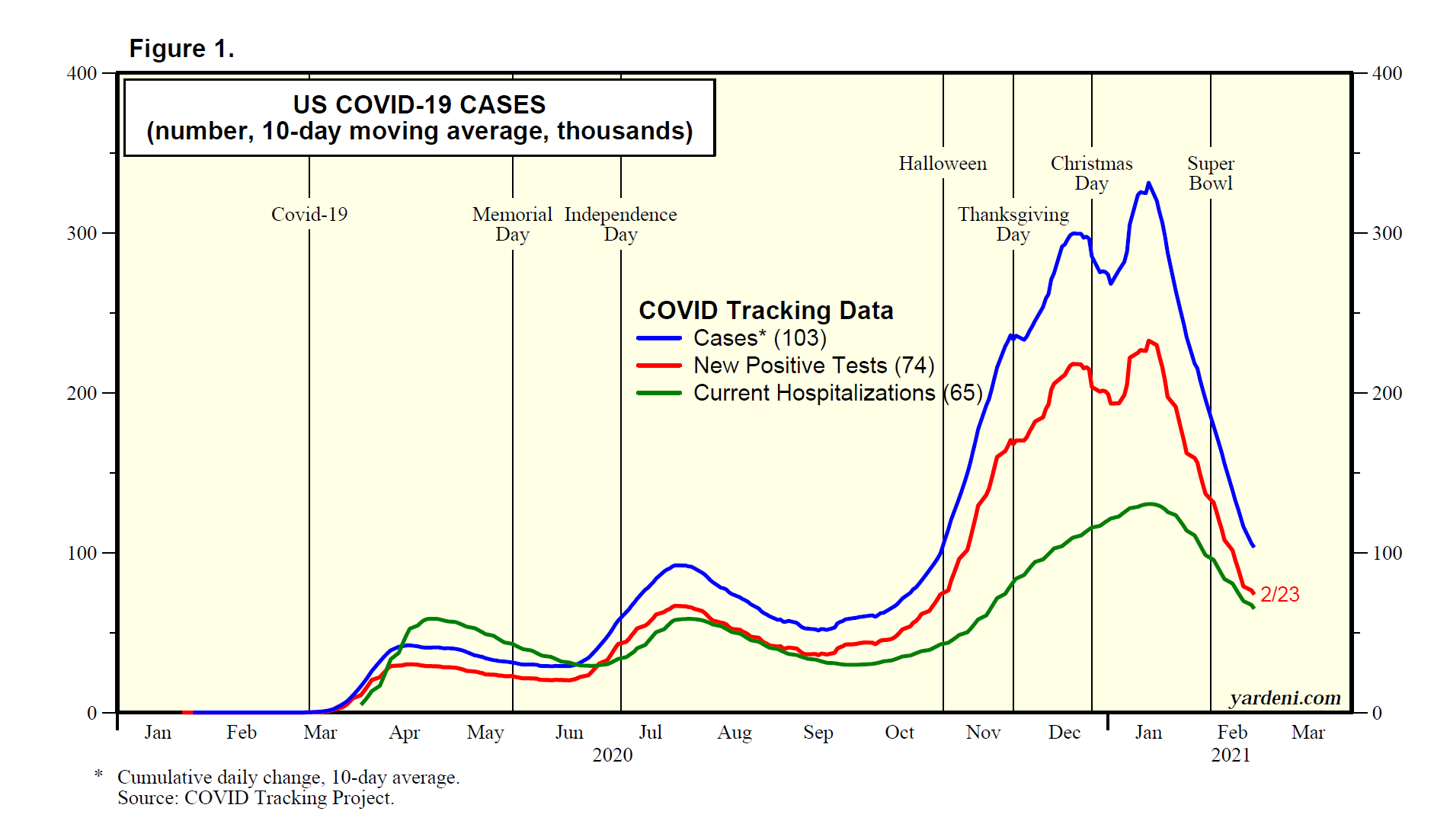

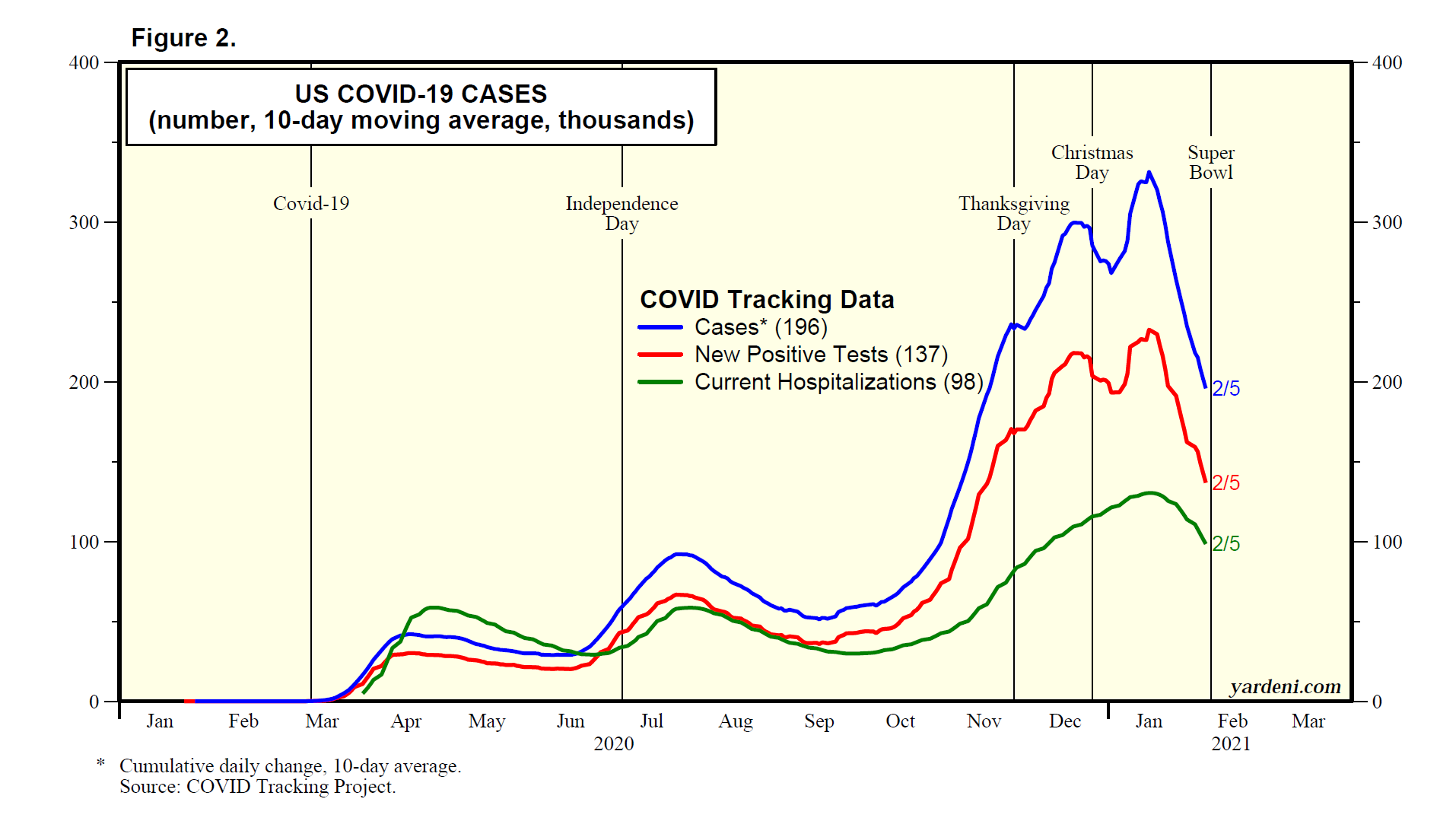

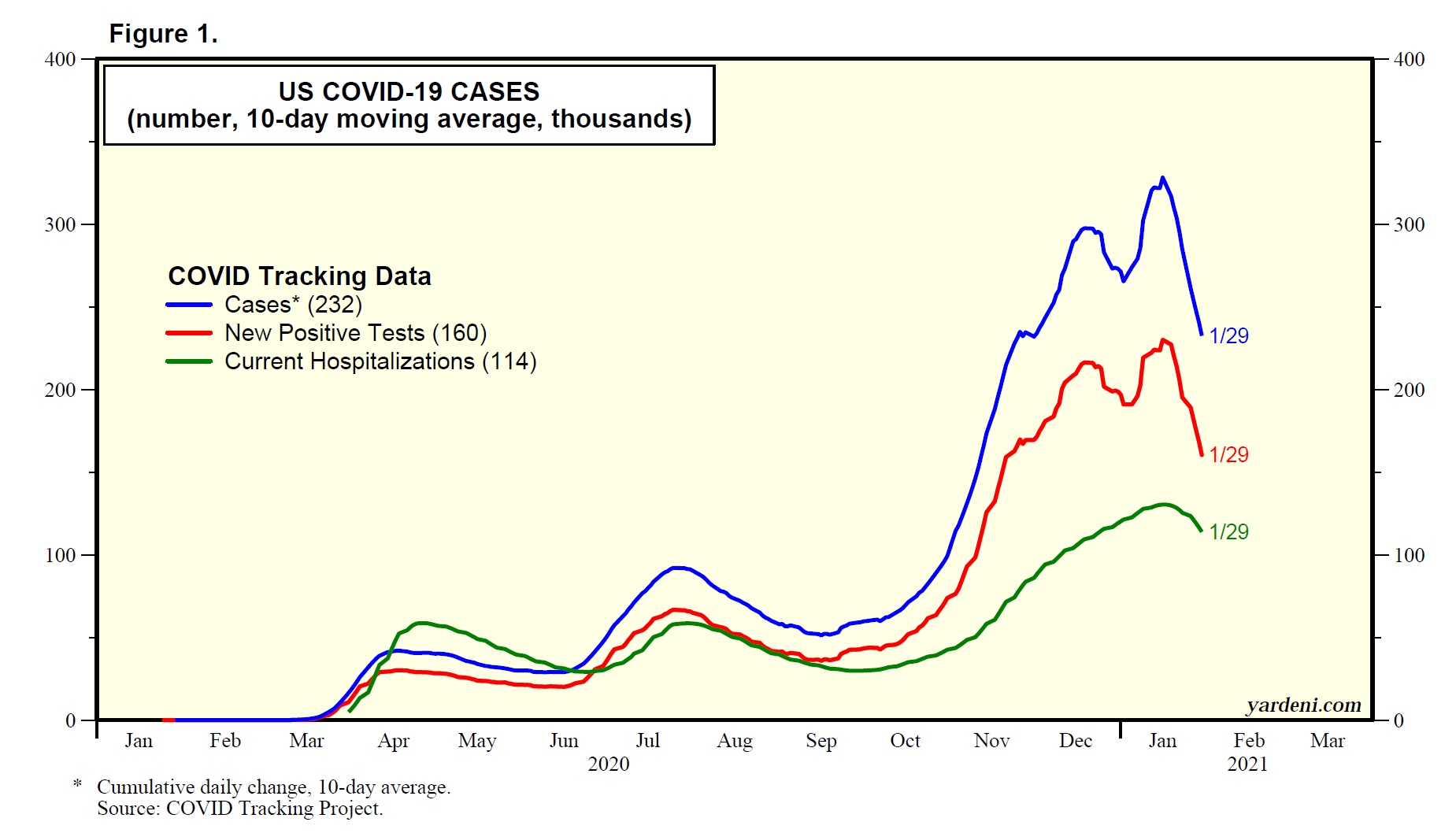

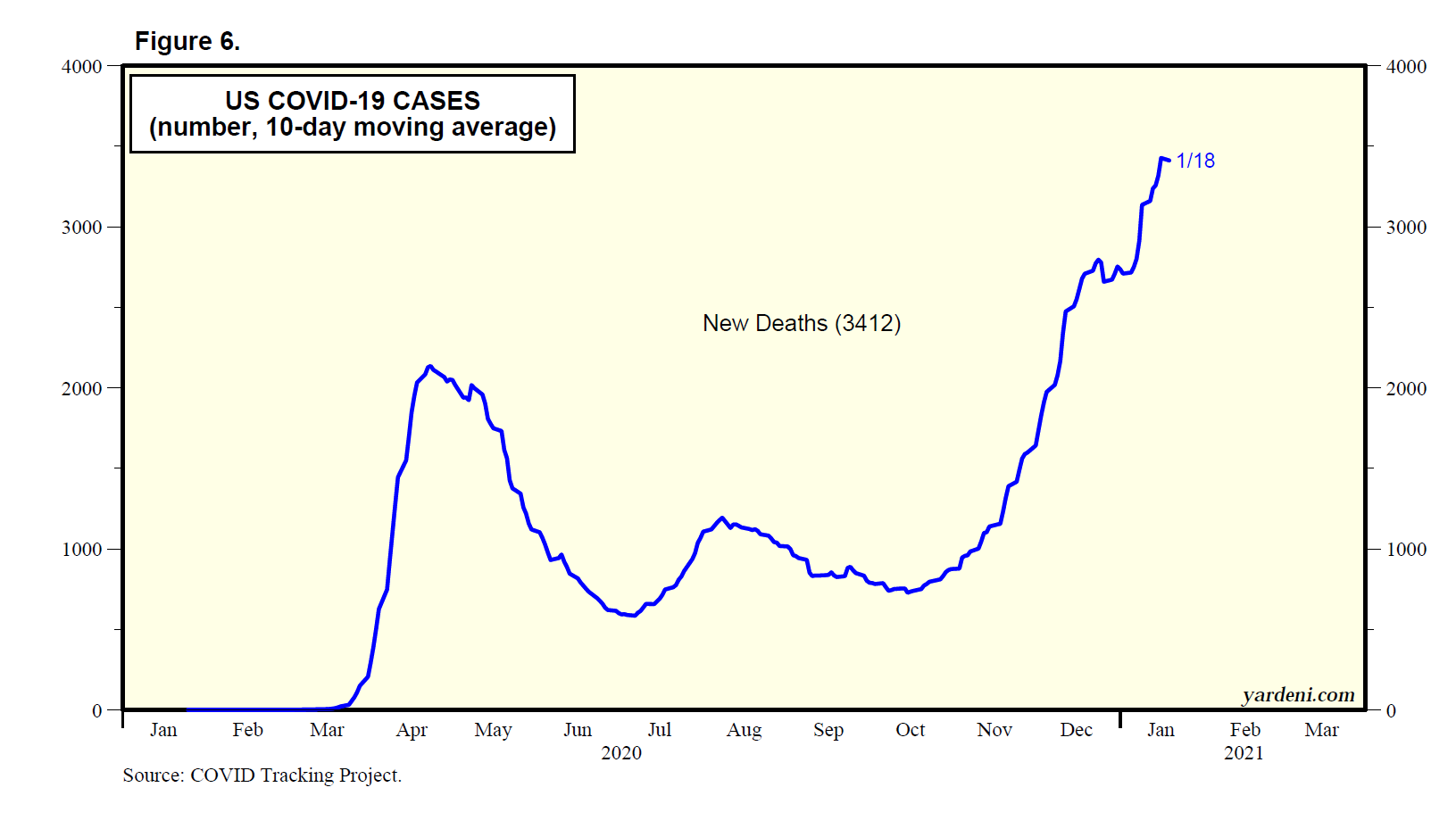

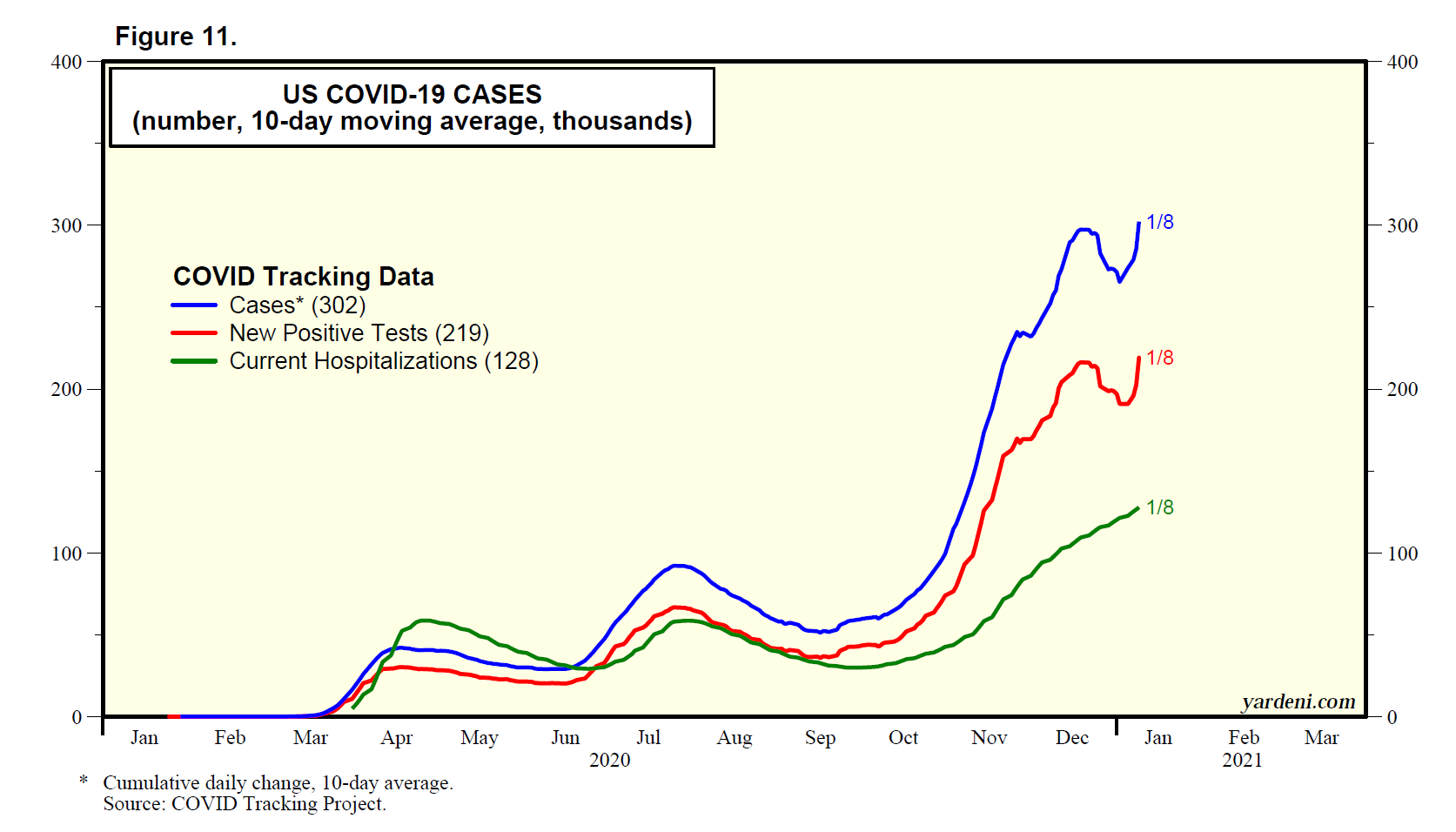

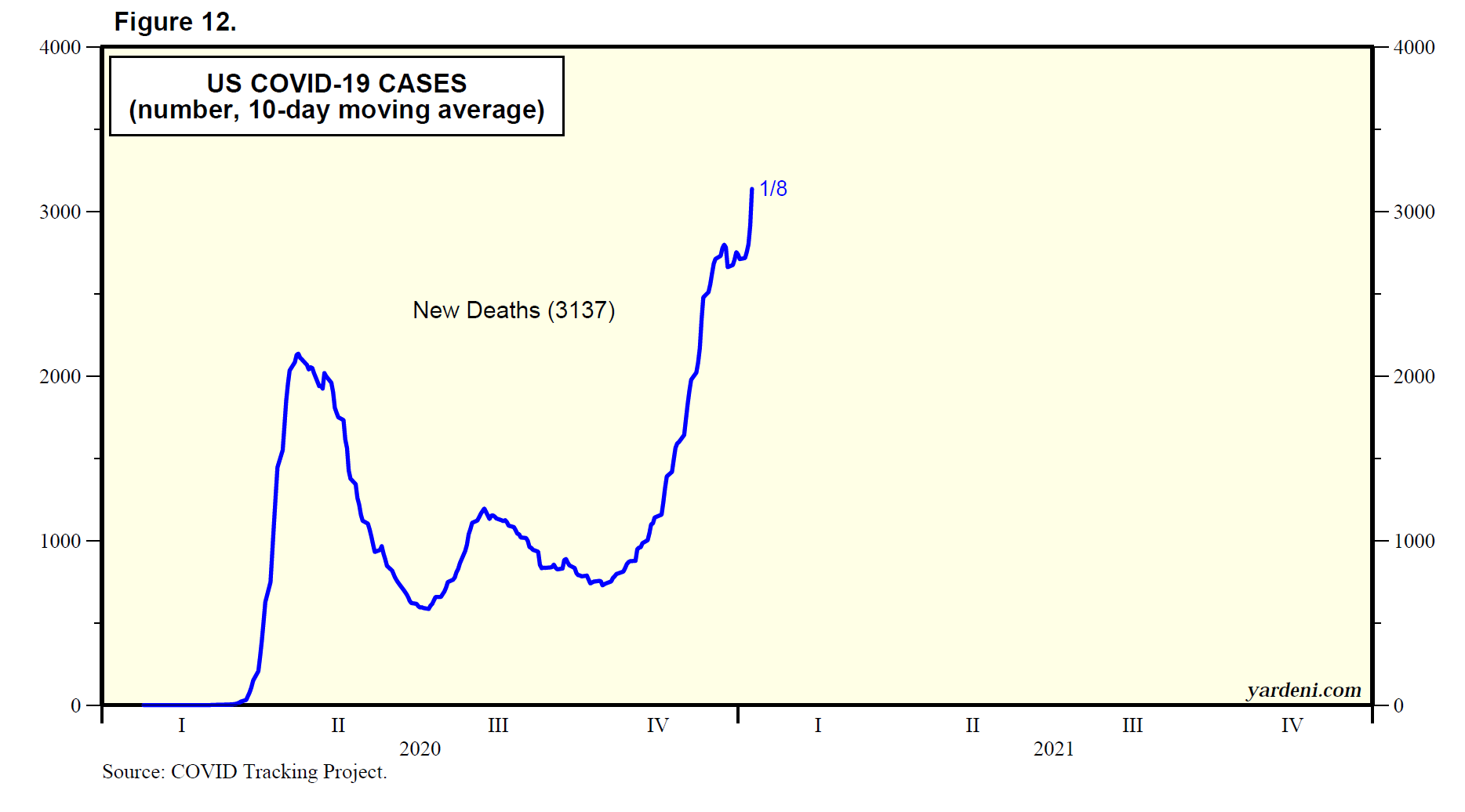

We should know more in coming weeks by comparing new cases to hospitalizations and deaths. In the US, there has been an upturn in both in recent days from recent lows (Fig. 1). The number of deaths continues to decline from its recent high (Fig. 2). Somewhat encouraging is that the recent jump in the count of new cases in the UK—to a pandemic-era record high—has yet to significantly boost hospitalizations (Fig. 3). New cases have been soaring in continental Europe too, but hospitalizations remain relatively low (Fig. 4 and Fig. 5).

It’s interesting to see that after a huge spike in India’s new cases during the spring of this year, the cases there have remained remarkably low in recent weeks (Fig. 6). Might that suggest some degree of herd immunity?

China’s new cases have remained extraordinarily low since the government imposed its zero-tolerance policies after the initial breakout of the pandemic over there during January and February 2020. However, the new Omicron variant may prove more challenging for China to contain. China has administered at least 2.6 billion doses of its killed-virus Covid vaccines, covering some 94% of the population. An October article in Nature noted that immunity from a double dose of the killed-virus vaccines wanes rapidly and that the protection given to older people may be limited. The Chinese vaccines aren’t as effective as mRNA vaccines.

(2) More hawkish FOMC variant. Last Wednesday, the FOMC turned more hawkish. The committee’s statement noted that the “path of the economy continues to depend on the course of the virus” and that progress on vaccinations should keep the economy growing. “With inflation having exceeded 2 percent for some time,” the FOMC decided to speed up the monthly pace of tapering its bond purchases from $15 billion to $30 billion starting in January. That presumably will set the stage for hiking the federal funds rate earlier next year.

Indeed, the Fed’s dot plot, released after the FOMC meeting on Wednesday, showed that all 18 members of the FOMC now expect at least one rate hike in 2022, up from only nine in September’s forecast. Moreover, 12 of them now see at least three quarter-point hikes during the year, and two think four increases will be necessary.

Contributing to Friday’s stock market selloff was Federal Reserve Governor Christopher Waller’s characterization of inflation as “alarmingly high” in a speech to the Forecasters Club of New York. He added that March’s FOMC meeting may be “a live meeting,” i.e., one in which a rate hike would be on the table.

Strategy II: Many Happy Returns? Santa’s sleigh is loaded with bags full of liquidity. The financial markets are trying to ascertain whether he has enough to drown the Grinches. Joe and I think so. Consider the following financial market reactions to the two Grinches this past week:

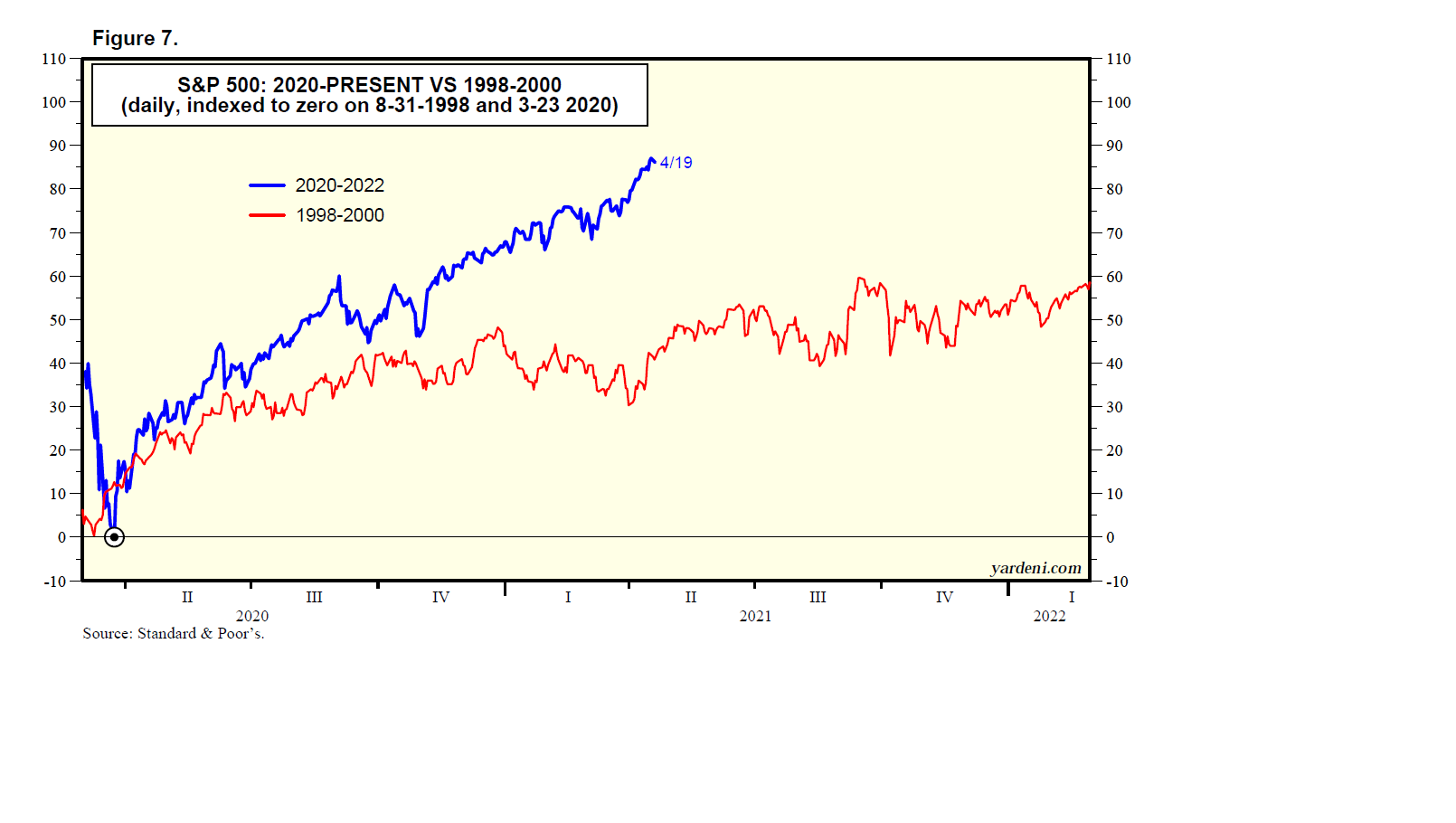

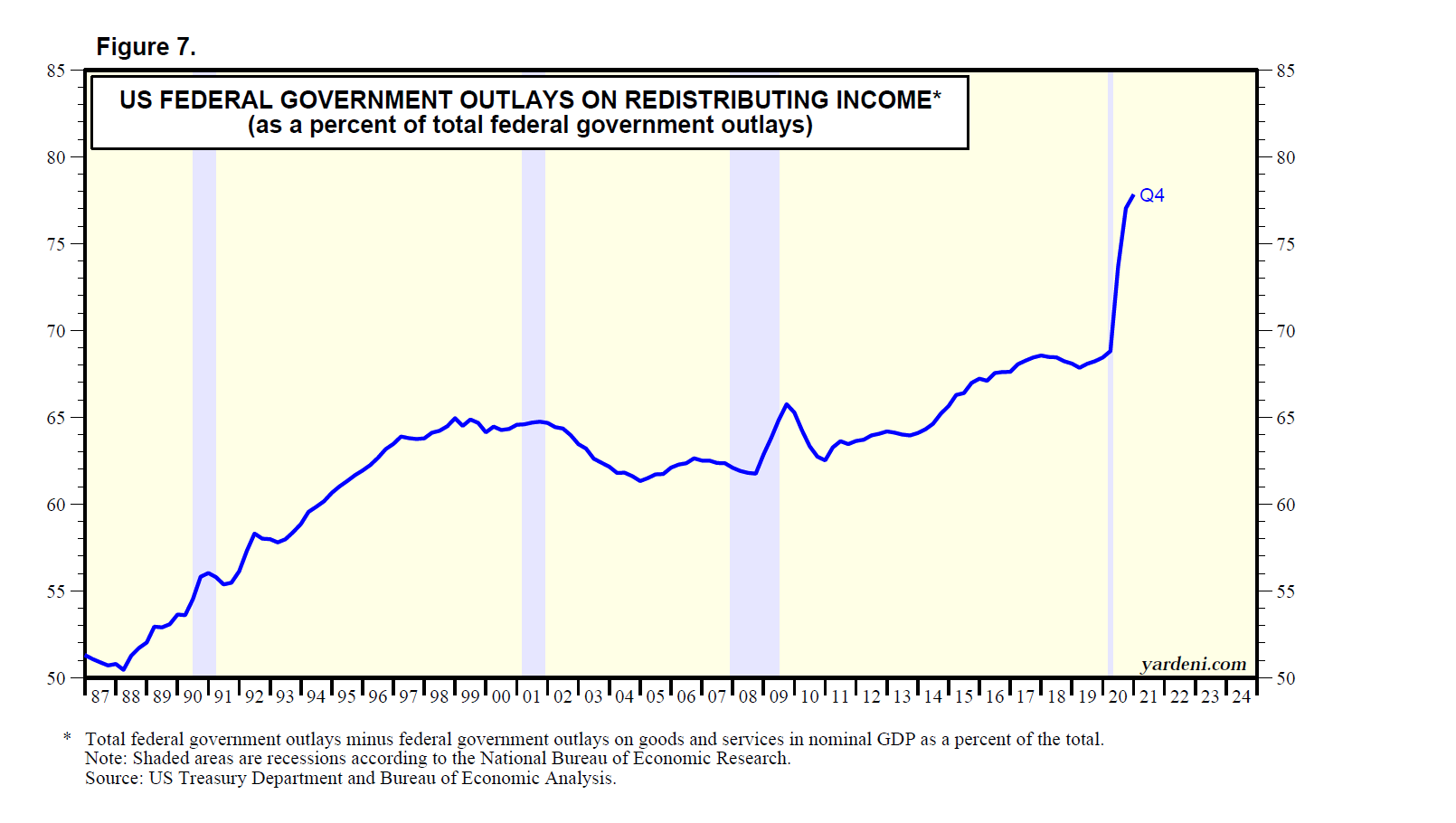

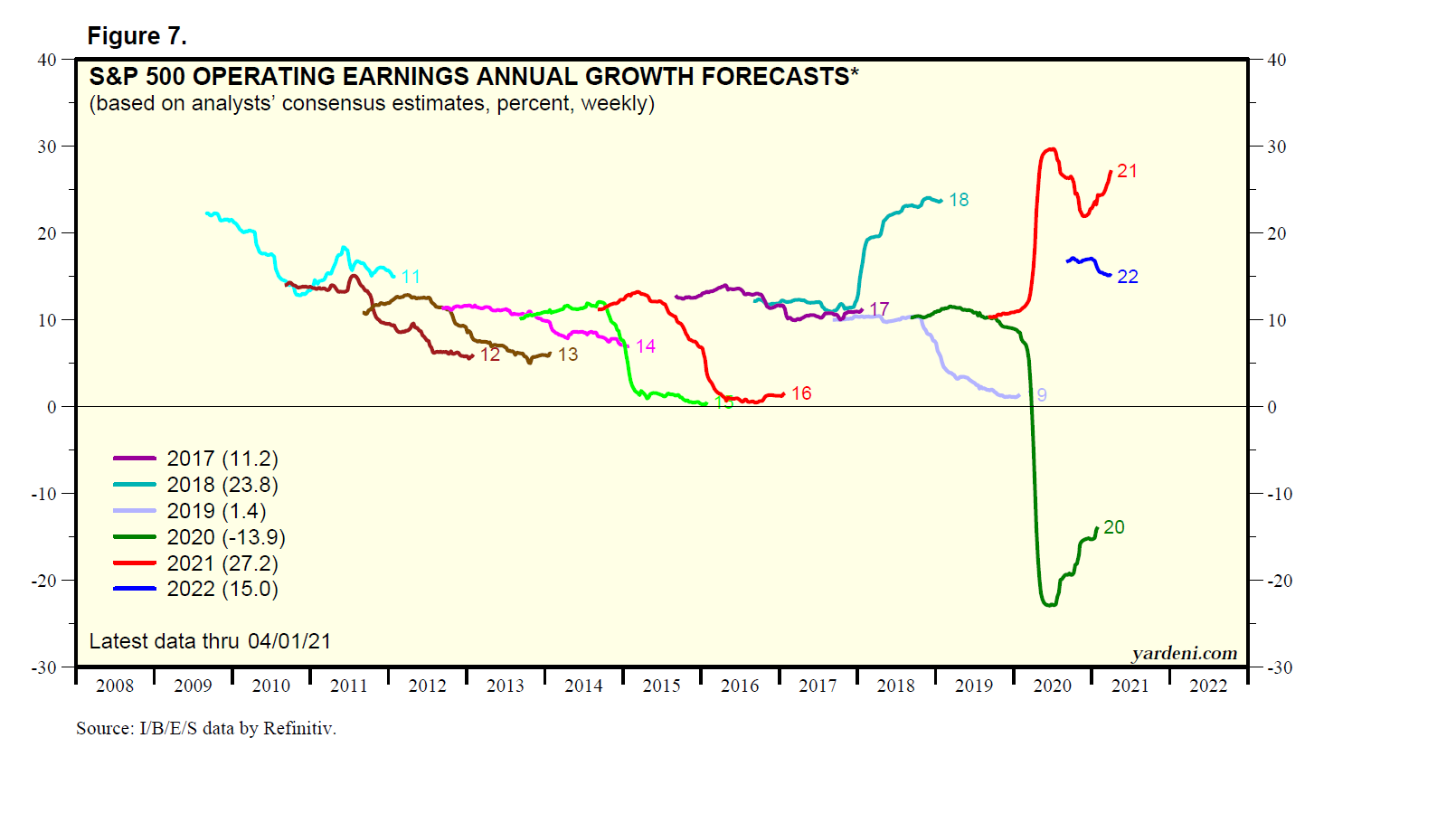

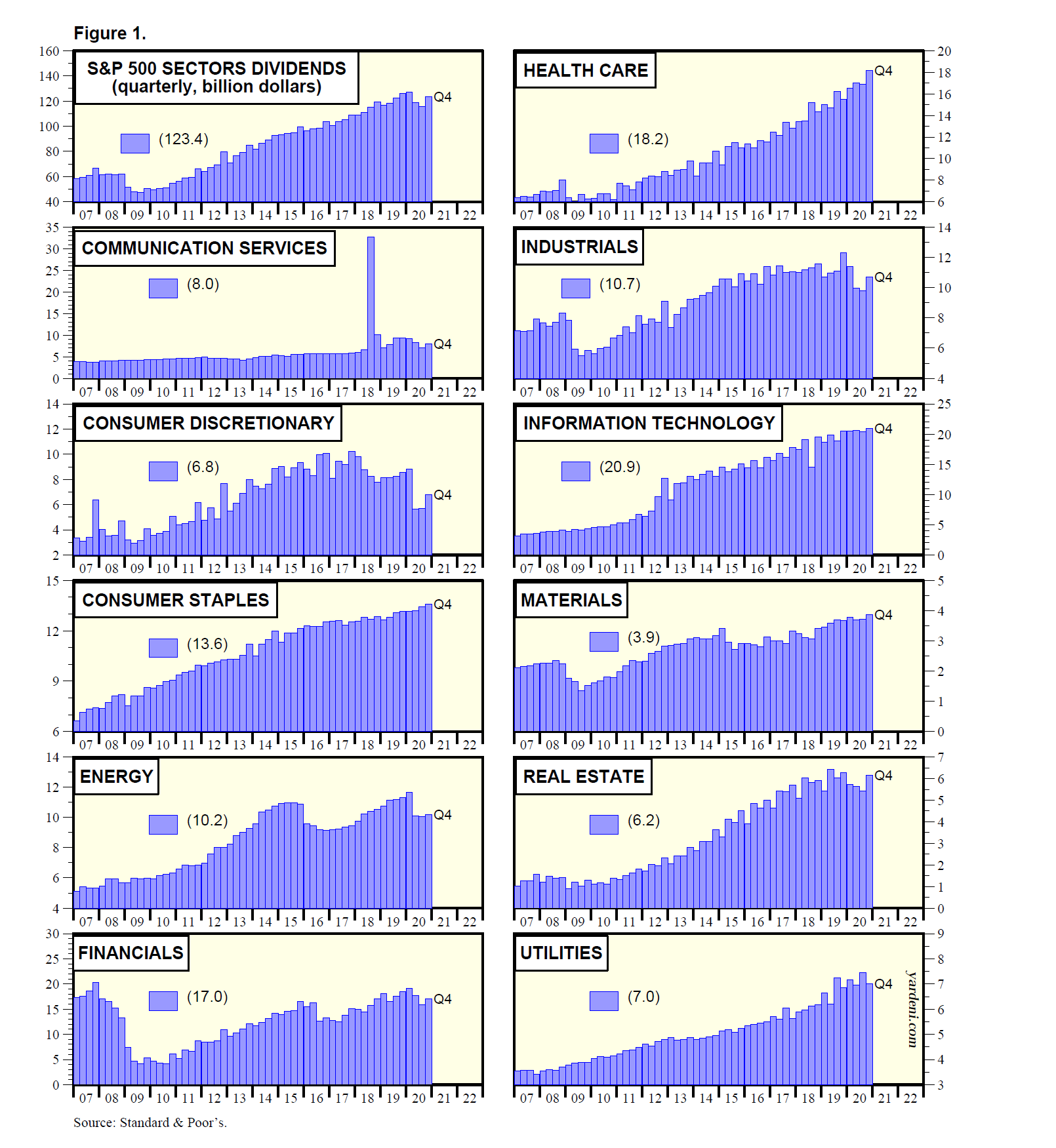

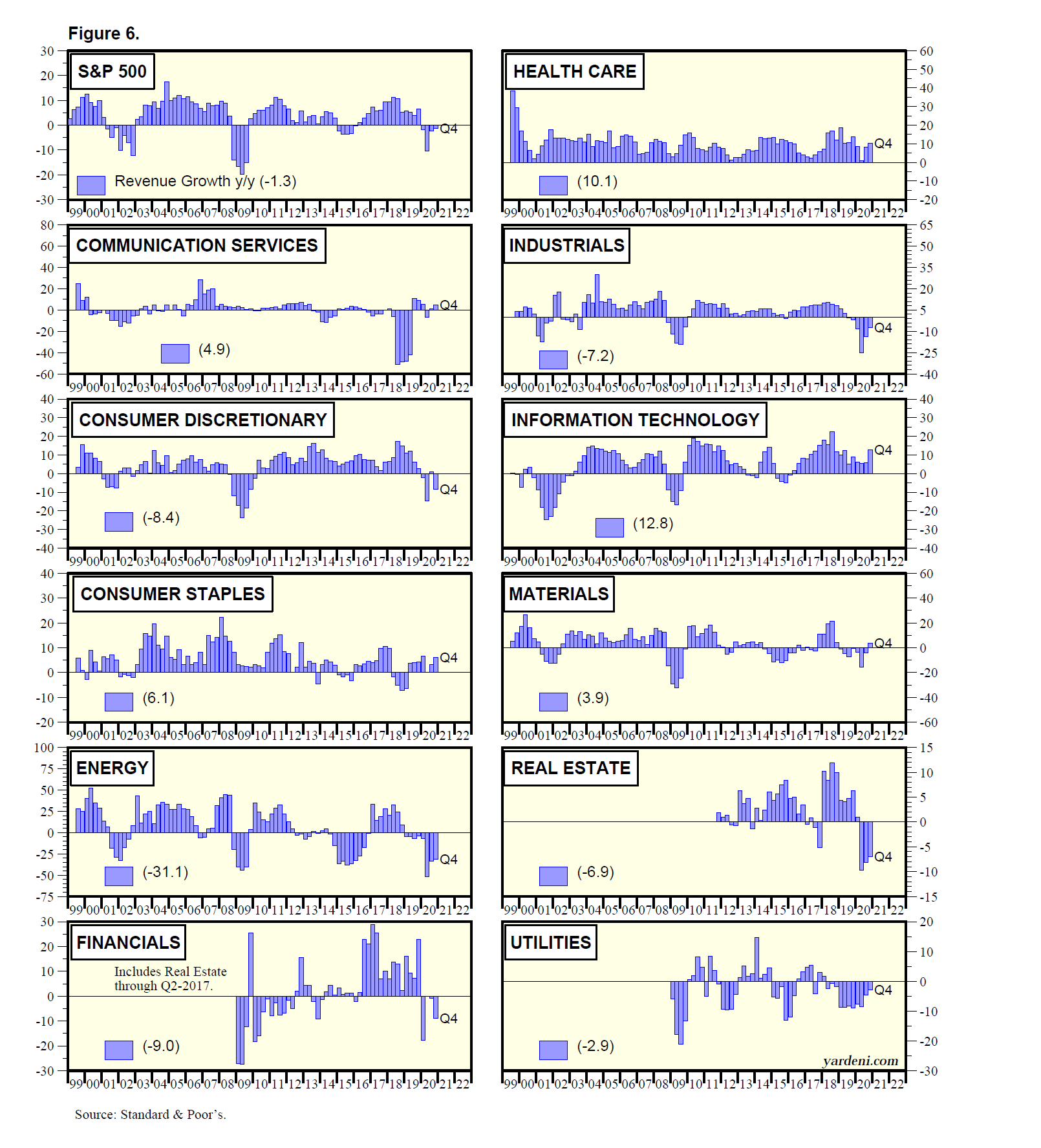

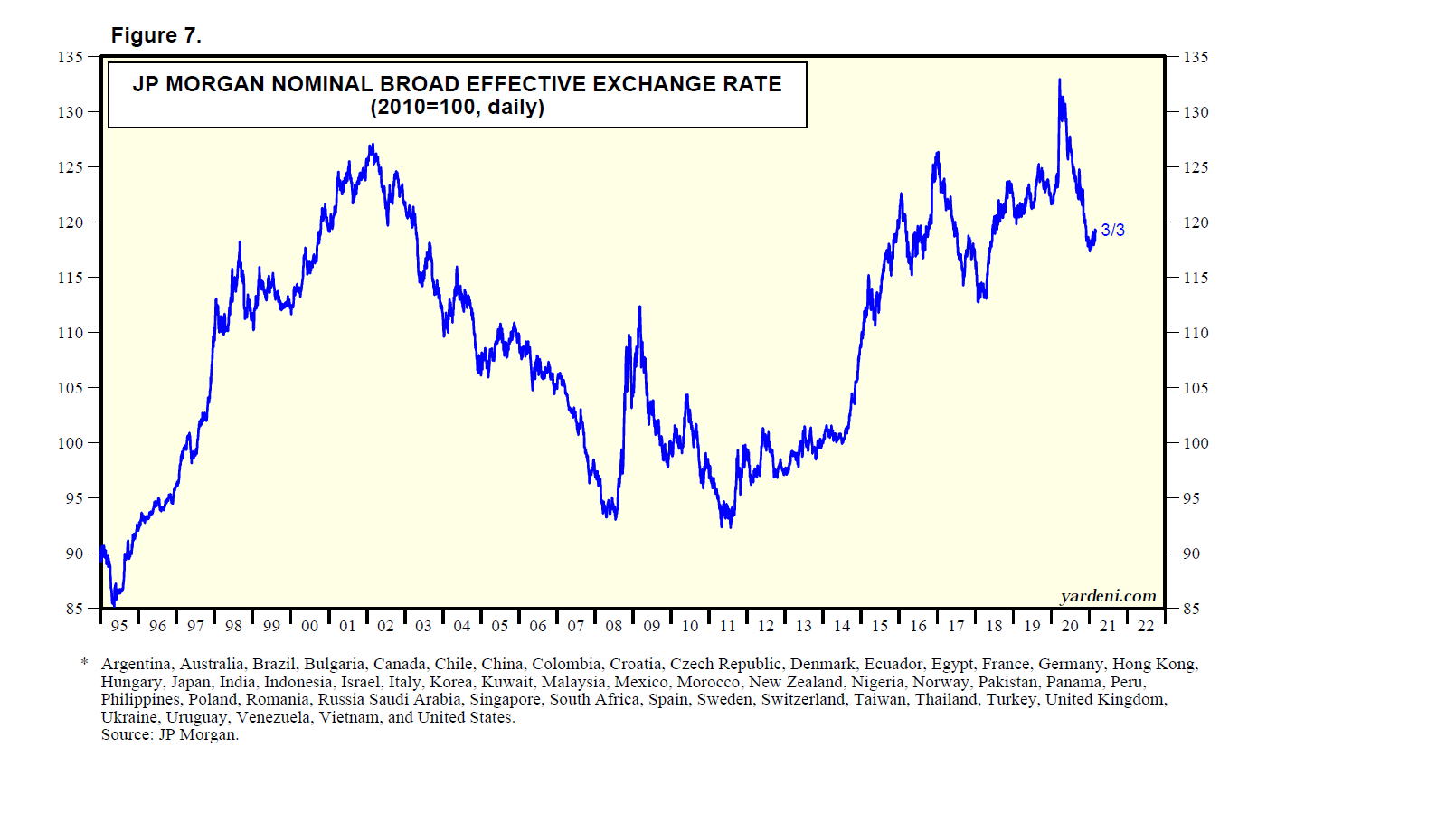

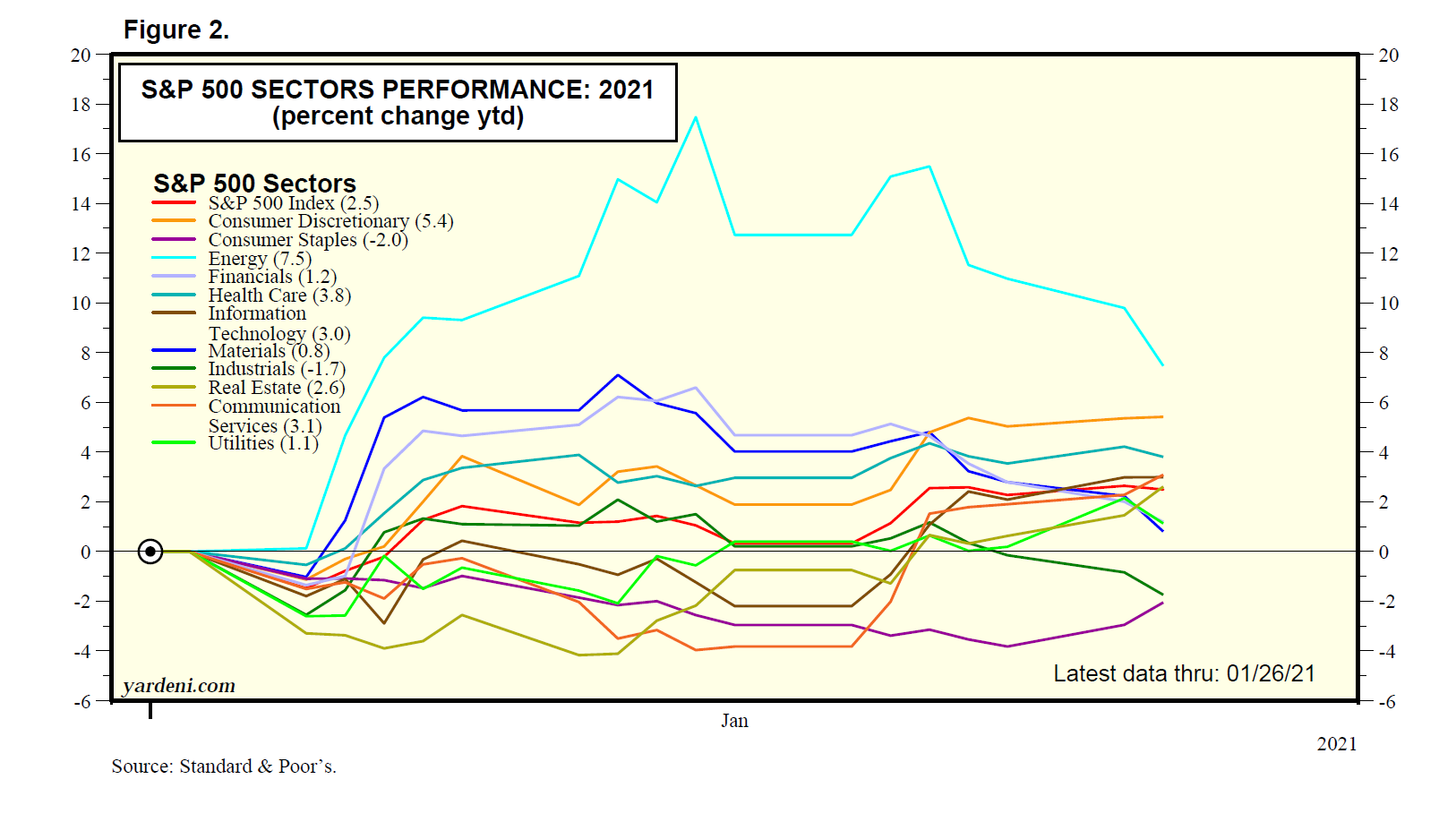

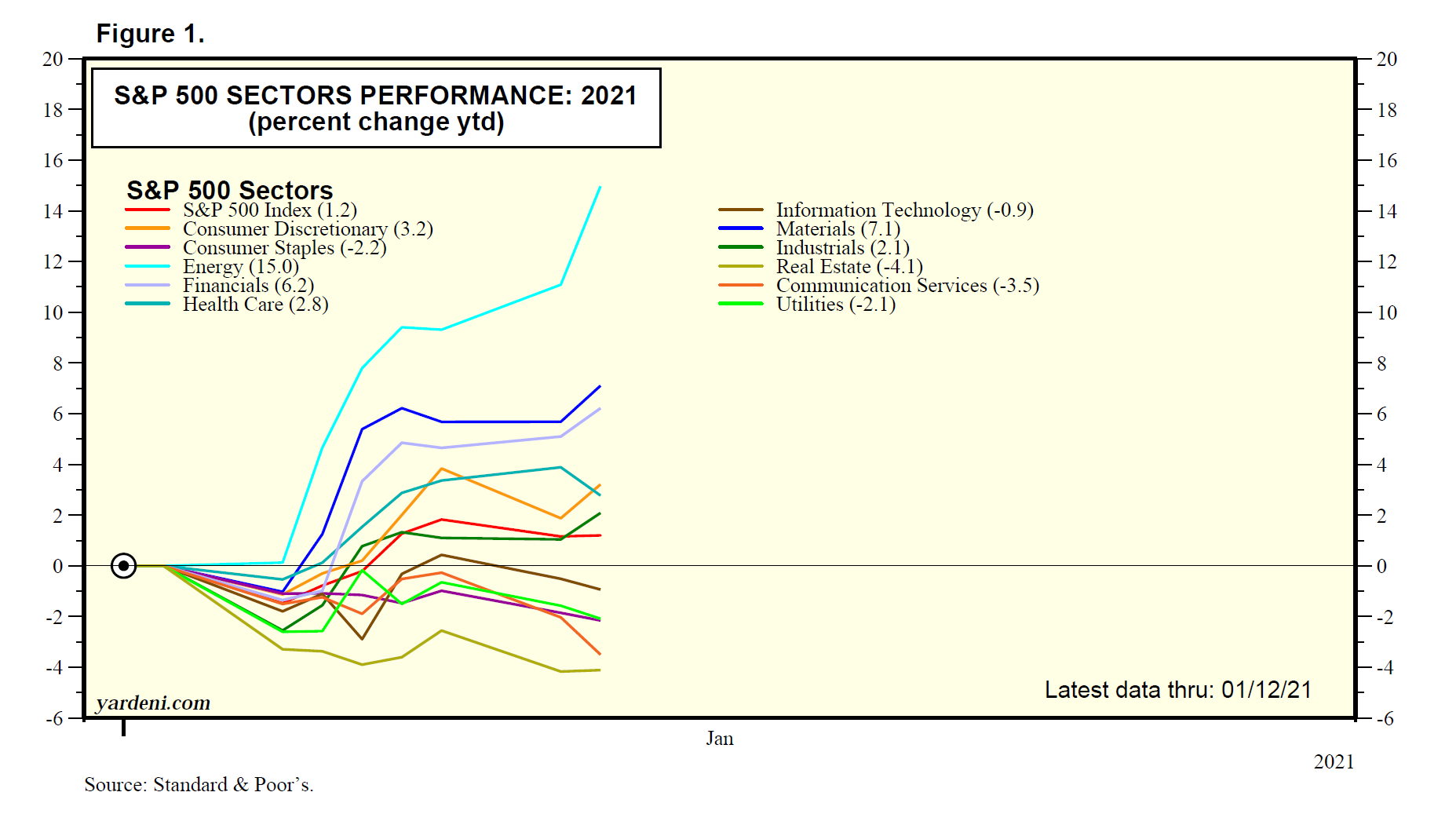

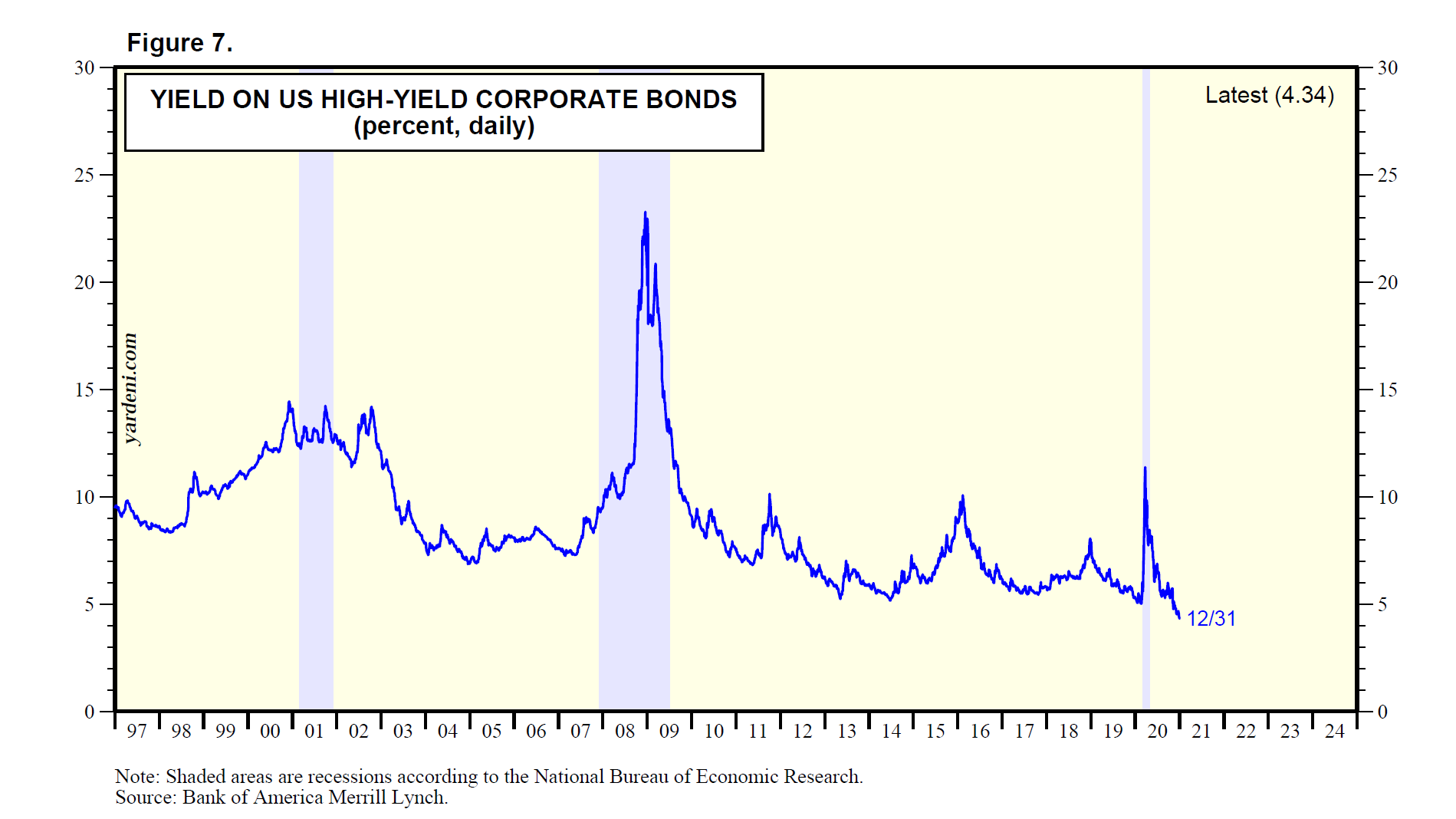

(1) Stock market rotating, again. You need a neck brace to trade the stock market these days. The S&P 500 was up 3.8% two weeks ago, led by a 6.0% increase in its Information Technology sector (Fig. 7). This past week, it was down 1.9%, led by the Energy (-5.1), Consumer Discretionary (-4.3), IT (-4.0), and Industrials (-2.8) sectors. Cyclicals got whacked by renewed fears of the rapidly spreading Omicron variant of Covid. Defensive sectors outperformed as follows: Health Care (2.5), Real Estate (1.6), Utilities (1.2), and Consumer Staples (1.2). (See our Performance Derby tables for the S&P 500 sectors and industries over the past week.)

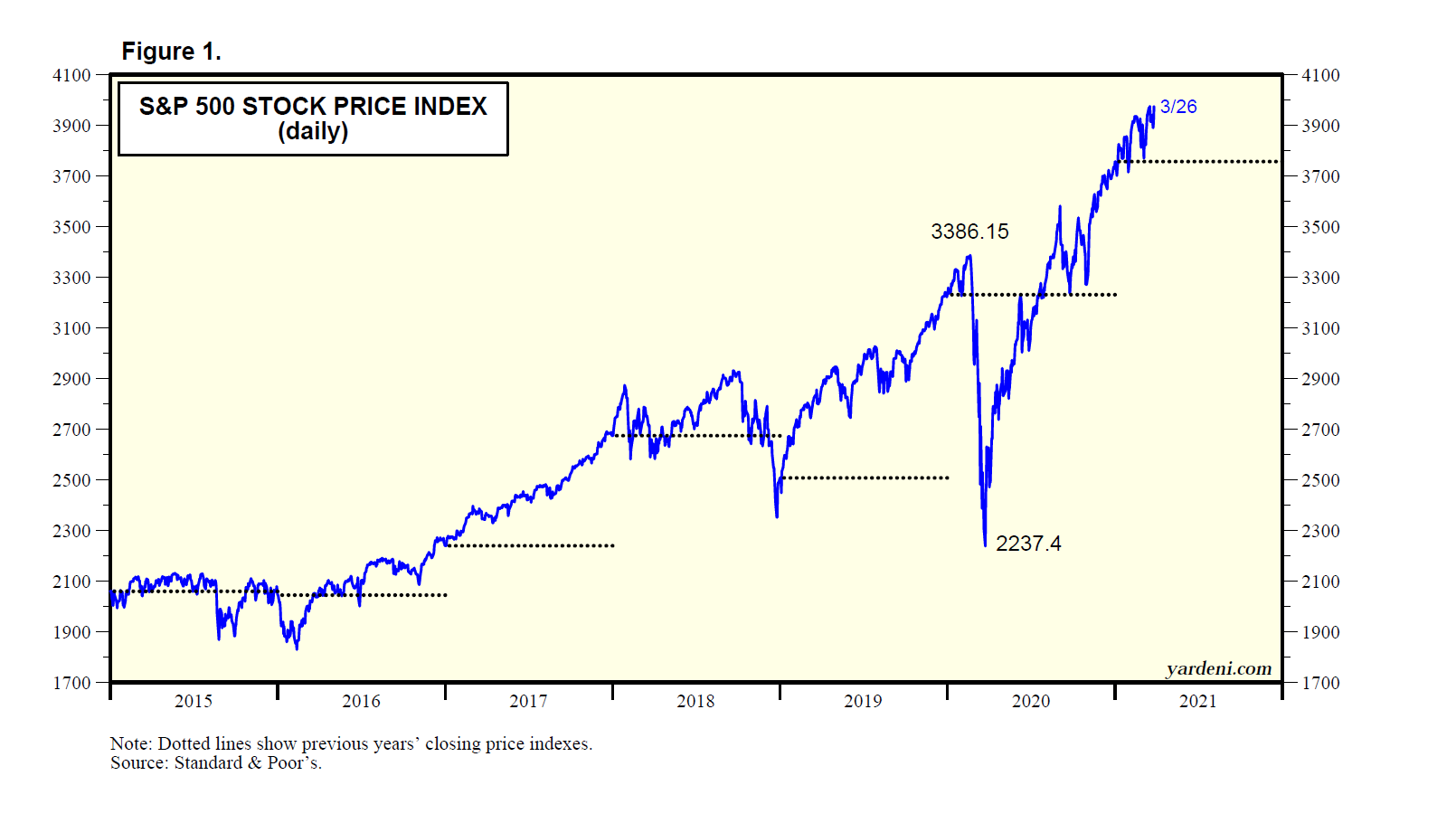

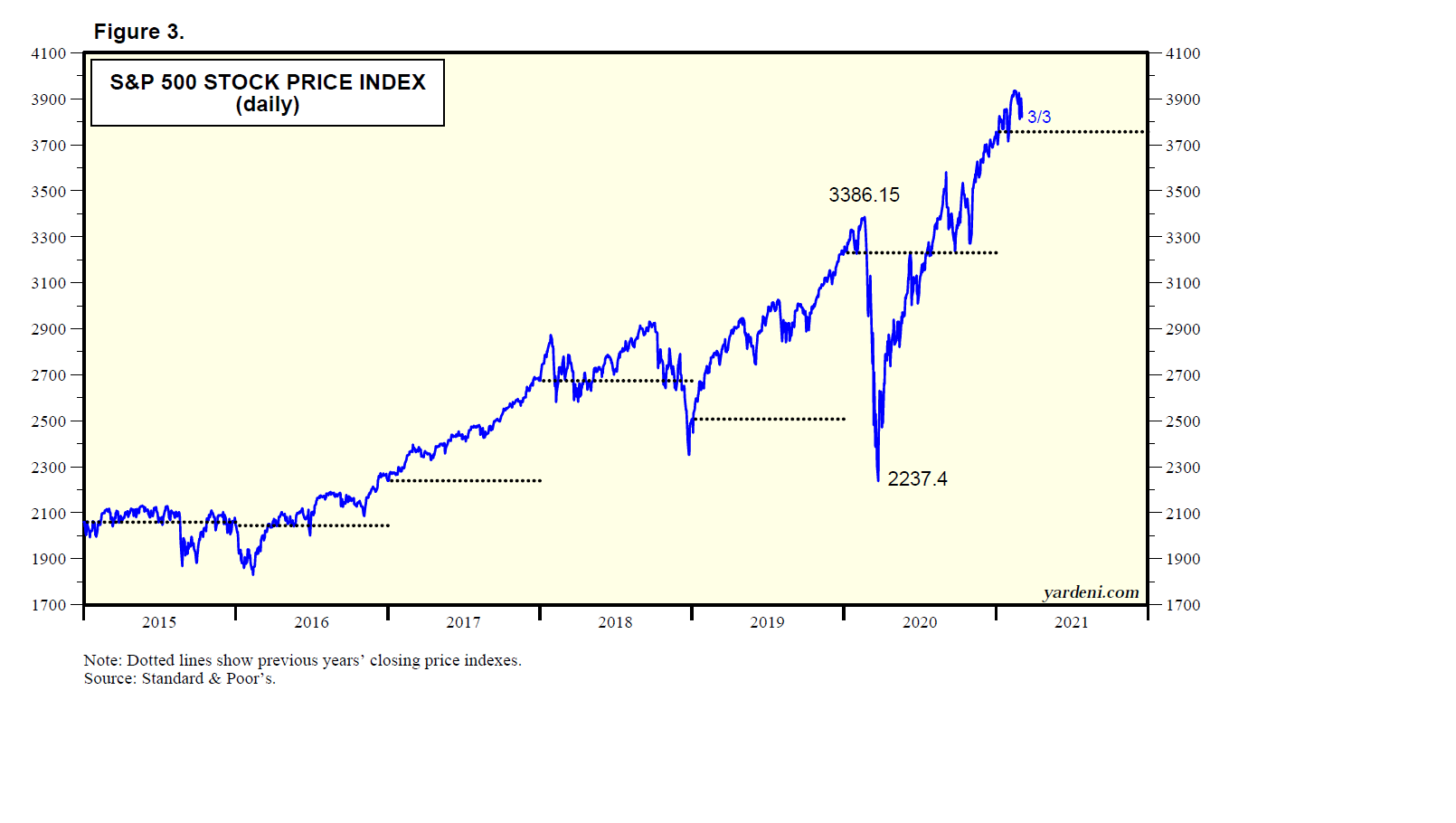

The S&P 500 peaked at a record high of 4712.02 a week ago Friday. It was down every day this past week except for Wednesday, when a big jump took it almost back to Friday’s high. That was surprising since the FOMC announced on Wednesday a faster pace of tapering and signaled three rate hikes in 2022. Coincidently, there was also news suggesting diminishing odds of Congress’ passing Biden’s Build Back Better (BBB) bill. That might be viewed as bullish for stocks to the extent that more fiscal stimulus would push inflation even higher.

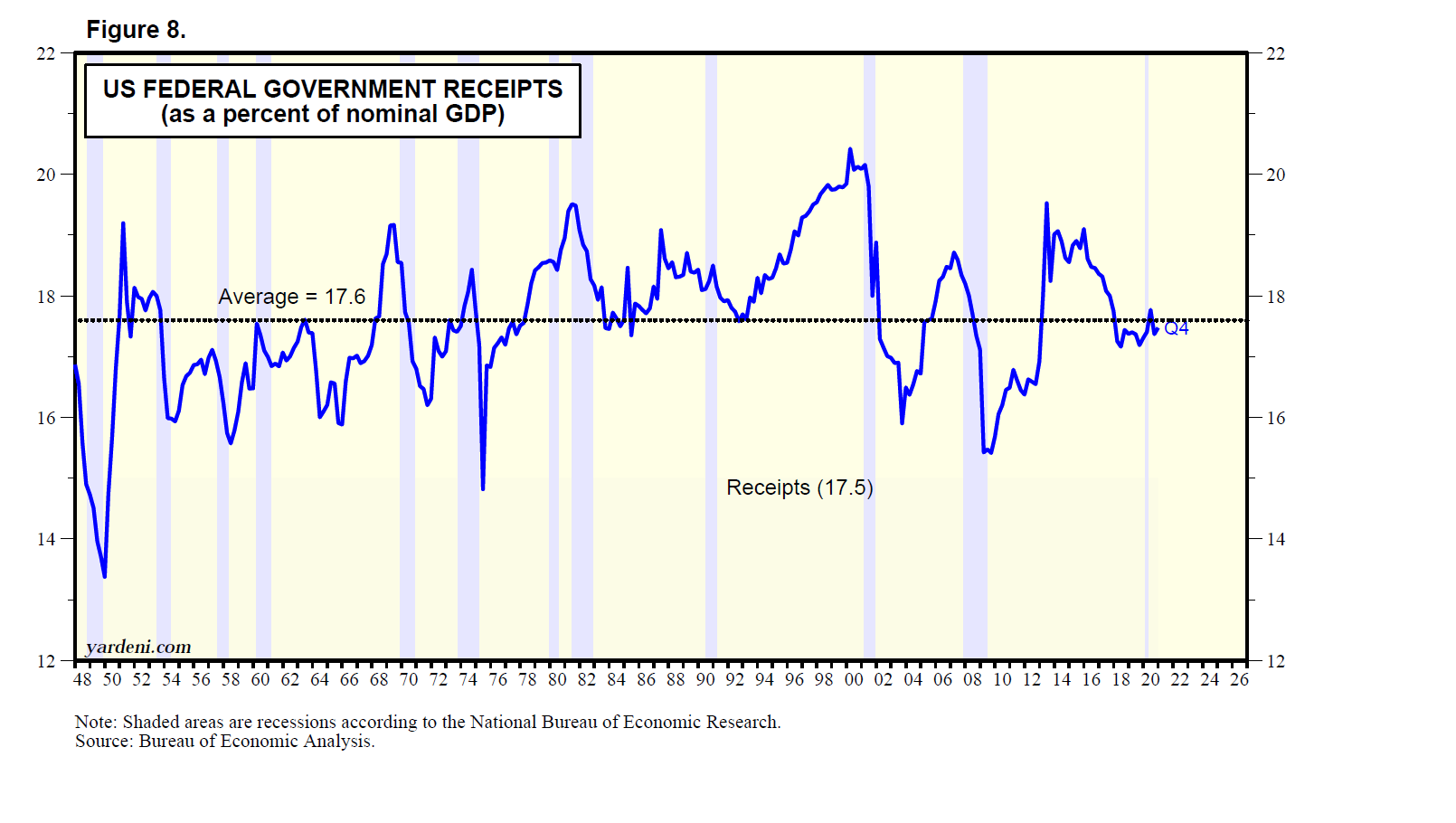

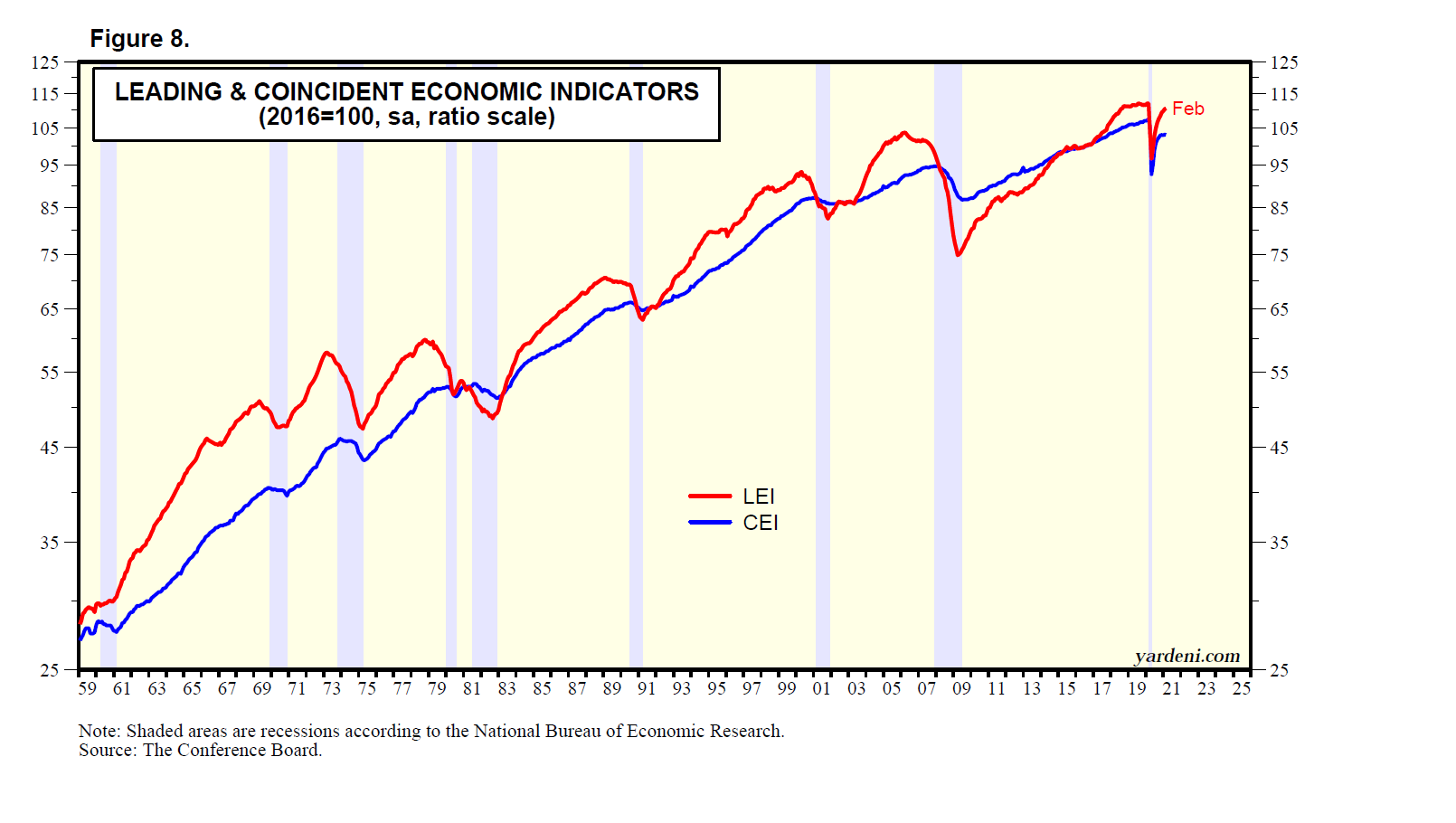

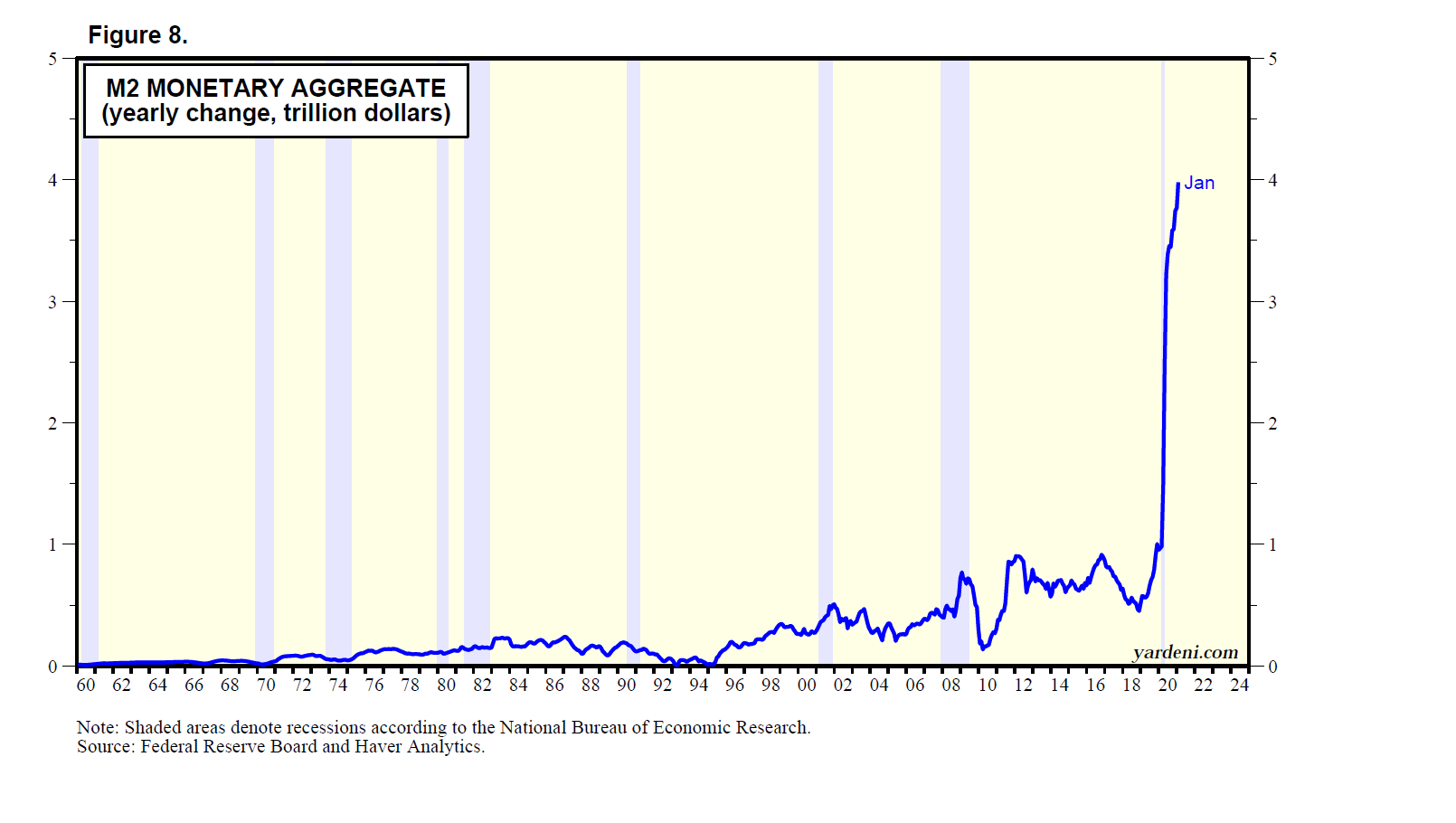

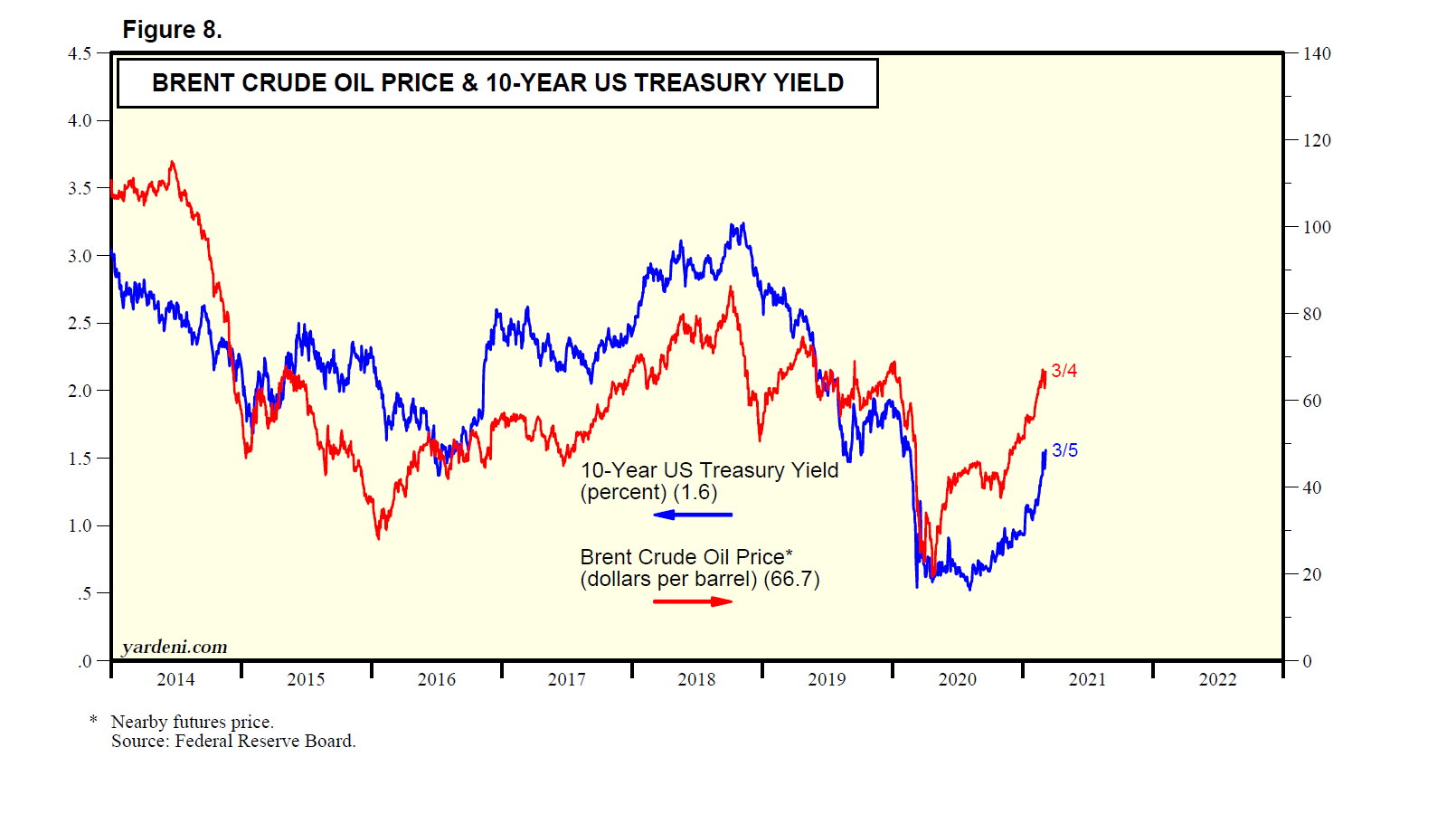

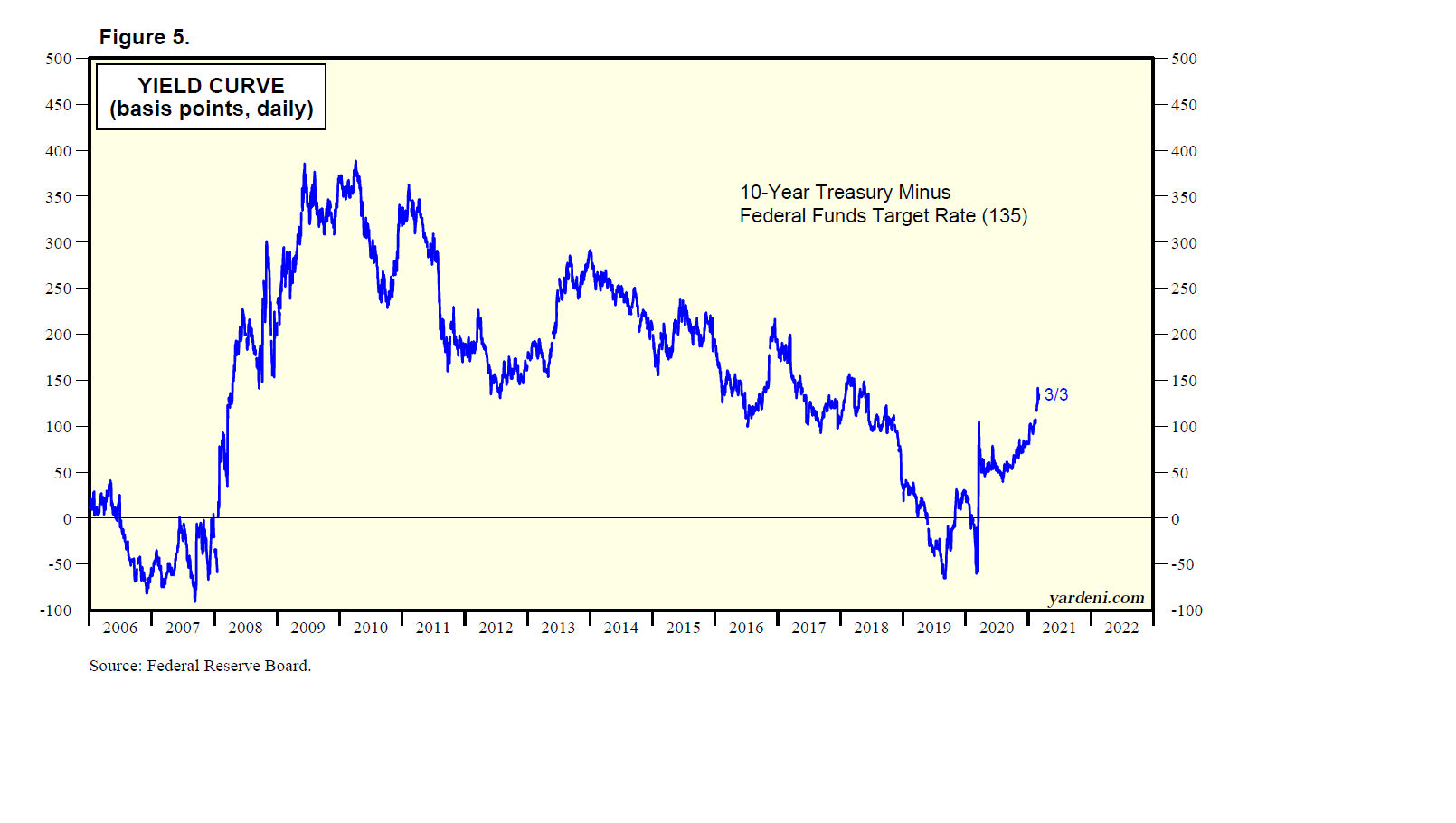

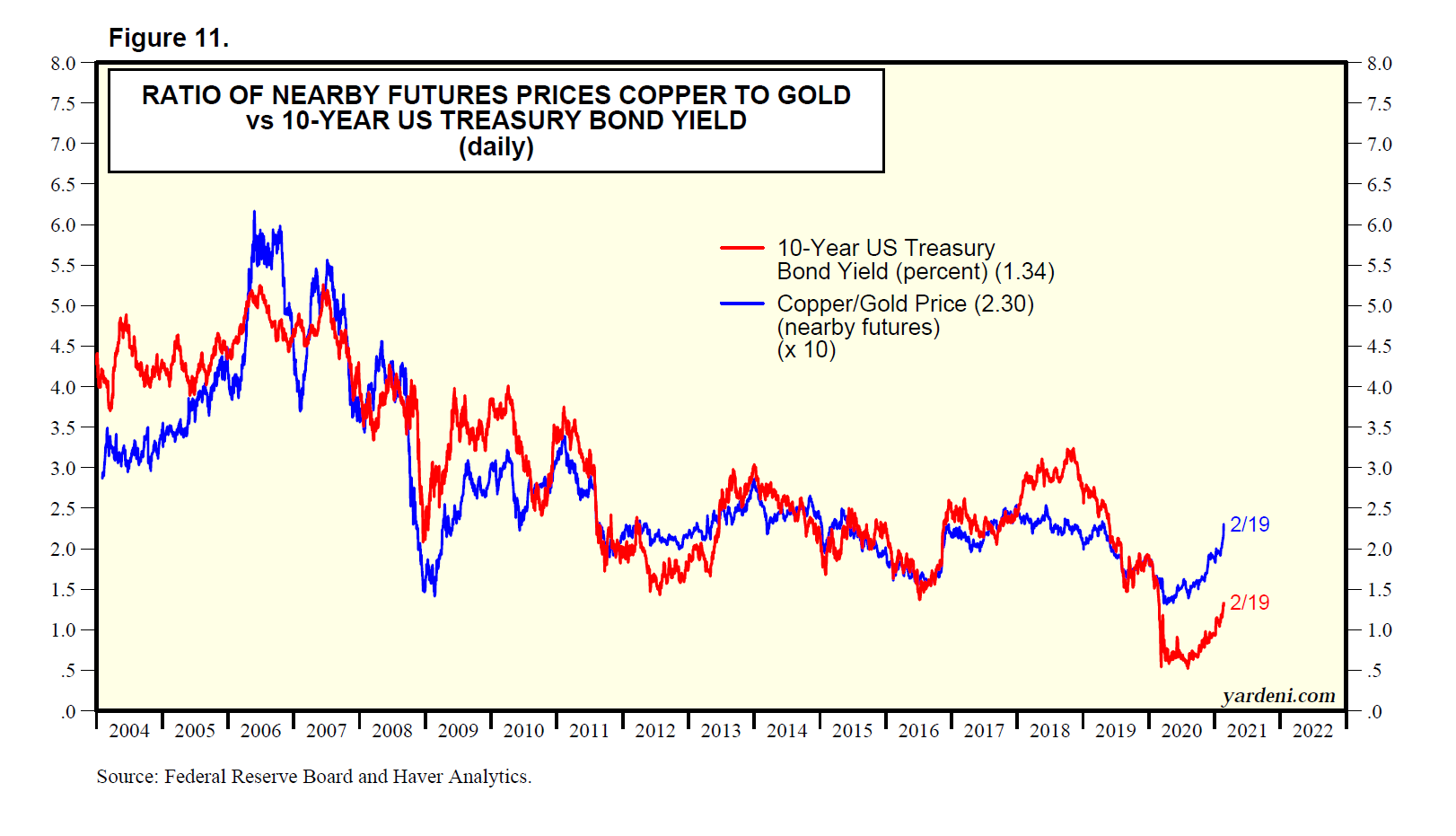

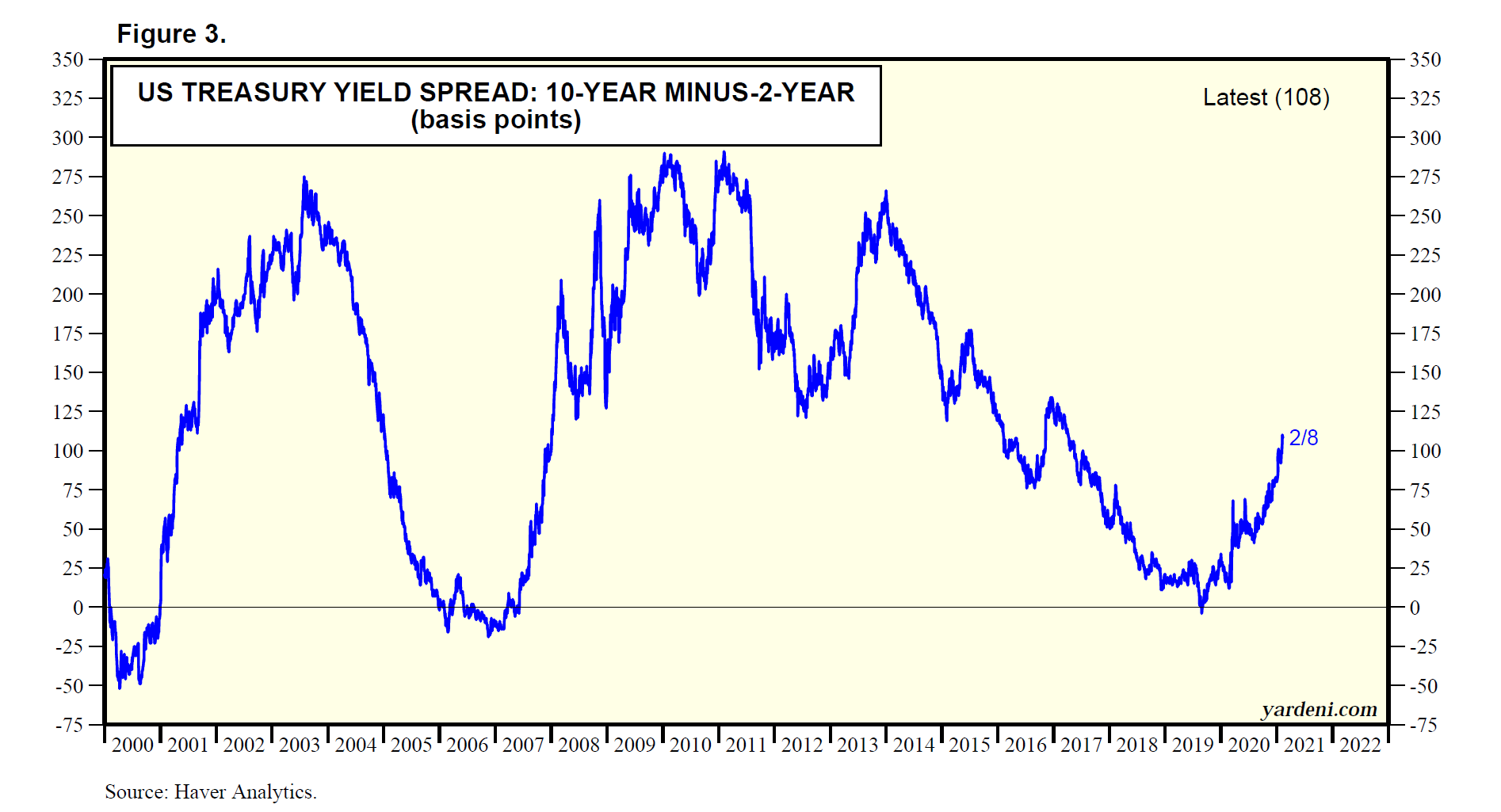

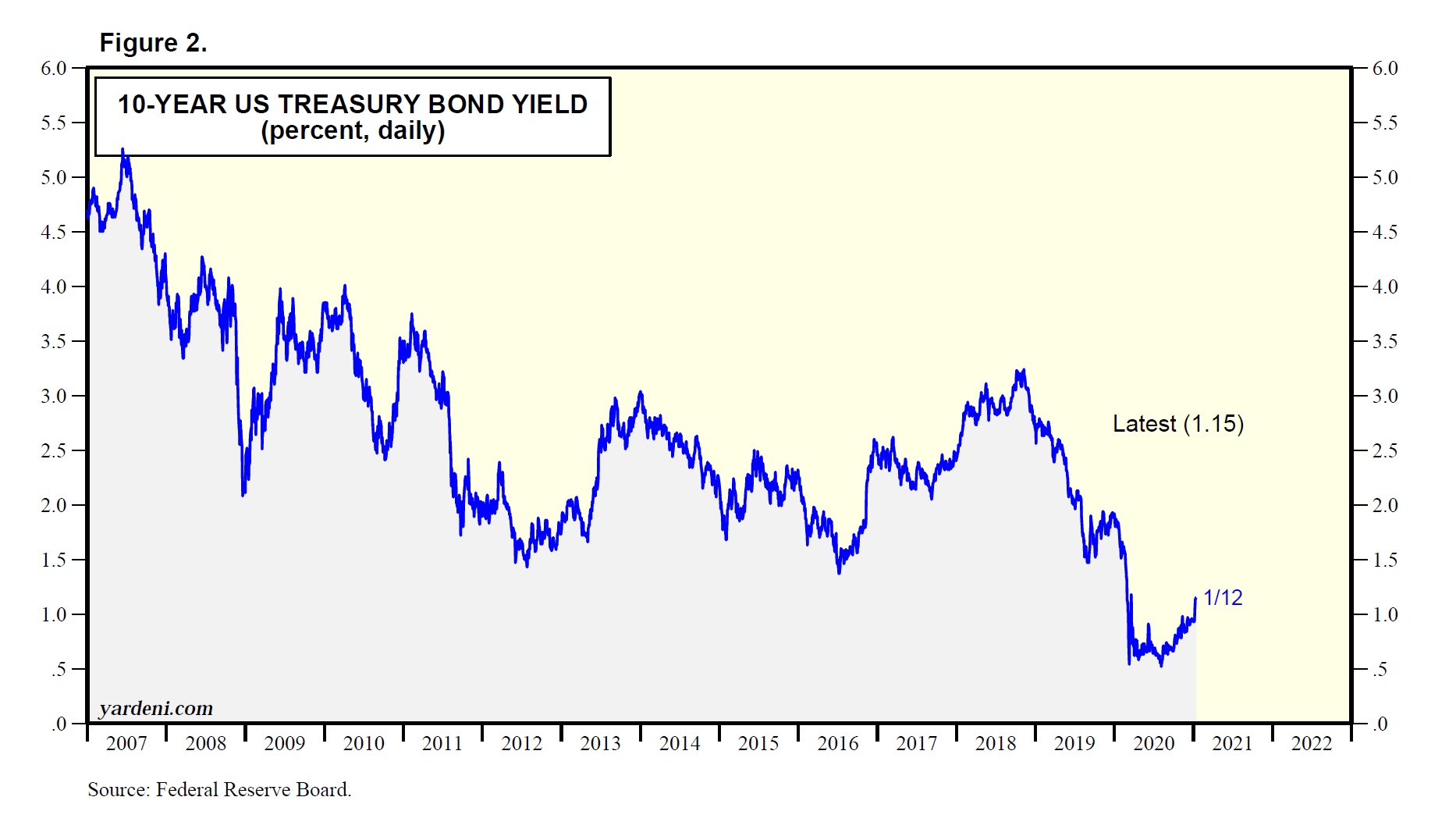

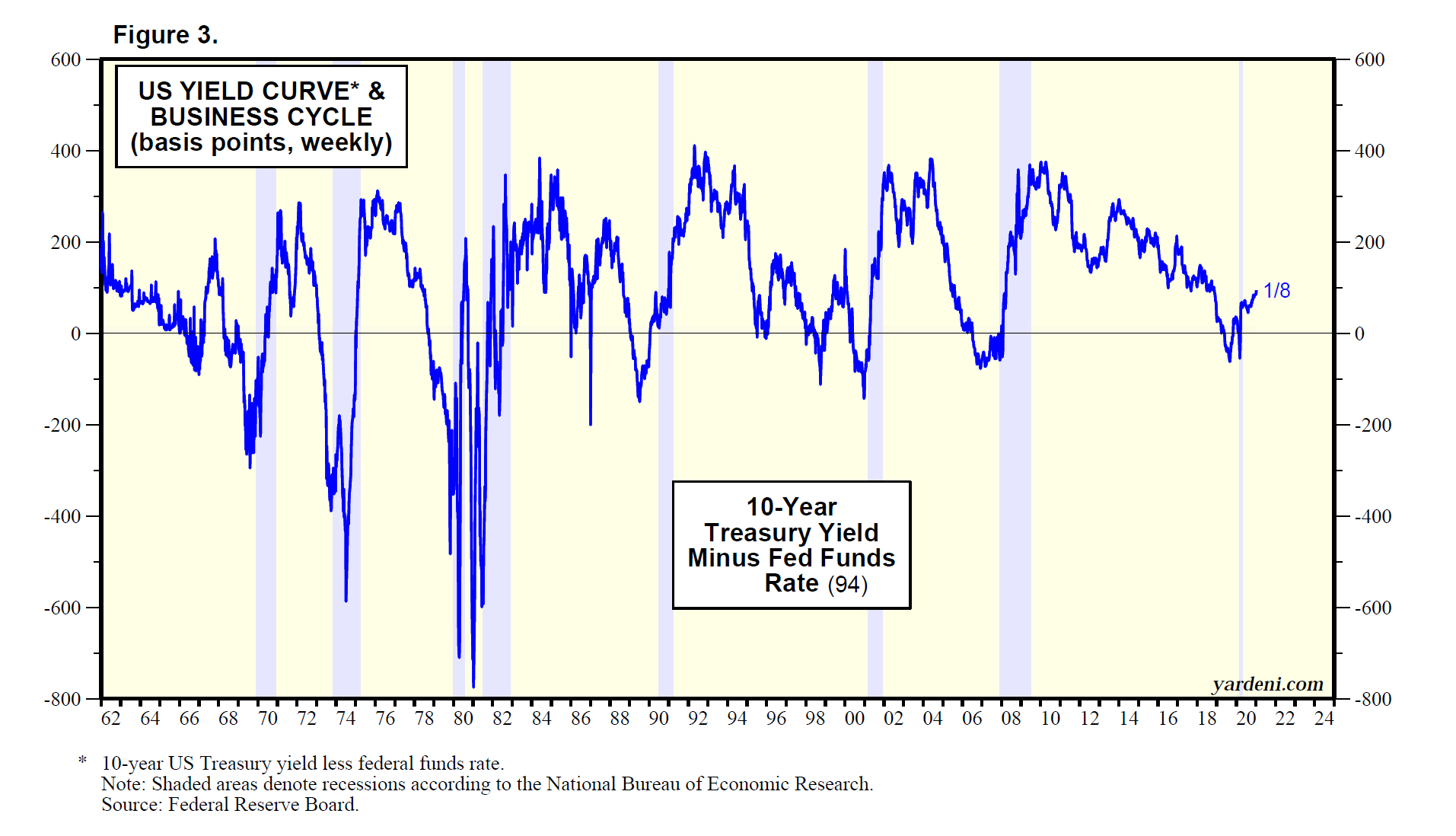

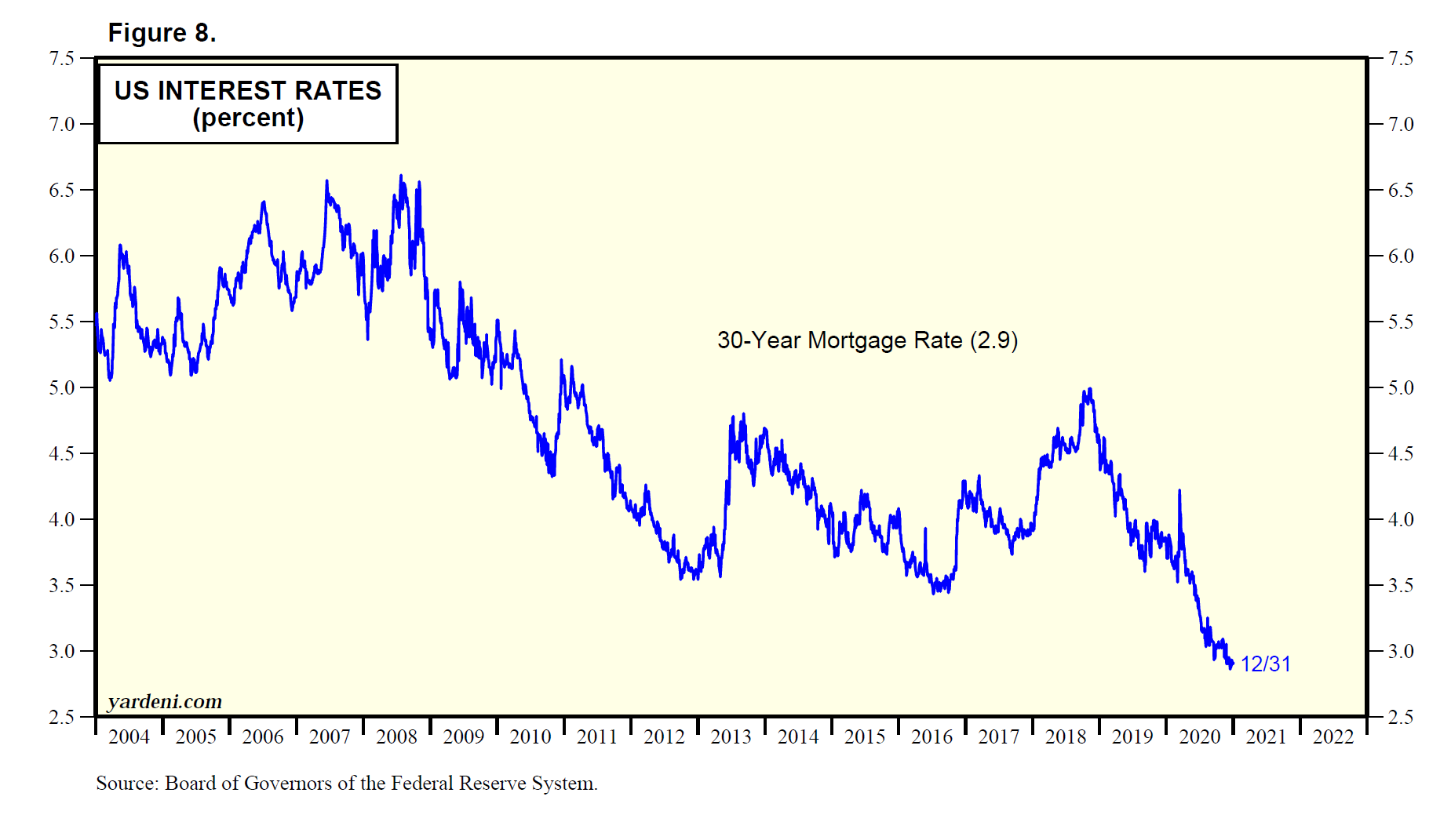

(2) Yield curve flattening, again. The flattening yield-curve spread between 10-year and 2-year Treasury notes suggests that three rate hikes next year might be enough to lower inflation, especially if Congress can’t get enough votes for yet another round of fiscal stimulus (Fig. 8).

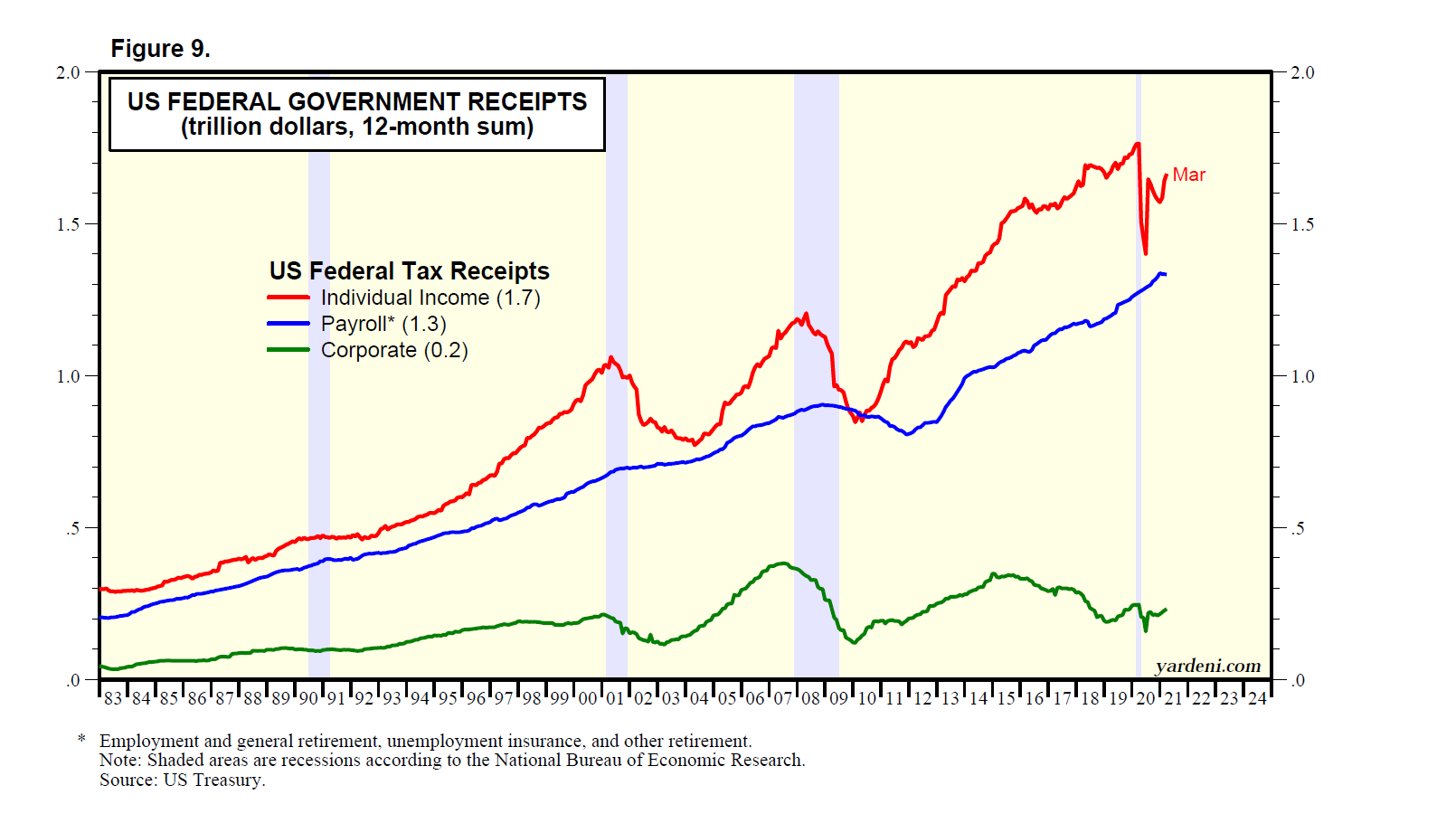

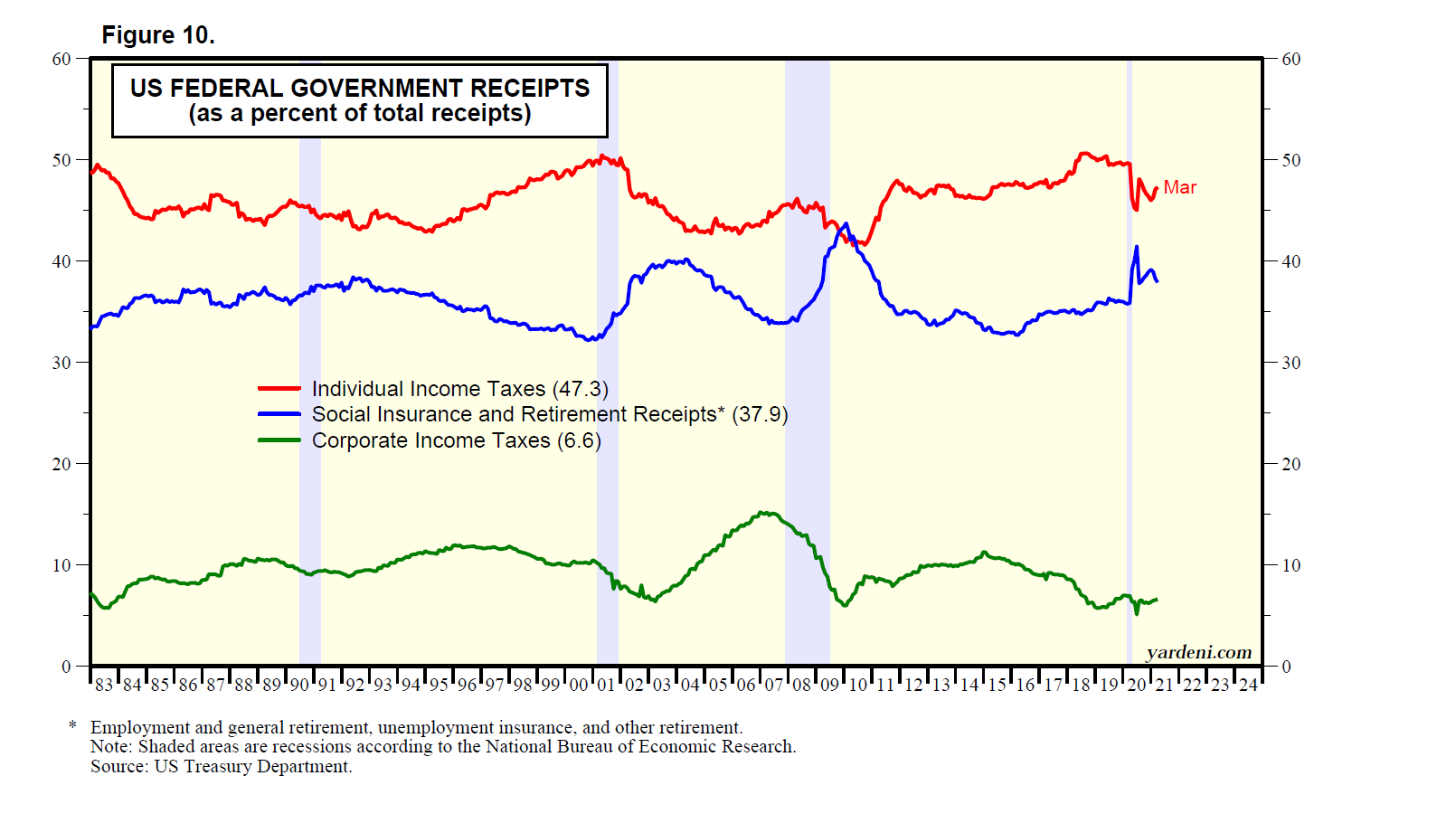

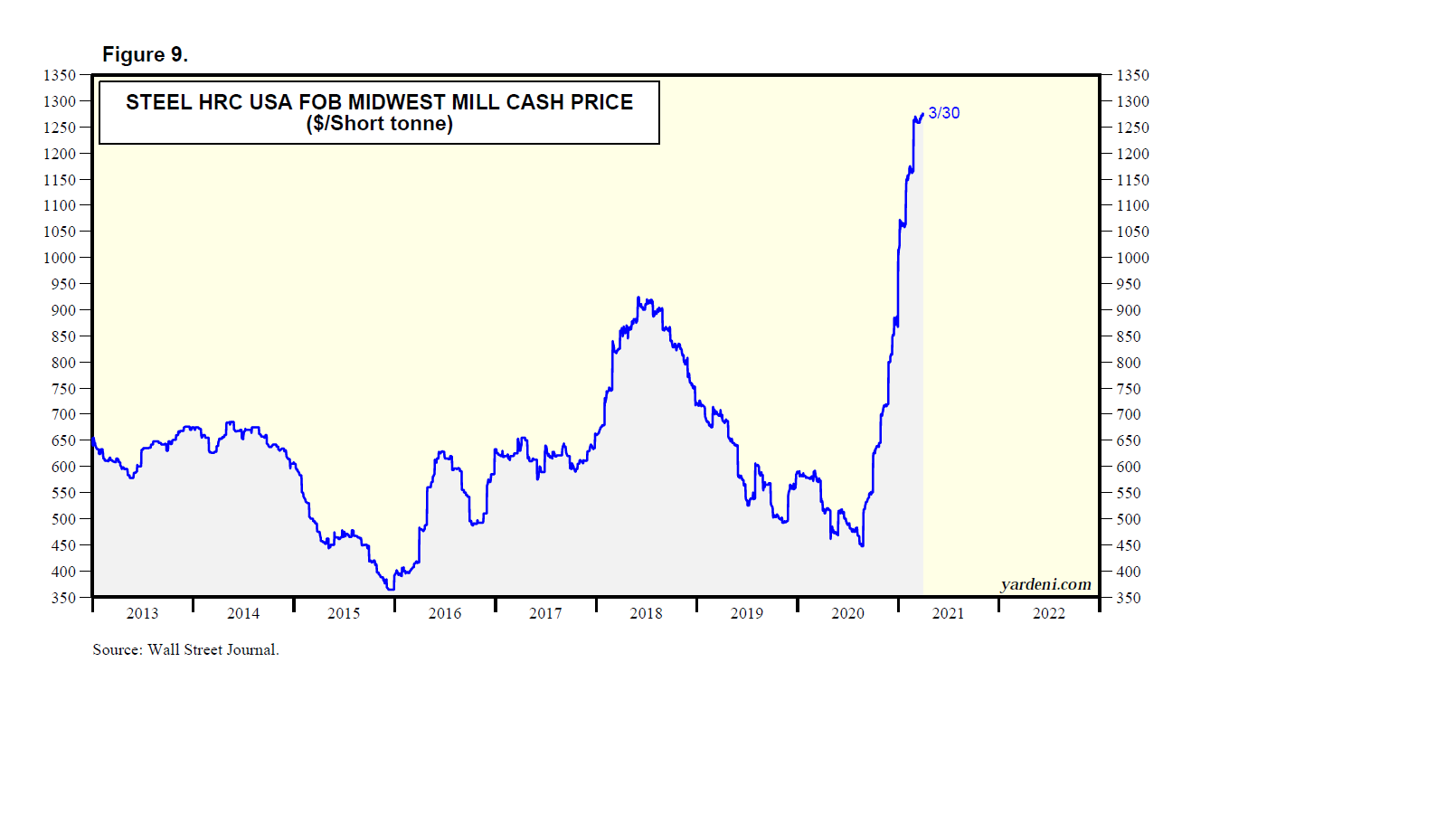

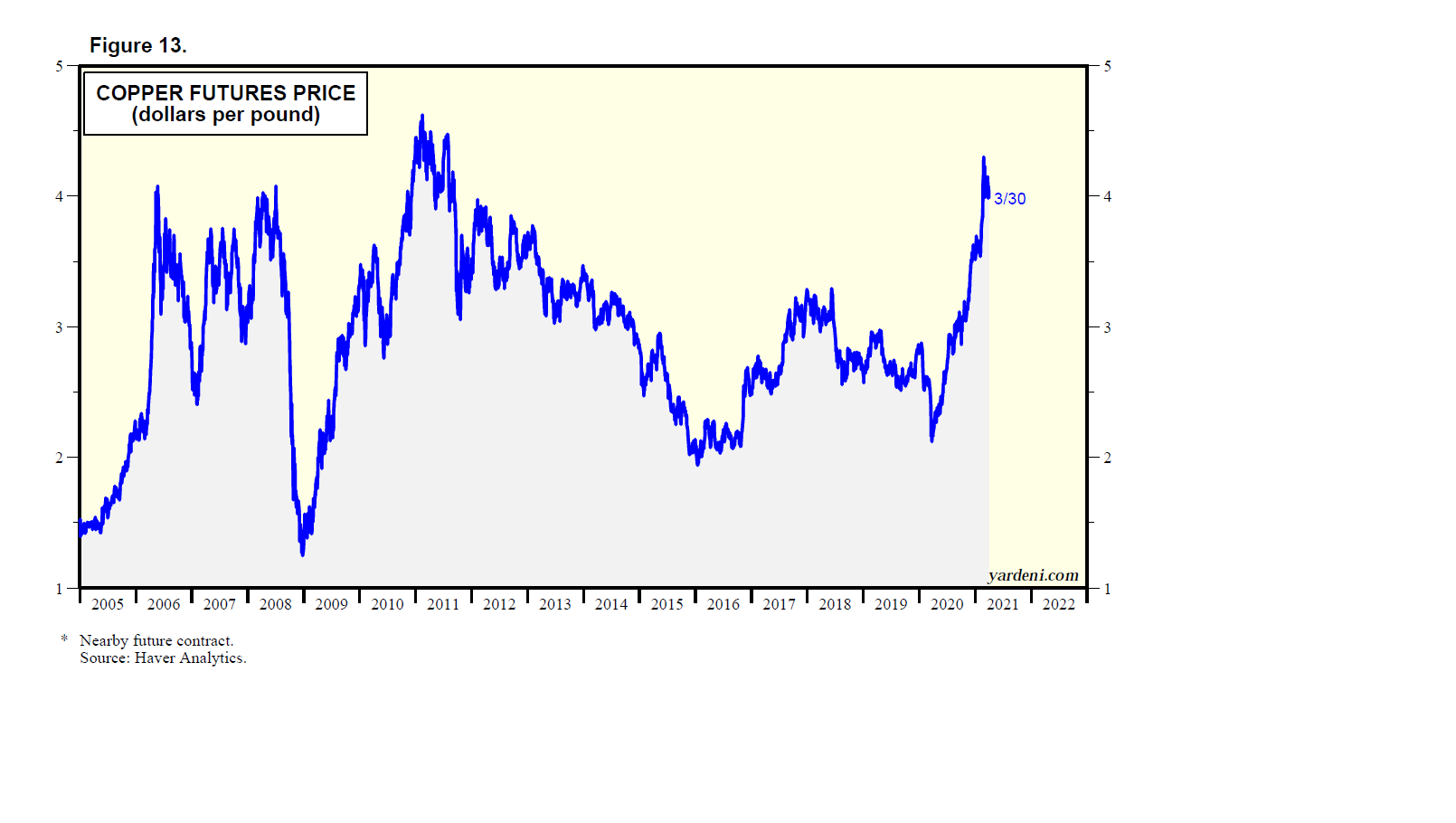

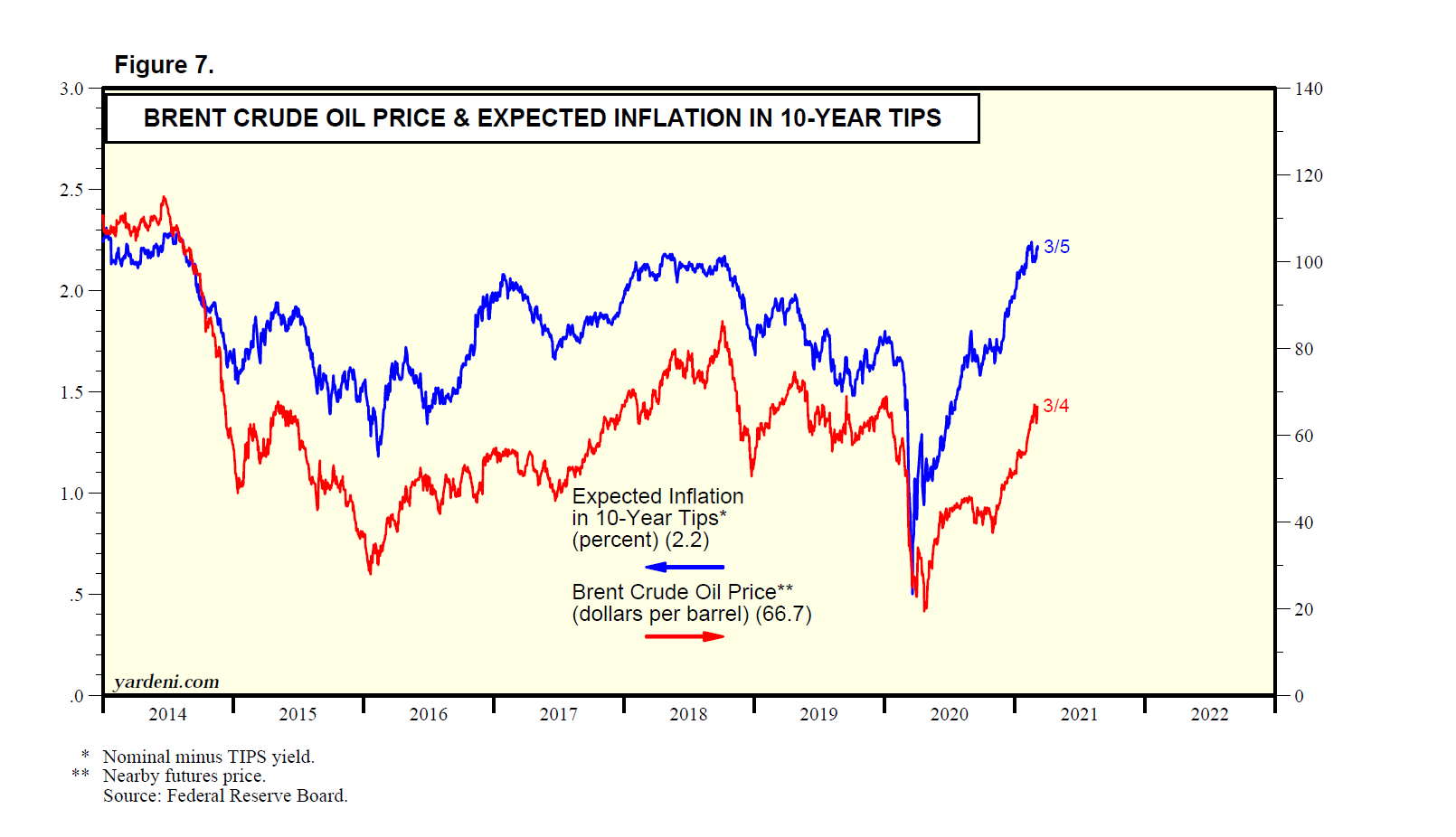

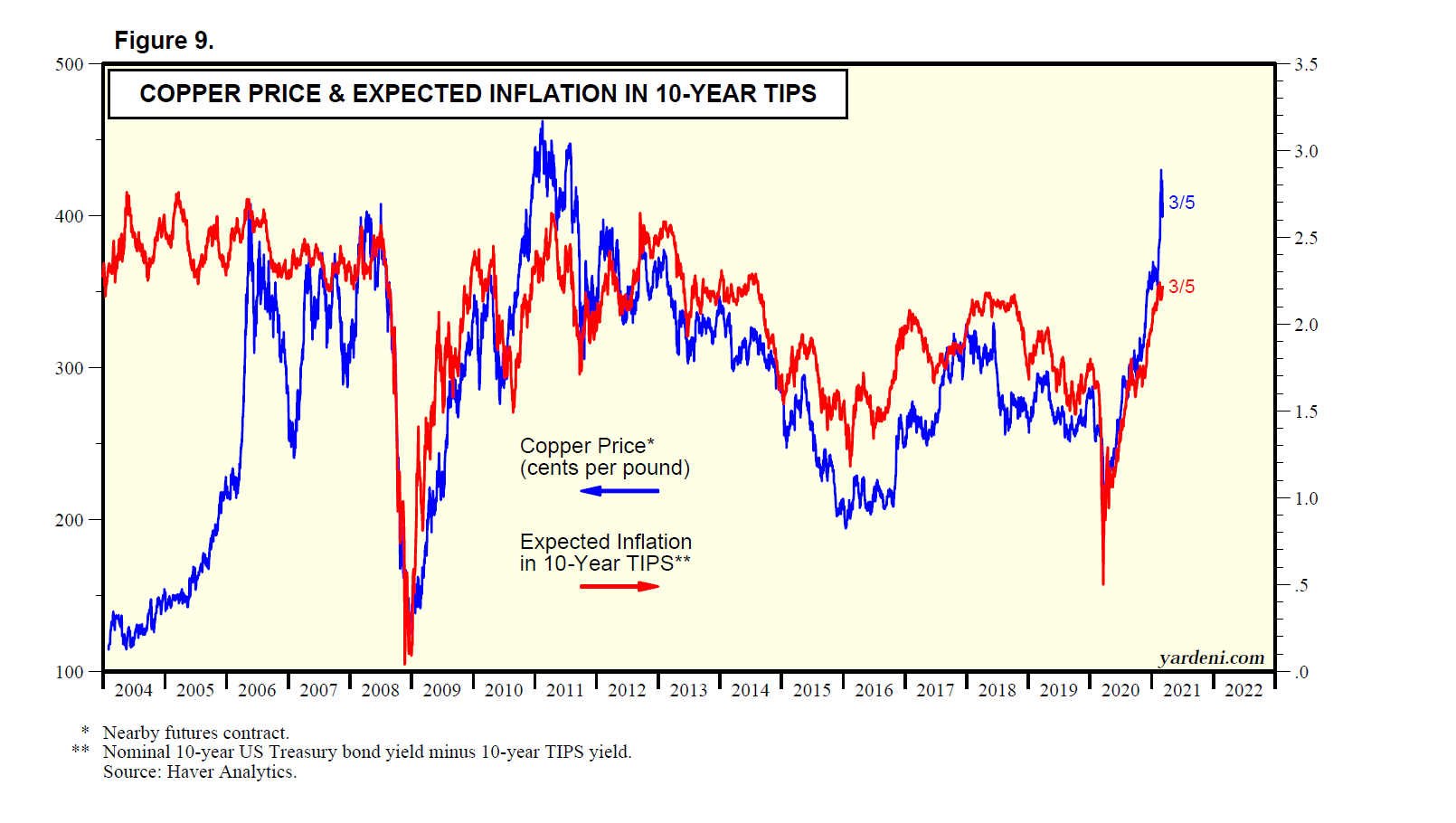

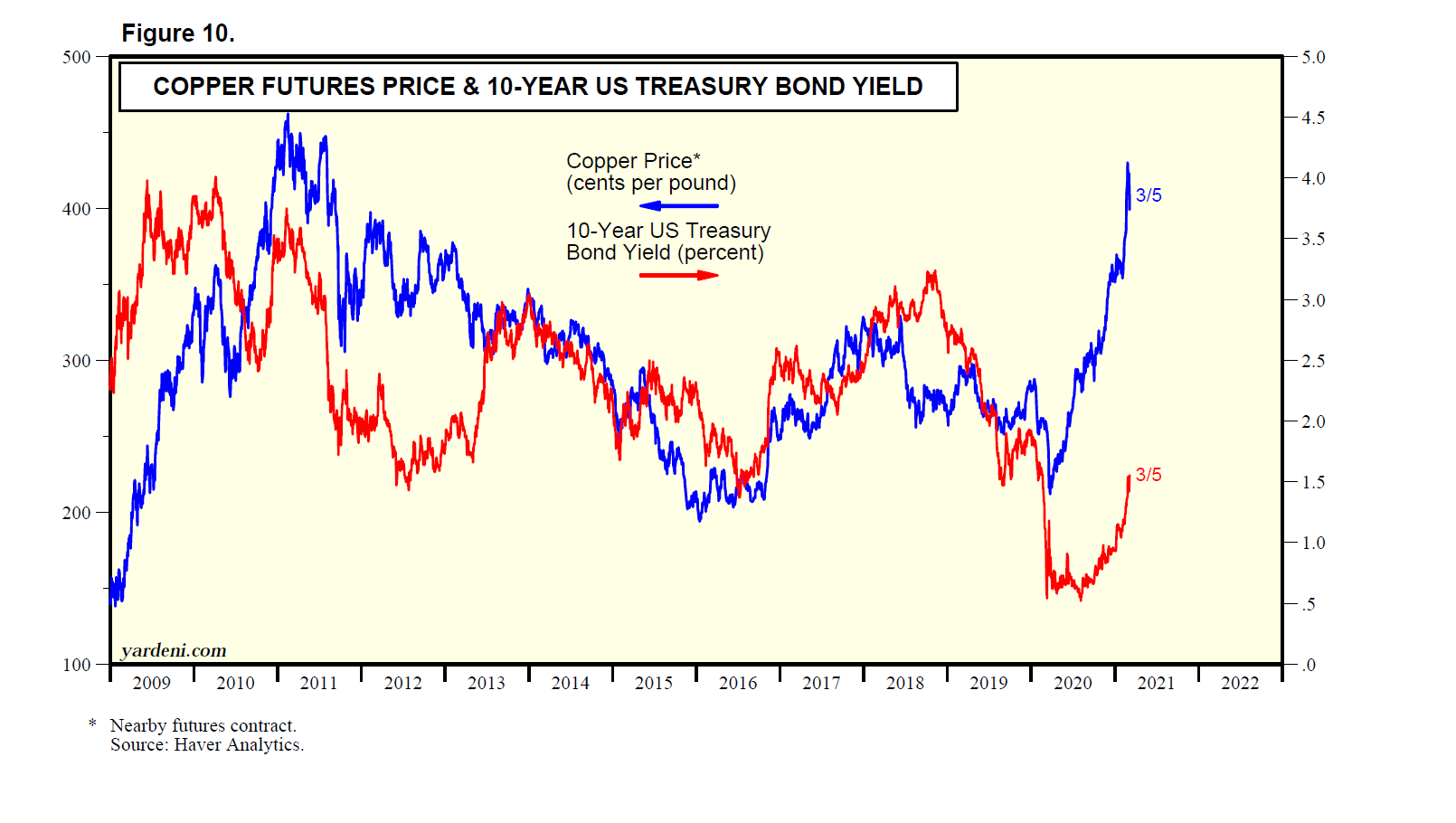

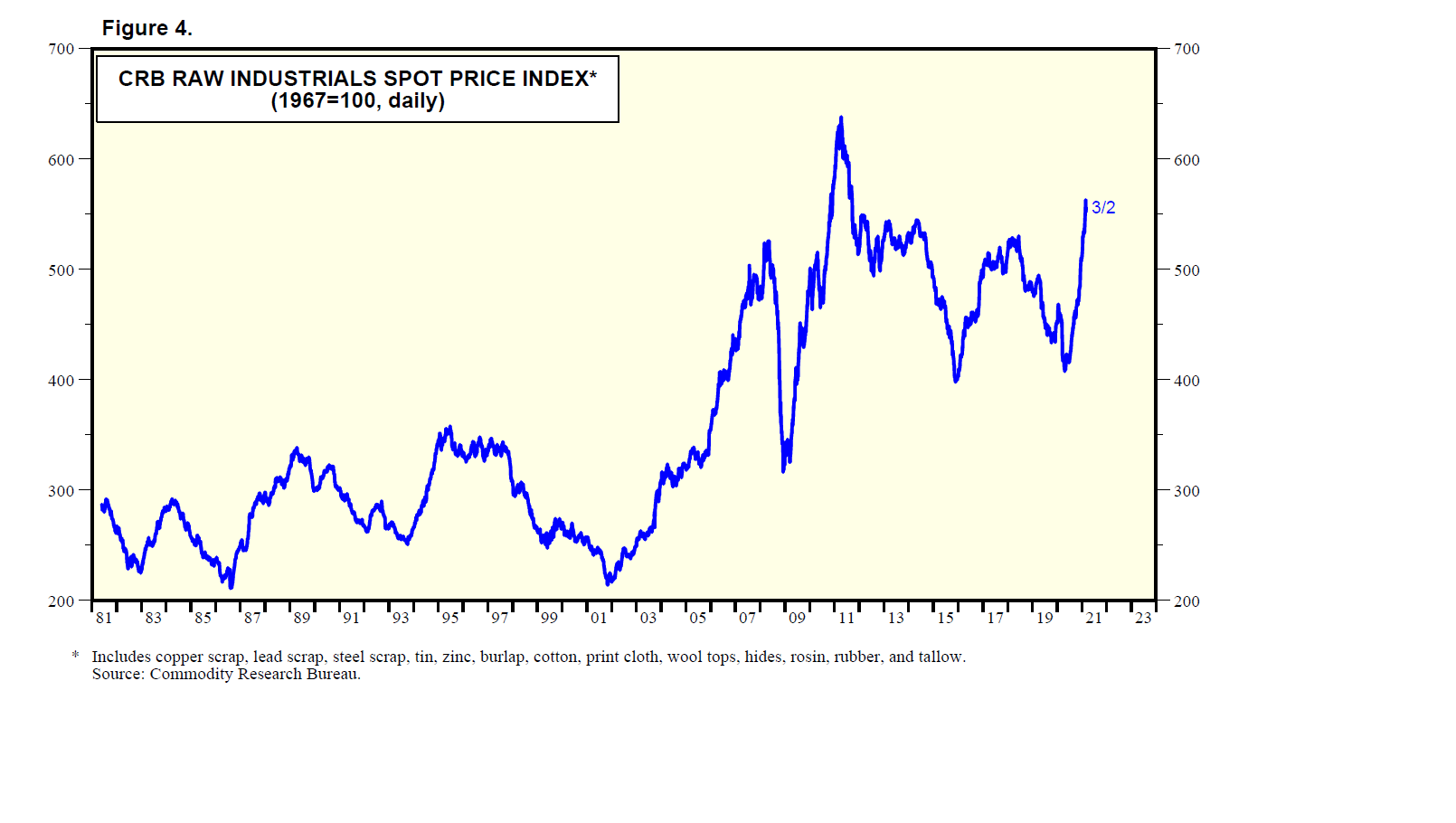

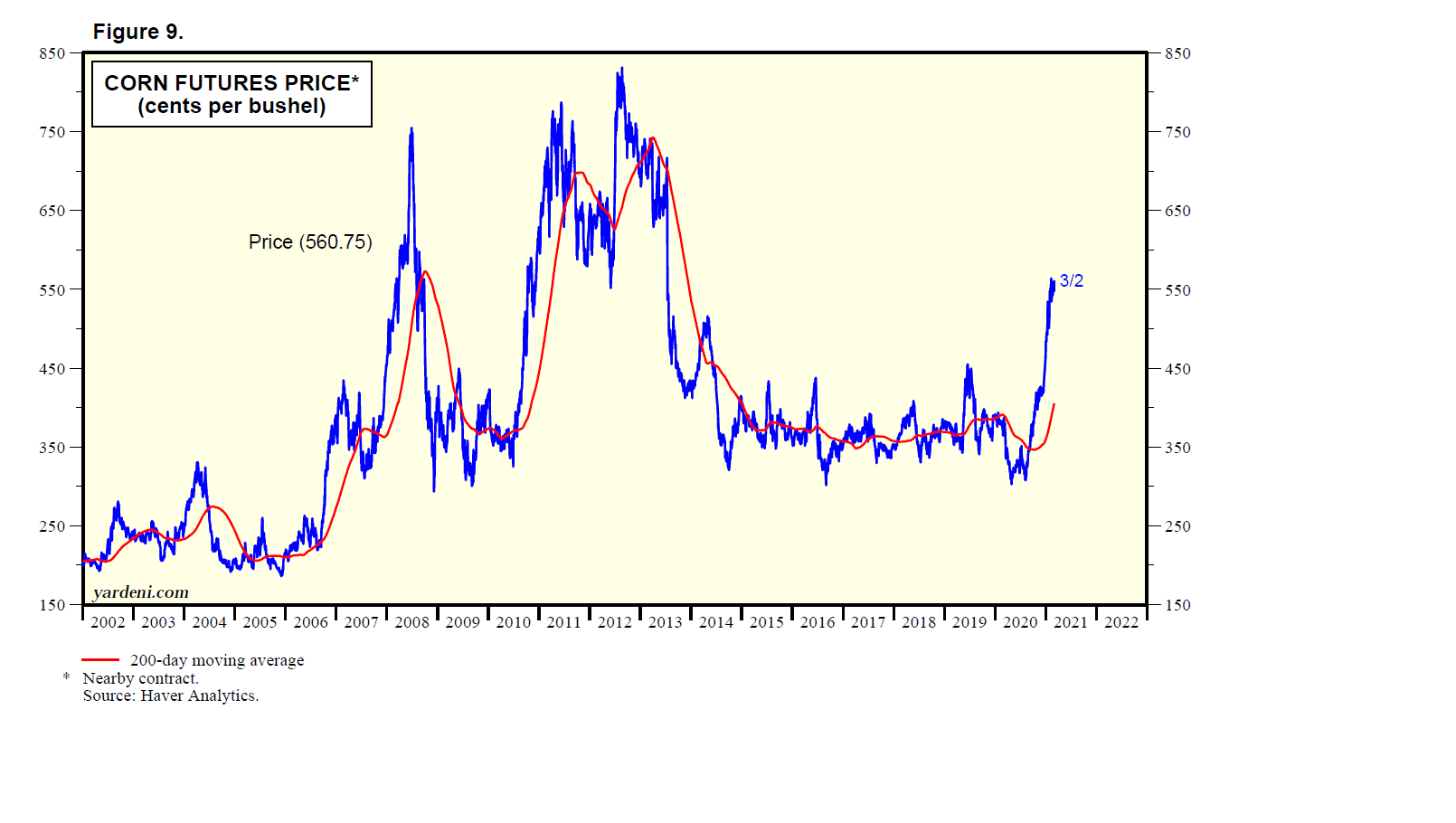

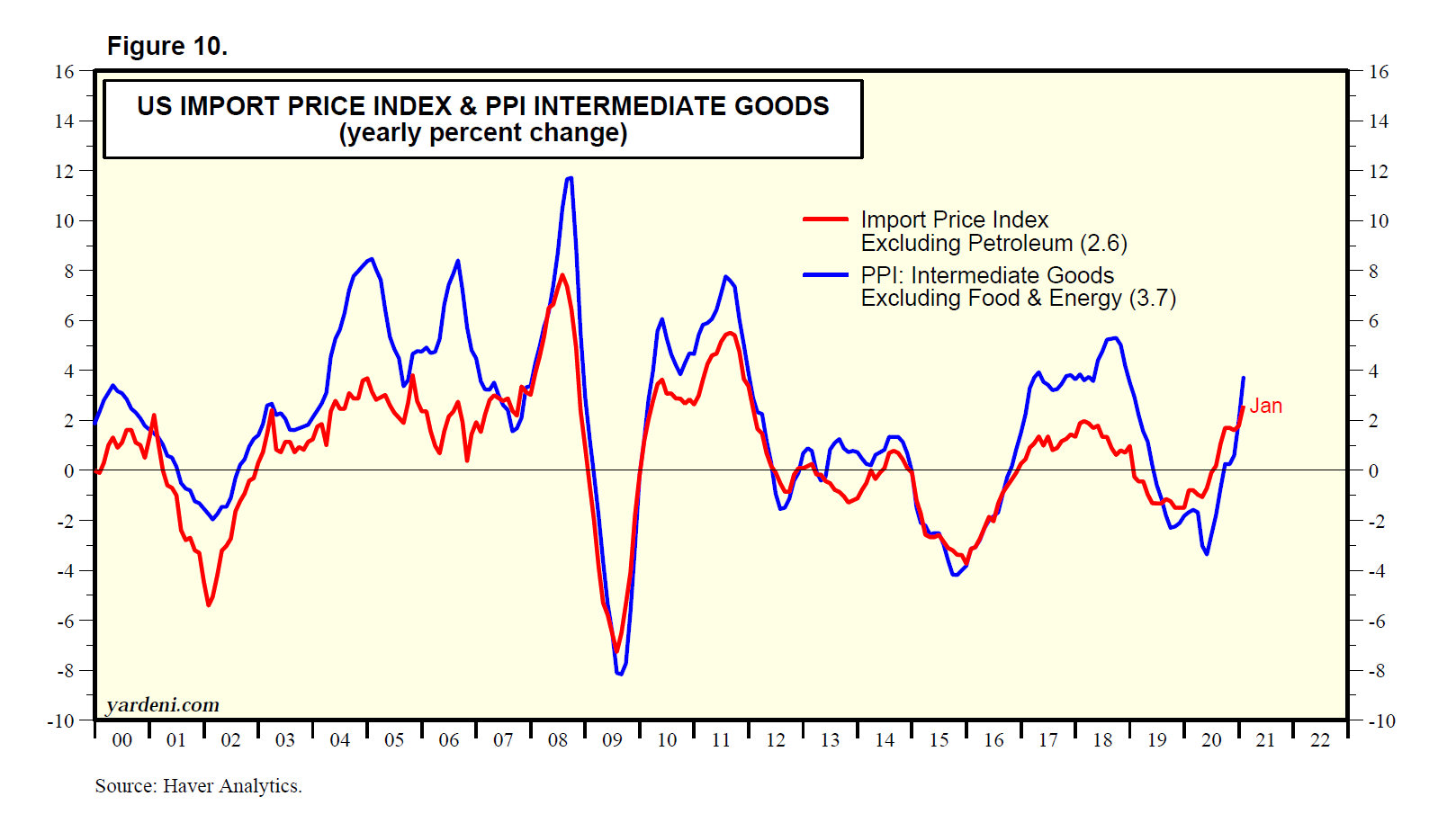

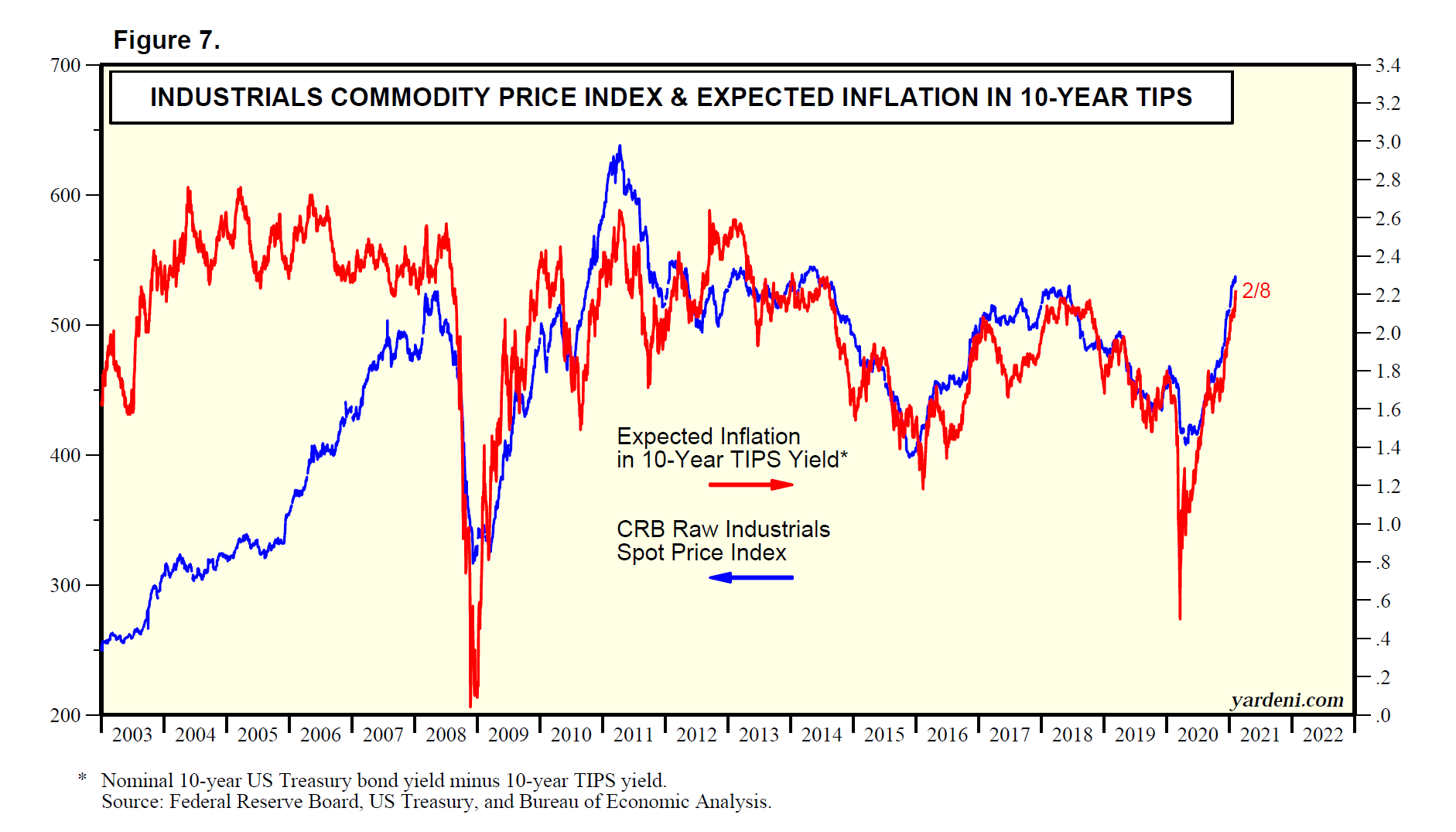

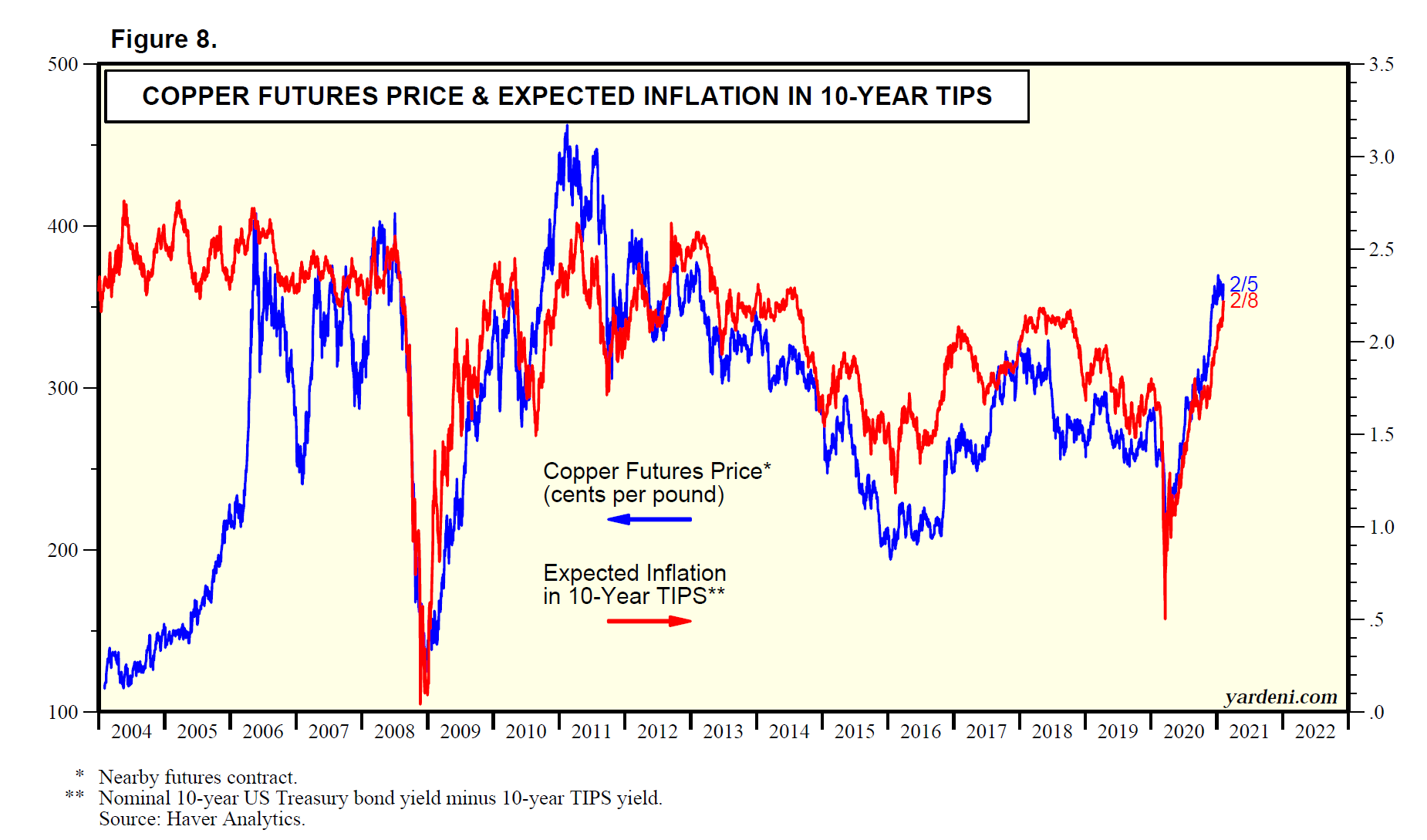

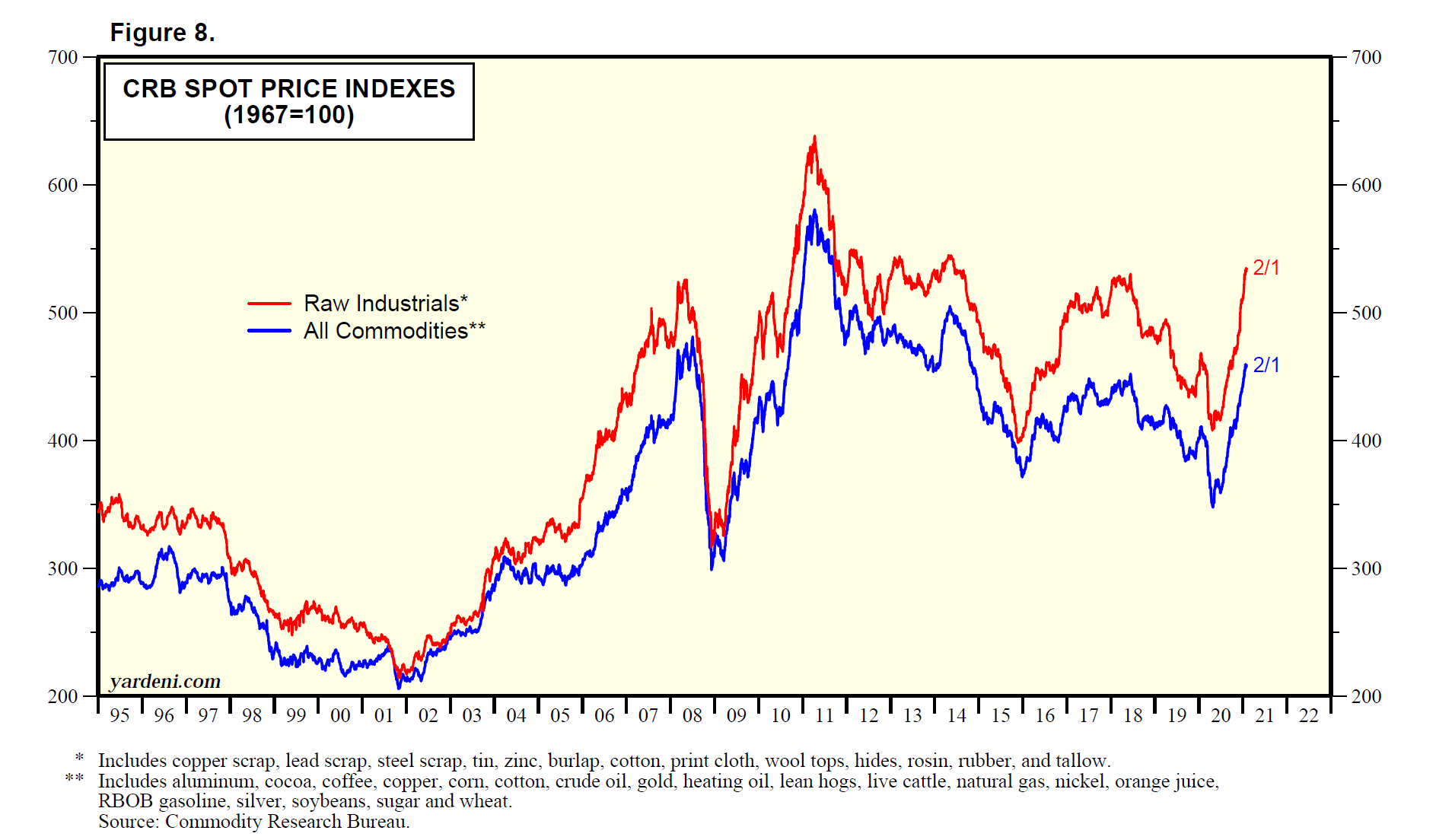

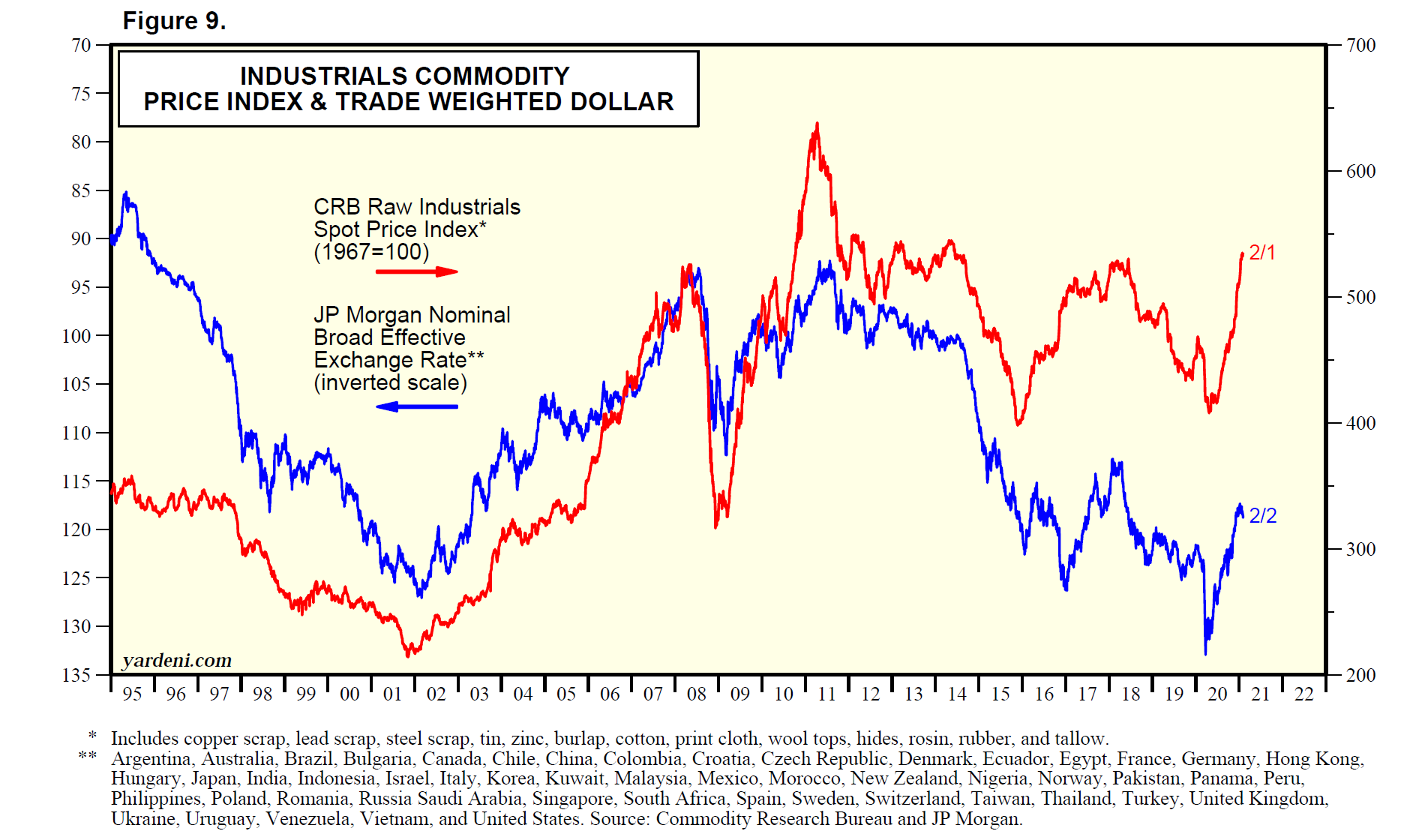

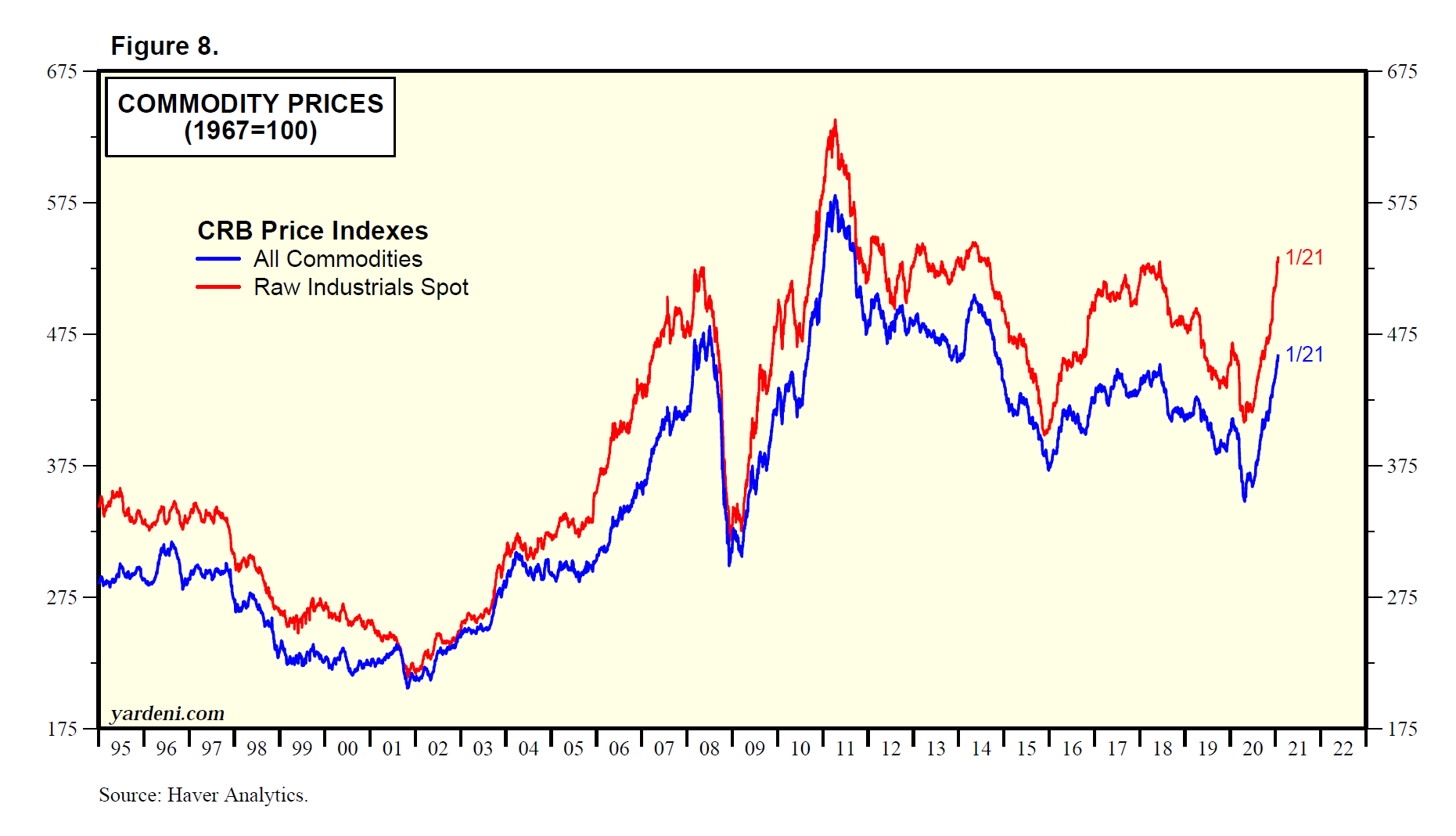

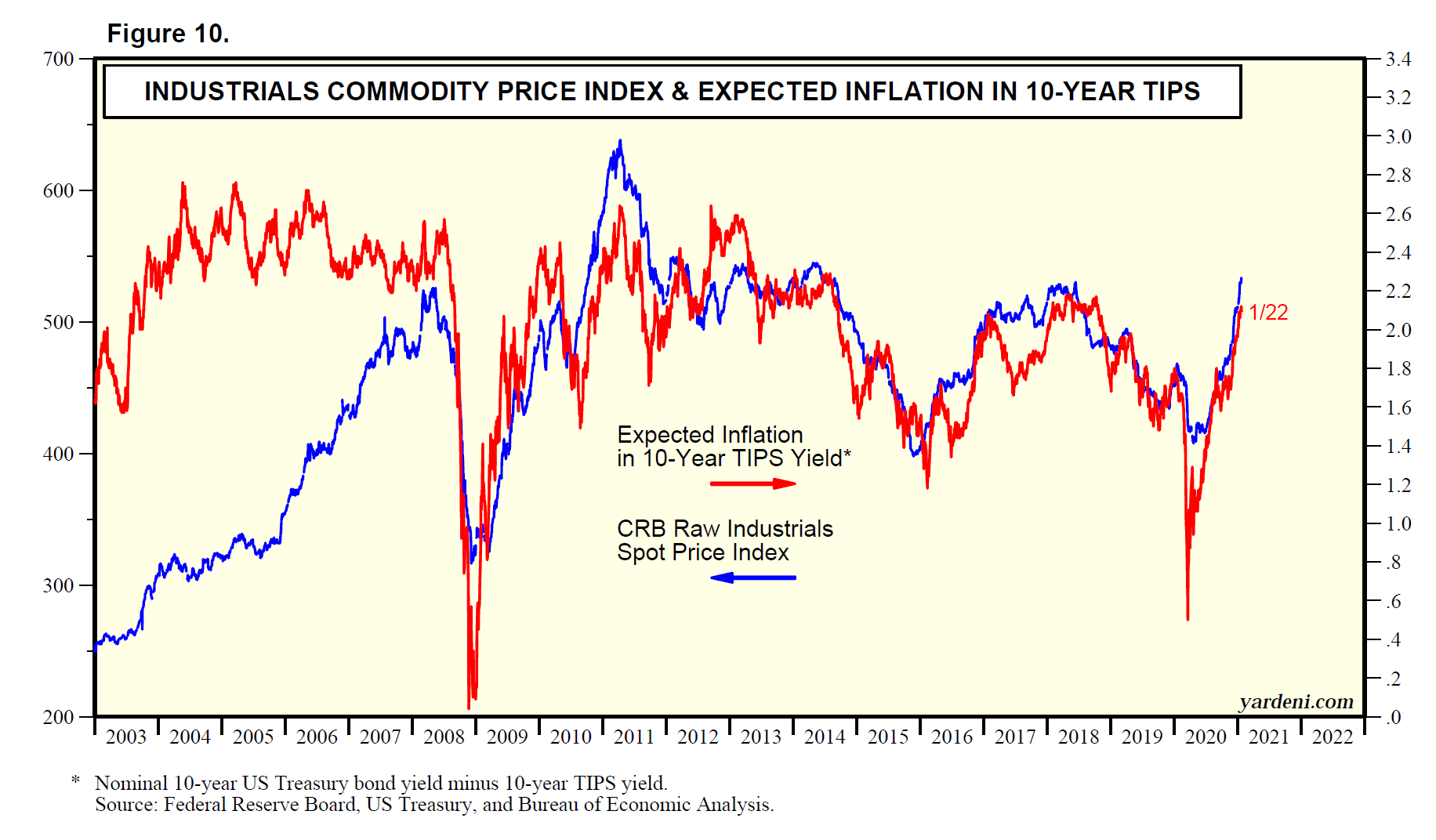

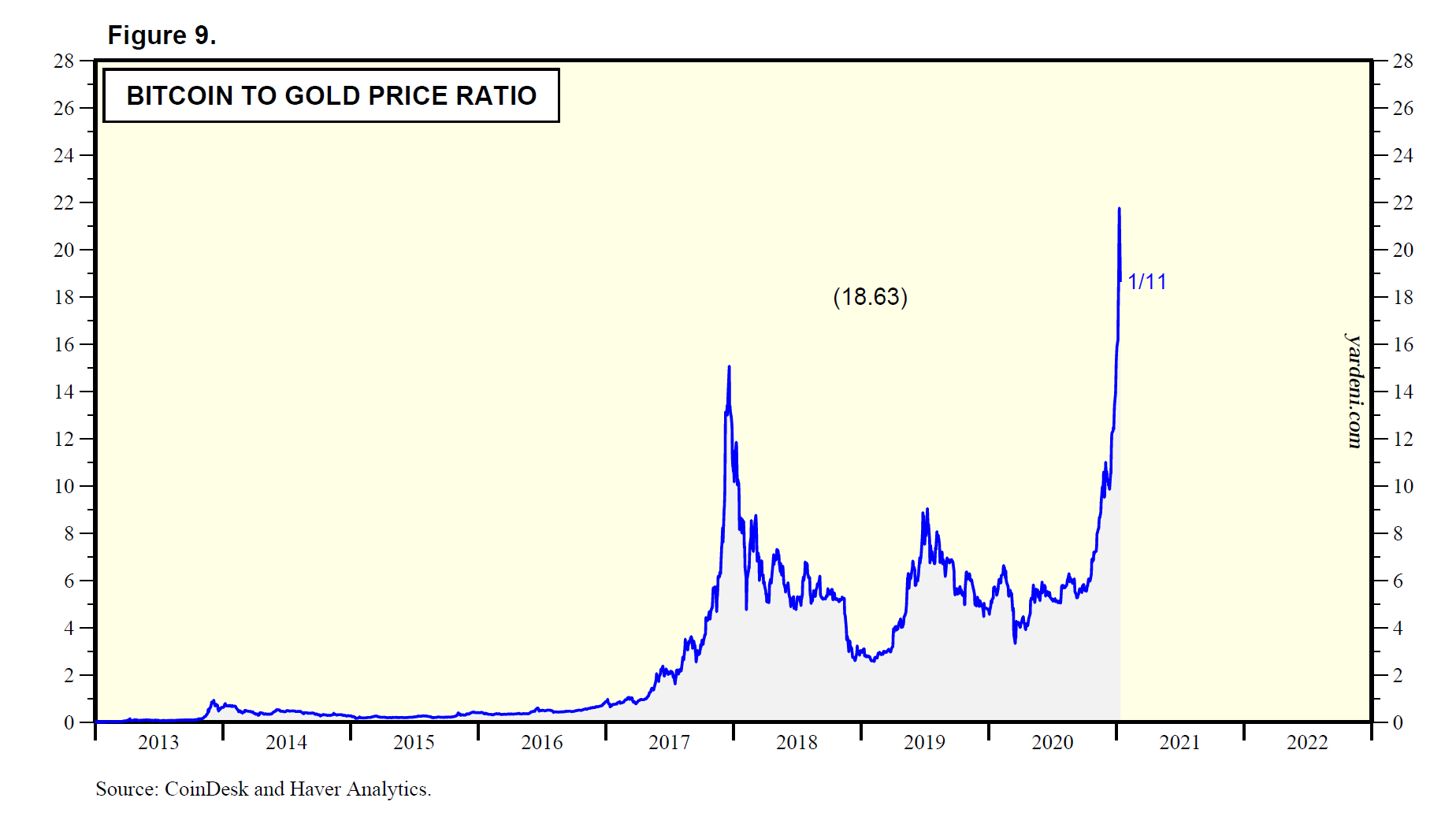

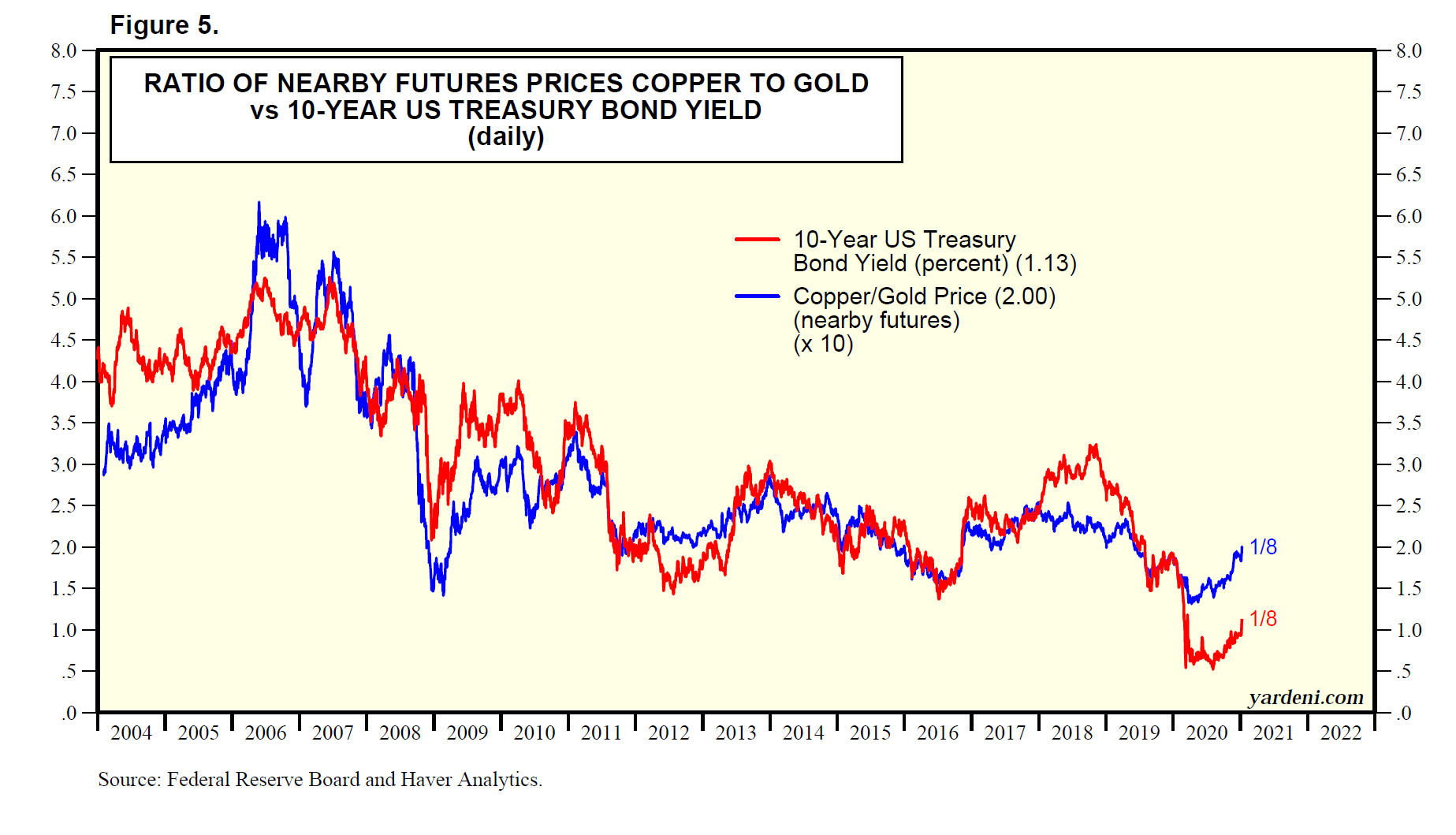

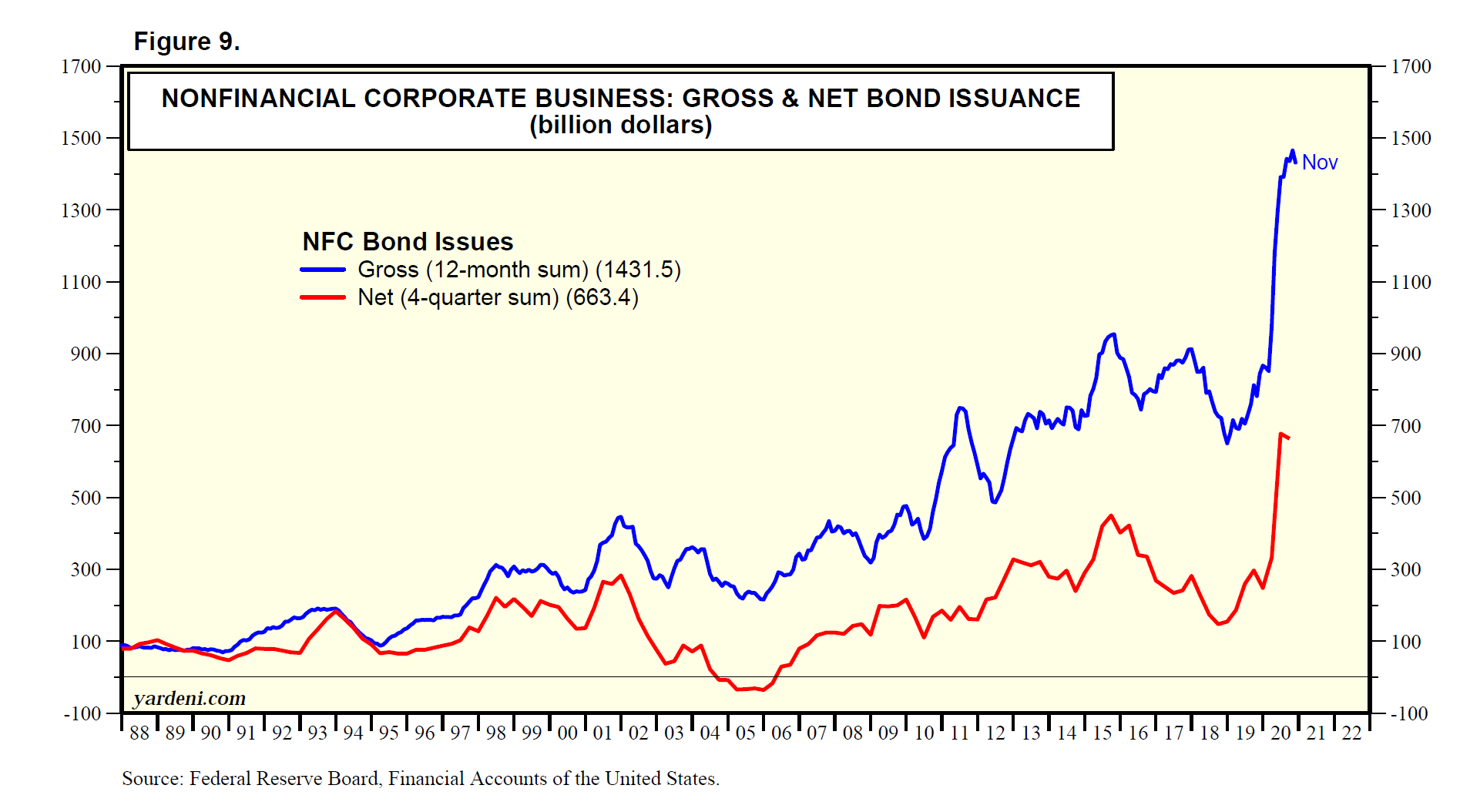

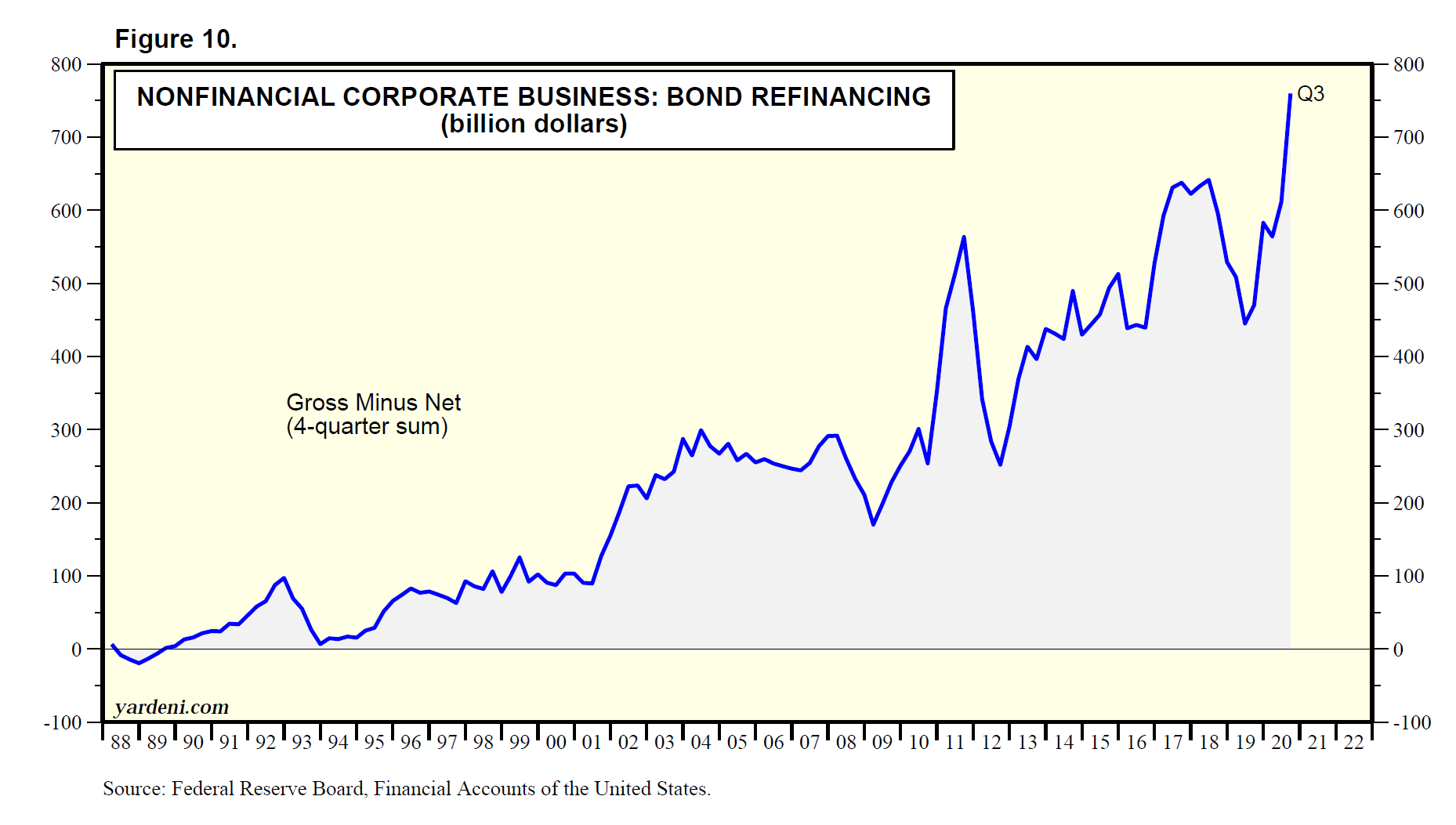

(3) Commodity prices peaking. Slower global economic growth, especially in China, and more hawkish central bank policies seem to be capping the CRB all commodities index and the CRB raw materials index (Fig. 9). The same can be said about the price of copper (Fig. 10).

US Fiscal Policy: No Xmas Gift. The Senate adjourned for the year early Saturday morning and will return to Washington on January 3. My vote is to let the senators stay home for 2022. The Hill observes that “leaving for the holidays officially punts both President Biden’s climate and social spending legislation and voting rights legislation, which would require a change in the Senate rules, into next year.”

On Friday, Senate Majority Leader Charles Schumer (D-NY) acknowledged that Biden’s BBB legislation won’t be enacted this year. He is expecting that Biden will negotiate a BBB deal with Senator Joe Manchin (D-WV), a key vote, by early next year. Manchin would like to hold off on another round of fiscal stimulus because it would add to the current bout of inflationary pressures.

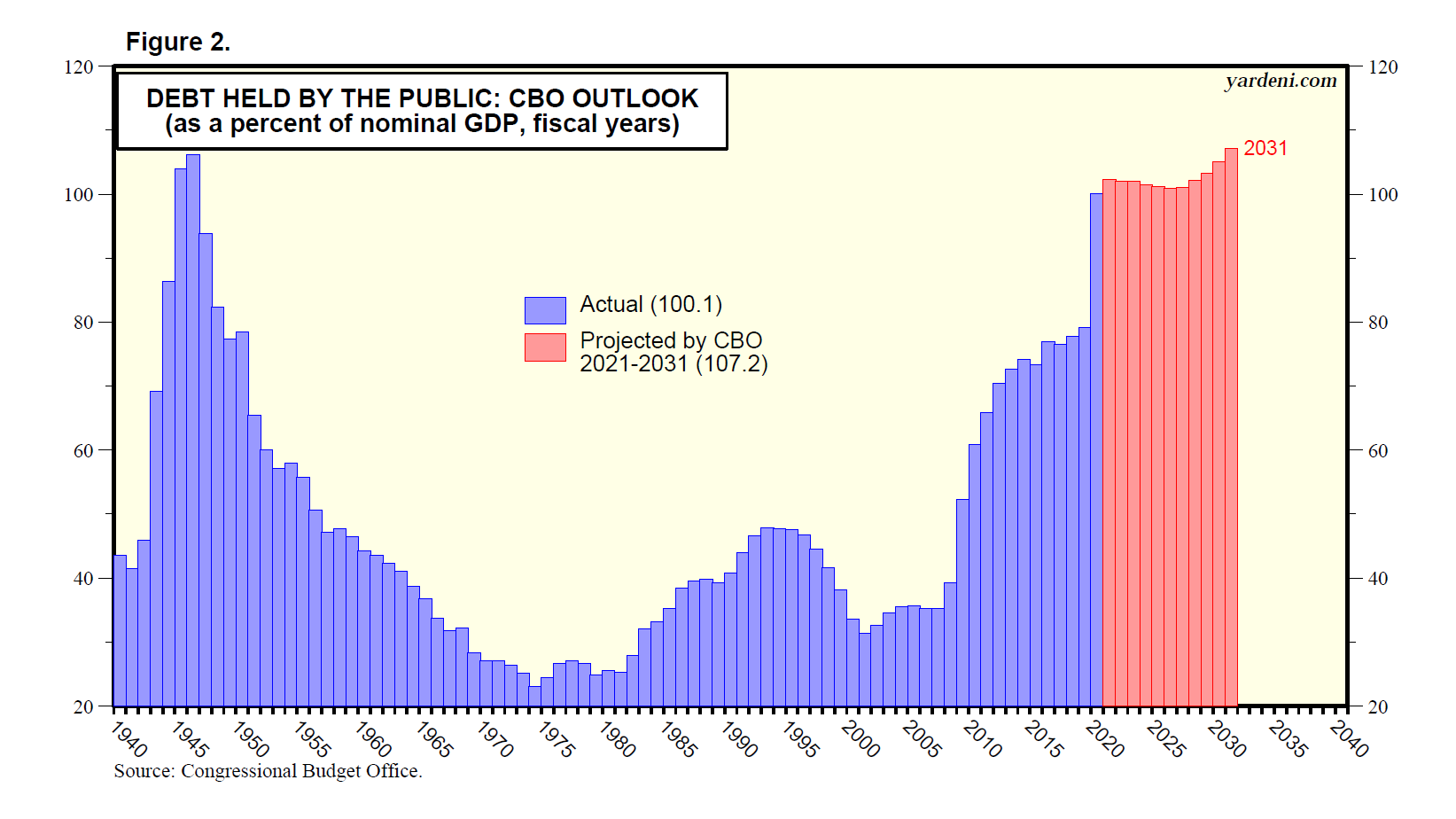

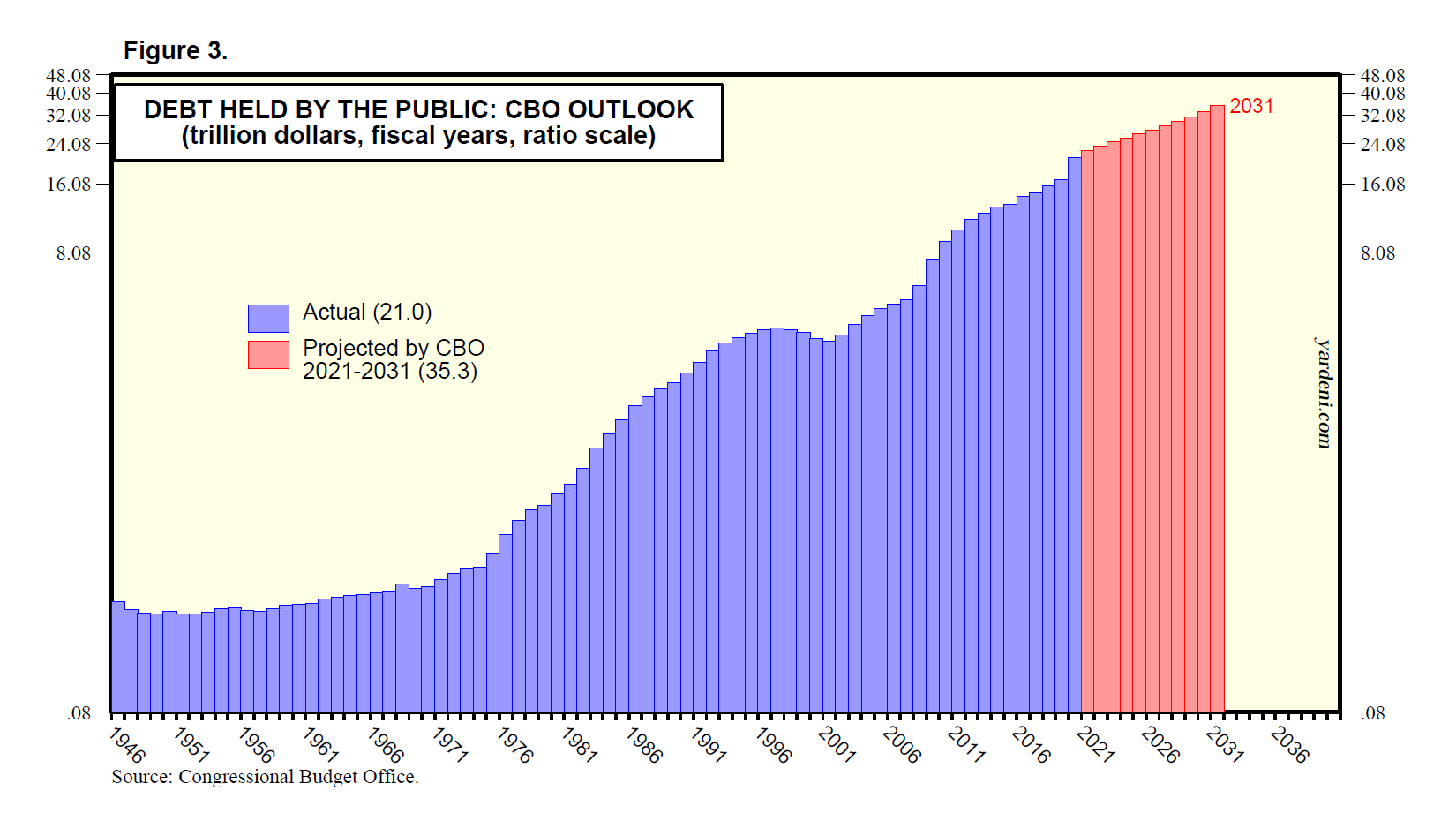

Jim Lucier, our good friend at CapitalAlpha, is one of the most astute Washington watchers. He currently believes that a streamlined version of BBB could eventually get done, but probably not until February at the earliest. He expects it to be reduced to $1.5 trillion and to maintain the 21% corporate tax rate as well as other positive features of the Trump tax reform. He attributes this expectation to the actions of Senator Kyrsten Sinema (D-AZ). To get her vote for BBB, she has demanded no corporate rate hike, no individual rate hike, no capital gains rate hike, and no broad based tax increase of any kind. The result would be a bill with $1.5 trillion in other revenue raisers.

However, as Jim observes, “The problem is that progressives and the Biden administration are not happy with $1.5 trillion paid-for and still want to cram $5 trillion worth of stuff in a $2 trillion package.” A December 10 letter from the director of the Congressional Budget Office (CBO) responded to questions from a couple of members of Congress about BBB. They wondered what the impact would be if “specified modifications … would make various policies permanent rather than temporary.” The response stated that it would increase the deficit by $3.0 trillion over the 2022–31 period.

Late-breaking news: On Sunday morning, CNBC reported that Senator Manchin said he won't vote for Biden’s Build Back Better Act, likely killing the bill for now.

China: Disappearing People. People who have criticized China’s Beijing regime often vanish for several months, during which time they are interrogated in a nondescript government building, according to a recent article in The Telegraph. They are abducted under the Chinese regime’s program of “enforced disappearances,” known officially as “RSDL,” or “Residential Surveillance at a Designated Location.” Many then “re-emerge in society with an outwardly different personality, their plucky mode of resistance replaced by a supine deference to Beijing authorities.”

Chinese tennis star Peng Shuai went missing for more than two weeks after claiming in a social media post that former Vice Premier Zhang Gaoli had forced her to have sexual relations with him. She briefly returned to the public eye when she spoke to the president of the International Olympic Committee during a 30-minute video call on Sunday, November 21. She insisted that she was safe and well at her home in Beijing.

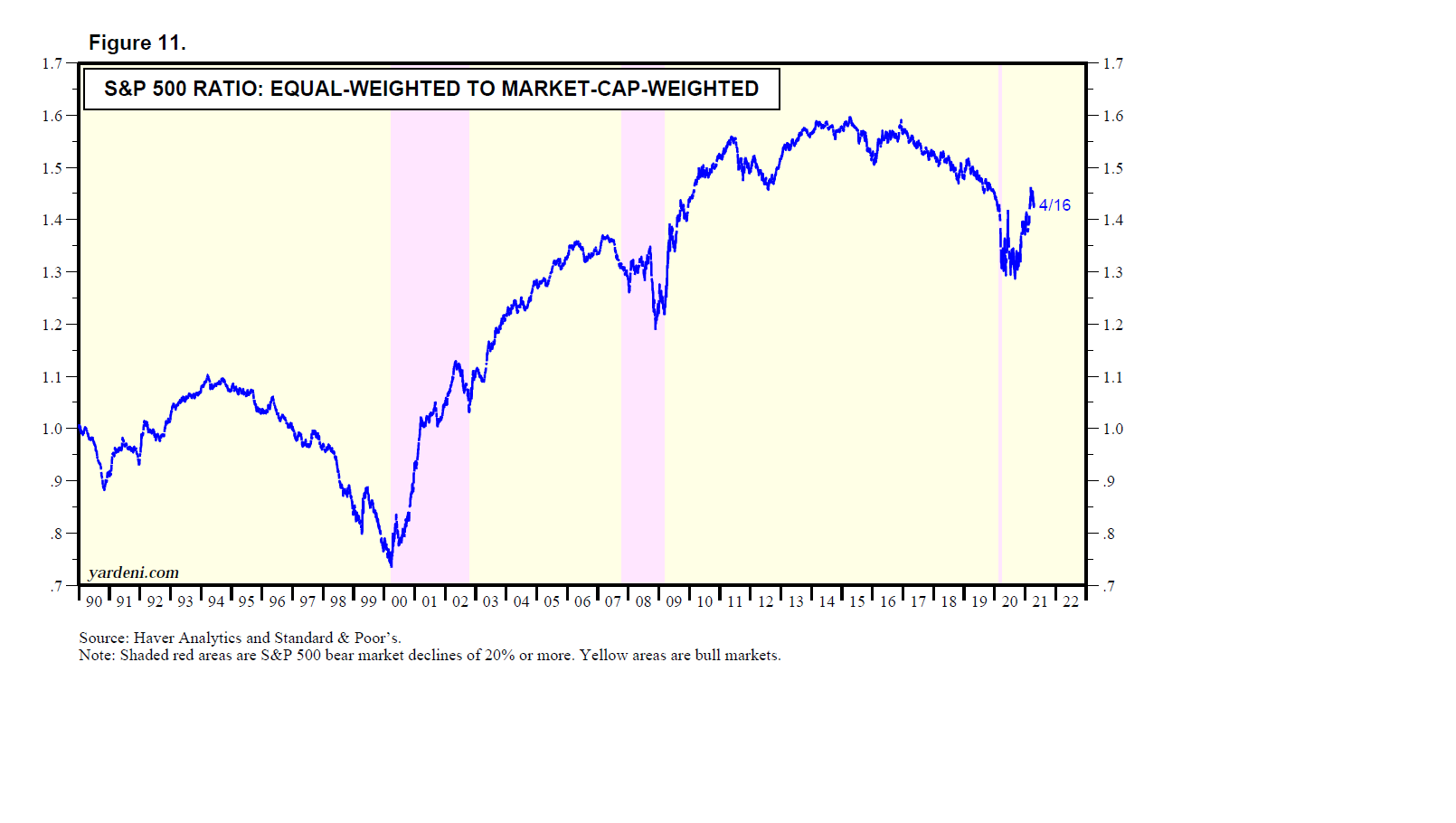

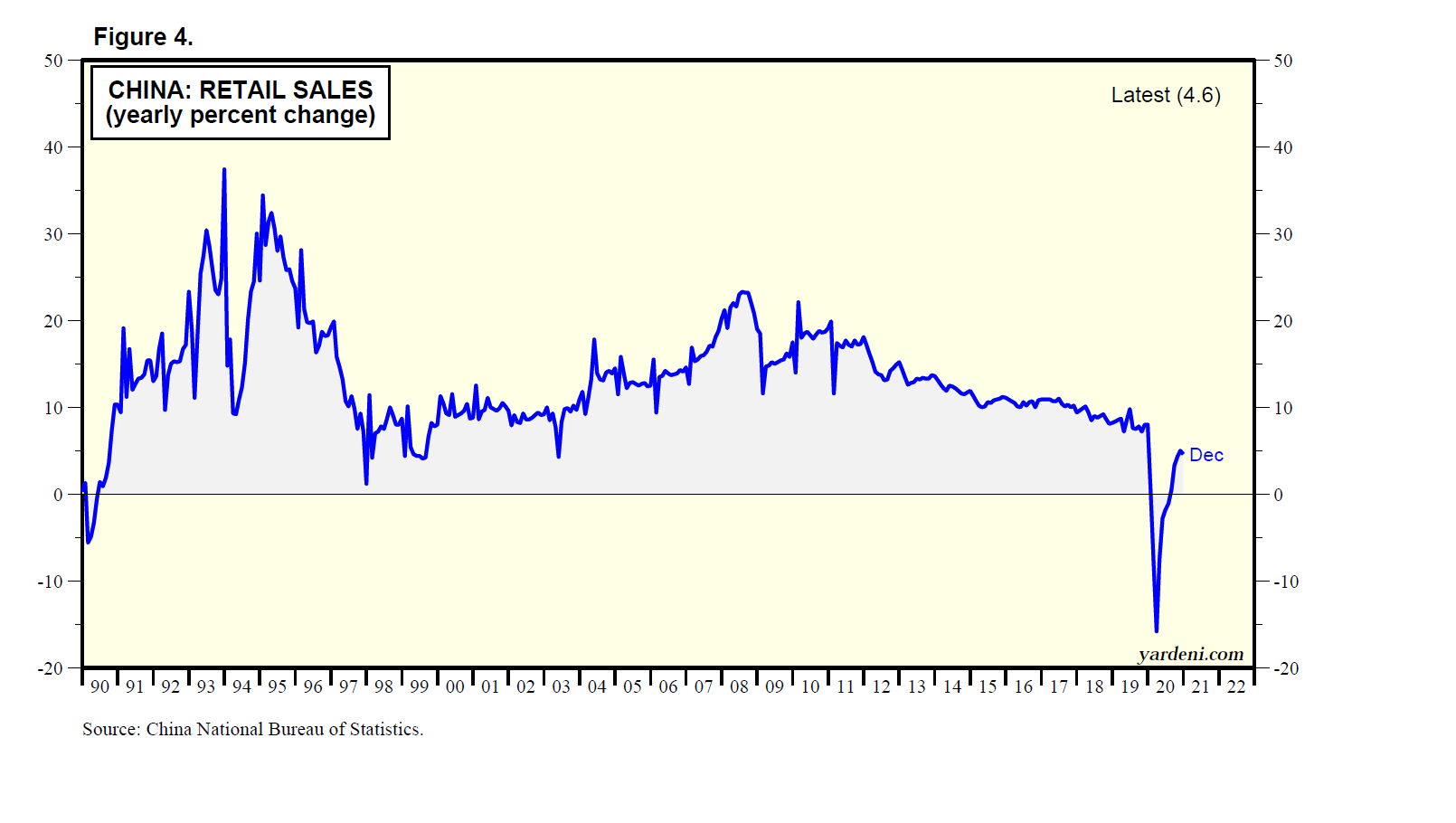

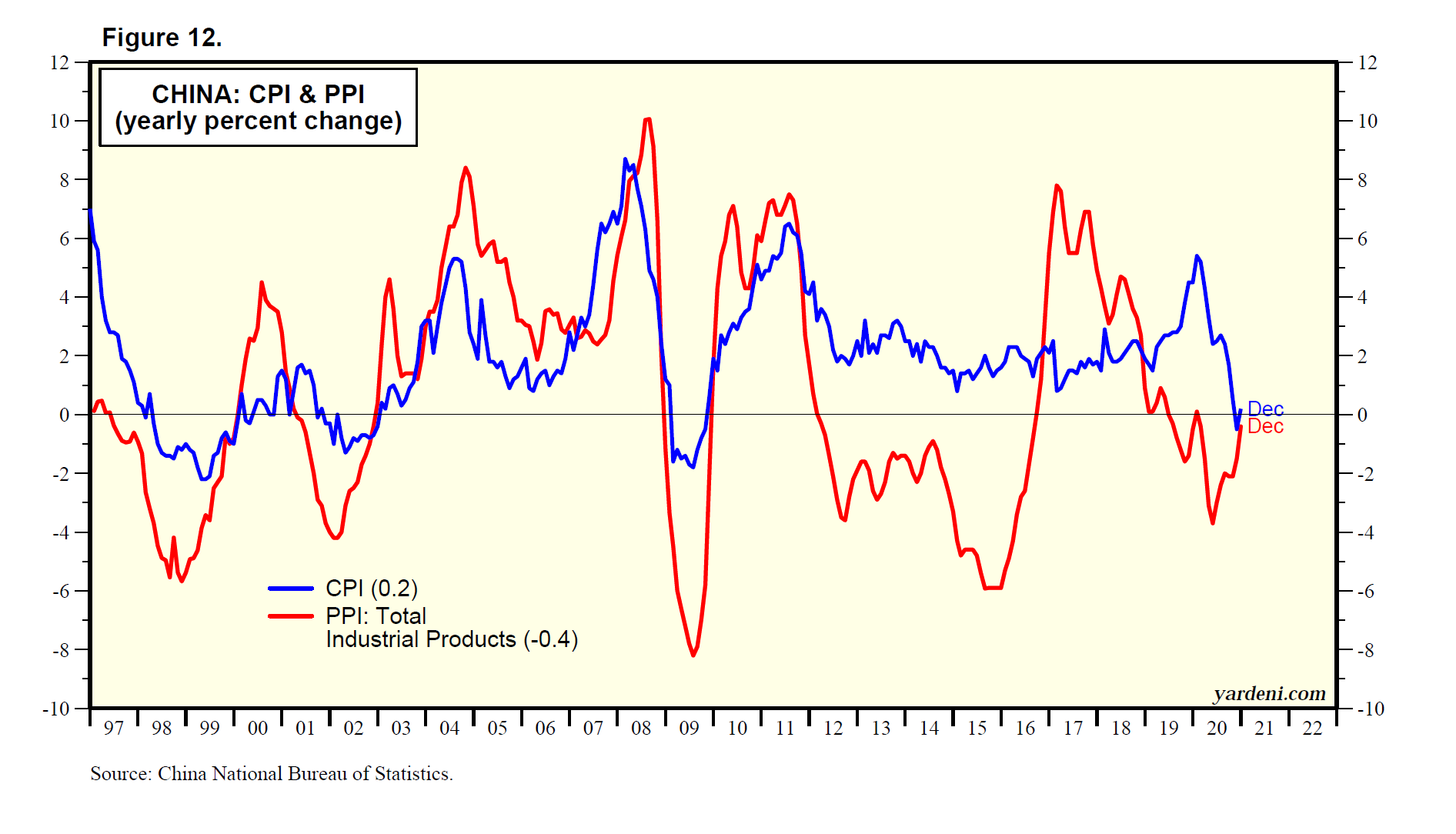

Also gone missing is China’s working-age population (Fig. 11). This development likewise can be attributed to the Chinese Communist Party’s (CCP) authoritarian policies, particularly the one-child limits imposed on families from 1980 to 2015. The result has been a drop below the replacement fertility rate since the second half of the 1990s (Fig. 12). Rapid urbanization also contributed to the drop in fertility, which now is rapidly converting China into the world’s largest nursing home.

The Chinese government reversed course in 2015, eliminating the one-child policy in an effort to boost population growth. The CCP wants China to be a global superpower. That’s hard to do while the nation’s demographic profile is turning increasingly geriatric. Consider the following:

(1) China’s birth rate dropped to a new low in 2020, confirming the demographic challenge facing the government as it tries to deal with a shrinking labor force and growing population of elderly people. There were 8.5 births per 1,000 people last year, the lowest in data back to 1978, according to the latest yearbook from the National Bureau of Statistics.

(2) The number of newborns may decline again this year from the 12 million born in 2020, a health commission official said in July. Some demographers estimate that China’s population could have started falling this year. Critics of the CCP have charged that Beijing is disproportionately reducing births among its Muslim minority in the Xinjiang region as part of an ethnic-cleansing crackdown.

(3) We believe that the combination of urbanization and the one-child policy is weighing heavily on Chinese consumers. Just think about all those young adults who are the only children of two elderly parents. In China, children have a social responsibility to take care of their aging parents. That’s a heavy burden for only children. A married pair of only children has four older parents to support.

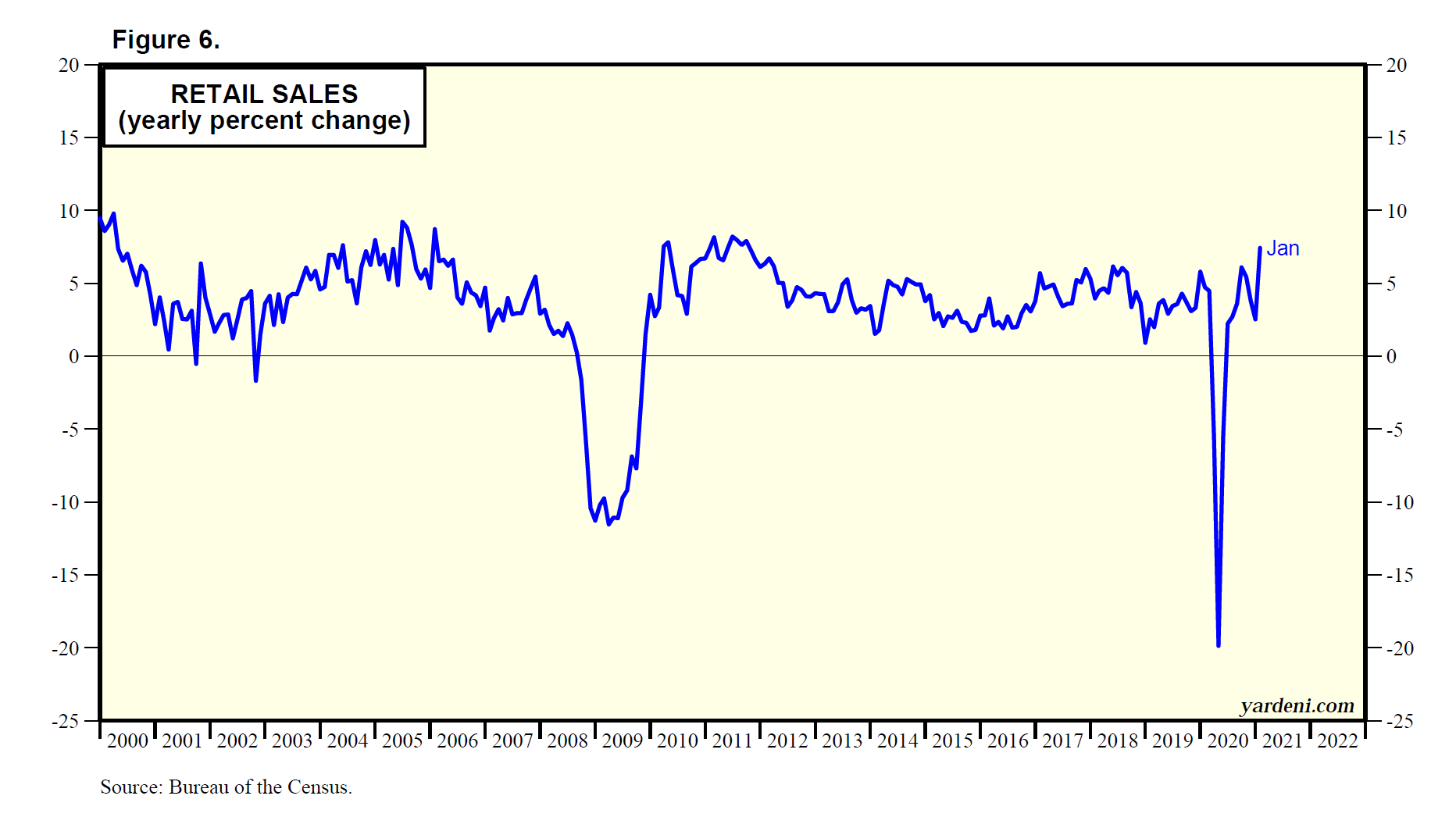

This certainly helps to explain why the growth rate of inflation-adjusted retail sales has plunged in recent years. Every month, the Chinese government releases data on the y/y growth in nominal retail sales and the CPI. A few years ago, we realized that we could easily calculate real retail sales using the two series (Fig. 13). During November, retail sales rose only 3.9%, while the CPI increased 2.3%, resulting in a 1.6% increase in real retail sales.

To better see the underlying trend in real retail sales growth, Debbie and I track the 24-month percent change in the 24-month average of real retail sales at an annual rate (Fig. 14). It shows a calamitous plunge in real retail sales growth from about 18% ten years ago to ZERO as of November!

(4) That’s very bad news for China’s economy, especially now that China’s speculative property bubble is bursting. On Friday, S&P Global Ratings downgraded China Evergrande Group to one of its lowest possible ratings, a cut that means the world’s three largest credit-rating firms all now judge the giant developer to be in default. The December 17 WSJ reported: “Failures to repay investors are piling up in China’s property sector, as real-estate companies buckle under the strain of falling home sales, government curbs on borrowing and a massive bond-market selloff that has made it difficult for many firms to raise fresh funds.”

The government is trying to engineer a soft landing. The People’s Bank of China lowered reserve requirements by 50 bps on December 6 (Fig. 15). Yet a soft landing is a tall order because the ailing property market accounts for between a quarter to a third of annual GDP growth in China. Again, the CCP’s aspirations to make China a superpower may flounder along with its economy.

Movie. “Spencer” (+) (link) is described as a fable based on what really happened to Princess Diana, admirably played by Kristen Stewart. It’s an intense psychological look at her life focusing on three days over Christmas 1991 at Sandringham, Queen Elizabeth’s estate in the UK. The biopic suggests that she might have hit bottom during those three days near the end of her unhappy marriage to Prince Charles. She did her best to spend as little time as she could with him and the other royals. Diana is clearly miserable, as shown by her eating disorder and visions of Anne Boleyn, who was beheaded by her faithless husband, King Henry VIII. This Christmas film is a depressing antithesis of “It’s A Wonderful Life,” and should be watched after the holiday season.

Will 2022 Be Better Than 2021?

December 16 (Thursday)

Check out the accompanying pdf and chart collection.

(1) Outdoor gas heaters collecting dust. (2) Taking on the bears. (3) Higher buybacks mean more stock grants. (4) Coming tax hikes may be spurring insider stock sales. (5) Households own lots of stock, but are they crazy like a fox? (6) Stocks have rallied at the start of Fed tightening cycles. (7) What could go right in year ahead? (8) Covid could go from pandemic to endemic. (9) Opportunities in travel-related areas. (10) Boeing could finally fly. (11) Everyone’s getting married. (12) Energy recovery should continue. (13) The year of the autonomous truck.

Strategy I: Countering the Bears. It seems like another lifetime, but only a year ago we would bundle up and gather with friends, appropriately distanced, around newly purchased outdoor gas heaters on sunny winter days. Makeshift opportunities for cautious socialization had to do. There were no extended family gatherings. There were no vacations. The Grinch stole Christmas 2020.

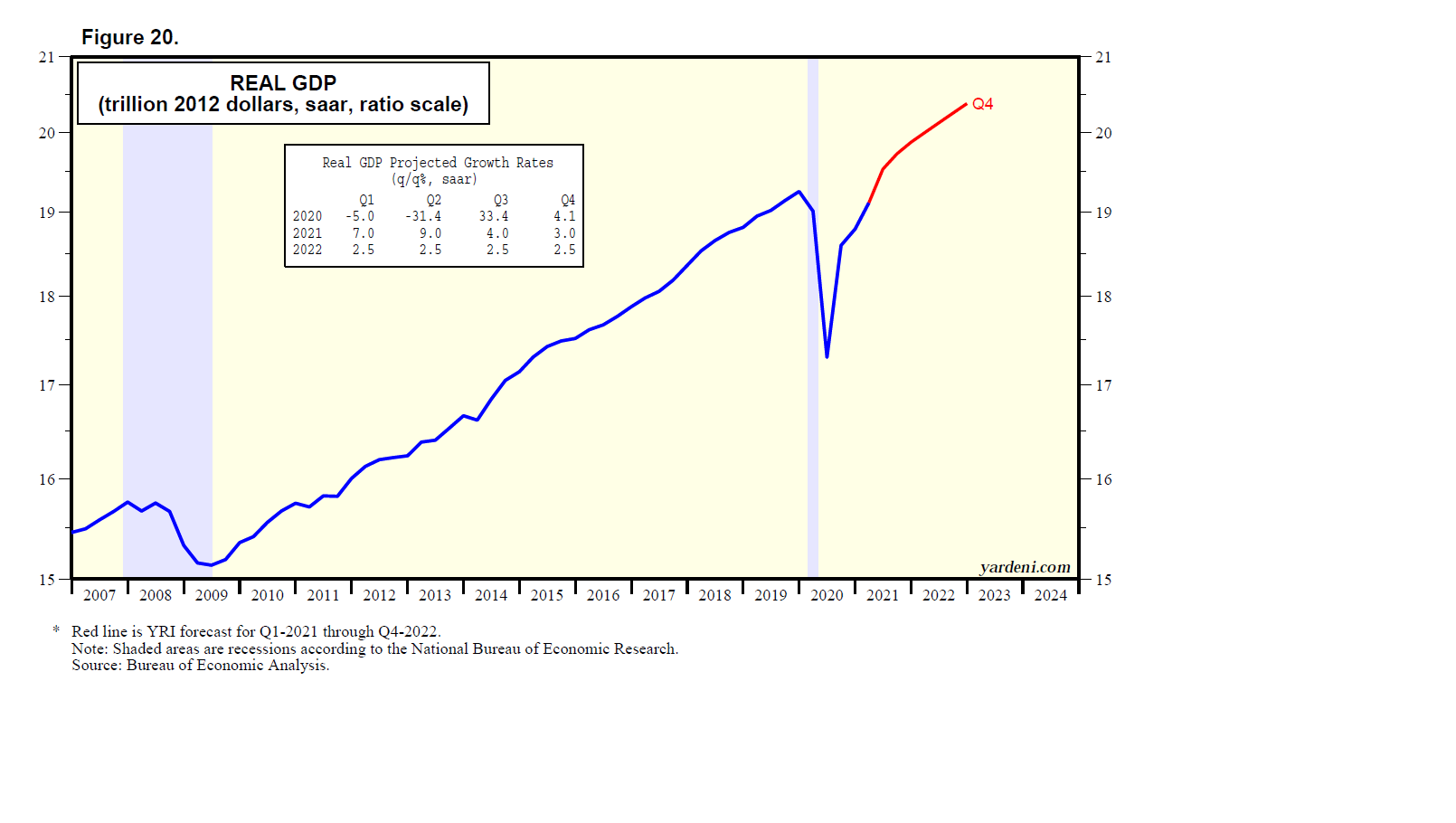

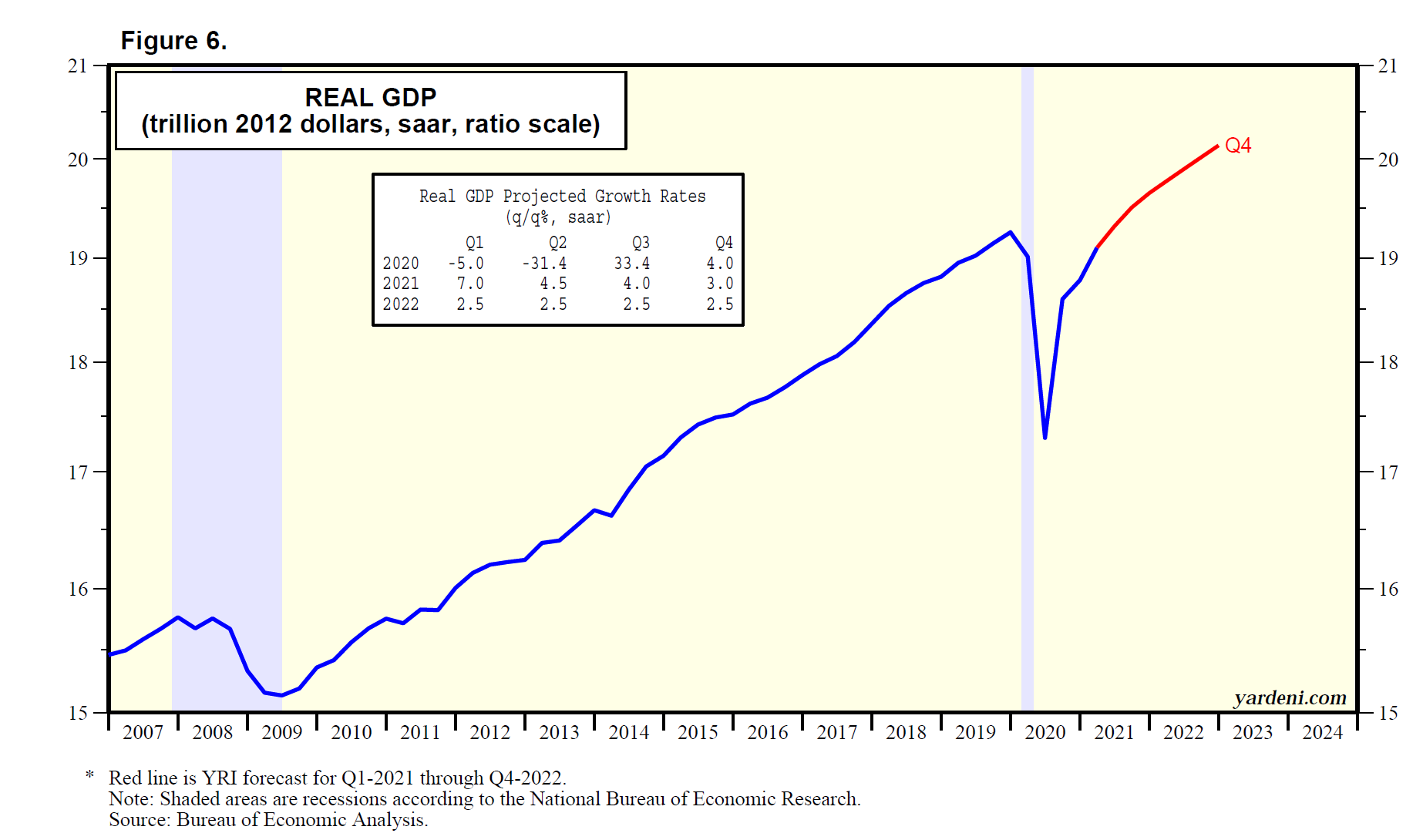

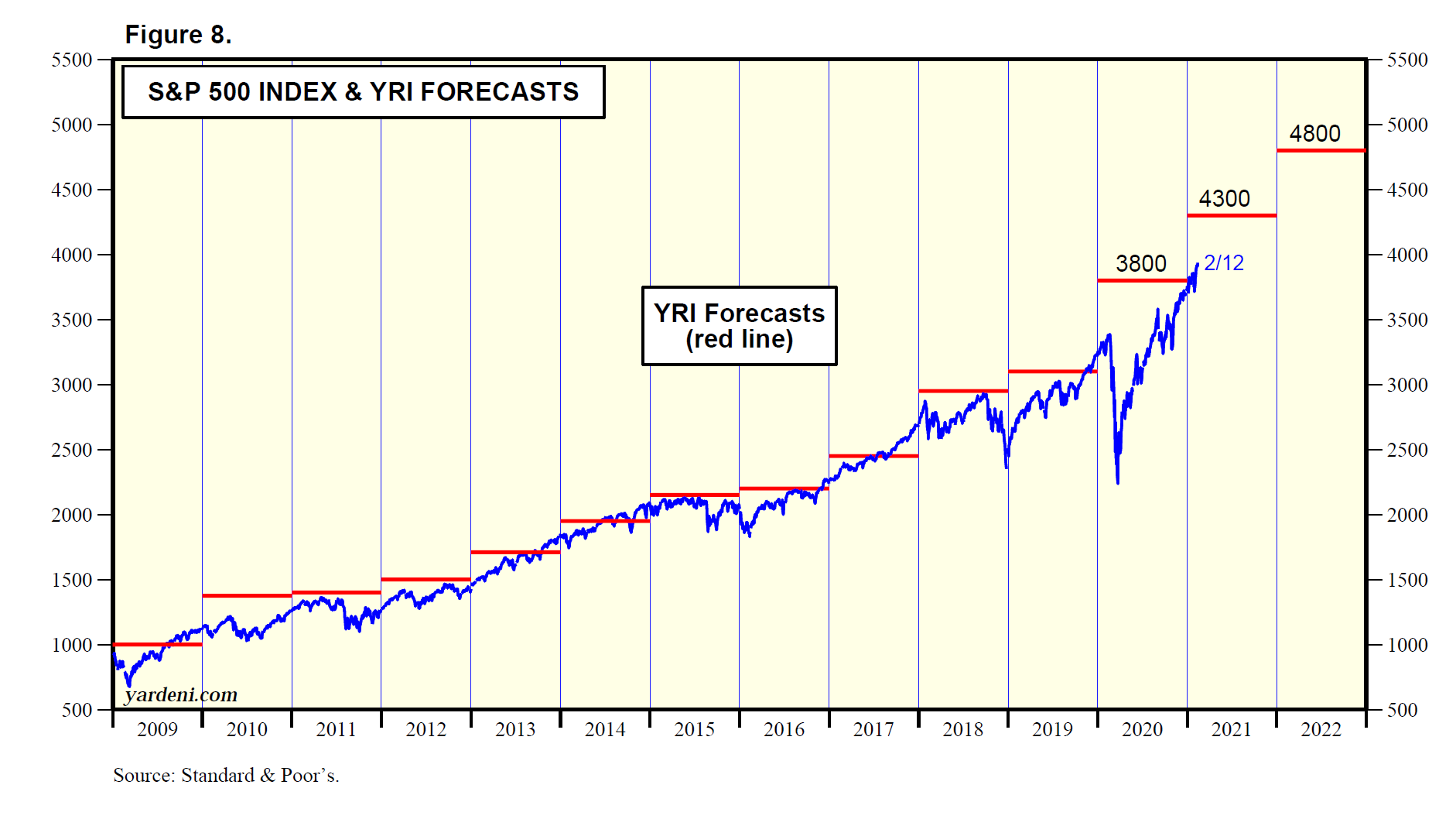

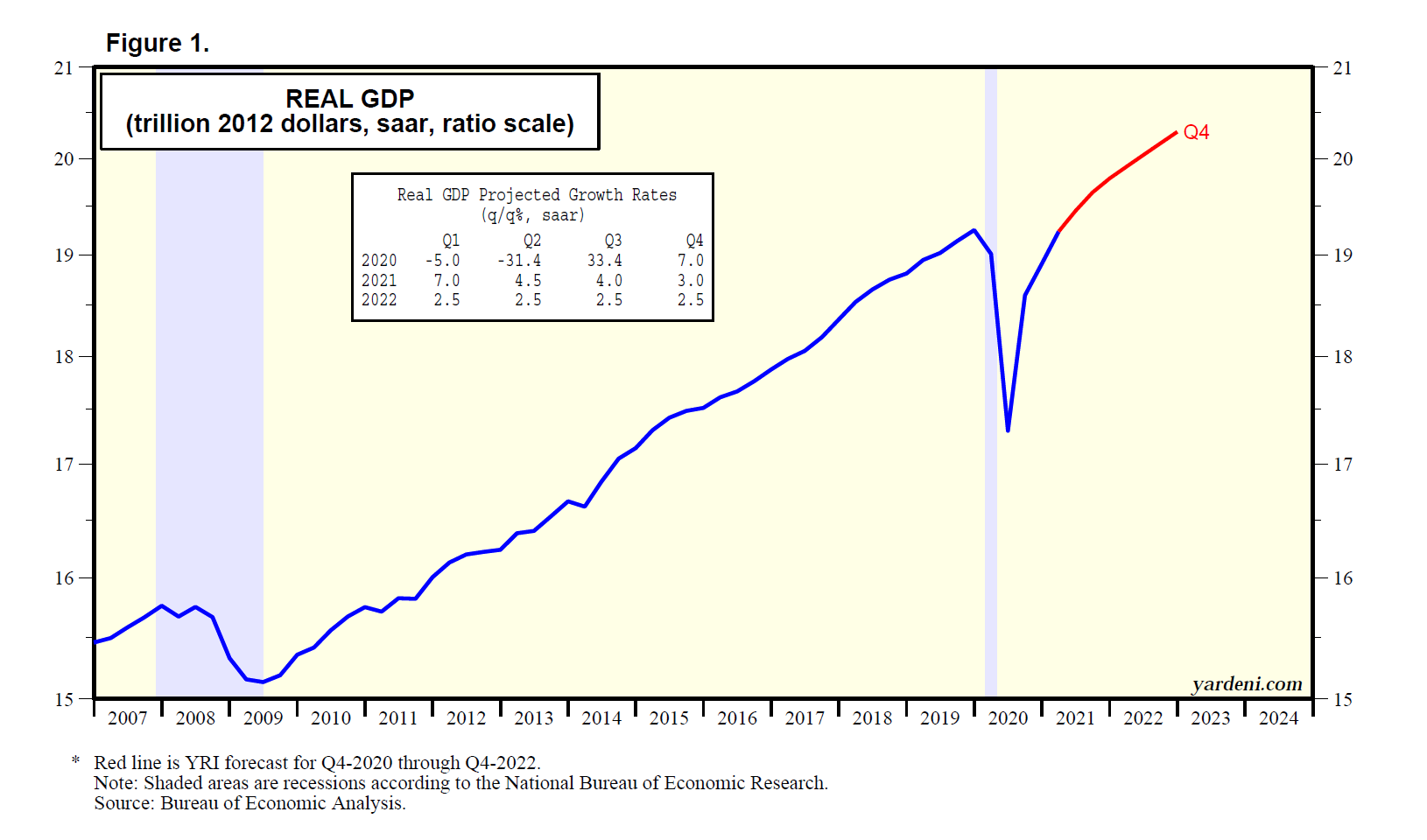

Things aren’t perfect this year, but they’re a heck of a lot better. More than 60% of Americans are fully vaccinated, and many are lining up for boosters. The S&P 500 has risen 23.4% ytd through Tuesday’s close, and GDP growth looks to be on track to rise 5.0% in Q4.

We’re hopeful that the economy will continue to reopen in 2022 and that the slow but steady return to normalcy will drive the market higher. However, the arrival of the Omicron variant may mean that we’re about to take one step back after having taken two steps forward.

But the bears seem too pessimistic. Let’s take a look at why we dismiss some of the bears’ arguments before looking at which areas of the economy and the stock market appear ready to rebound:

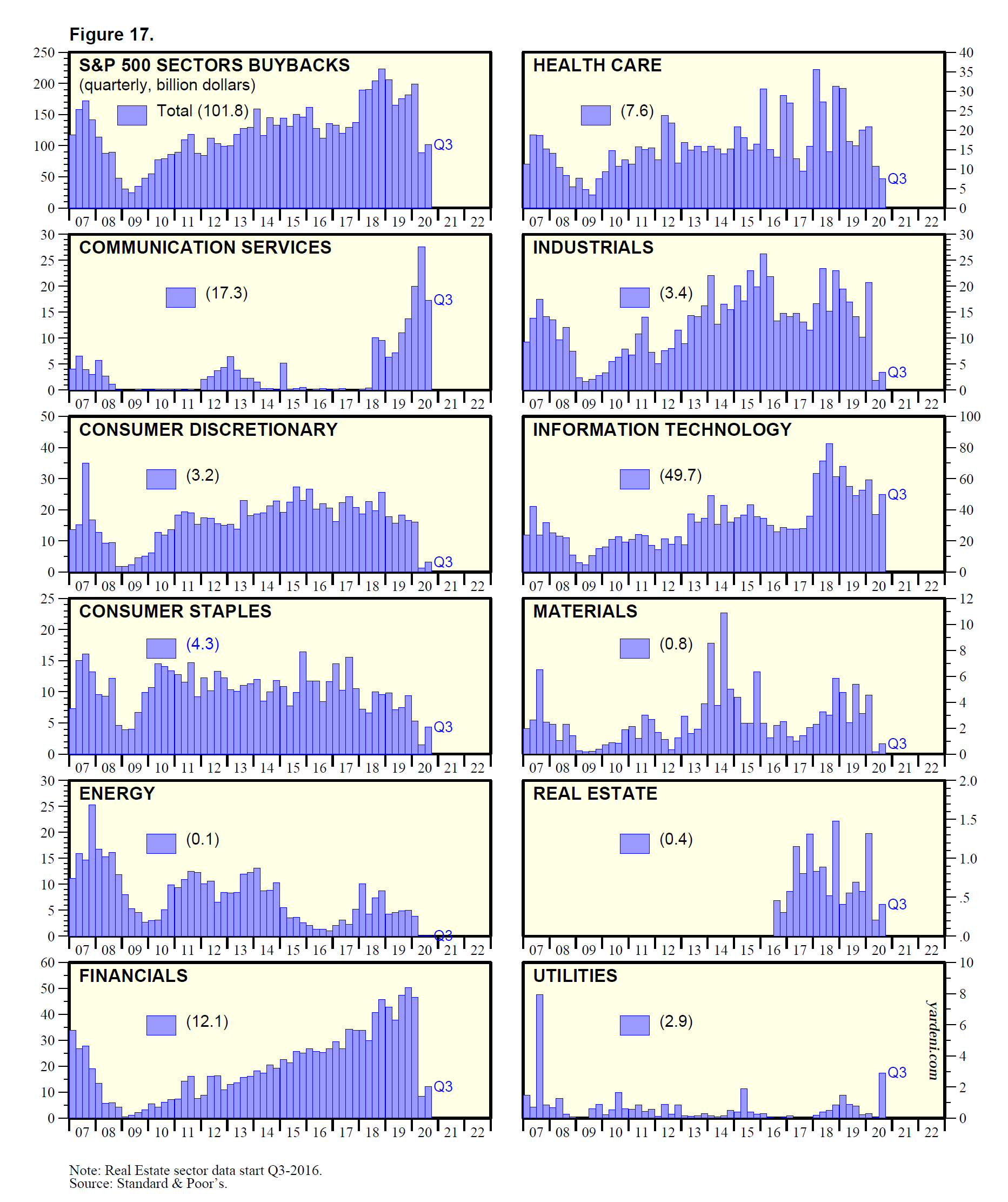

(1) Buybacks are at record highs. According to the preliminary data released by S&P in early December, S&P 500 companies bought back $234.5 billion of shares in Q3-2021, topping the previous record of $223 billion purchased in Q4-2018 (Fig. 1). The record amount marks a rebound from the meager repurchasing done during the height of Covid-19’s rampage in 2020, when economic uncertainty compelled companies to conserve cash. Rather than being a bearish signal, we believe buybacks often rise with the markets because rising markets increase the attractiveness of paying employees with stock grants. The dilution from the grants then is offset by buying back shares, we observed in our 2019 Topical Study “Stock Buybacks: The True Story.”

(2) Insider sales break records too. CEOs and corporate insiders have sold $69 billion of stock in 2021 through the end of November. Insider sales are up 30% from 2020 and up 79% above their a 10-year average according to InsiderScore/Verity data quoted in a December 1 CNBC article. Amazon’s Jeff Bezos, Tesla’s Elon Musk, Facebook’s Mark Zuckerberg, and Walmart’s Walton family account for 37% of this year’s sales. Microsoft CEO Satya Nadella’s sales were also notable: $285 million, or nearly half of his Microsoft shares.

While high stock prices undoubtedly were one reason insiders sold, taxes may be another. The CNBC article noted that by selling now, Nadella and Bezos will save on taxes because the state of Washington is imposing a 7% tax on capital gains over $250,000 starting in 2022. And there are also threats of higher taxes on high earners coming from Washington DC.

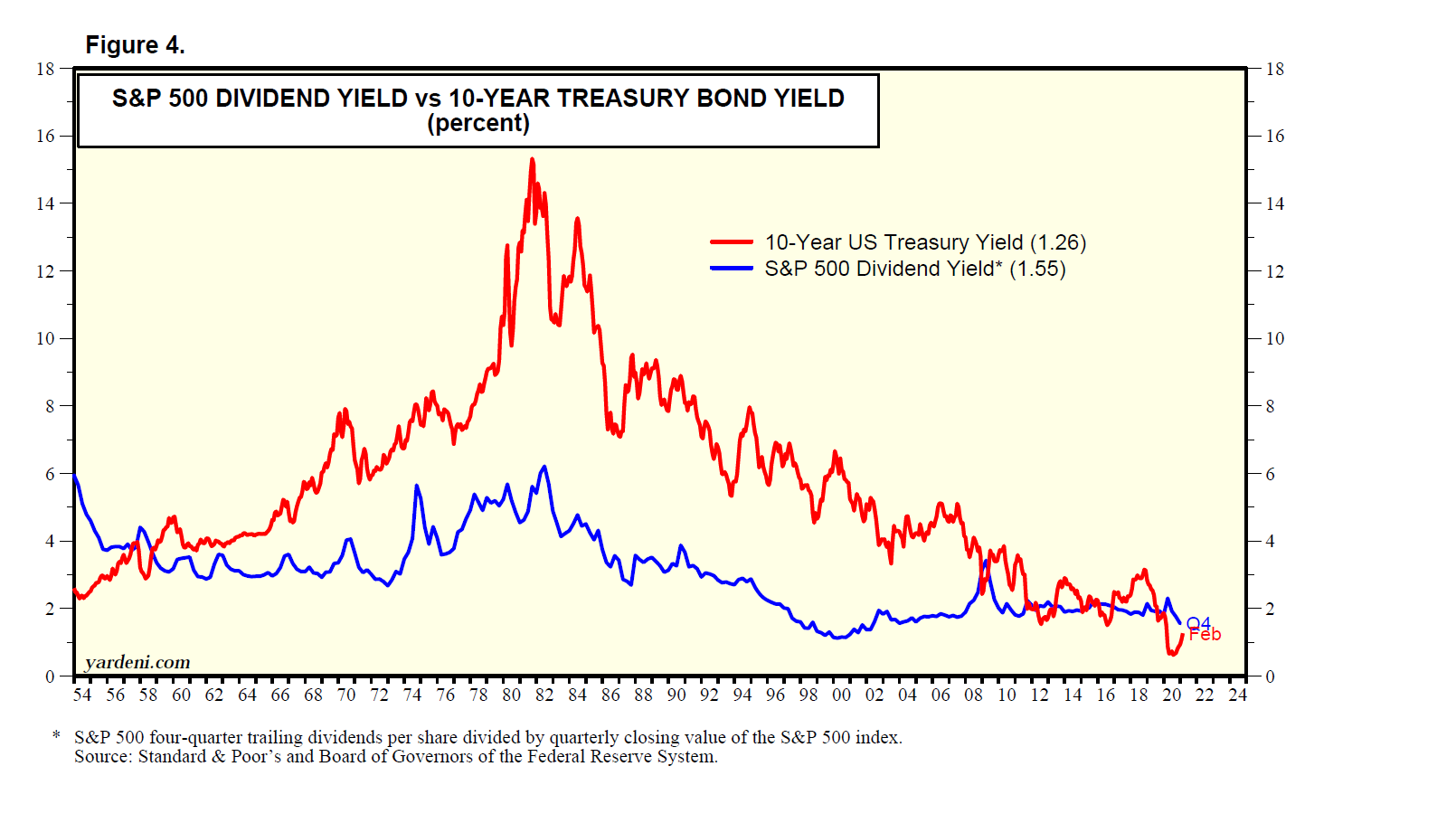

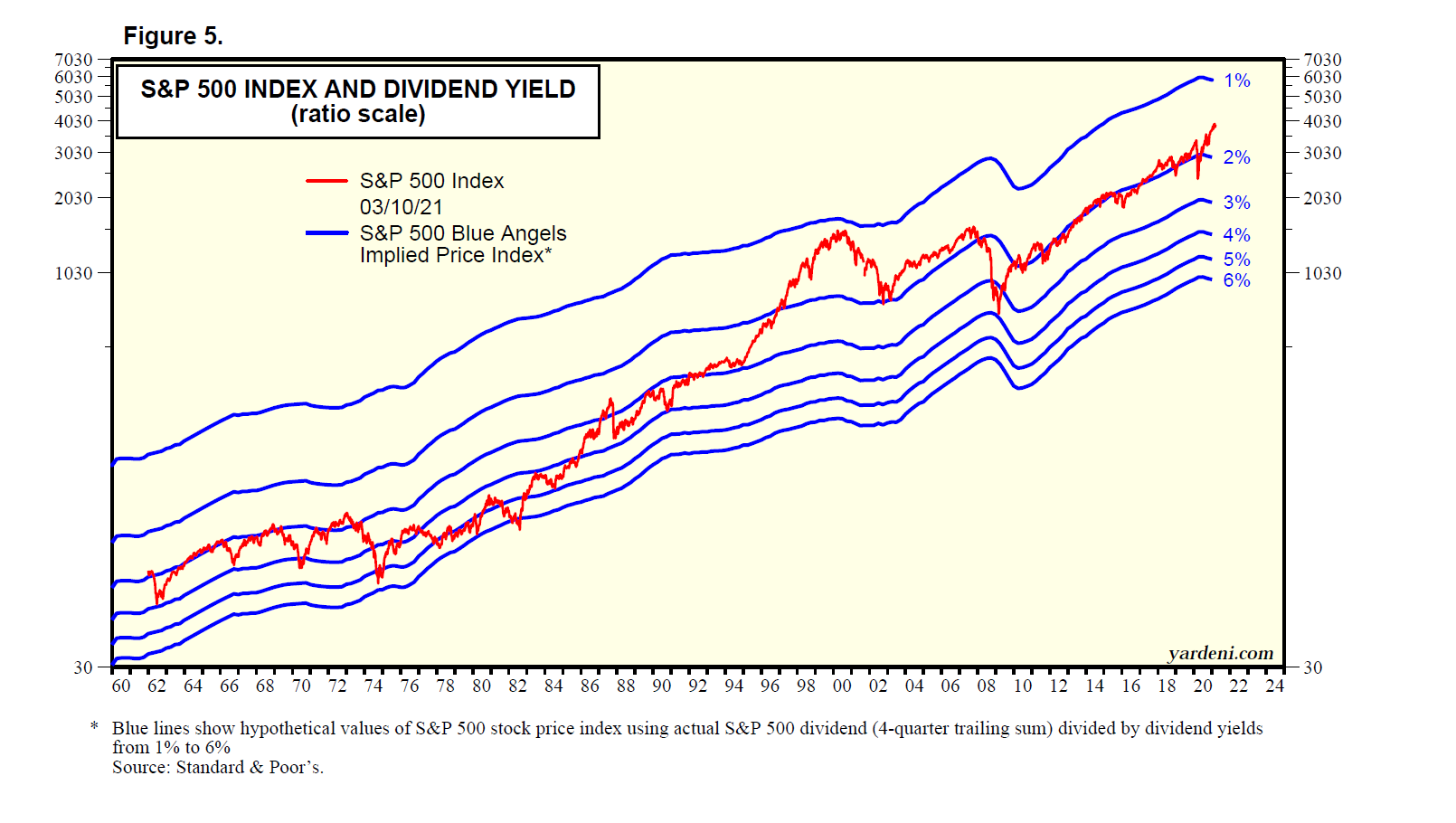

(3) Households own lots of stock. Equities represented 24% of household assets at the end of Q3, topping the last peak hit in Q4-2000, reported a December 13 Money article citing Wells Fargo data. That amount of exposure to stocks may suggest that individuals are acting rationally this time, unlike during 2000’s tech bubble frenzy. The S&P 500 dividend yield is 1.38%, almost as much as the 10-year Treasury bond yield of 1.47%, and stocks are one of the few assets considered to be a hedge against inflation (Fig. 2).

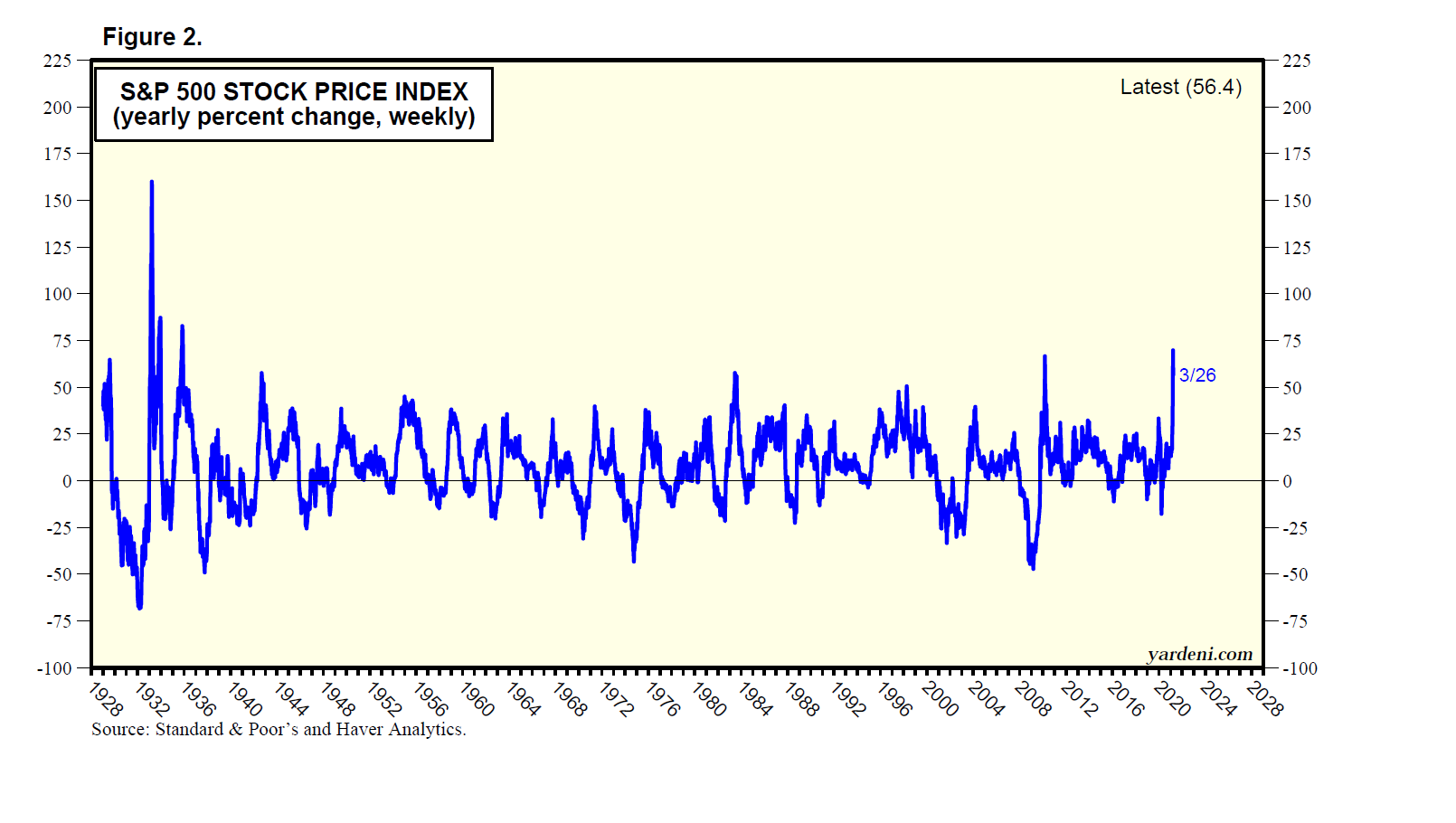

(4) The Fed is on the move. The Federal Reserve has done a good job preparing the market for higher interest rates. Even after it accelerated the end of its asset purchases and implied that there could be three interest rate hikes next year, the stock market managed to rally yesterday. There have been instances historically when stocks have rallied during parts of Fed tightening cycles. The S&P 500 rallied throughout 2016, when the Fed began a tightening phase that started on December 16, 2015 and lasted until August 1, 2019. The S&P 500 climbed 43.8% from December 16, 2015 through July 31, 2019 (Fig. 3).

Strategy II: What Could Go Right in 2022? Looking ahead, there seems to be plenty of room for the economy to continue to reopen, though different industries and sectors may benefit in 2022 than did so this year. Many employees still need to return to offices, where they’ll buy lunches and go out for happy hour. Business travel and trade shows have just started to resume. And the number of weddings this spring and summer is expected to surge.

Now let’s lay out some of the reasons why the stock market’s rally should continue:

(1) Covid is under control. We are in a much better position regarding Covid than we were even a few months ago. The Centers for Disease Prevention and Control (CDC) finds that 72.2% of all Americans have at least one Covid vaccine dose, 61.0% are fully vaccinated, and 27.2% have booster shots. But the situation is even better than those figures imply in the sense that “all Americans” includes children under five, who can’t receive a vaccination. Among Americans 18 or older, 84.5% have had at least one vaccine dose. Even more importantly, among those considered most at risk—folks who are 65 years or older—95.0% have had one dose, 87.2% are fully vaccinated, and 51.9% have received booster shots.

That said, Covid cases have risen as we’ve headed indoors for the winter. The seven-day average was 117,890 as of December 13, up from a low of 64,152 in October but less than half of January’s case load. Those who are vaccinated appear to be getting mild cases and staying out of the hospital.

The CDC tracked 43 cases of Covid-19 attributed to the Omicron variant in a December 10 report. The bad news is that 34 of the cases (79%) occurred in people who were vaccinated, and 14 of those infected (33%) had received an additional or booster dose. The good news is that only one patient was hospitalized, for two days, and no deaths were reported. The most common symptoms were cough, fatigue, and congestion or runny nose. More data is certainly needed to draw conclusions about vaccination efficacy against the variant; but so far, so good.

In the same vein, Pfizer reported that laboratory studies suggest that its anti-Covid pill should work against the Omicron variant. In studies before the emergence of Omicron, hospitalization and deaths were reduced by nearly 90% in patients who took the Pfizer pill within three to five days of the onset of symptoms.

(2) Still pockets of opportunity. The S&P 500 has had a great year, with every sector up by percentages in the double digits. Here’s the S&P 500 and its sectors’ ytd performance derby through Tuesday’s close: Energy (45.8%), Real Estate (34.6), Financials (31.4), Information Technology (29.6), S&P 500 (23.4), Materials (20.4), Consumer Discretionary (20.2), Health Care (18.7), Communication Services (18.5), Industrials (16.2), Consumer Staples (12.0), and Utilities (10.1) (Fig. 4).

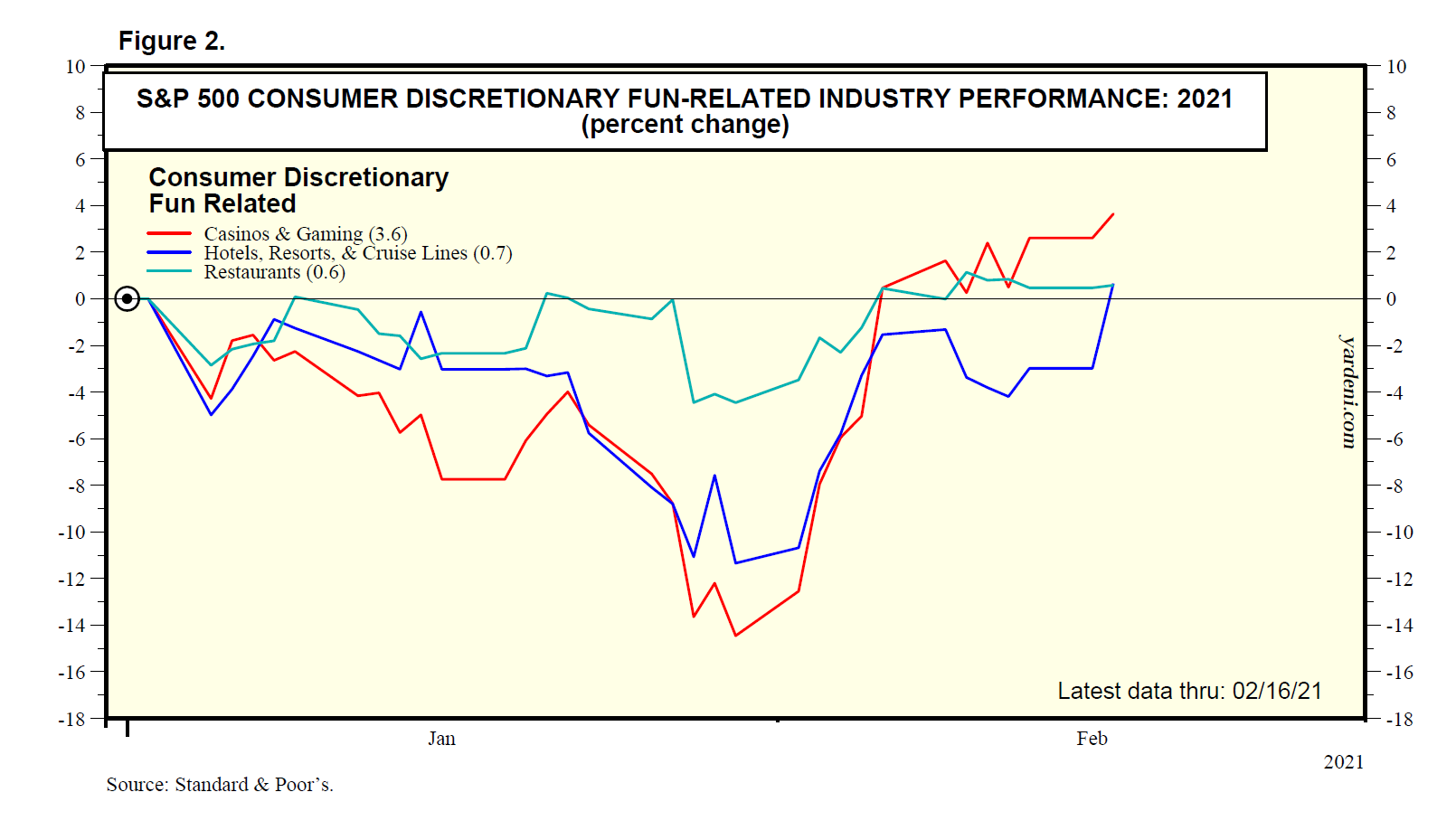

Where could there possibly be room for improvement? Traveling, particularly among the business set, hasn’t entirely rebounded yet with Covid still circulating, and many travel-related stocks have not recovered, as shown by the ytd performances of these S&P 500 travel-related industry price indexes: Casino & Gaming (-17.5%), Airlines (-7.6), and Hotels Resorts & Cruise Lines (8.3).

American Airlines plans to hire 18,000 workers in 2022 after hiring about 16,000 employees this year to bring its workforce up to about 130,000 currently, a December 14 CNBC article reported. Southwest plans to hire more than 8,000 employees in addition to the 5,000 hired this year.

The S&P 500 Restaurant index gained 17.9% ytd, but if restaurant companies can manage wage and goods inflation, their businesses should keep improving over the next year.

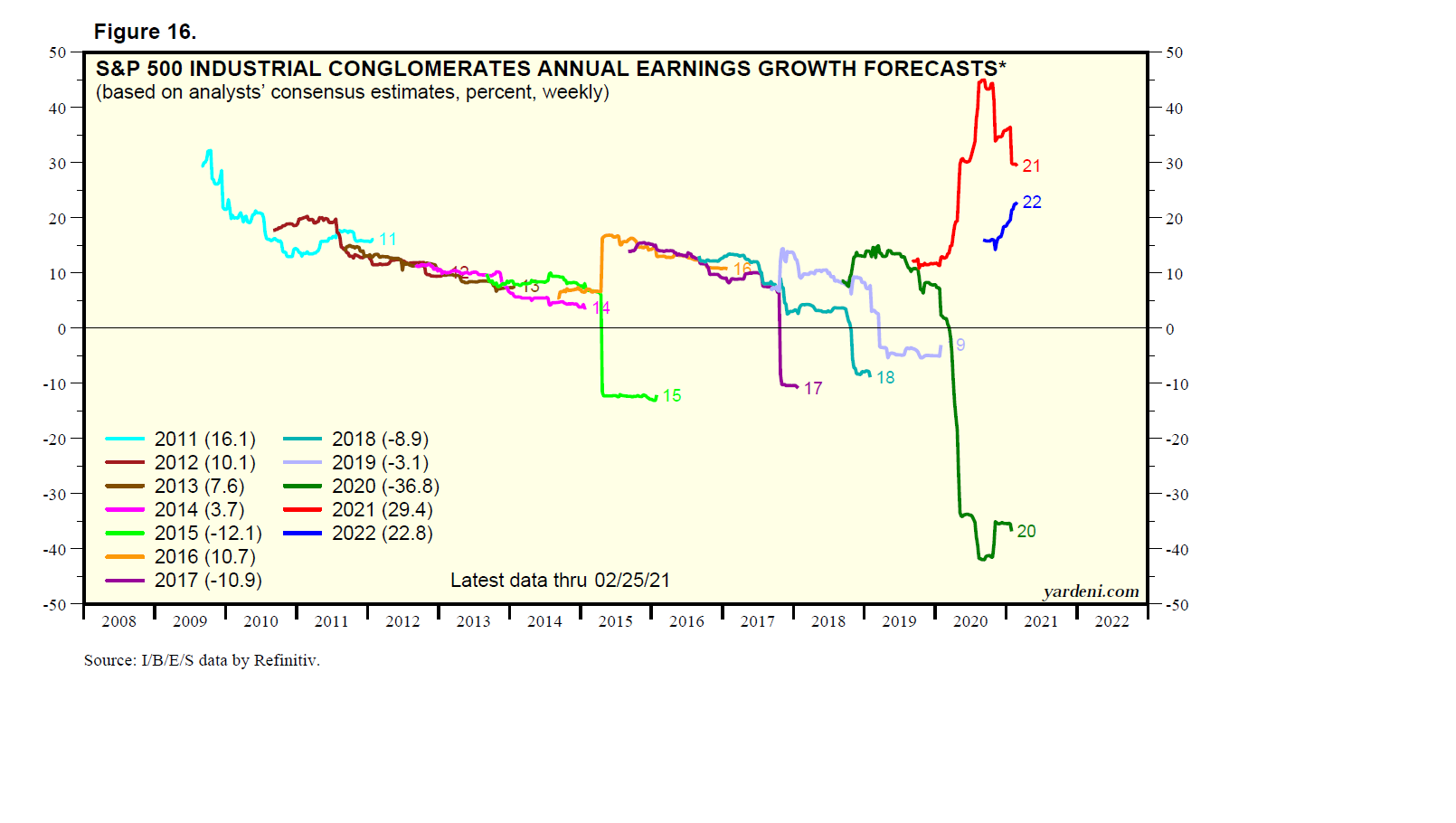

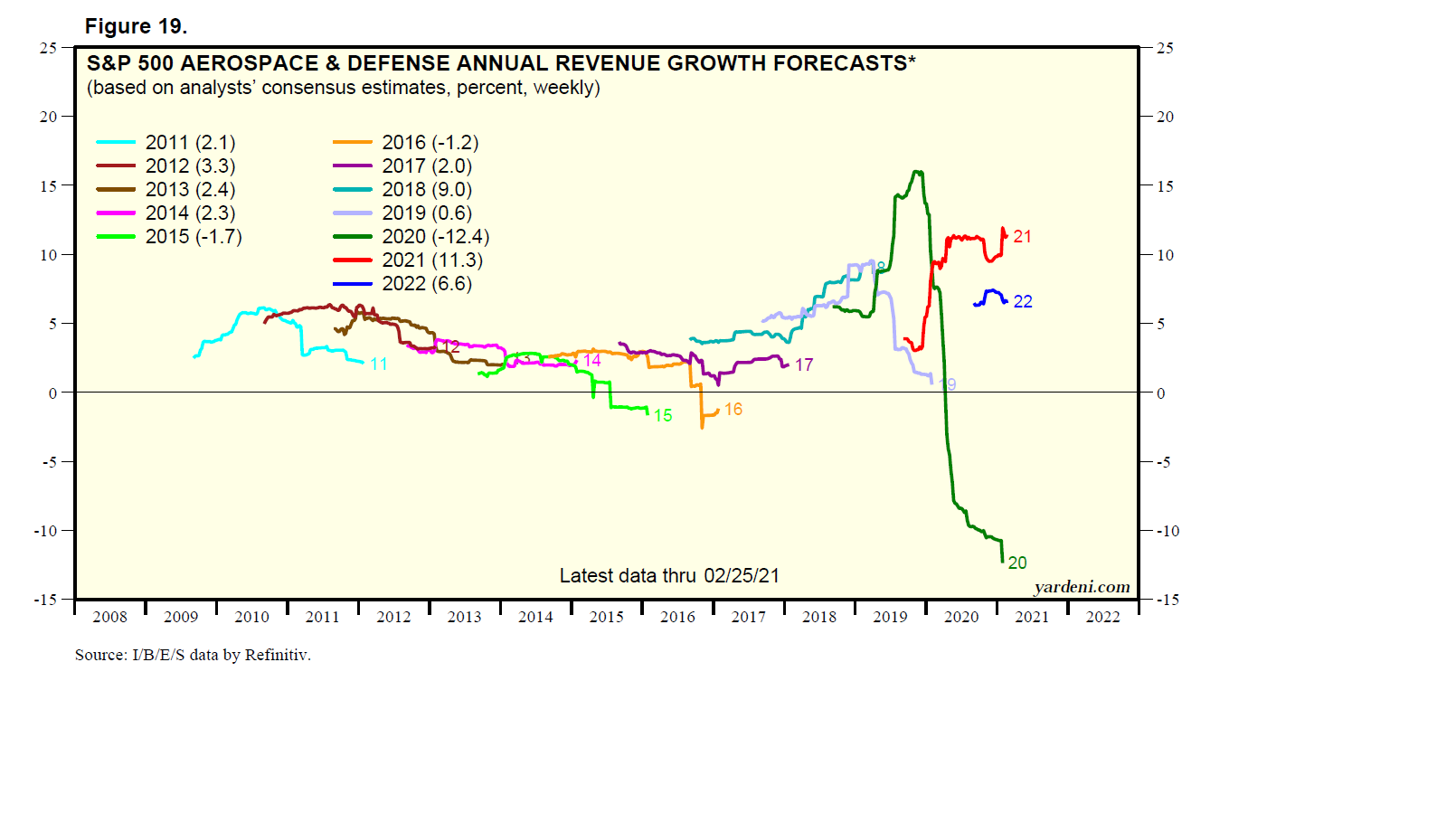

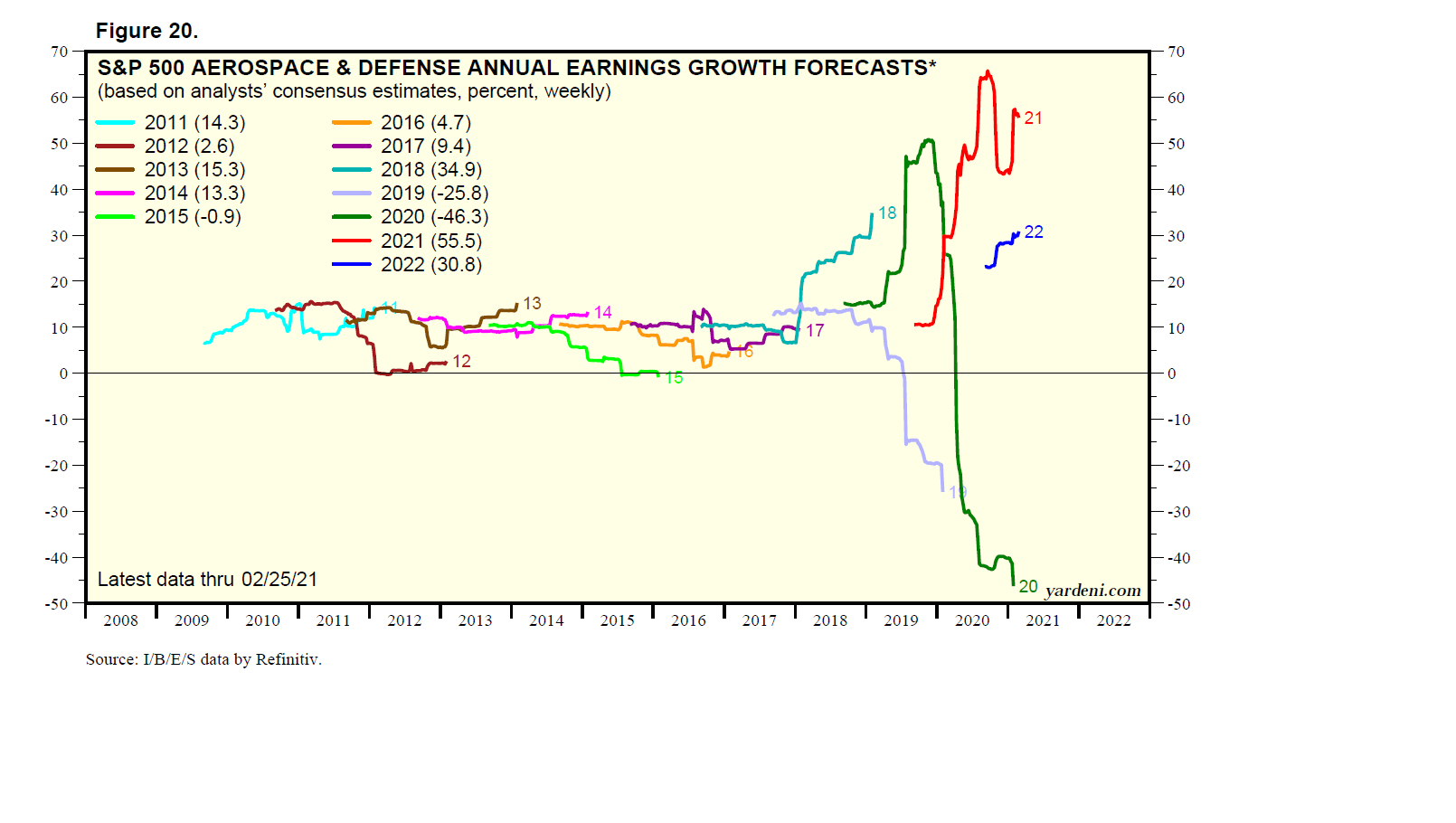

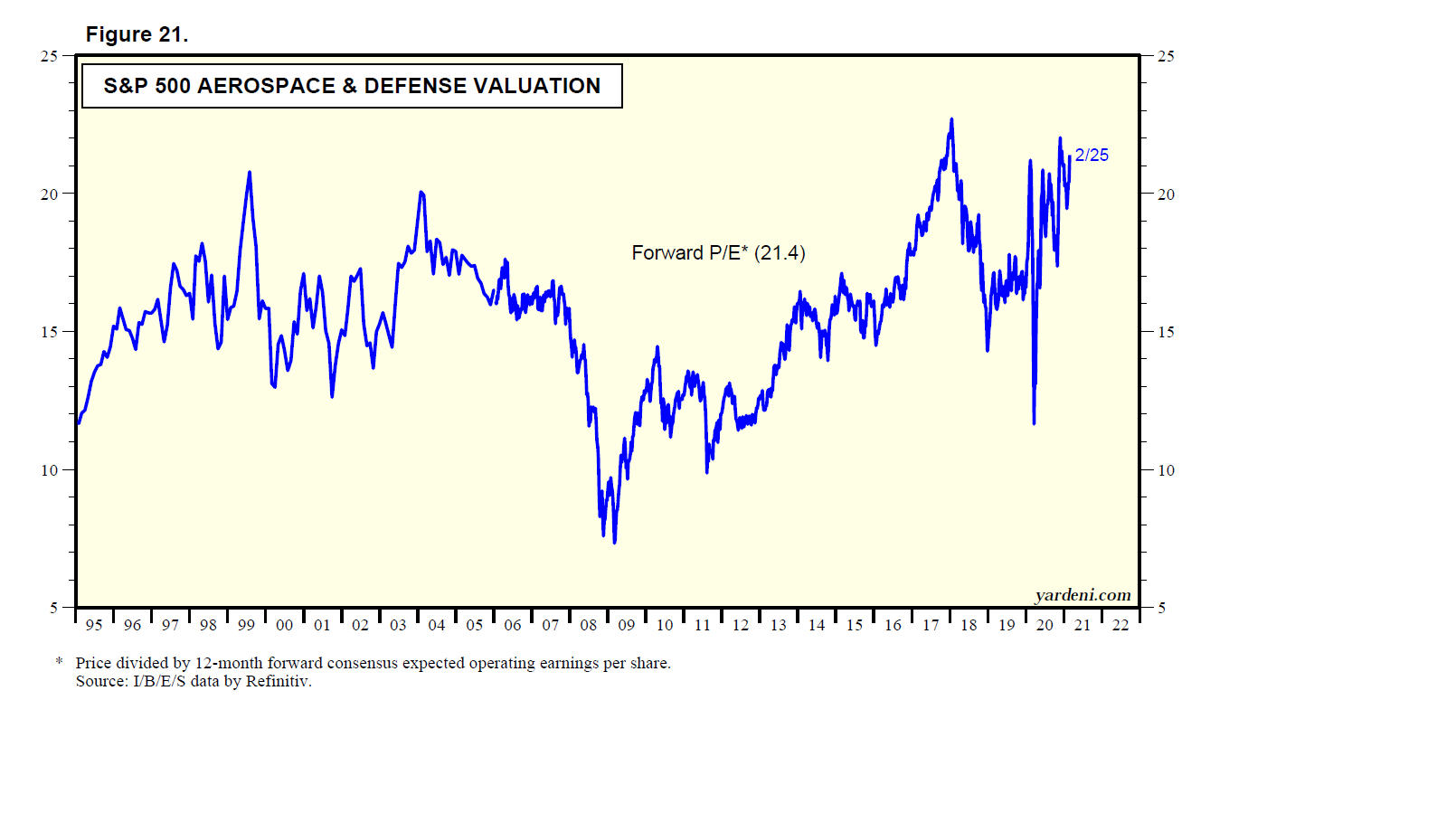

(3) Will Boeing finally revive? The S&P 500 Aerospace and Defense industry stock price index gained only 8.0% ytd, dragged down by Boeing’s 8.7% decline (Fig. 5). The company has started to fly straight again after a terrible few years when plane crashes weighed on its operations.

Boeing delivered roughly 302 planes this year, almost twice the 157 it delivered in 2020 but still below the 380 delivered in 2019. Deliveries of its giant 787 Dreamliner are still suspended due to manufacturing flaws. And while the 737 Max has returned to the air in the US and most other countries, it remains grounded in China.

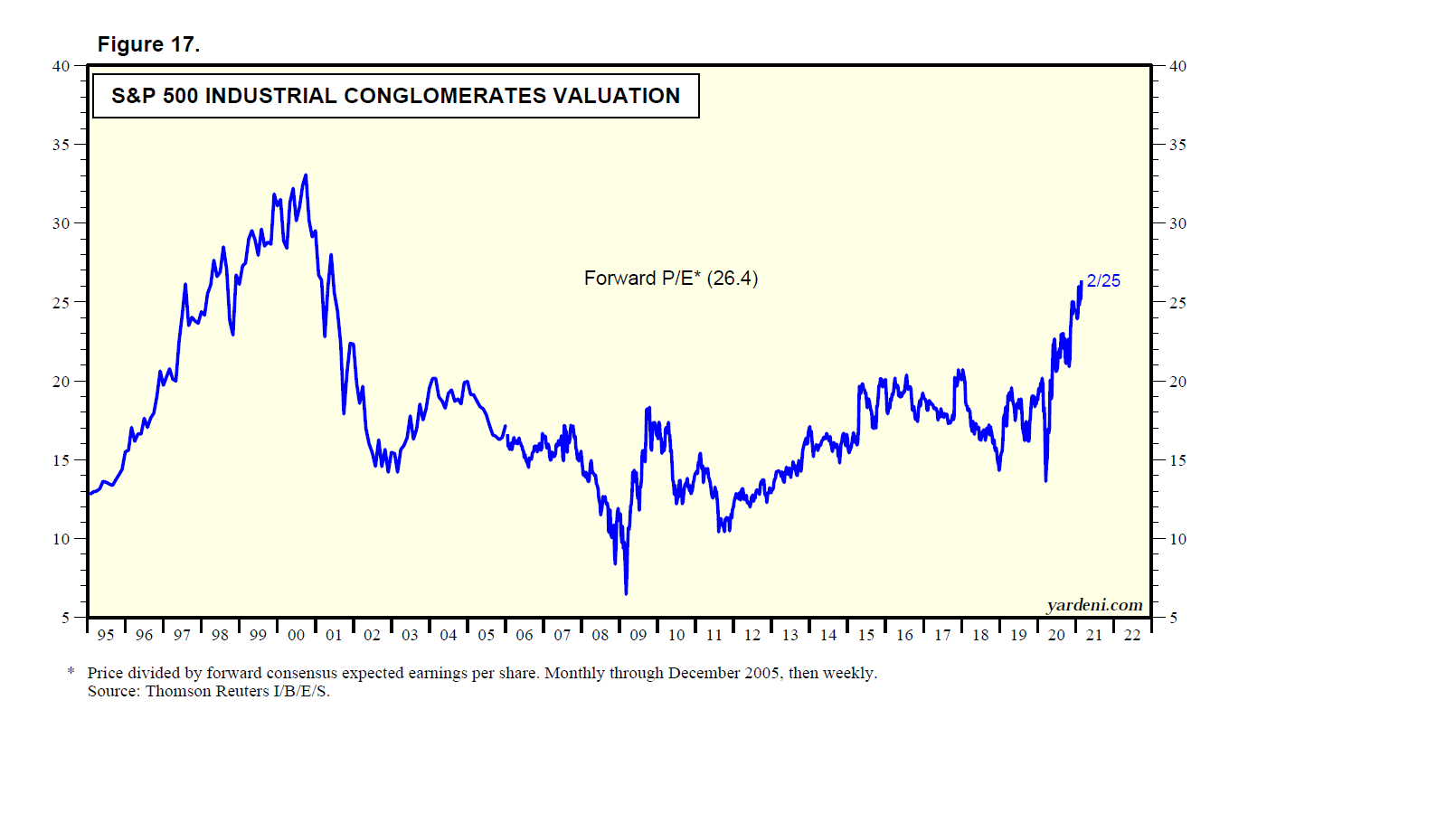

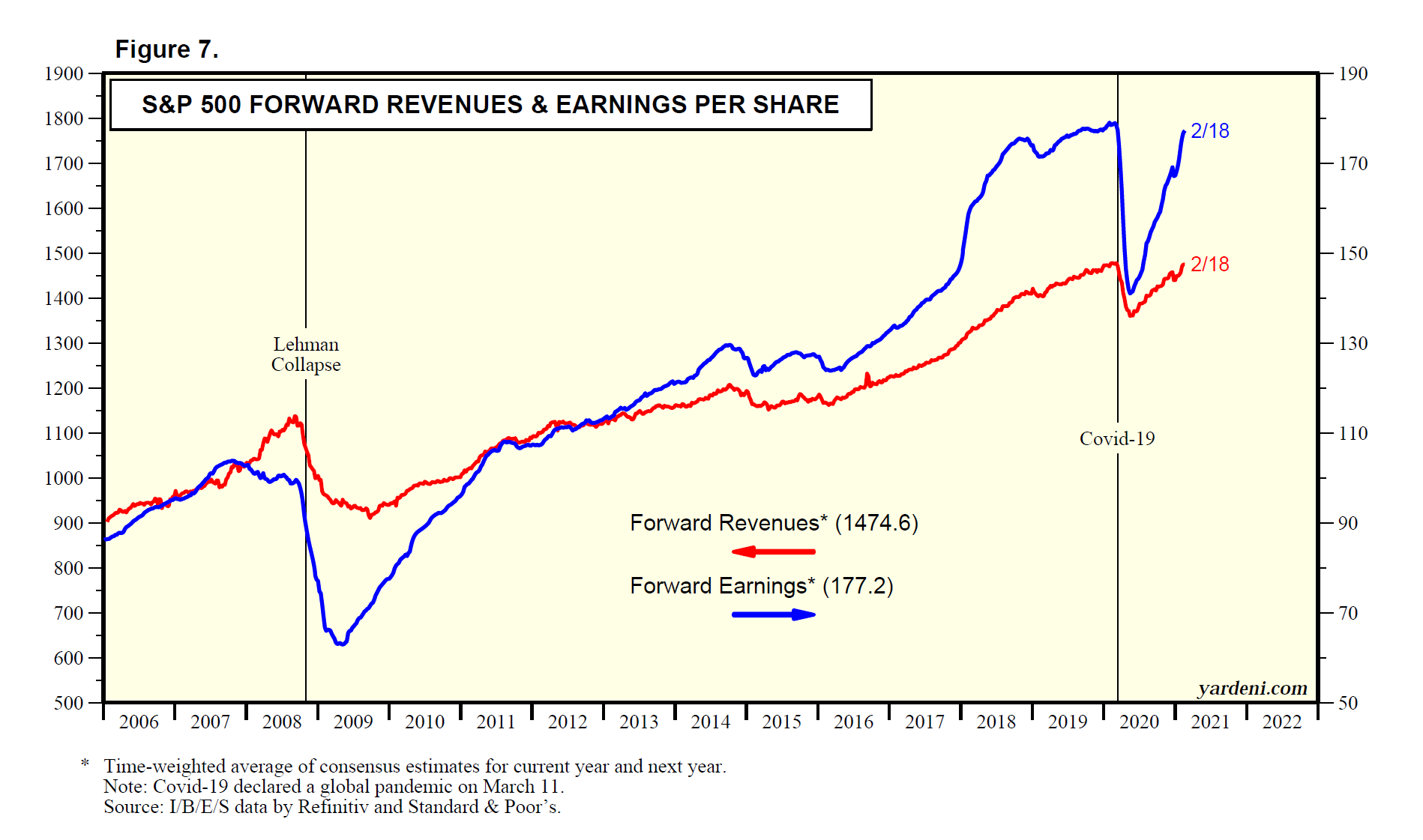

Wall Street analysts see the company’s earnings moving from a loss this year to $4.59 a share in 2022 and $7.67 in 2023. As for the entire industry, analysts are calling for revenue growth of 10.7% and earnings growth of 30.3% in 2022 (Fig. 6 and Fig. 7). And the industry’s forward P/E, which topped out at 22.3 in early June, has fallen to 17.3 (Fig. 8). (The forward P/E is the multiple based on forward earnings, or the time-weighted average of analysts’ consensus earnings estimates for this year and next.)

(4) 2022: The year of the wedding. Covid-19 meant putting event plans on hold, and weddings were no exception. The number of weddings fell from 2.1 million in 2019 to 1.3 million in 2020 before climbing to 1.9 million this year. But get ready to party next year, when pent-up demand is expected to push the count to 2.5 million, the most since 1984, according to The Wedding Report.

This wedding bubble is good news for catering venues, florists, limo rental companies, wedding planners, jewelry stores, and, of course, dress makers. It might even help out companies that provide wedding registries, like Tiffany, Macy’s, Amazon, Target, Bed Bath & Beyond, Crate & Barrel, Pottery Barn, and others listed in this October 26 Brides’ registry ranking.

As large events like weddings and trade shows resume, we are going to need new clothes. Yet the S&P 500 Apparel Retail industry’s stock price index has risen only 8.1% ytd, while the S&P 500 Apparel, Accessories & Luxury Goods index has climbed even less, 4.8% ytd.

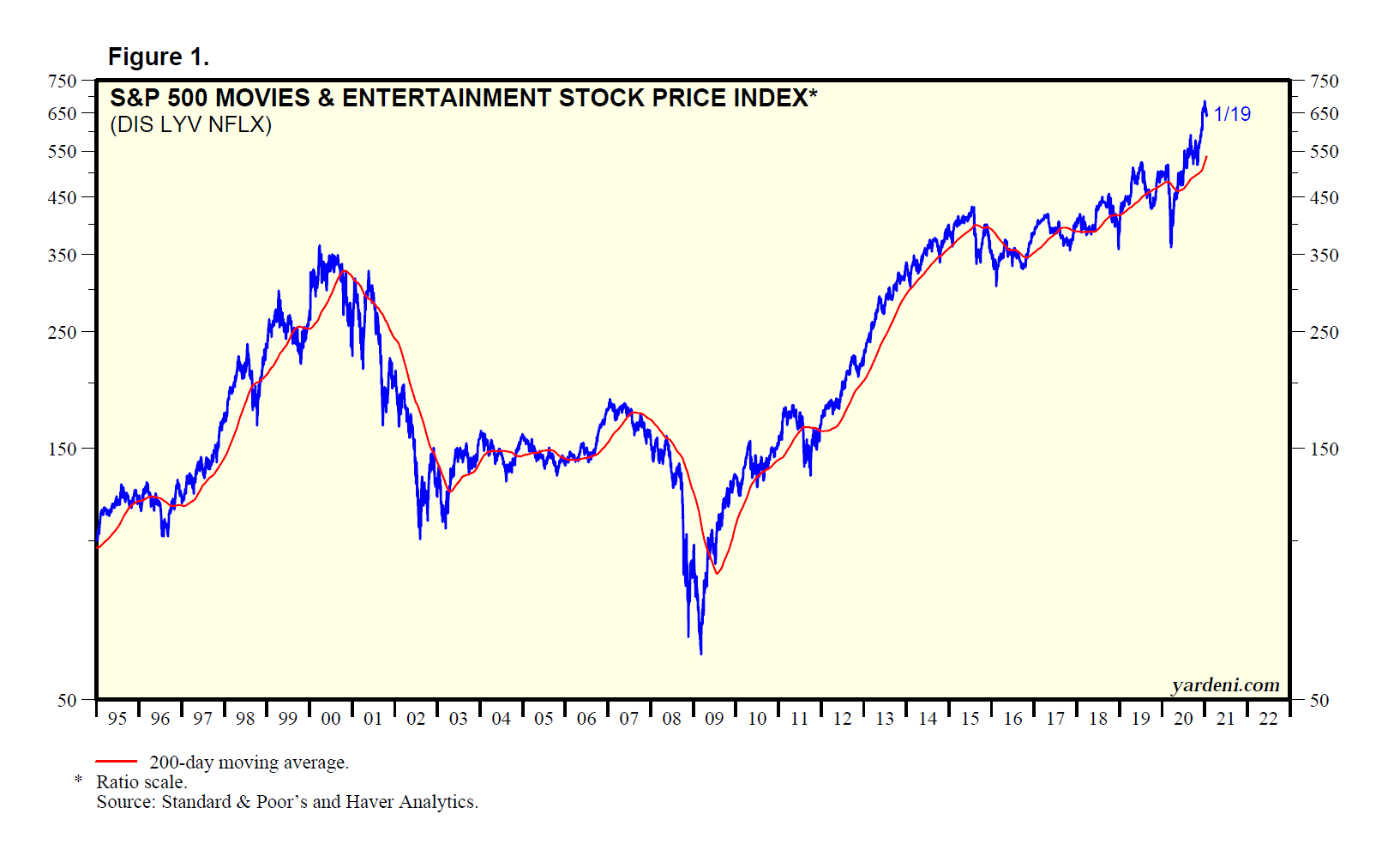

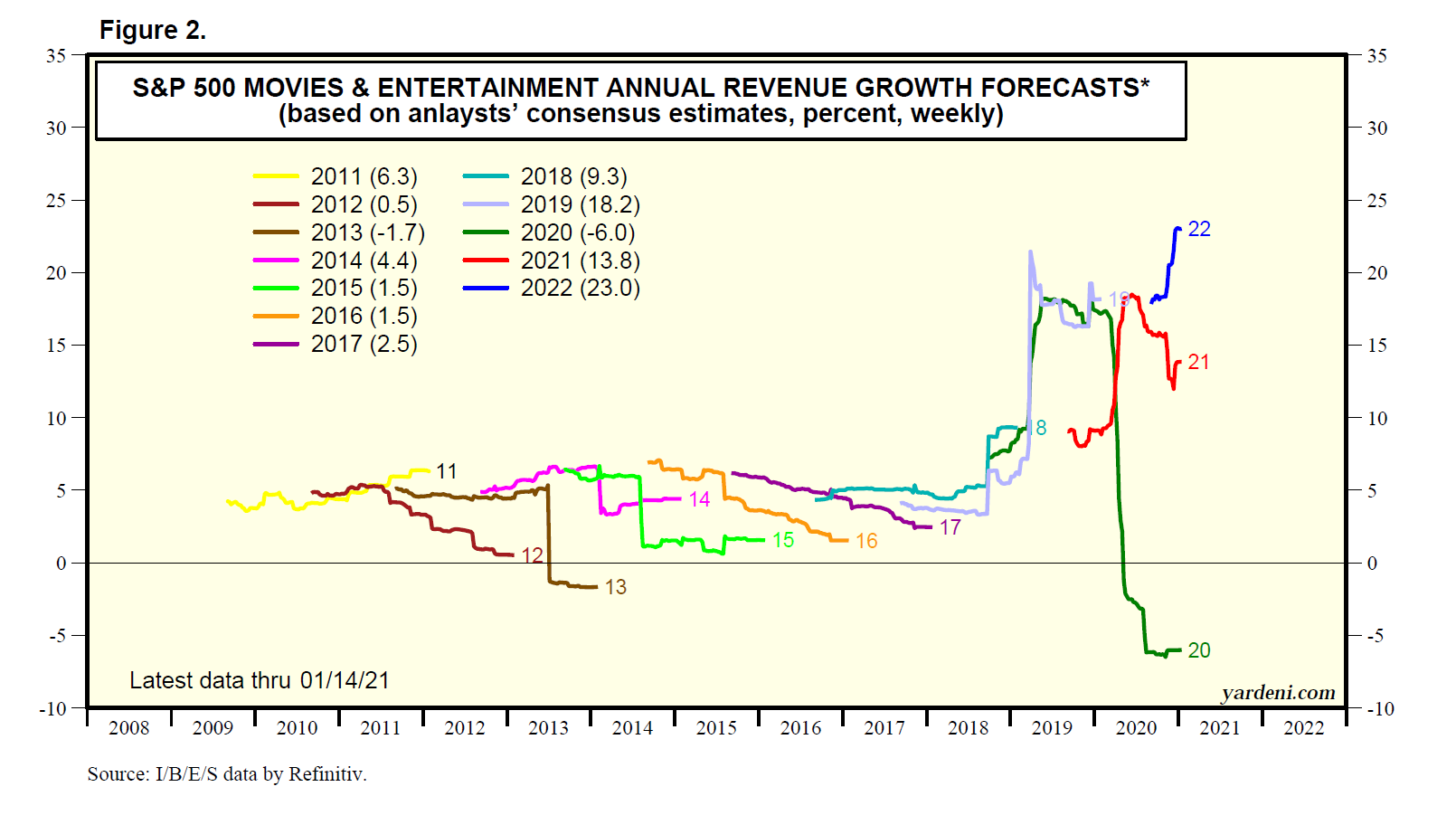

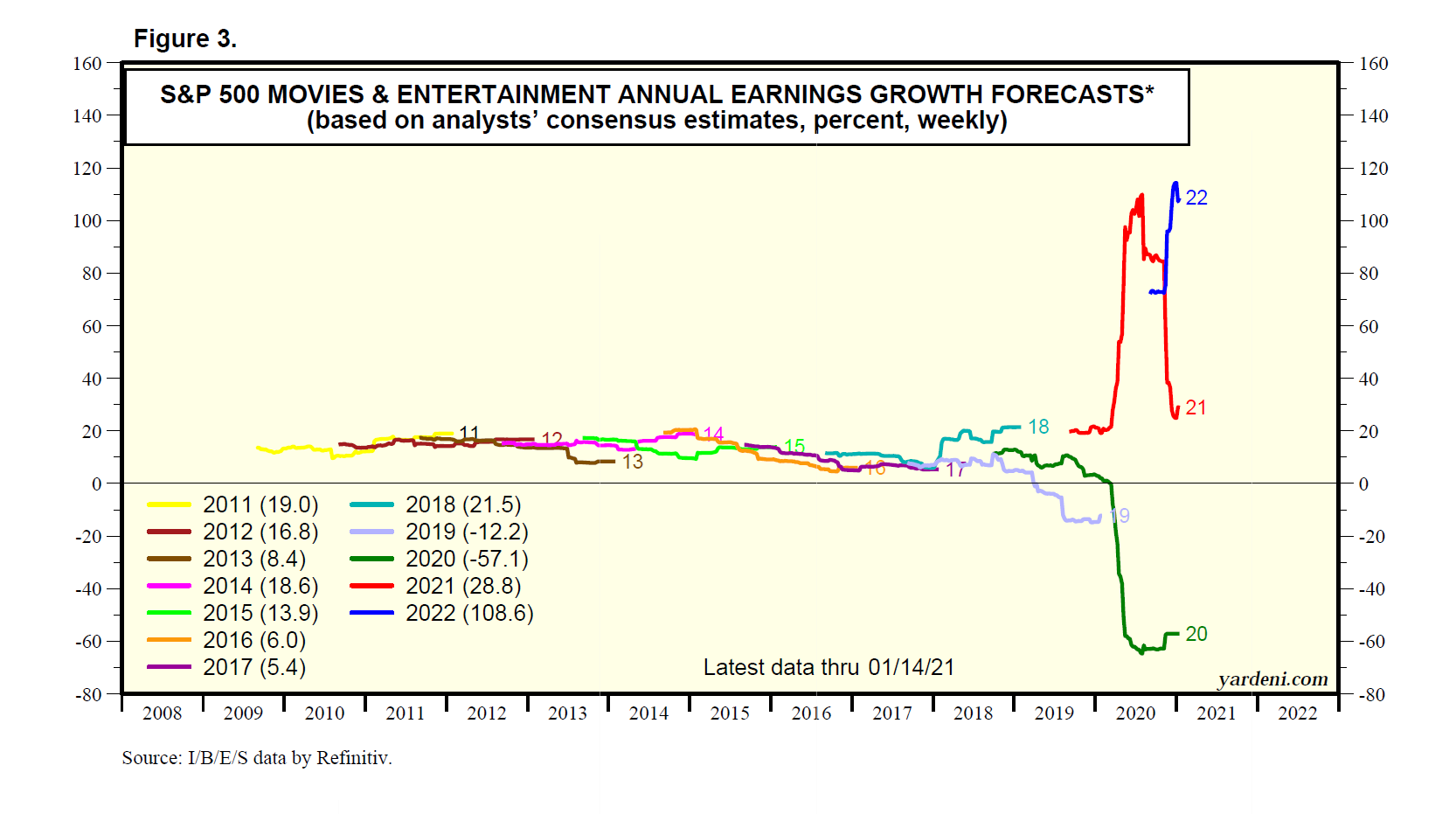

We’d also expect the masses to see a movie or two and throw back a pint or more next year. Yet this year, the associated industries have been decidedly out of favor: The S&P 500 Movies & Entertainment stock price index is down 4.9% ytd, and Brewers is up only 1.5%.

(5) Another good year for energy? The rise of Omicron could slow the recovery in oil demand; but with broad economic shutdowns not expected, further improvement in the demand picture should continue.

“The impact of the new Omicron variant is expected to be mild and short-lived, as the world becomes better equipped to manage COVID-19 and its related challenges. This is in addition to a steady economic outlook in both the advanced and emerging economies,” OPEC said in a recent report, according to a December 14 Oilprice.com article. OPEC kept its demand growth forecasts for 2021 and 2022 unchanged.

World crude oil production remains 8.4% below year-end 2019 levels (Fig. 9). And US inventories are far below 2019 and 2020 levels (Fig. 10).

Meanwhile, US supply remains below pre-pandemic levels. “For the U.S. to bring supply back up to levels that we saw pre-pandemic, it’s going to take to July of 2023. So I think there’s going to continue to be upward pressure on the price of oil,” Nancy Tengler, CEO of Laffer Tengler Investments, told CNBC on December 9.

Disruptive Technologies: Autonomous Trucks Arrive. In the upcoming year, it looks like autonomous trucking may roll into the mainstream. Walmart is testing autonomous trucks using Gatik software, UPS is testing autonomous truck routes in Texas, and TuSimple’s autonomous trucks are cruising across the southern US states. Progress in autonomous trucking may even be passing progress in autonomous passenger vehicles, in part because trucks often drive predictable routes and can avoid the tricky situations cars may encounter.

Venture capitalists are watching. “In the year through Dec. 6, total investment activity for self-driving logistics vehicles leapt fivefold to $6.5 billion from $1.3 billion in the same period in 2020, according to startup data platform PitchBook. Investment activity for robotaxi firms, meanwhile, fell 22% to $8.4 billion from $10.8 billion over the same period,” a December 9 Reuters article reports.

Here's Jackie’s look at some of the autonomous truckers hitting the road:

(1) Walmart tests last-mile autonomy. Walmart announced last month that it has been using two autonomous box trucks on a seven-mile loop in Bentonville, Arkansas—without a safety driver behind the wheel since August. The trucks shuttle between a fulfillment center and a Walmart store.

The retailer is working with Gatik, a startup company that focuses on the business-to-business market and short-haul routes like transporting retail goods from warehouses to stores. Gatik’s autonomous trucks drive day and night as they’re being tested on dense urban roads with traffic lights and intersections, a November 8 press release stated. Unlike autonomous taxis, they generally are able to avoid left turns across oncoming traffic, blind turns, and any other complicated driving, as well as schools, hospitals, and fire stations.

Founded in 2017, Gatik has raised $114.5 million and is backed by Koch Disruptive Technologies, Innovation Endeavors, Wittington Ventures, and others, and it has partnered with Ryder, Goodyear, Isuzu, and others, the press release stated.

(2) UPS tests handsfree trucking. UPS plans to test Waymo’s Class 8 autonomous trucks for long-haul deliveries between Dallas-Fort Worth and Houston, but the truck will have humans behind the wheel. The two companies have been working together, with UPS testing Waymo’s self-driving minivans for local deliveries, a November 17 article in The Verge reported.

Waymo announced this summer that it’s working with JB Hunt Transport Services on hauling goods in a Class 8 autonomous truck for one of JB Hunt’s customers between Fort Worth and Houston. The trucks will be supervised by Waymo employees in the cab. Waymo is also working with Daimler, which plans to use Waymo’s autonomous technology in its heavy-duty Freightliner Cascadia semi-trailer trucks, a June 10 article in The Verge reported.

Waymo is perhaps best known for the trials of its autonomous taxis in the suburbs of Phoenix without a safety driver and in San Francisco with one. A December 8 Reuters article questioned whether the company was losing its lead over others with similar ambitions. Ford Motor’s Argo AI says it will partner with Lyft to run robotaxis in Miami before year-end with a safety driver present, and General Motors’ Cruise hopes to have permits next year for a middle-of-the-night driverless taxi offering.

(3) Texas welcomes autonomous trucks. Waymo isn’t alone in Texas. Embark Trucks, another autonomous trucking software developer, next year plans to haul freight in its autonomous trucks between Houston and San Antonio, a December 9 FreightWaves article reported. The trucks will have backup drivers in the cabs.

Embark is working with development program members Werner Enterprises, Mesilla Valley Transportation, and Bison Transport. The company, which didn’t say how many trucks were involved, went public through a merger with Northern Genesis Acquisition Corp. in a November deal that valued Embark at roughly $5 billion.

TuSimple also has autonomous trucks on the Texas roads. Its 50 trucks with safety drivers on board are driving across the southern US. The company plans to have a national network crossing US highways by 2024.

Behind the Inflation Curve

December 15 (Wednesday)

Check out the accompanying pdf and chart collection.

(1) Fed head provided a heads-up. (2) Powell has mutated from dovish to hawkish variant of Fed chair. (3) FOMC’s latest projections likely to show more rate hikes in 2022. (4) Fed scrambling to catch up with inflation curve. (5) Real interest rates are unreal. (6) Is the bond yield alarming or not? (7) Durable goods inflation should moderate next year. (8) Inflation is currently disconcerting. (9) Supply chains are still kinky. (10) Monitoring the supply chains. (11) Amazon shows the way.

Fed I: The Dot Plot Thickens. What will the FOMC decide at its meeting today? Fed Chair Jerome Powell gave us all a heads-up about the possibility of the Fed’s speeding up the tapering of its asset purchases back on Monday, November 30. That’s the day that, in congressional testimony, he mutated from the dovish variant to the hawkish variant of Powell.

Testifying before a Senate committee, the Fed chair said he thinks reducing the pace of monthly bond buys can move quicker than the $15 billion-a-month schedule announced earlier in November. “At this point, the economy is very strong and inflationary pressures are higher, and it is therefore appropriate in my view to consider wrapping up the taper of our asset purchases … perhaps a few months sooner,” Powell said. “I expect that we will discuss that at our upcoming meeting.”

The Fed was on course to wrap up its tapering by mid-2022. A few months sooner than that would be consistent with doubling the monthly pace of tapering to $30 billion, thus ending bond purchases by the end of March. Consider the following related issues:

(1) FOMC rate forecasts. The decision on the pace of tapering could be a surprise, but it probably won’t be. More surprising might be the FOMC’s Summary of Economic Projections (SEP). In March, June, September, and December of each year, the Federal Reserve Board members and regional bank presidents submit their economic projections for the current and next couple of years. These include their latest forecasts for the federal funds rate, which are plotted on a chart that has come to be known as the Fed’s “dot plot.”

Both June’s and September’s dot plots showed the Fed’s 18 anonymous dots all in a row, suggesting expectations near a zero percent rate for 2021. For 2022, June’s plot showed seven dots indicating the opinion that a rate rise would be appropriate. In September, two dots crept up, as nine dots showed expected rate increases in 2022. Many more dots undoubtedly will join those nine in today’s SEP. The only question is: How many will be projecting one, two, or even three 25-bps increases in the federal funds rate next year?

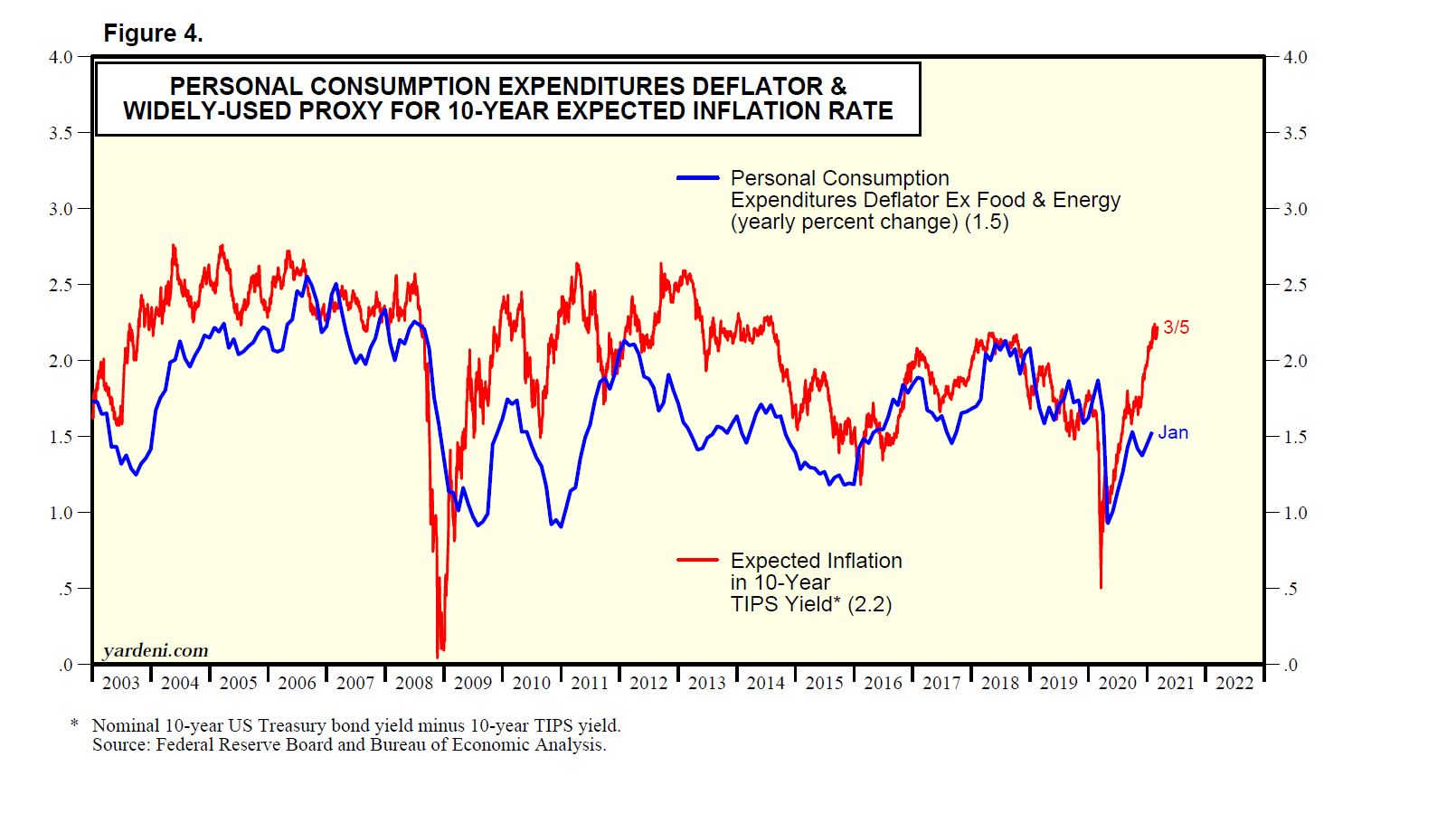

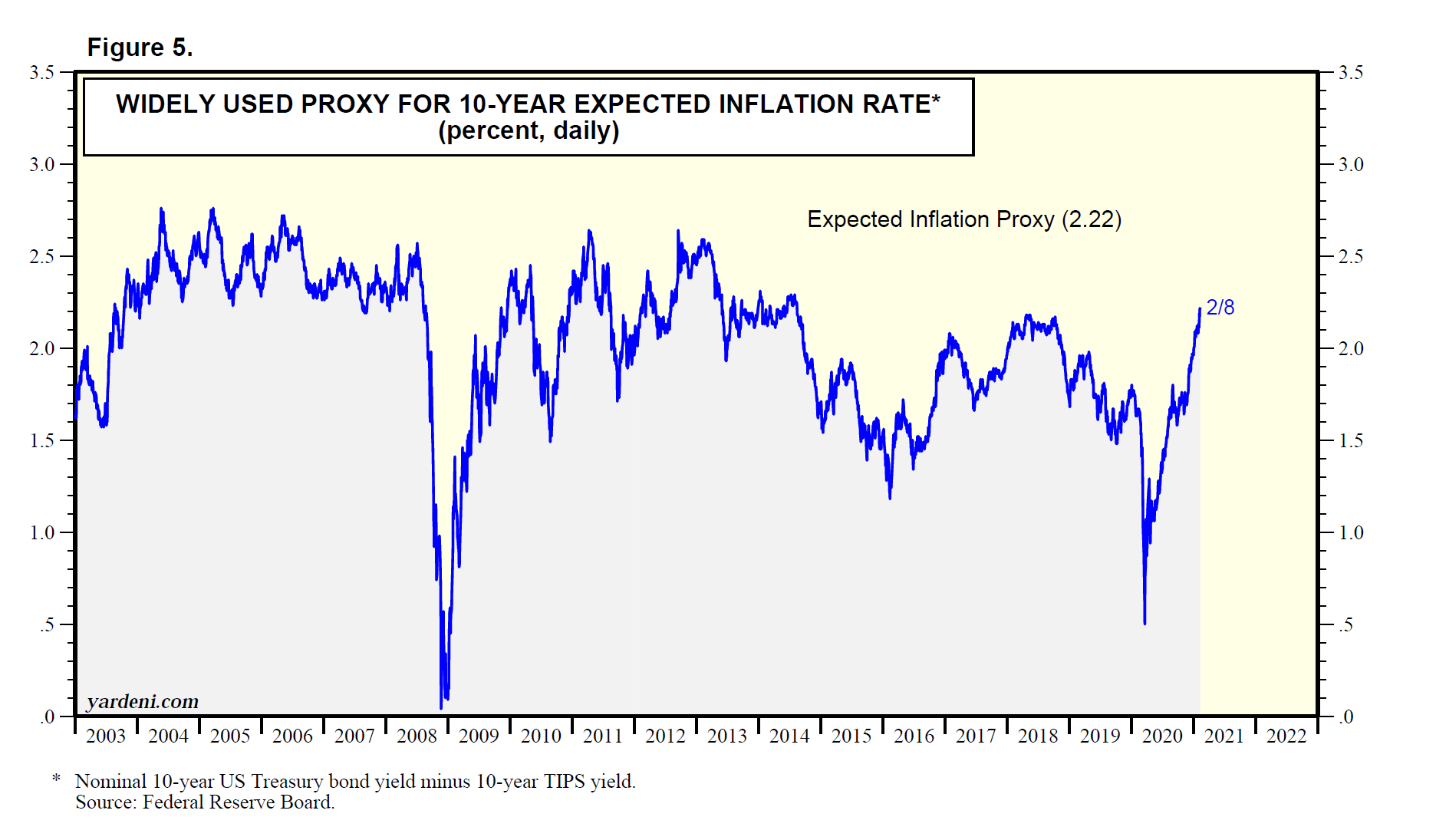

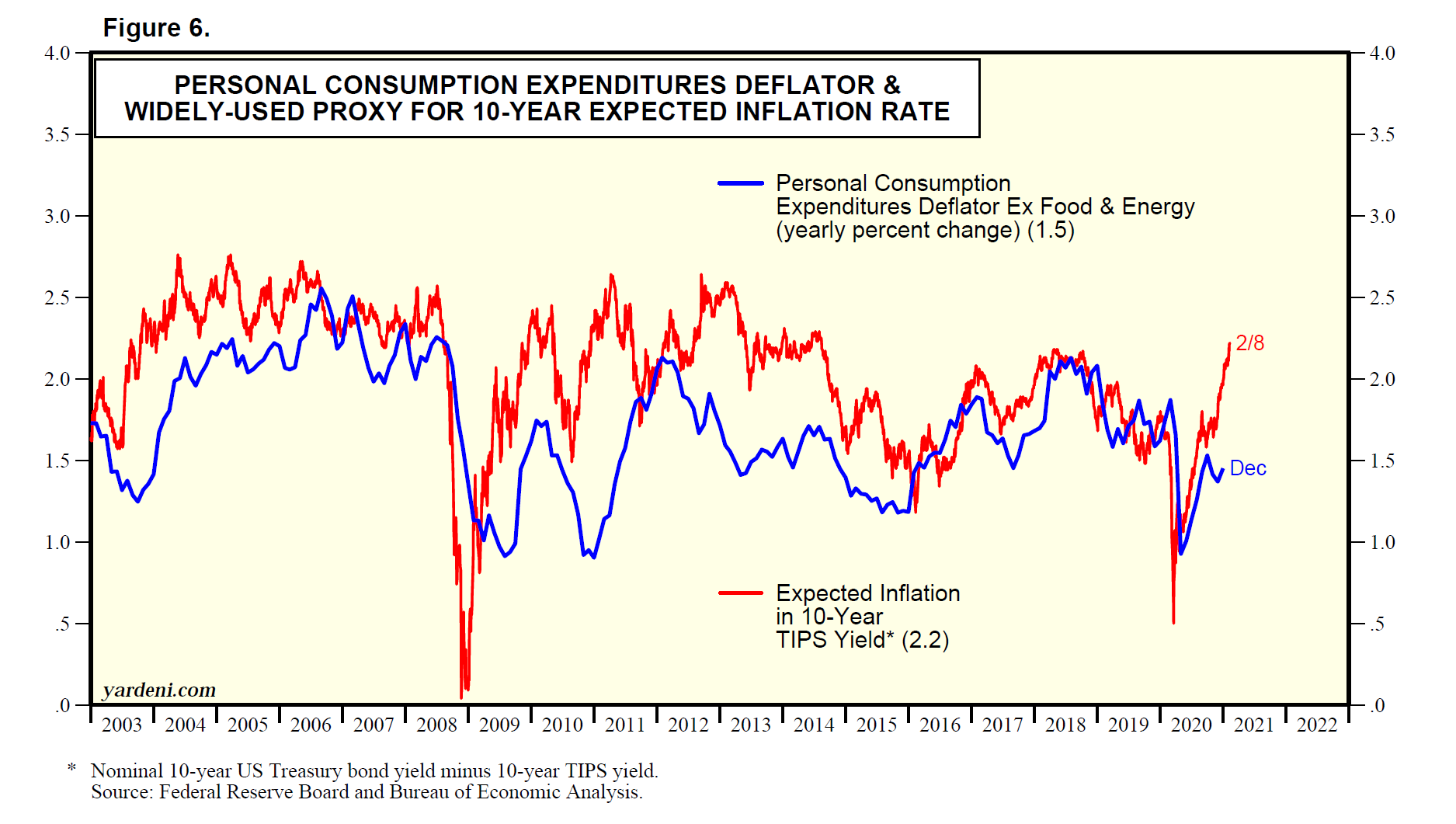

(2) FOMC inflation forecasts. Also interesting to see will be the FOMC’s consensus forecasts for the PCED inflation rate. For 2021, the committee projected 1.8% during the December 2020 meeting. This year, that projection rose to 2.4% at the March meeting, 3.4% in June, and 4.2% in September. The FOMC continued to project inflation around 2.2% during both 2022 and 2023. Odds are that it will raise both the 2021 and 2022 projections. (See our FOMC Economic Projections tables.)

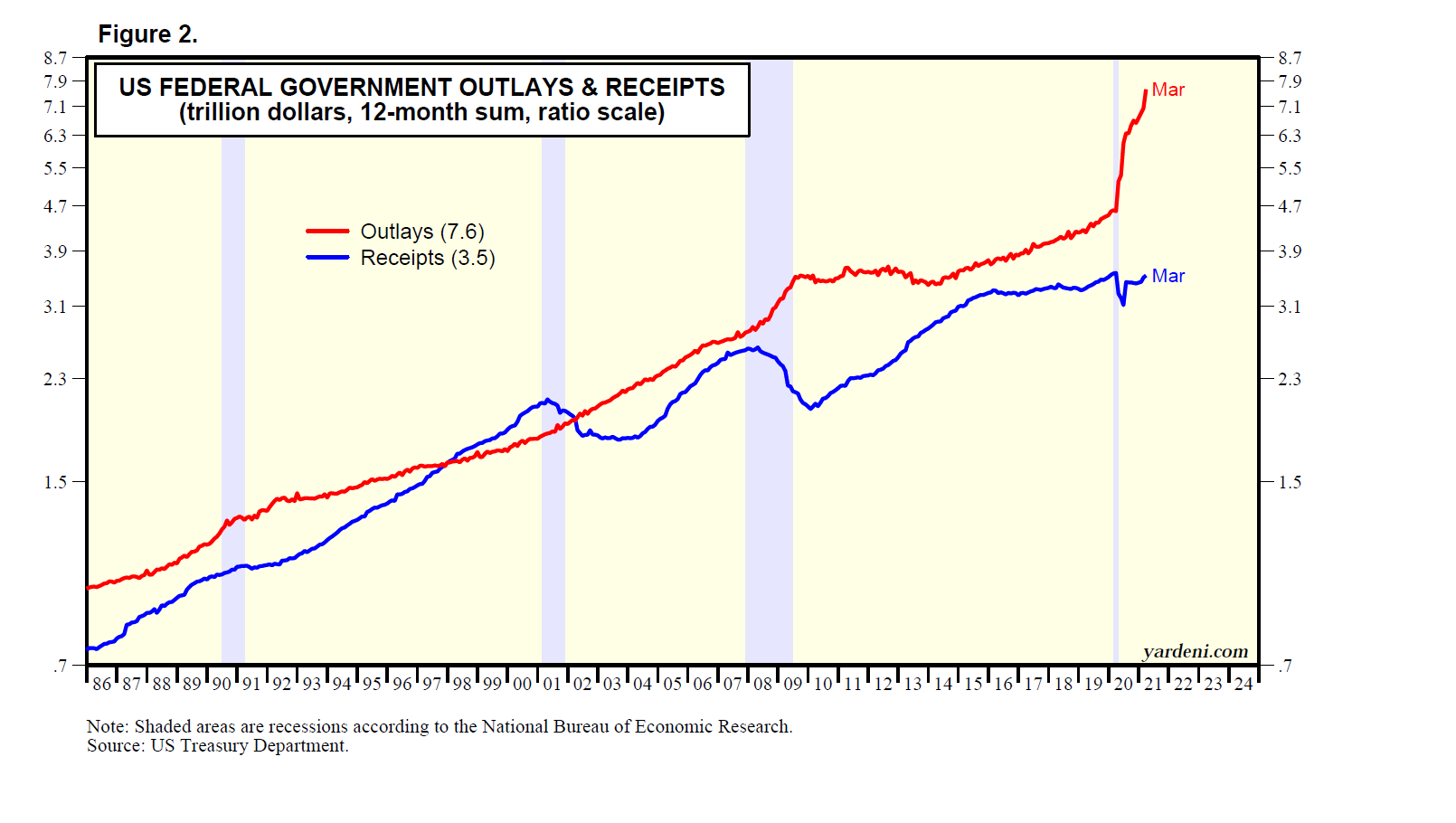

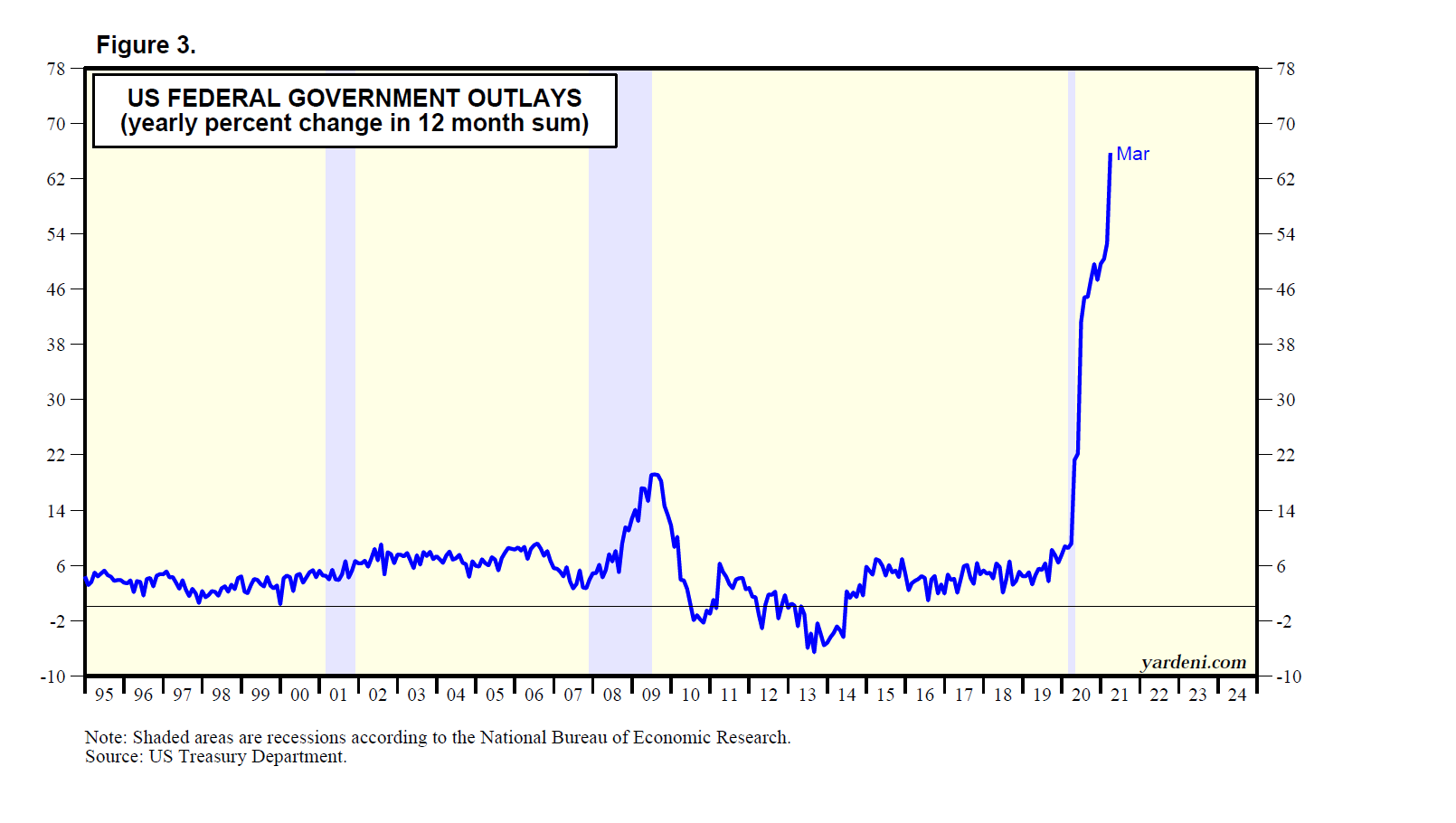

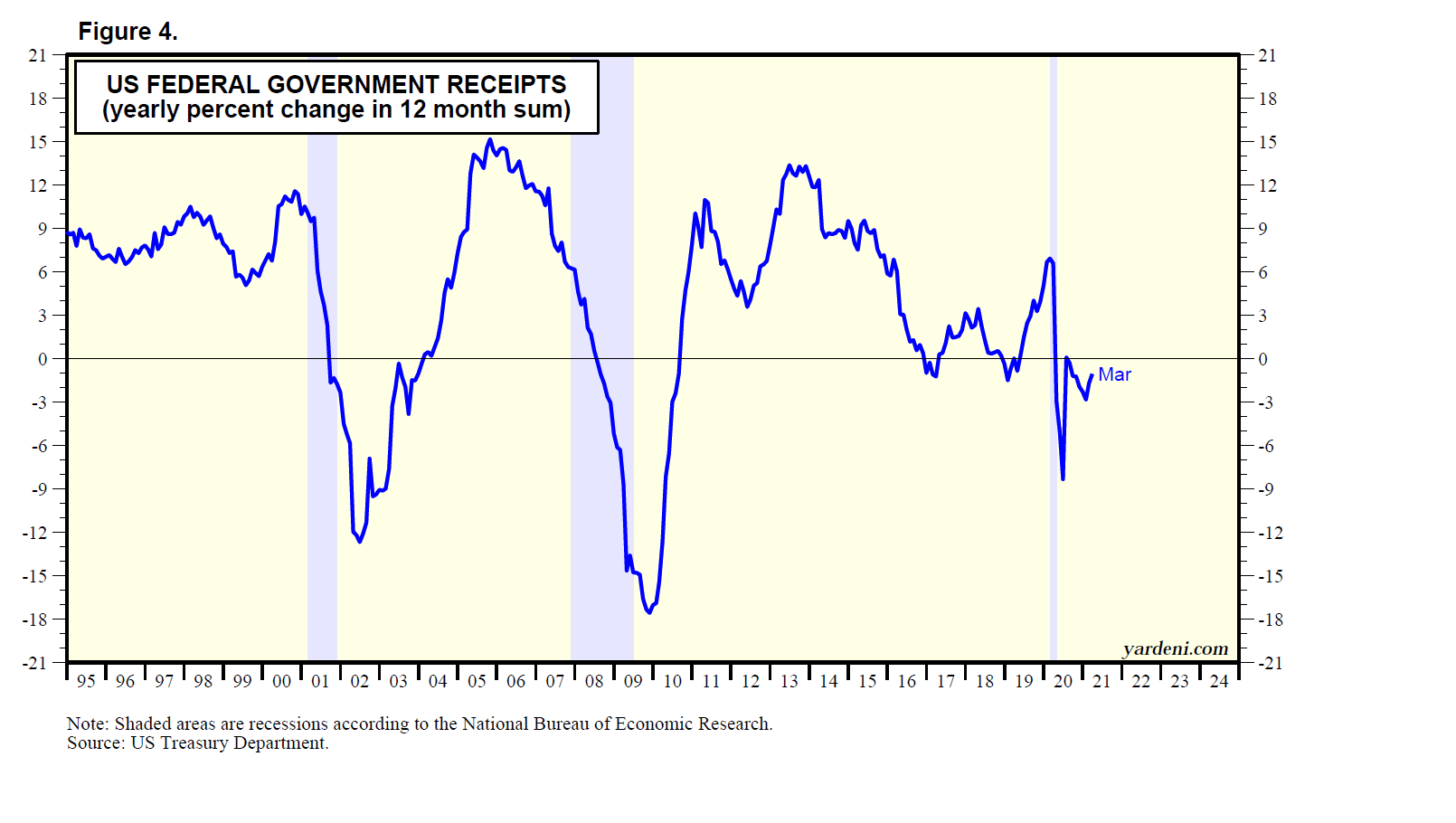

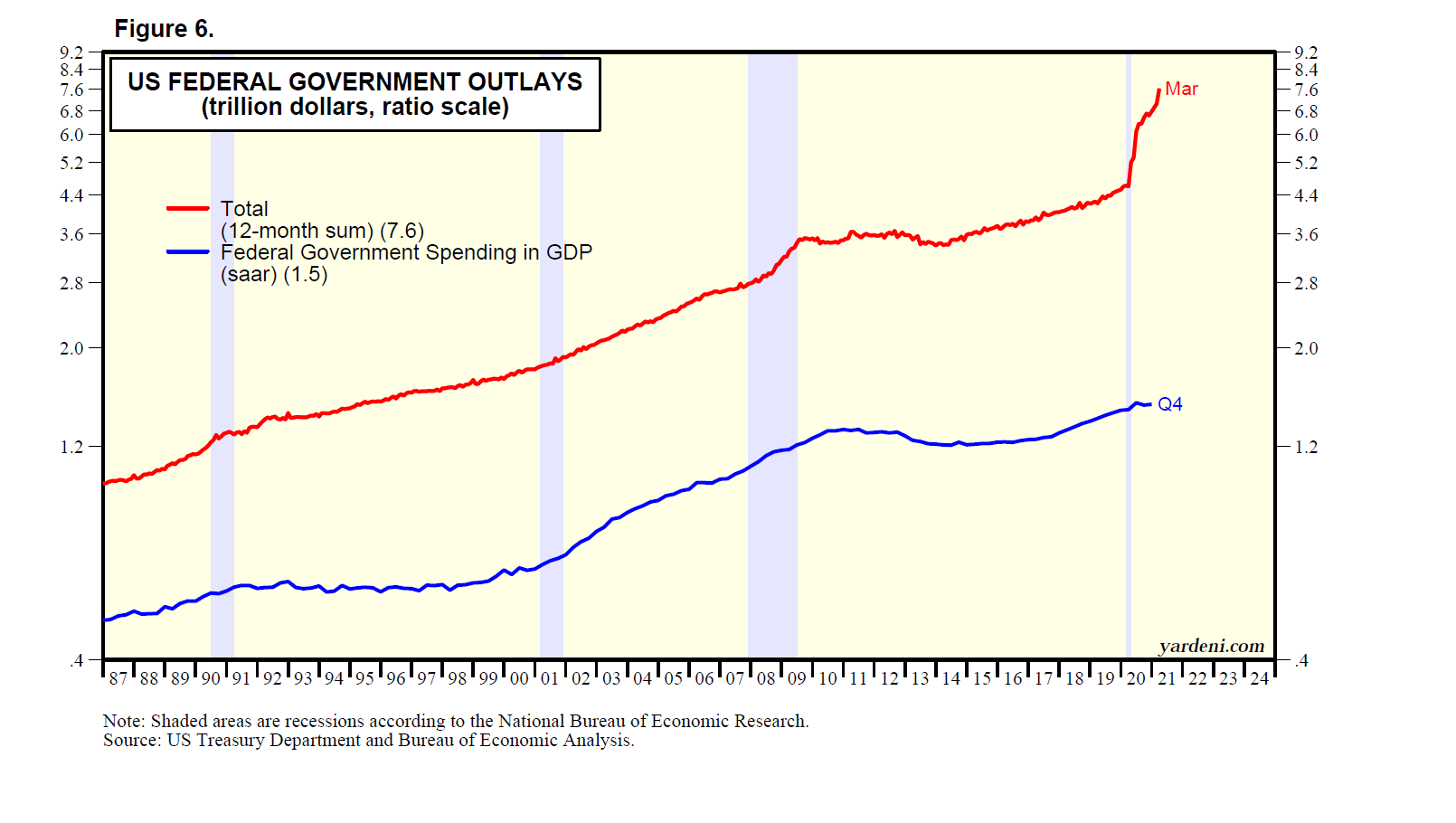

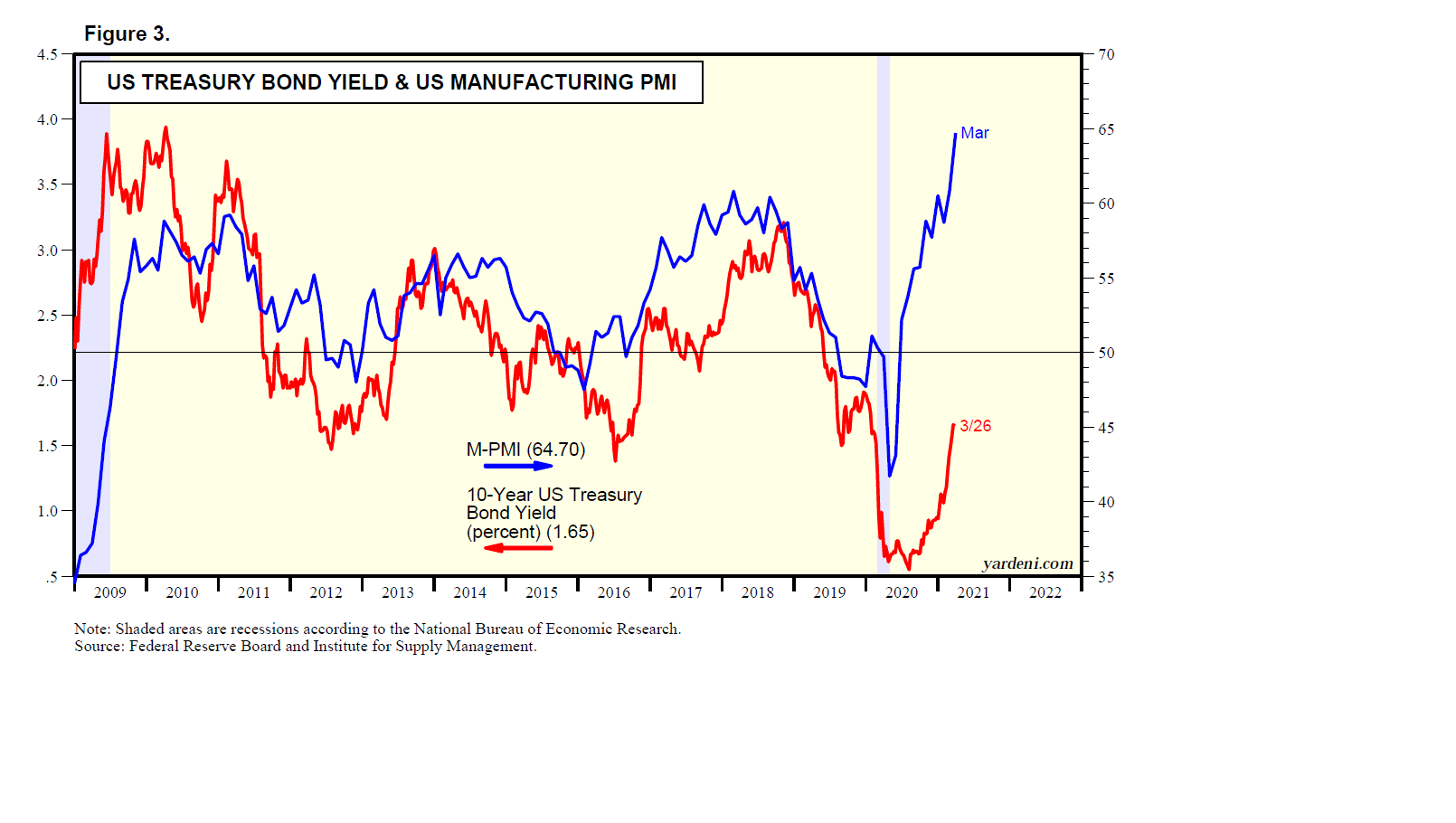

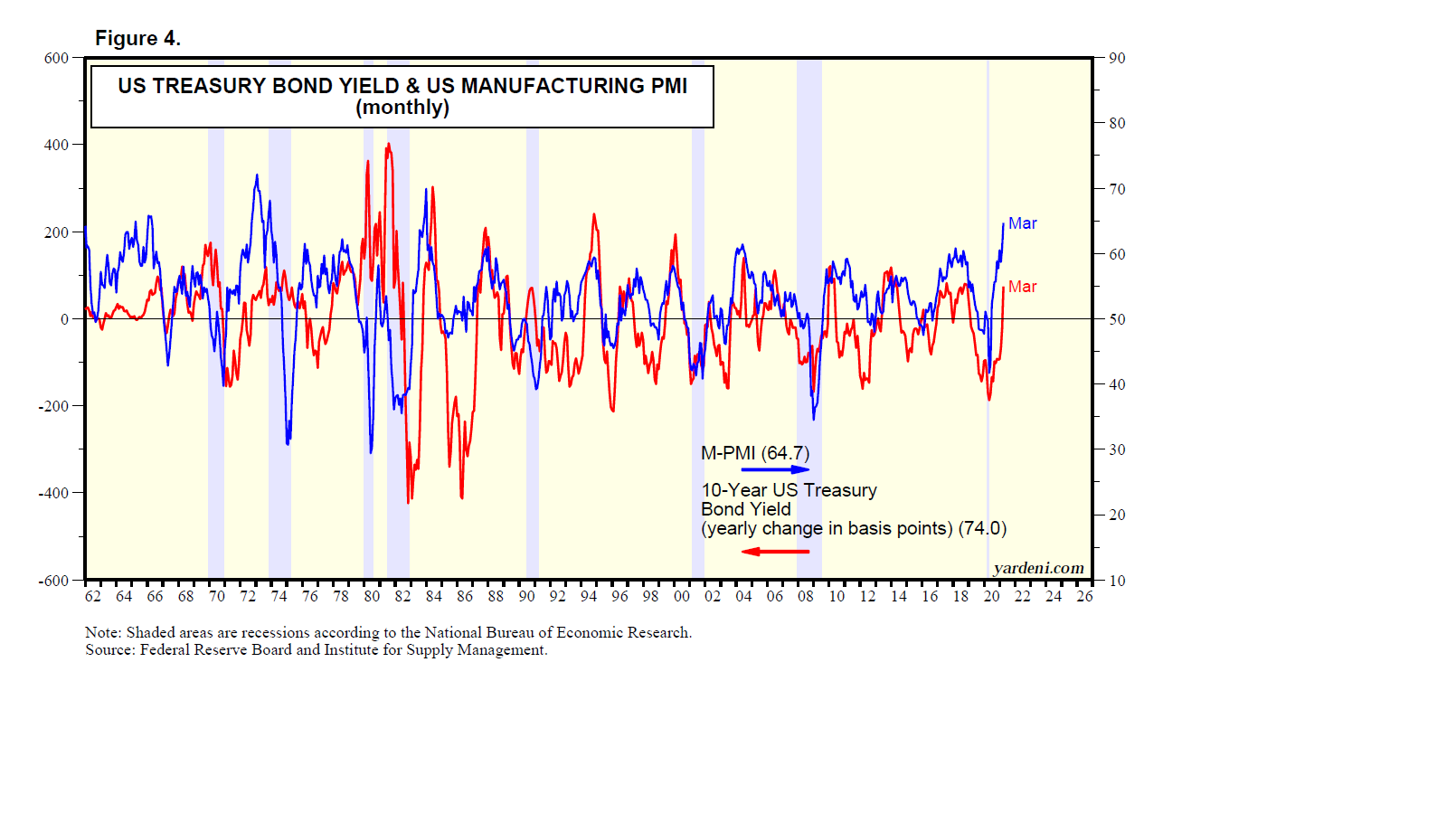

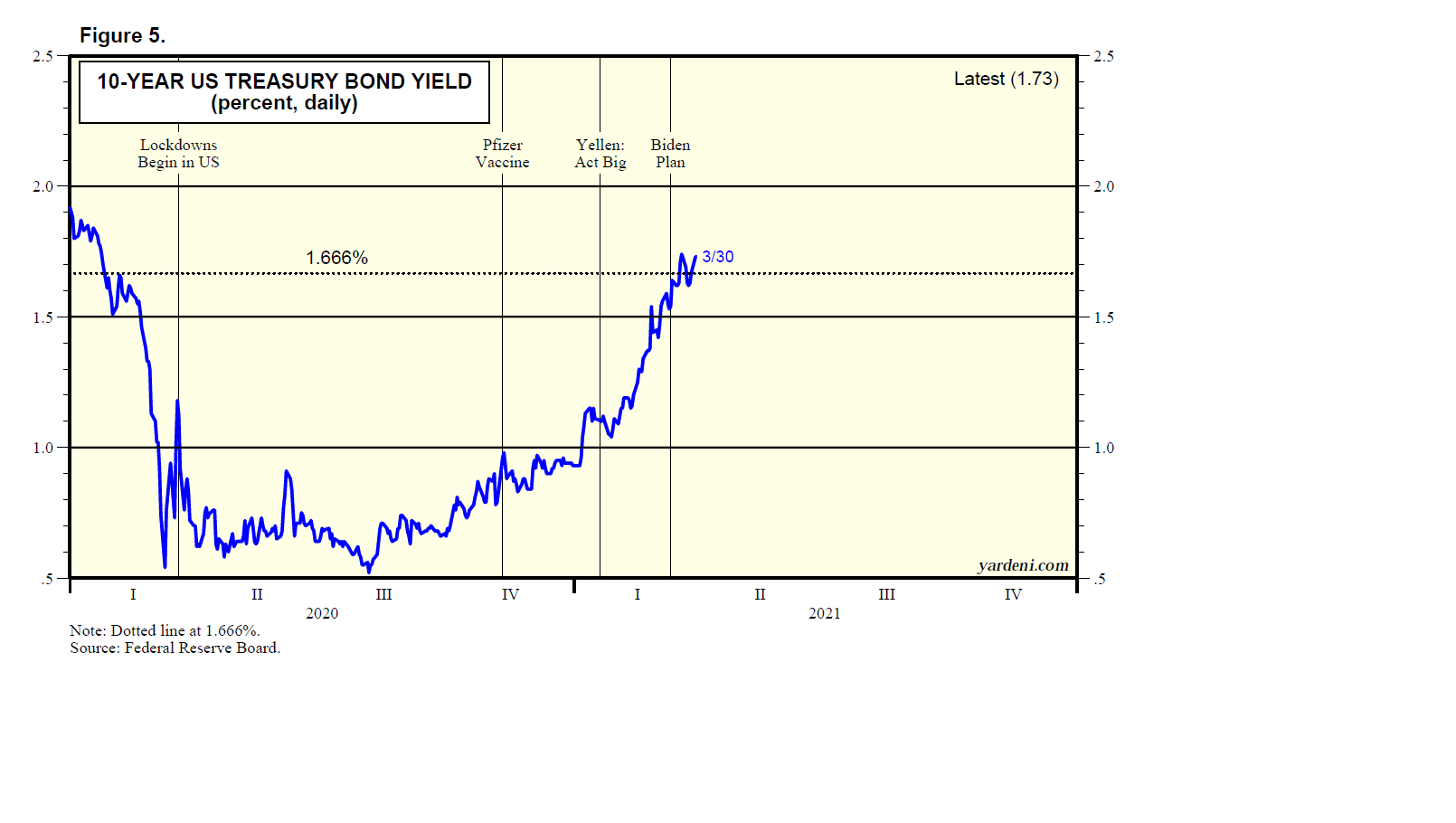

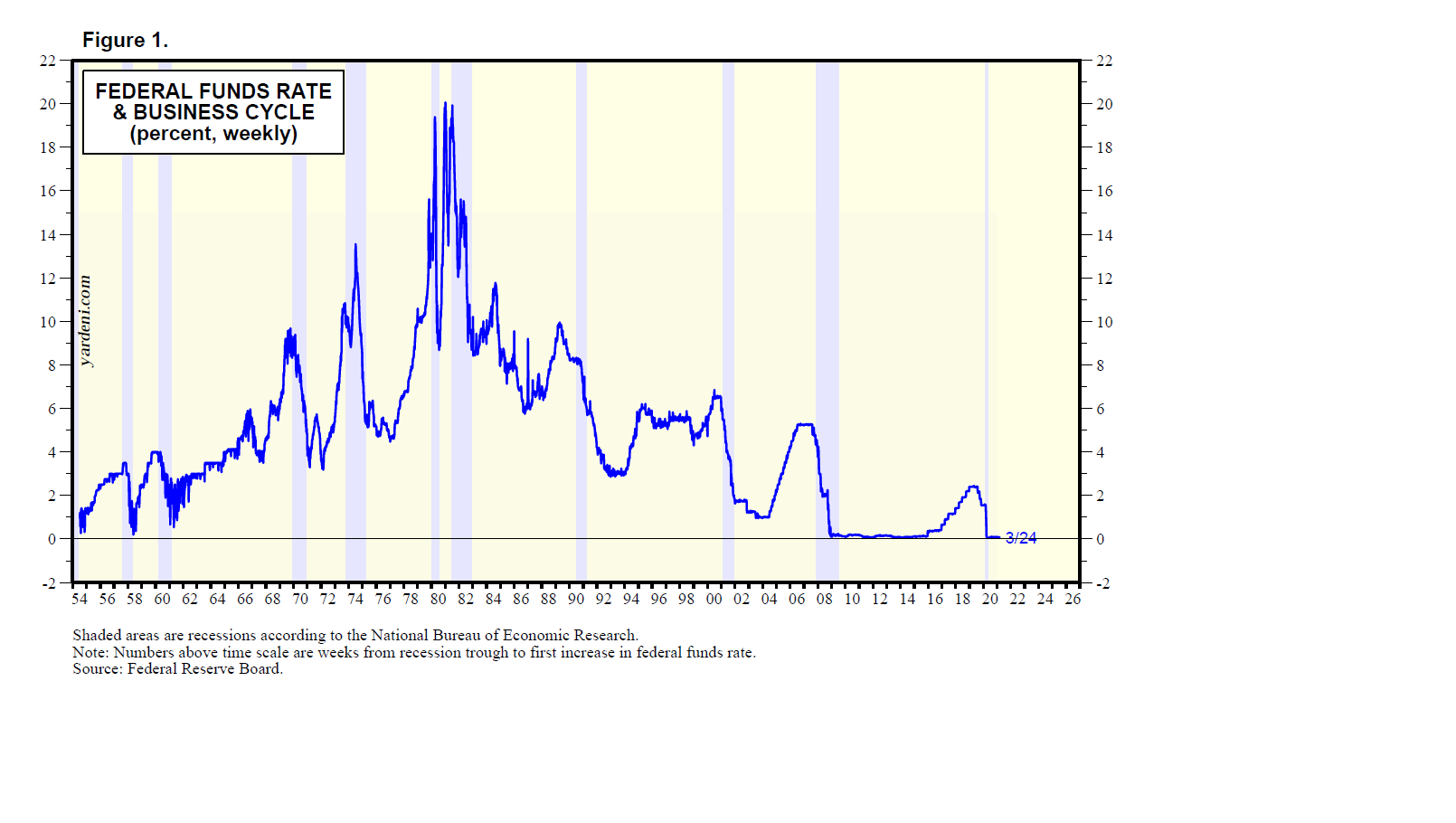

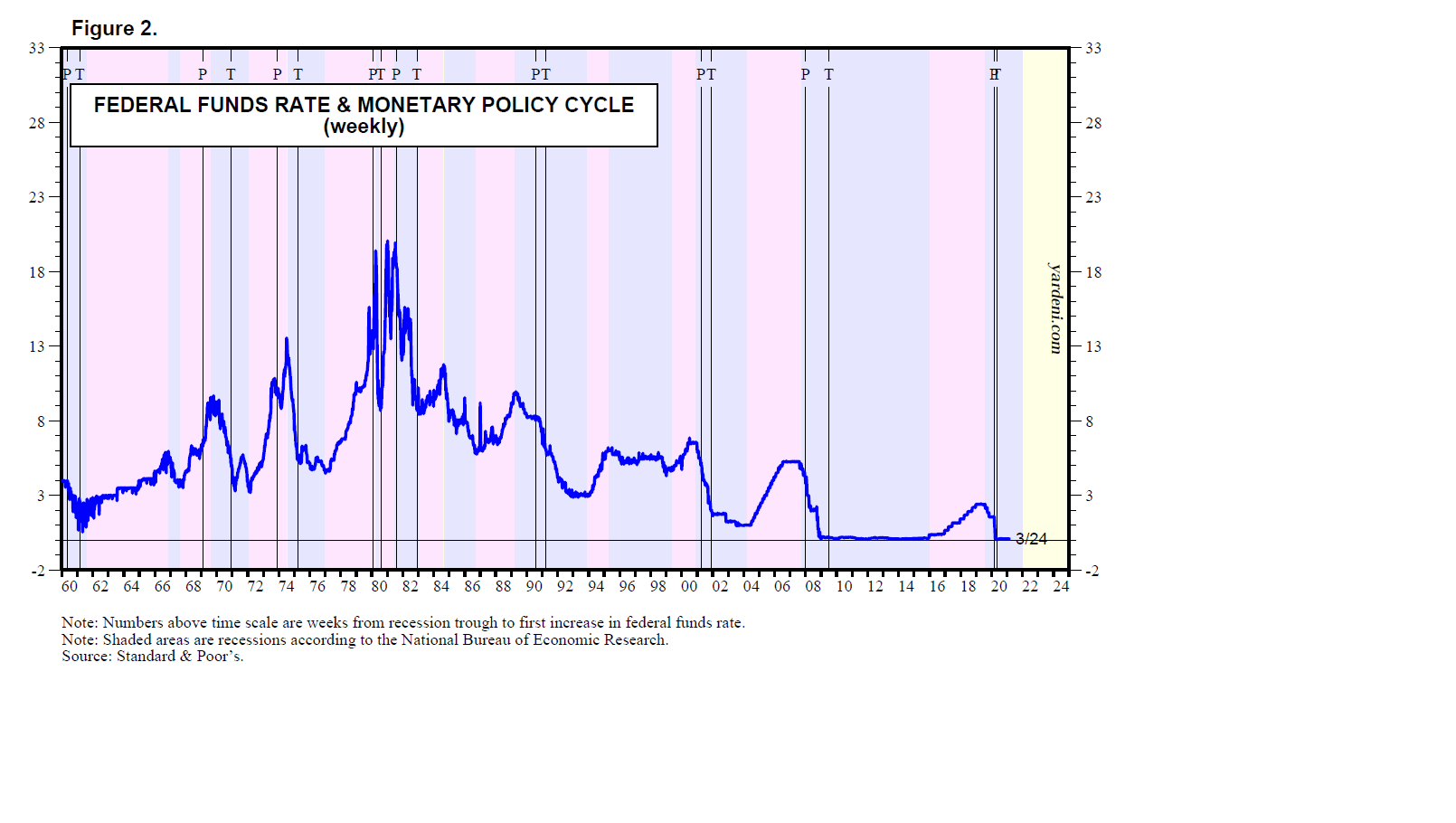

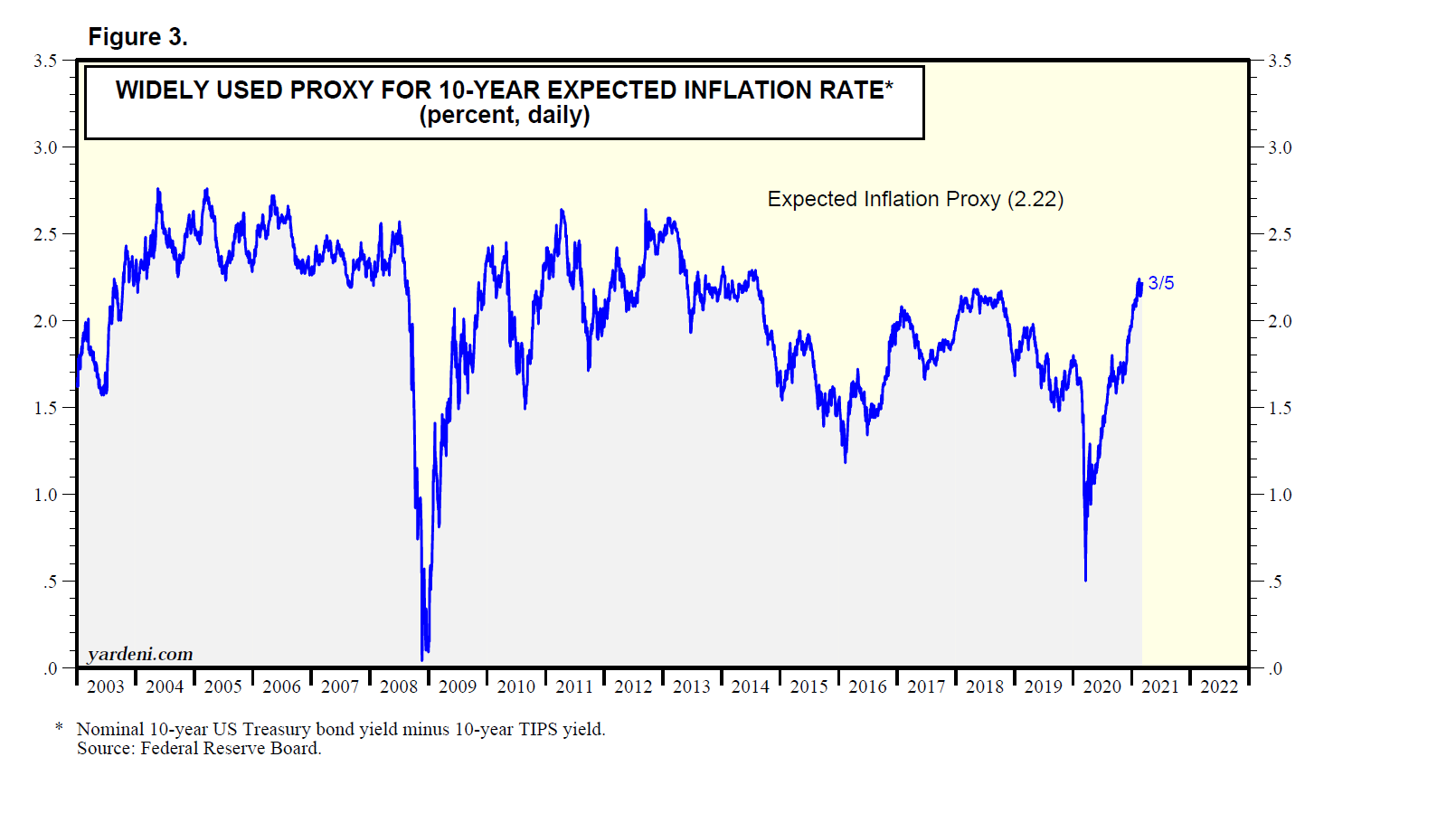

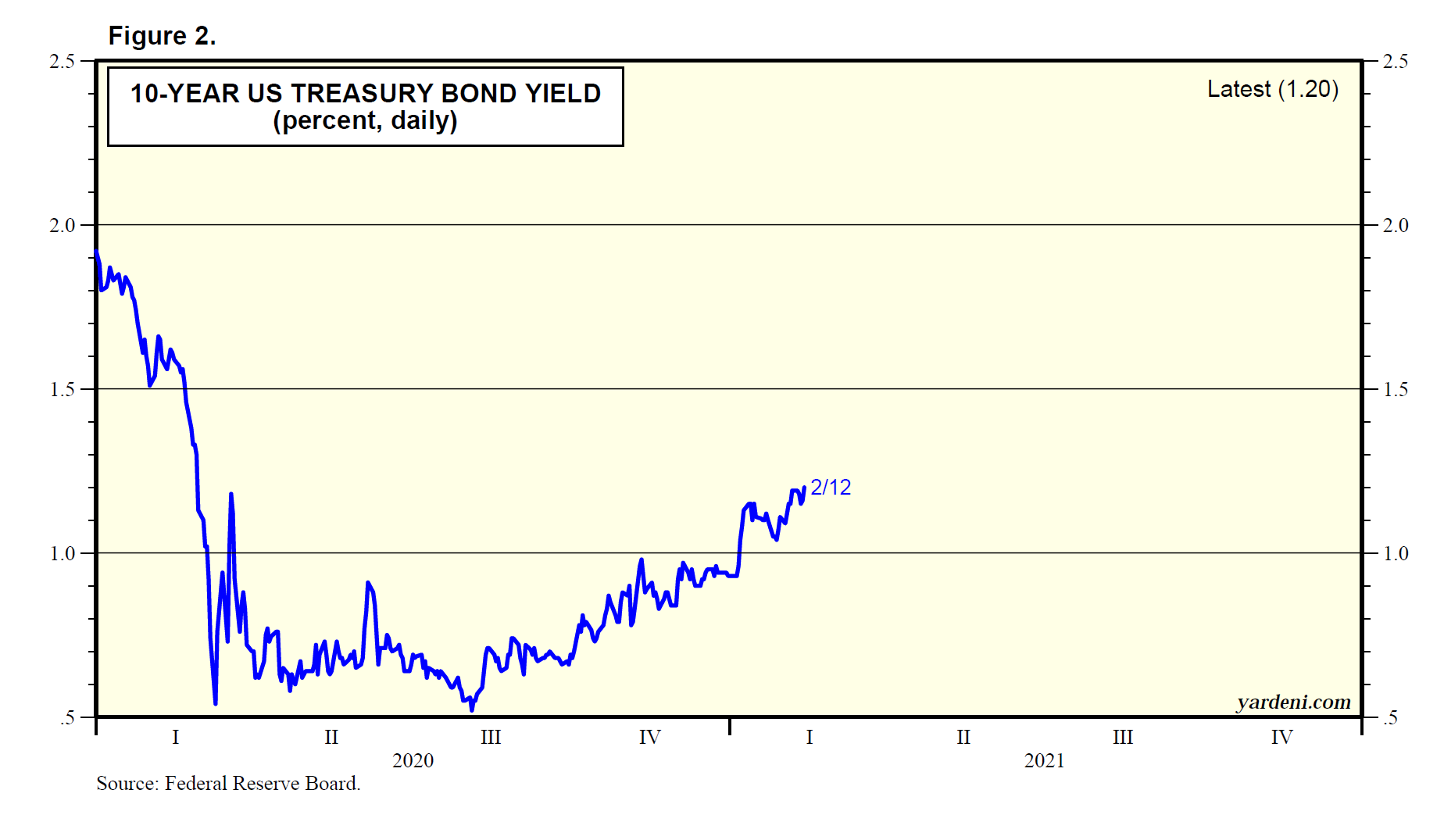

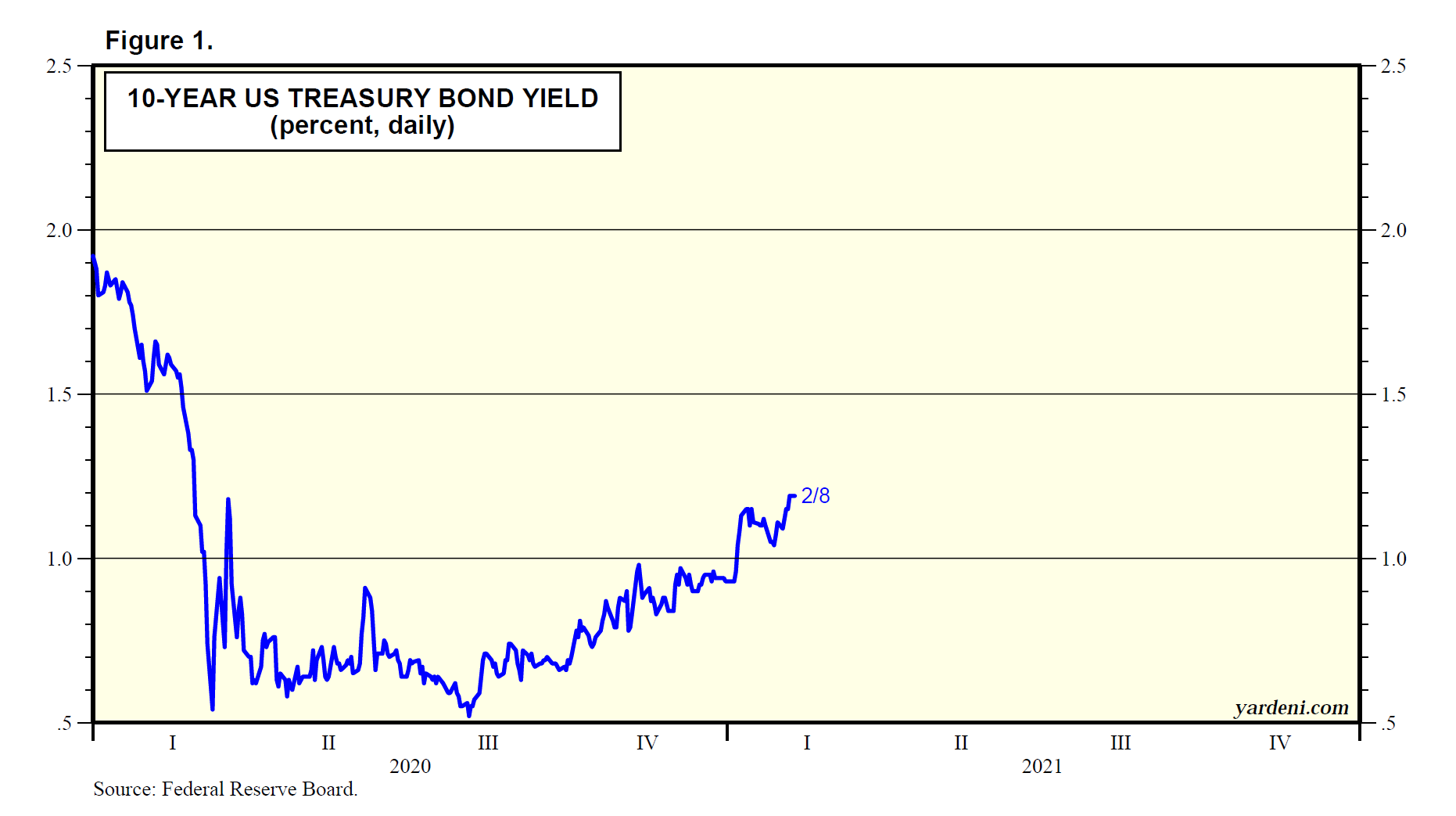

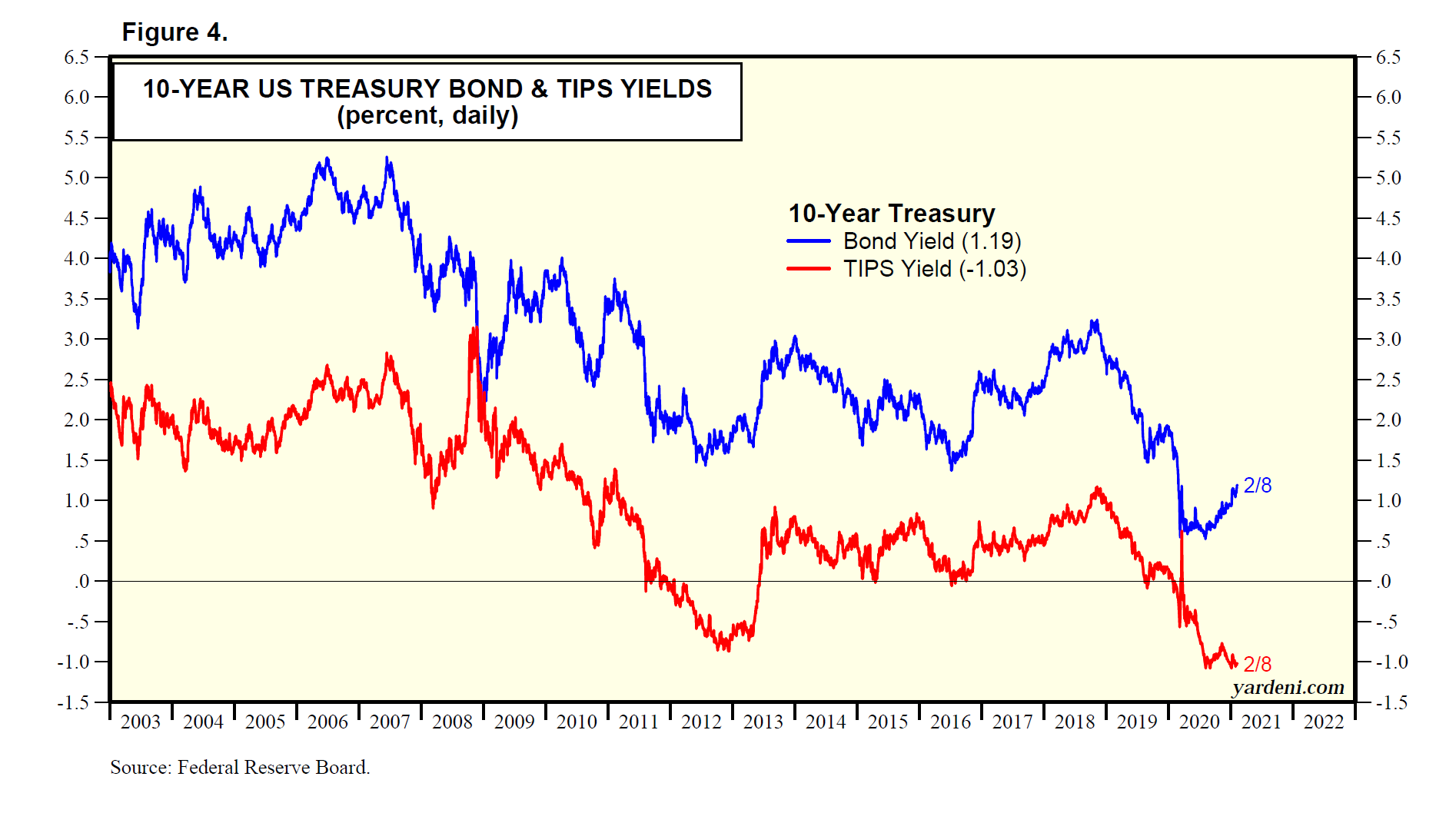

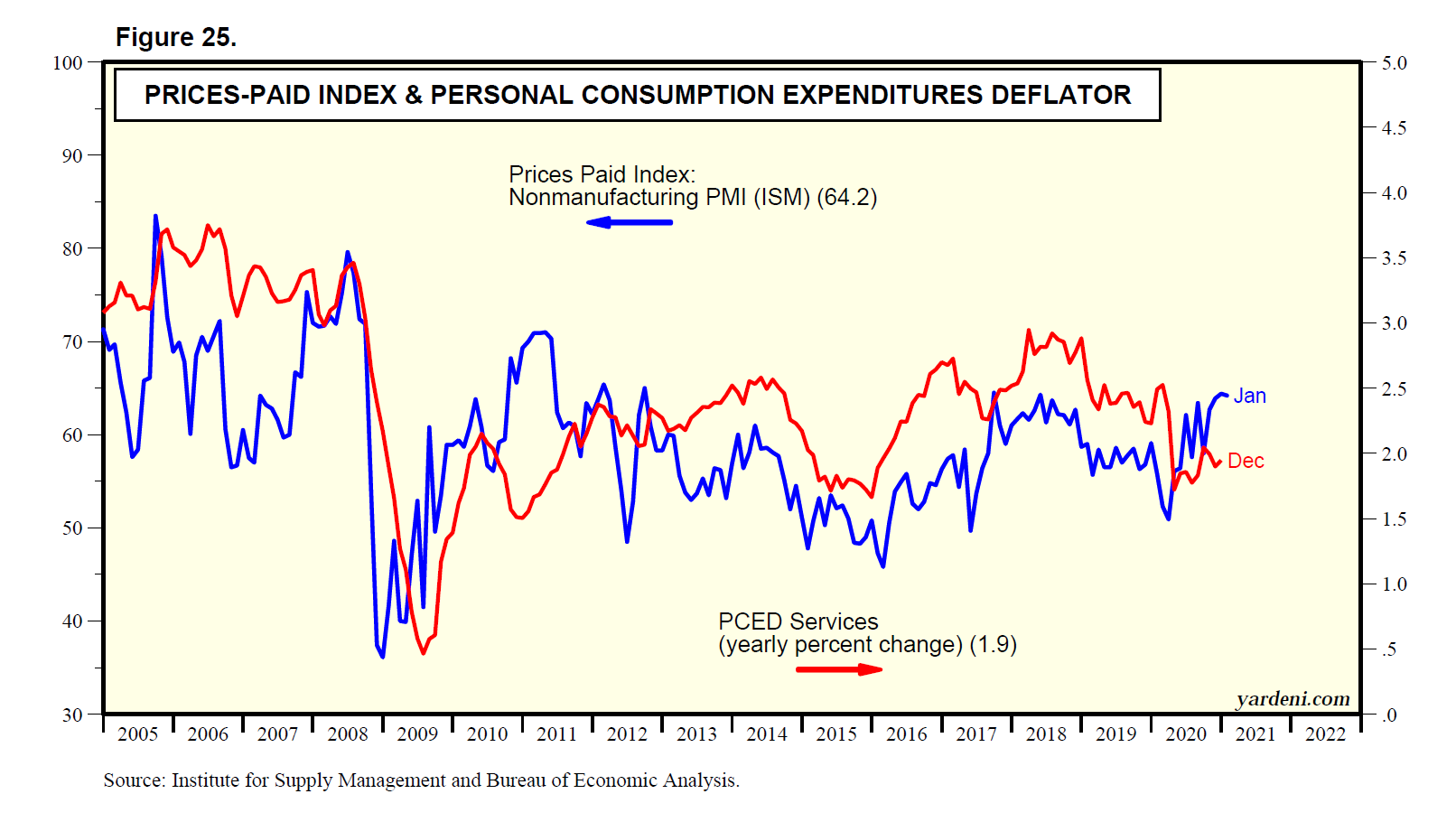

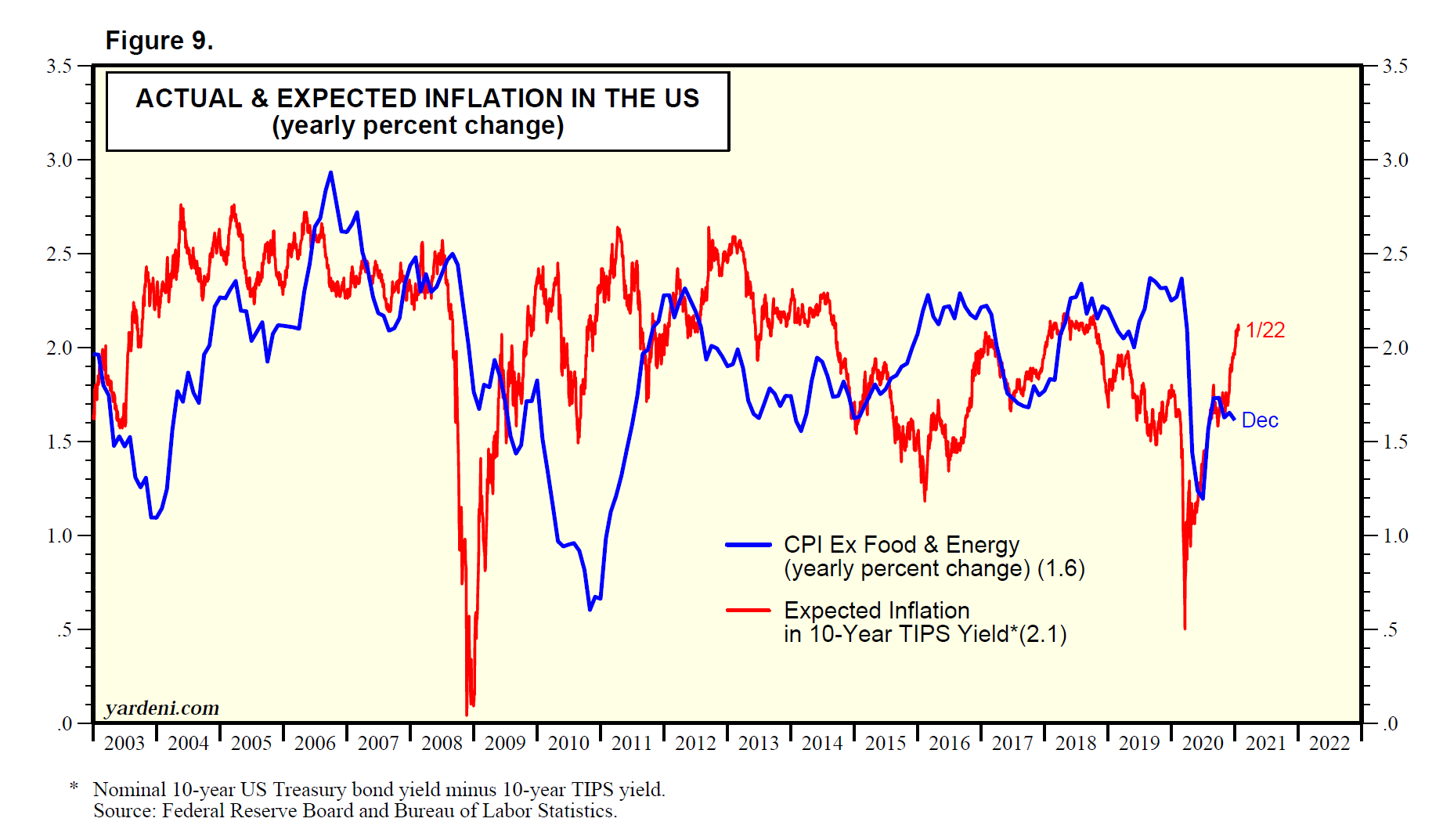

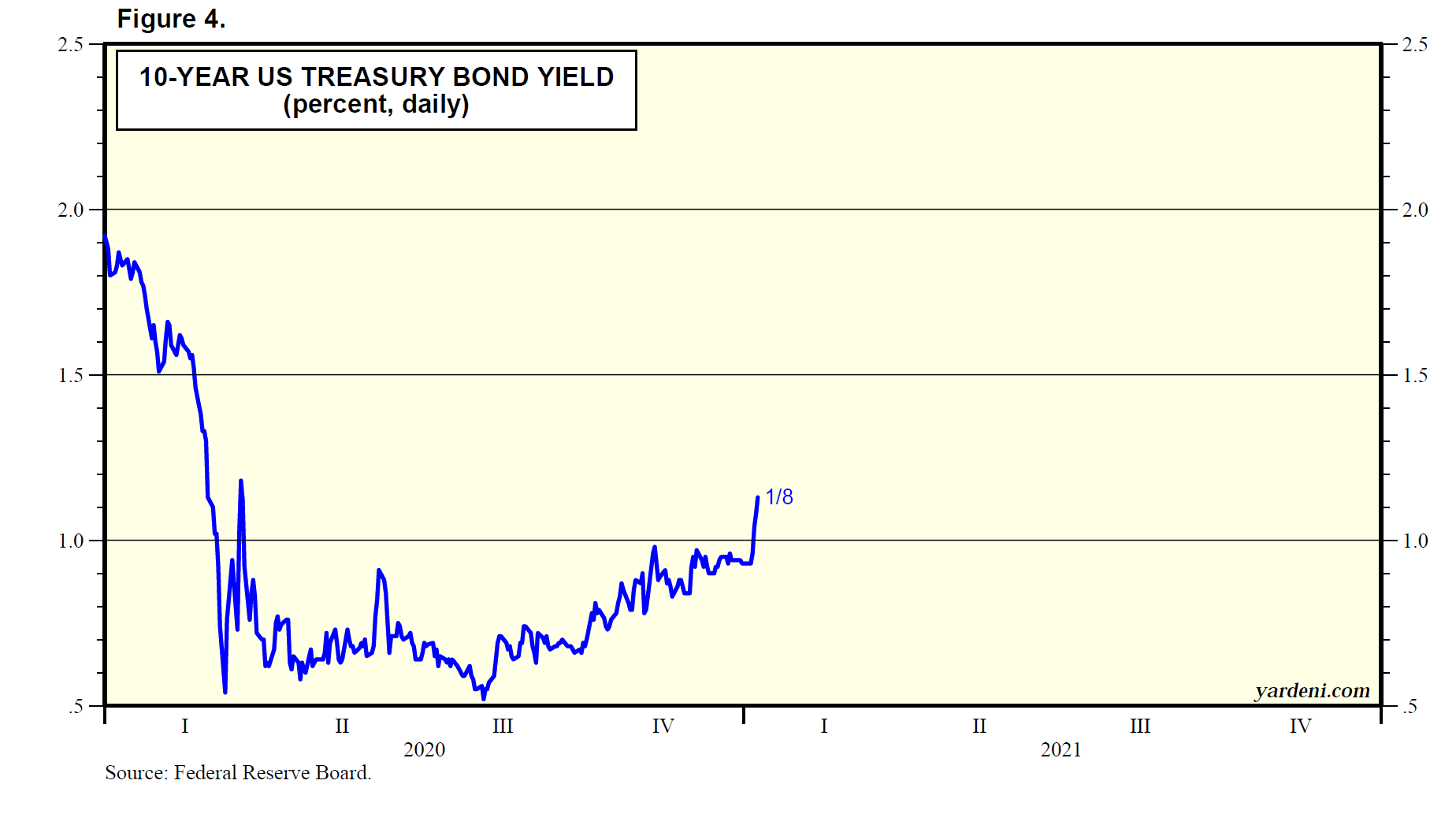

Fed II: Catching Up with the Inflation Curve. The Fed is well behind the inflation curve. The spread between the federal funds rate and the yearly headline CPI inflation rate was -6.7% during November, the most negative reading on record (Fig. 1 and Fig. 2). For that matter, the 10-year US Treasury bond yield is also well behind the inflation curve. The spread between the bond yield and inflation was -5.2% during November, also the most negative reading on record (Fig. 3 and Fig. 4).

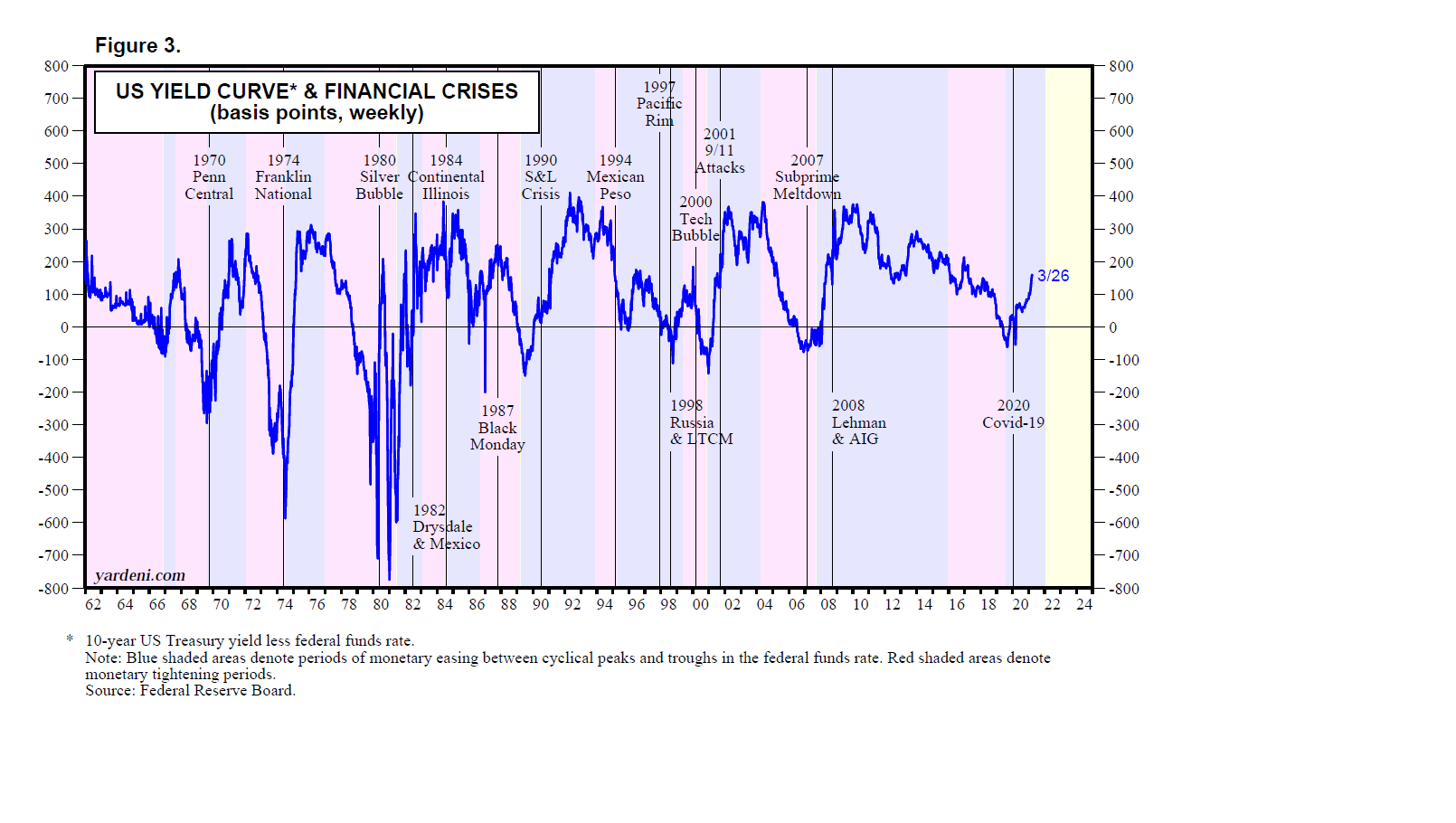

As Debbie and I have previously observed, the yield-curve spread between the 10-year US and 2-year US Treasury notes has declined from a recent peak of 159 bps on March 29 this year to only 77 bps on Tuesday (Fig. 5 and Fig. 6). The 2-year yield was 0.67% on Tuesday, implying three 25-bps hikes in the federal funds rate next year. The 10-year yield has been hovering around 1.50% all year, implying that two to three rate hikes in 2022 might be enough to bring inflation down (along with other factors) (Fig. 7).

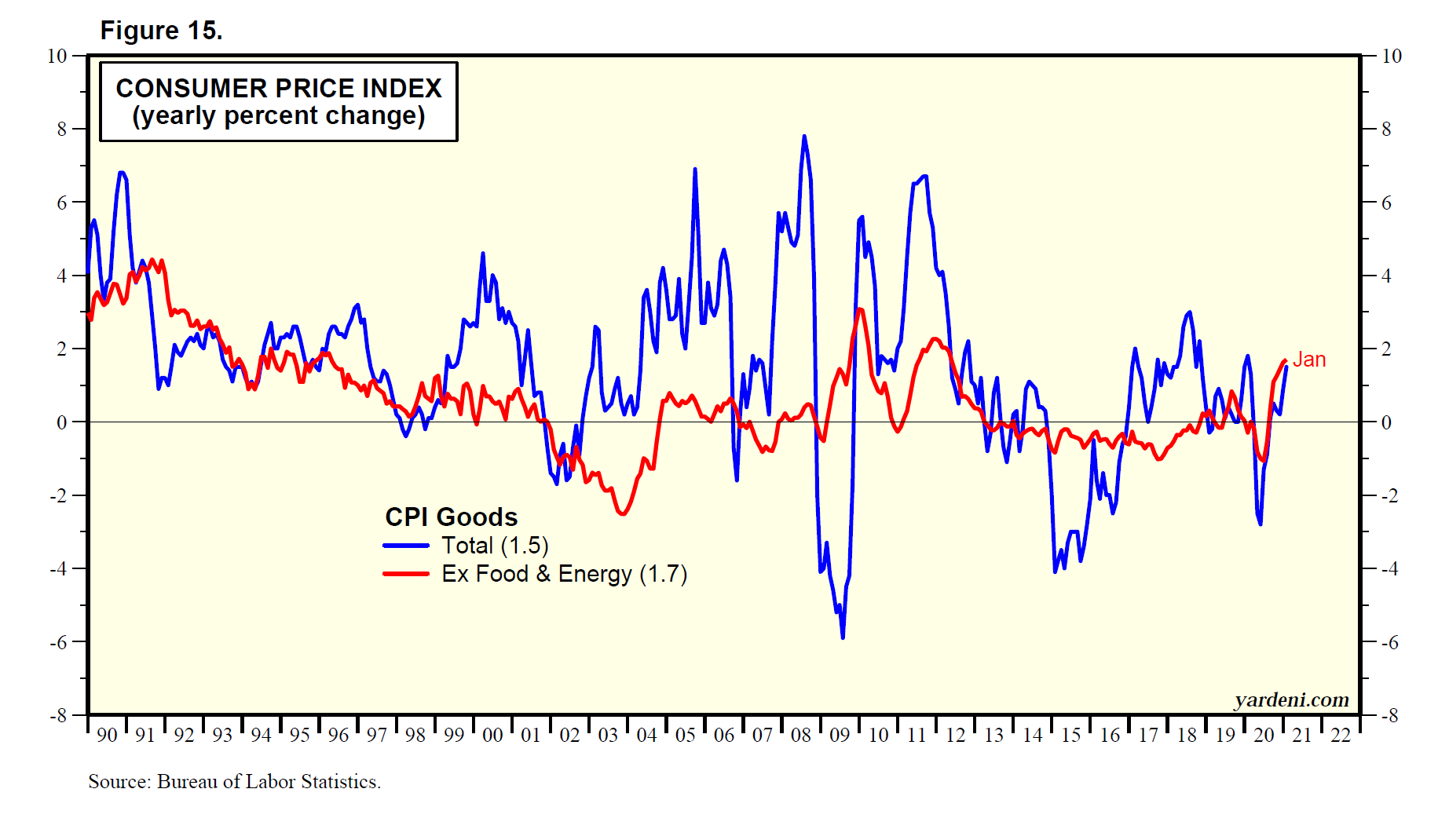

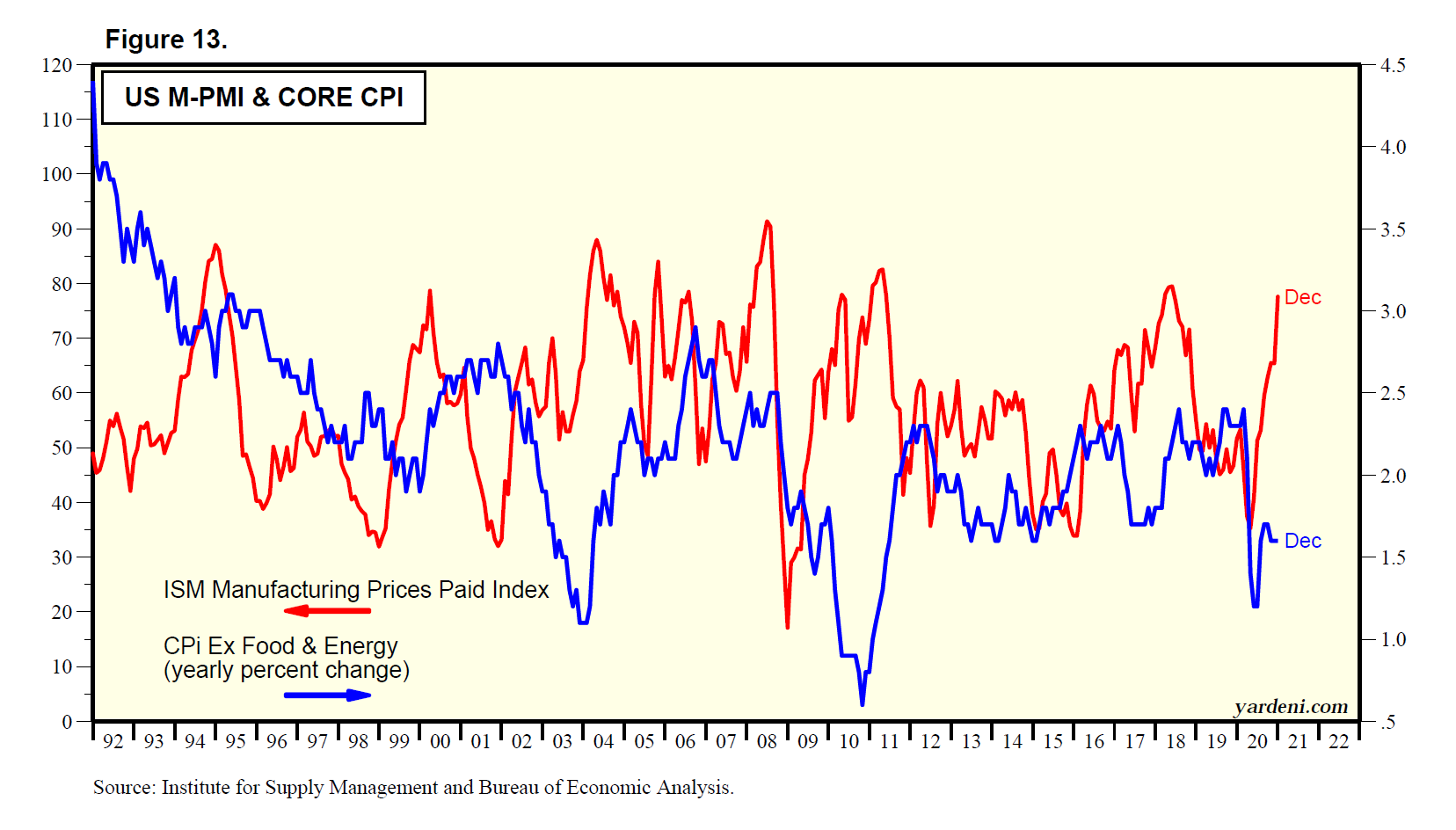

In other words, it might not take many hikes in the federal funds rate for the Fed to catch up with the inflation curve. That, of course, assumes that inflation itself moderates next year. That’s likely to happen if, as we expect, demand for durable goods moderates next year while supply increases, as we discussed in yesterday’s Morning Briefing.

That’s our expectation mostly because pent-up demand for durable goods should be more than satisfied by H2-2022. Durable goods prices have been leading consumer price inflation higher, as we discussed yesterday. So we are assuming that supply-chain disruptions will mostly be behind us after mid-2022, as discussed below.

For now, the latest inflation news remains disconcerting:

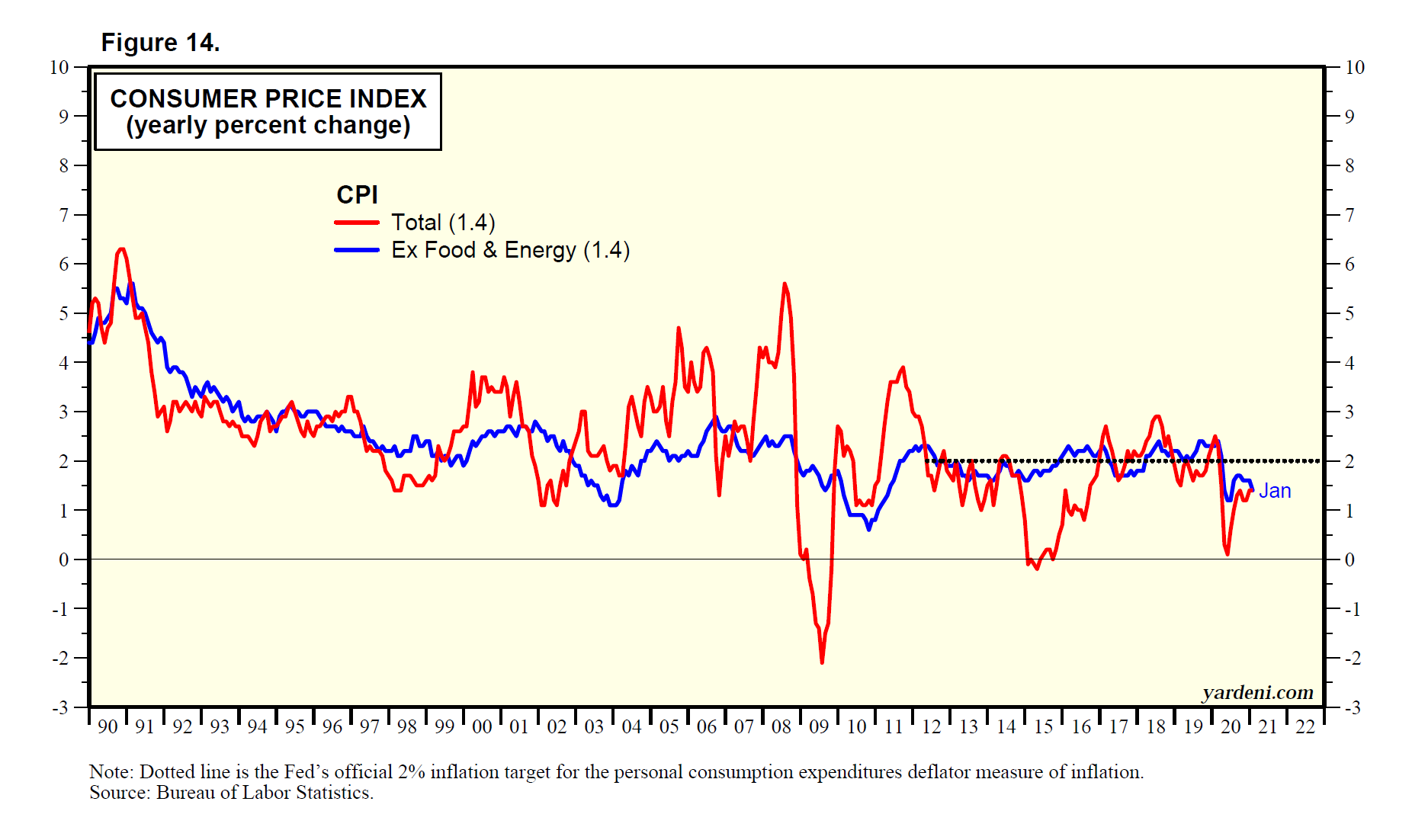

(1) Inflationary expectations. The Federal Reserve Bank’s November survey of consumers’ one-year-ahead inflationary expectations rose to 6.0% (Fig. 8). The latest CPI and PCED inflation rates are 6.8% and 5.0%.

(2) PPI inflation. November’s PPI for final demand was up 9.6% y/y, with goods up 14.9% and services rising 7.1% (Fig. 9). November’s PPI for personal consumption was 8.8% compared to 6.8% for the CPI and 5.0% for October’s PCED (Fig. 10).

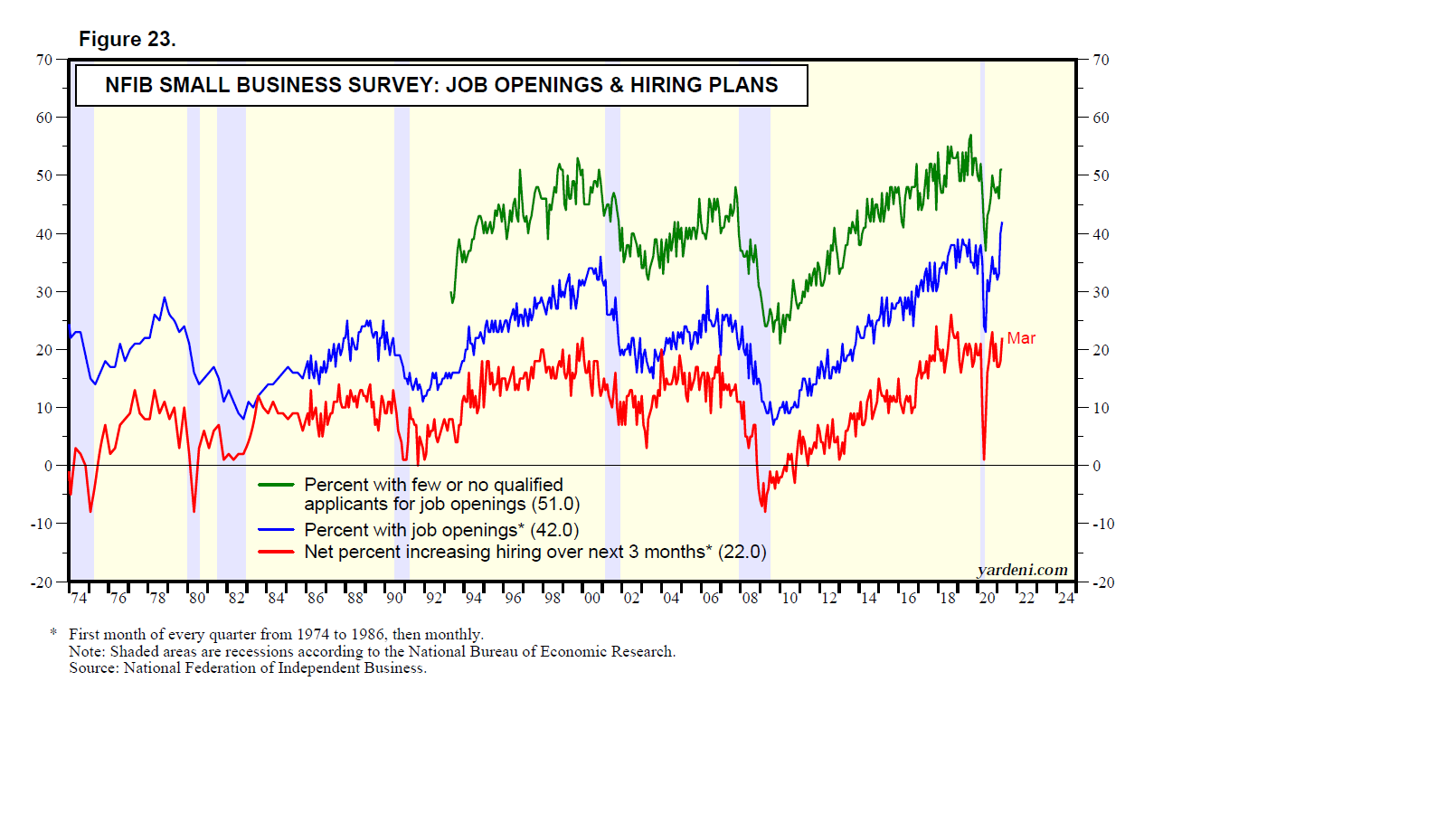

(3) Small business owners. November’s survey of small business owners conducted by the National Federation of Independent Business found that 59% of them are raising average selling prices and 54% planning to do so (Fig. 11). The former is the highest since the 1970s, the latter the highest on record. Furthermore, a record 32% of small business owners are planning to raise worker compensation (Fig. 12).

Global Supply Chains I: Durable Woes. The Fed’s December 1 Beige Book provided a good overview of where the kinks persist in supply chains. Several Federal Reserve districts reported strong demand and positive outlooks overall, but with growth constrained by supply-chain disruptions and labor shortages.

When the supply challenges are expected to subside is uncertain, with some Cleveland contacts saying they expect disruptions into 2022, some Chicago contacts citing H2-2022, and some Atlanta transportation contacts not anticipating supply-chain normalization until late 2022 or 2023. The widespread consensus seems to be mid-2022.

Here’s more on the bottlenecks, according to the Fed districts:

(1) Durable goods. Most impacted by weak supply chains are the availability of durable goods, especially autos. Boston contacts noted that overall consumer spending was steady but that sales of durables are restrained by severe supply shortages. Mostly due to a lack of supply, new vehicle sales continued to weaken, reported New York contacts. In Philadelphia, auto sales held at low levels as supply-chain issues “continued to plague auto dealers.” Persistent supply-side disruptions and related higher prices are causing some customers to put off spending until these pressures abate.

For some types of machinery, material and equipment lead times could be up to 10 months, Dallas contacts said. In New York, supply disruptions have caused “scattered stockouts,” particularly for furniture.

(2) Input & inventory shortages. Many of the goods that are held up are not getting through the production line because key components are missing. Auto manufacturers are producing well below capacity mainly because of the ongoing microchip shortages, two major St. Louis manufacturers observed. Nevertheless, a few Cleveland contacts suggested that the availability of semiconductors, a key constraint in the production of many goods including autos, had “increased somewhat over the prior two months.” However, auto dealers suggested that sales will remain weak until inventory levels recover. Atlanta auto dealer inventories remained challenged by supply-chain issues.

That’s not just the case for autos: Minneapolis retailers reported missed sales due to supply-chain-related inventory shortages. Chicago’s manufacturing contacts said that “for sale inventories rose slightly but were still tight, and there were shortages of a wide range of inputs including certain metals, chemicals, resins, foam, adhesives, pallets, paper, and electrical components.” Supply-chain disruptions or delays remained widespread, with many Dallas firms noting that the inability to secure raw materials was affecting their ability to meet demand.

Kansas City contacts noted a shift in their approach to managing supply-chain disruptions toward a strategy of holding larger inventories, which was further pressuring the demand for key inputs. San Francisco manufacturers were stockpiling raw materials despite reduced availability and rising costs for inputs. Some San Francisco contacts additionally mentioned increased investment in new technologies “to improve resilience in the production process.” Some St Louis firms aimed to get around the input challenges by working to manufacture their own electric vehicle components rather than relying on global supply chains.

(3) Logistics. Even once goods are produced, the challenges aren’t over: It’s been tough to get them where they are going. Richmond ports and trucking companies “saw modest to moderate increases in volumes from already high levels, and they had difficulty meeting demand due to capacity and labor constraints. Shortages of transportation equipment and warehouse space led imports to dwell at the ports for longer times, causing congestion. Contacts noted that many empty containers were being shipped back to Asia before they could be loaded with exports as ocean carriers could get higher rates for import cargos.”

(4) Real estate. In addition to durable goods, real estate is another market plagued by supply constraints. Demand for homes remains strong in Philadelphia, the district reported, but sales are constrained by higher prices and longer delivery times. Also in the region, construction activity remains busy, but efficiency is challenged by supply constraints and contractor availability. Cleveland contacts noted increased lead times for new homes as weak supply-chains hindered construction activity. Chicago’s residential and nonresidential construction growth was held back by materials and labor supply challenges.

Global Supply Chains II: Downer Dashboard. Several key economic indicators, including inflation rates, may hold clues to whether the supply disruptions are worsening or improving. Among those besides inflation that we’re monitoring are the following:

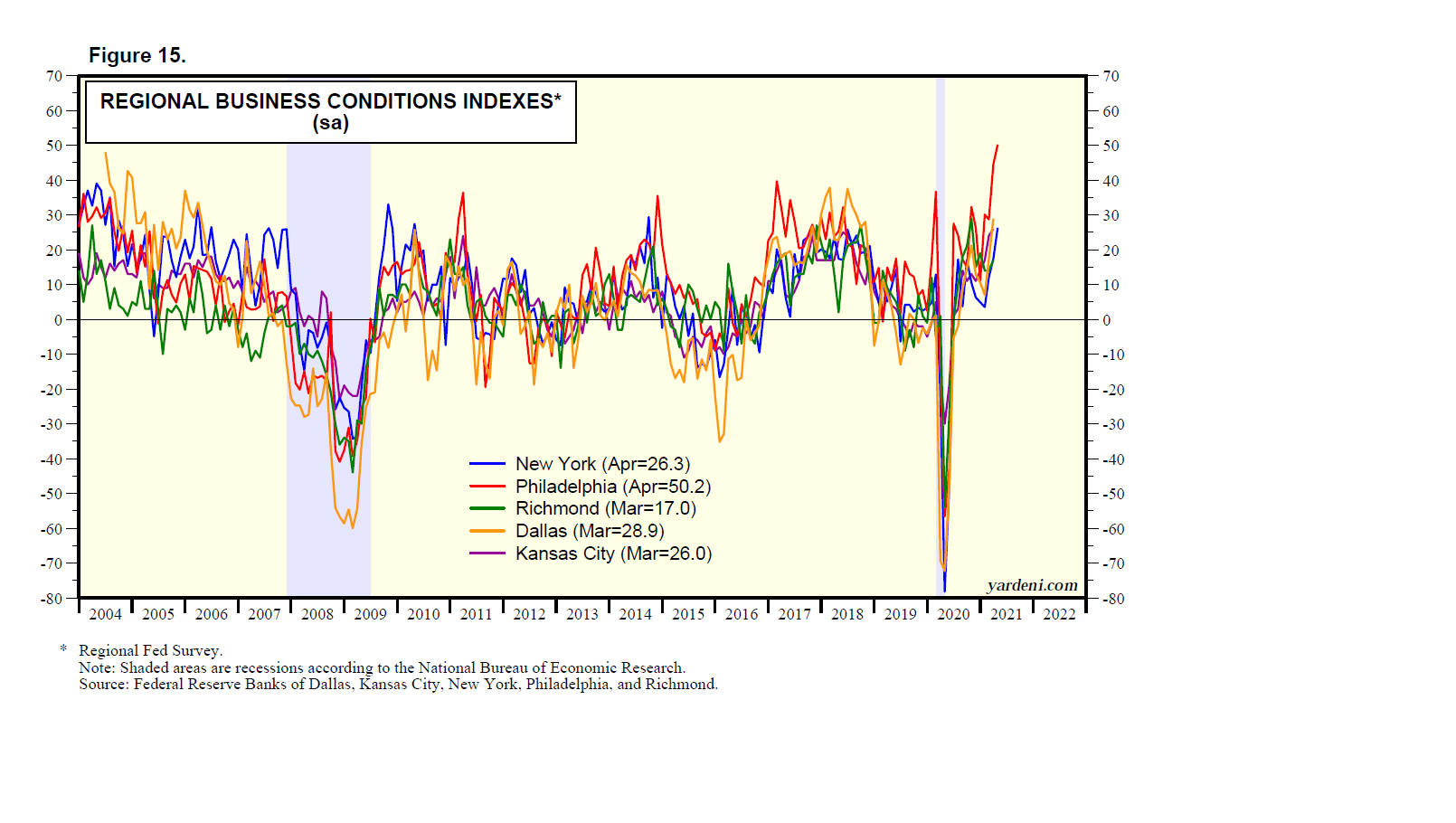

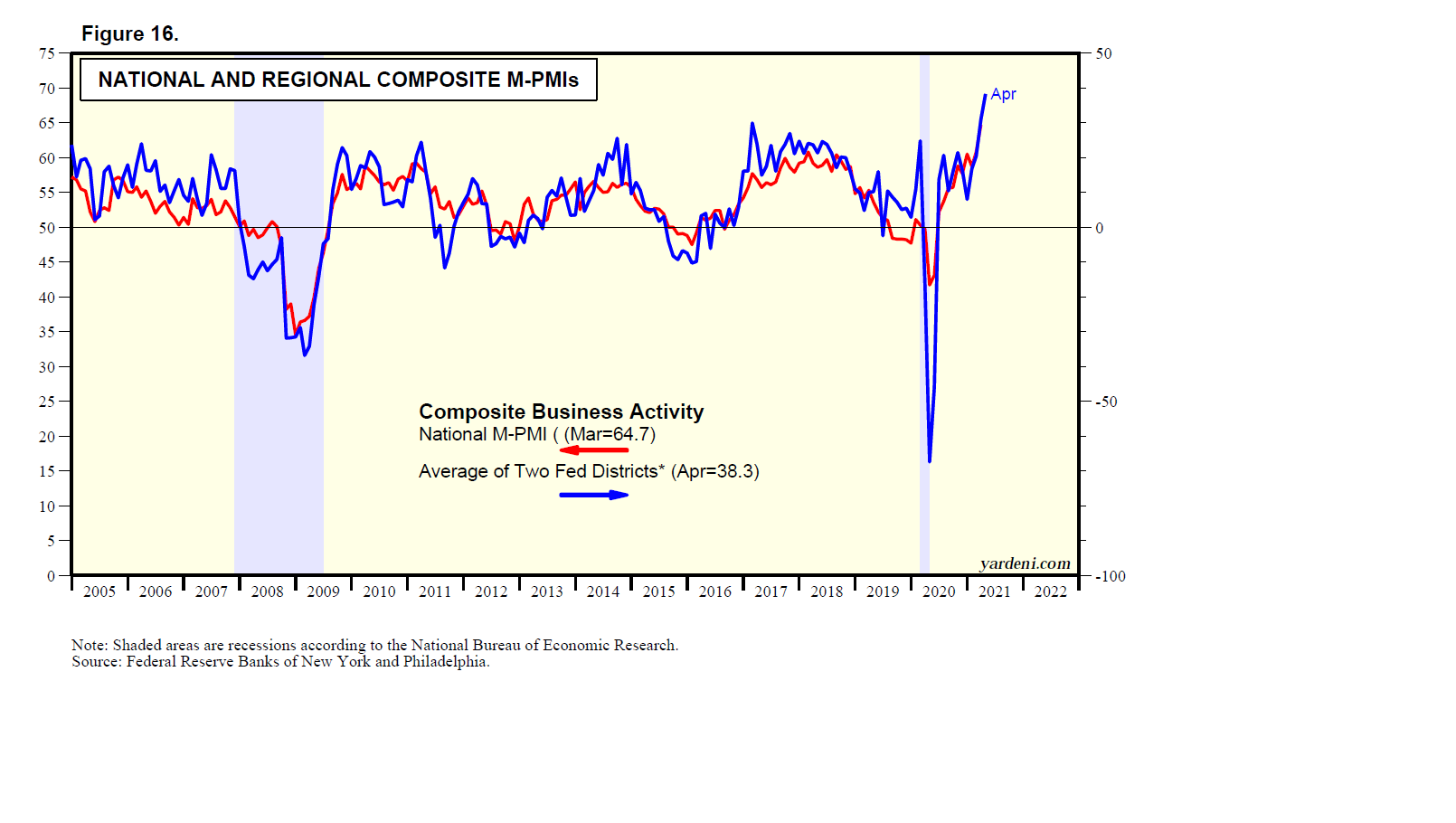

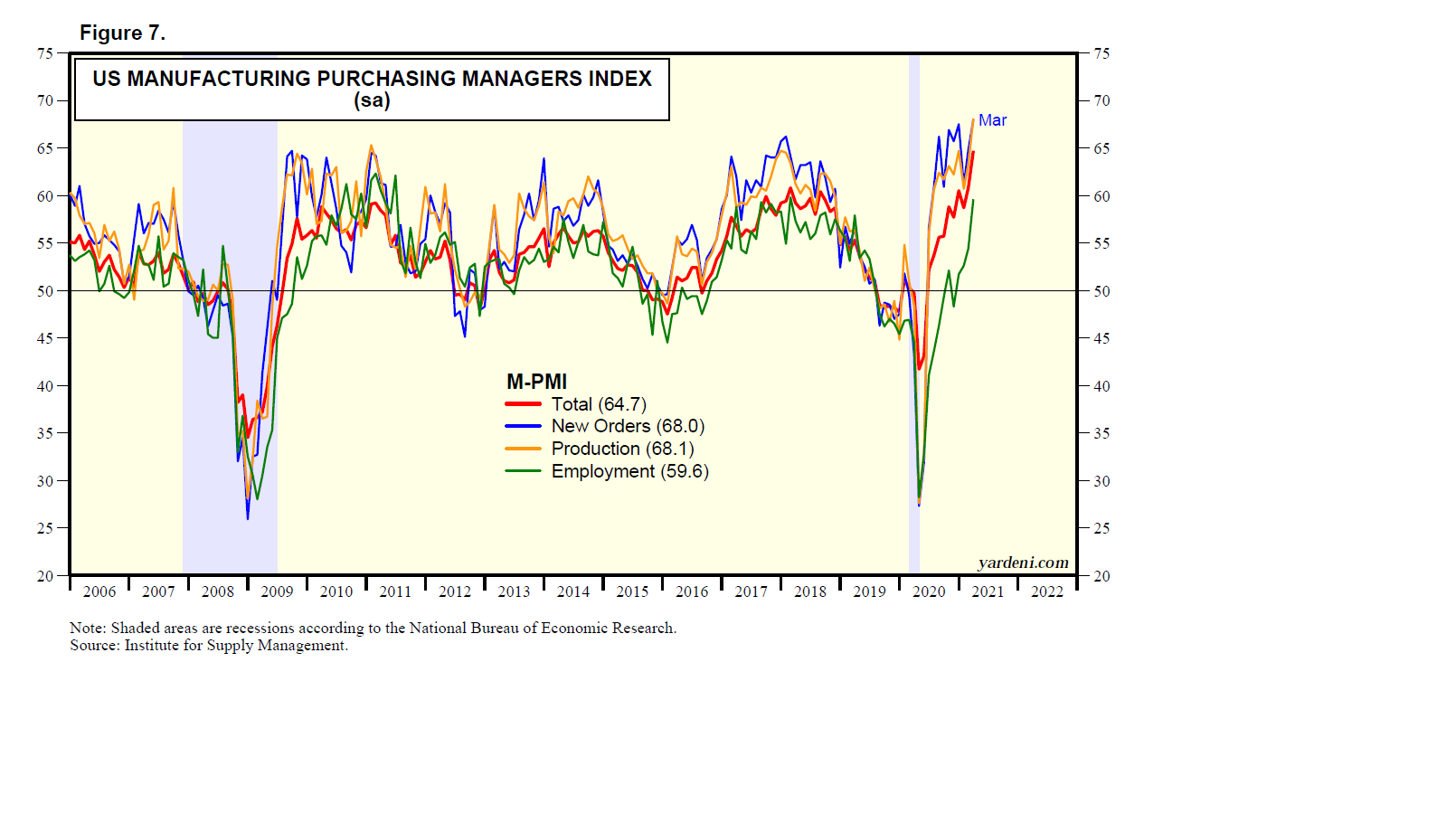

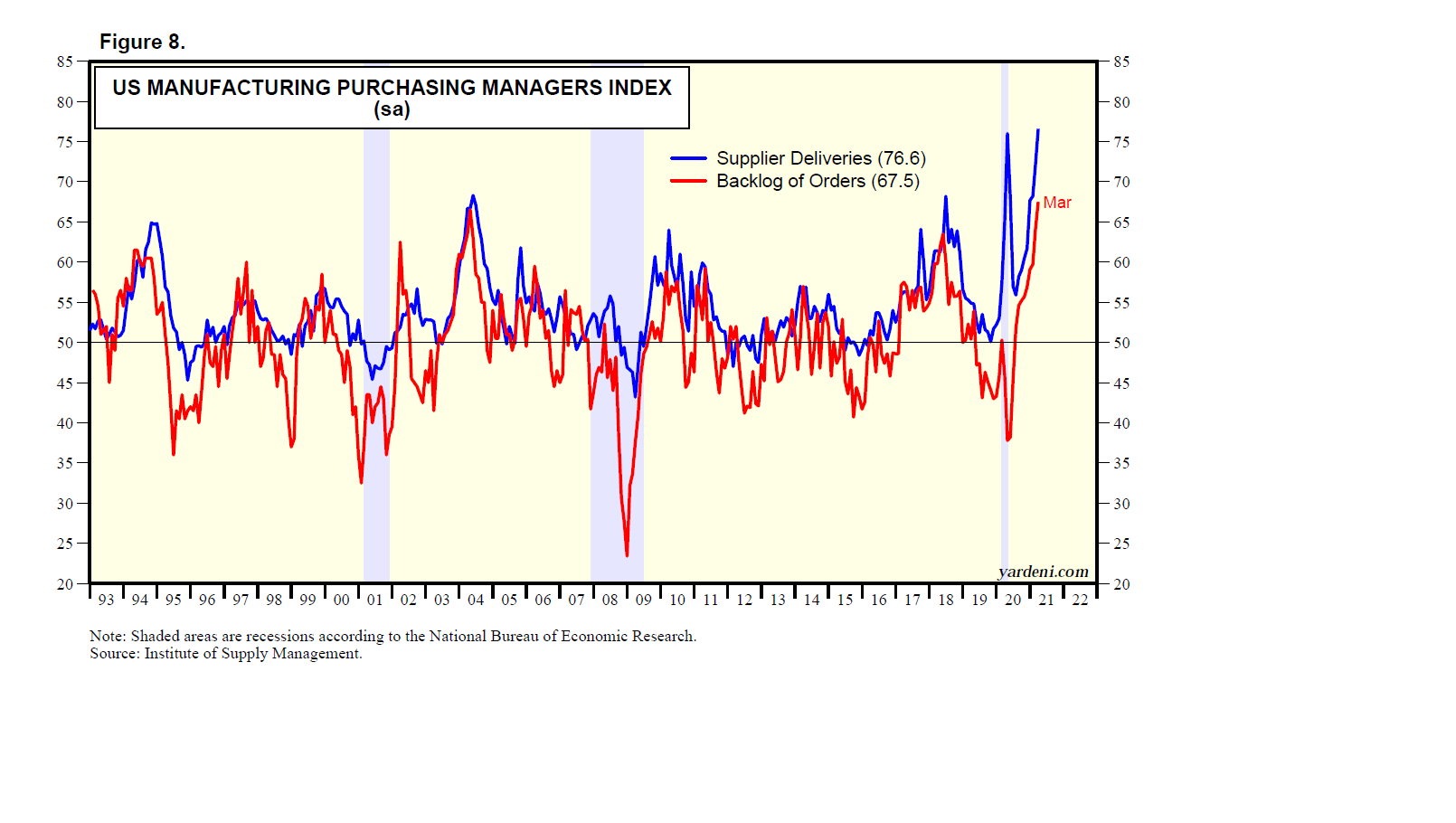

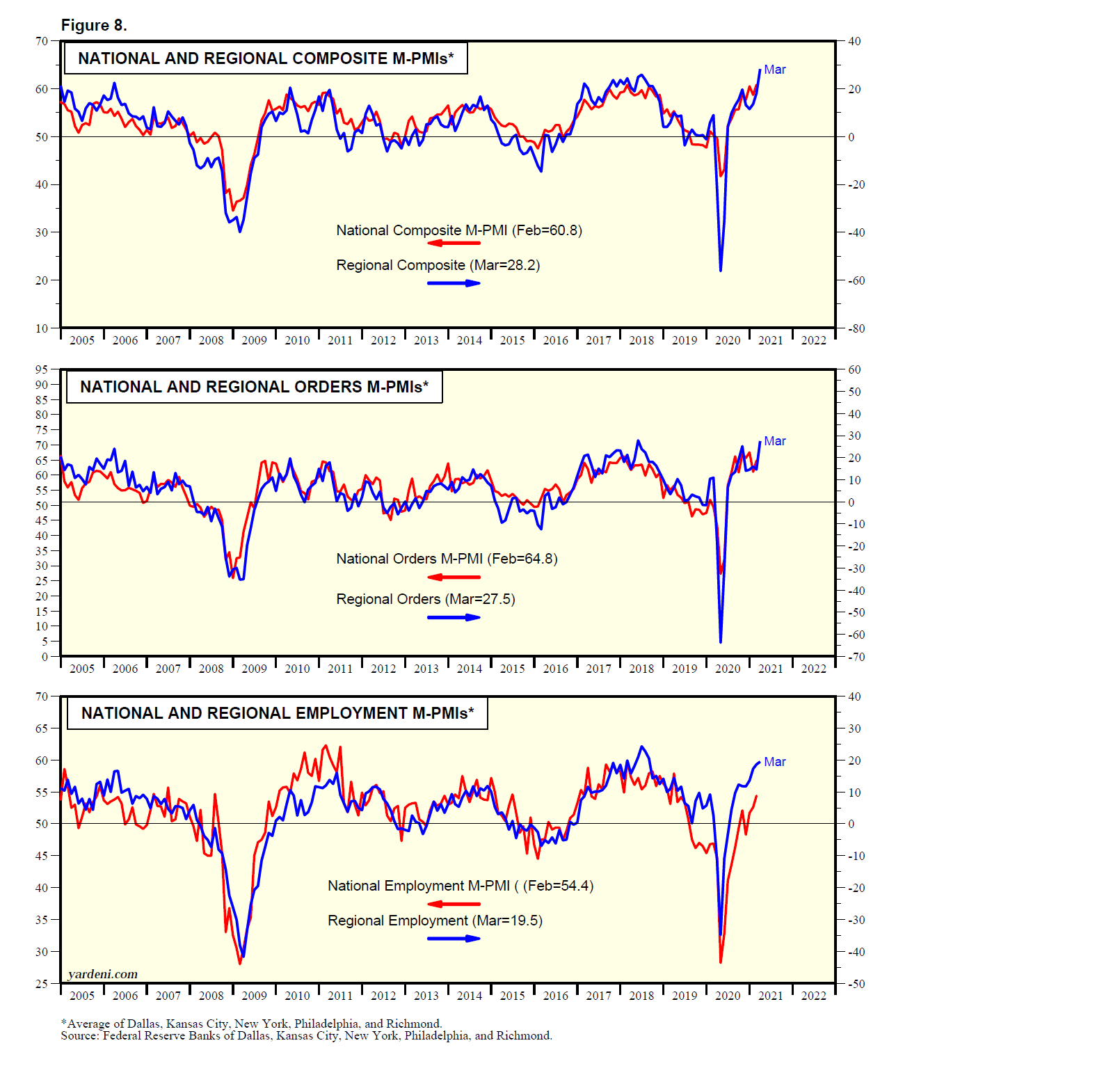

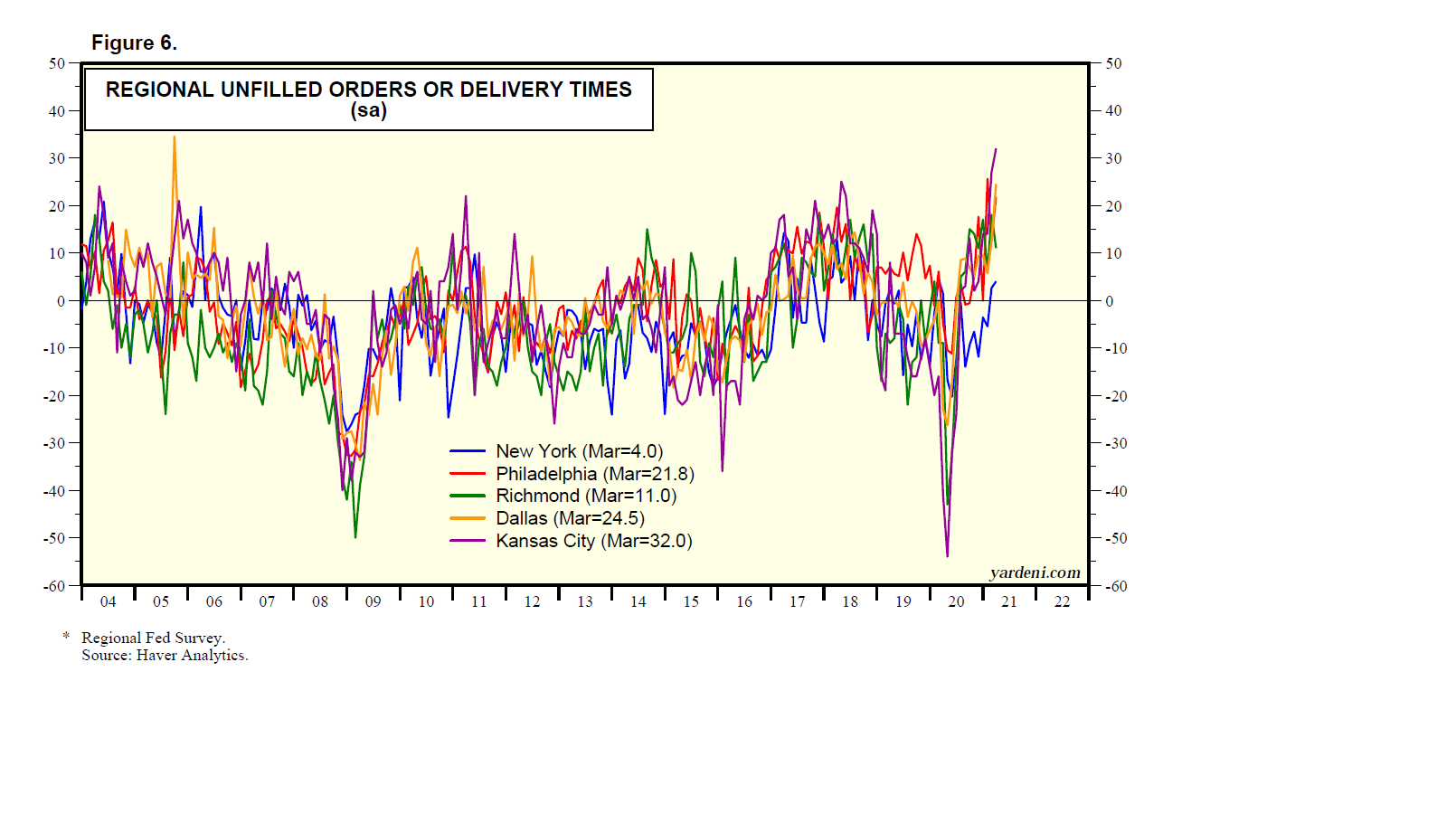

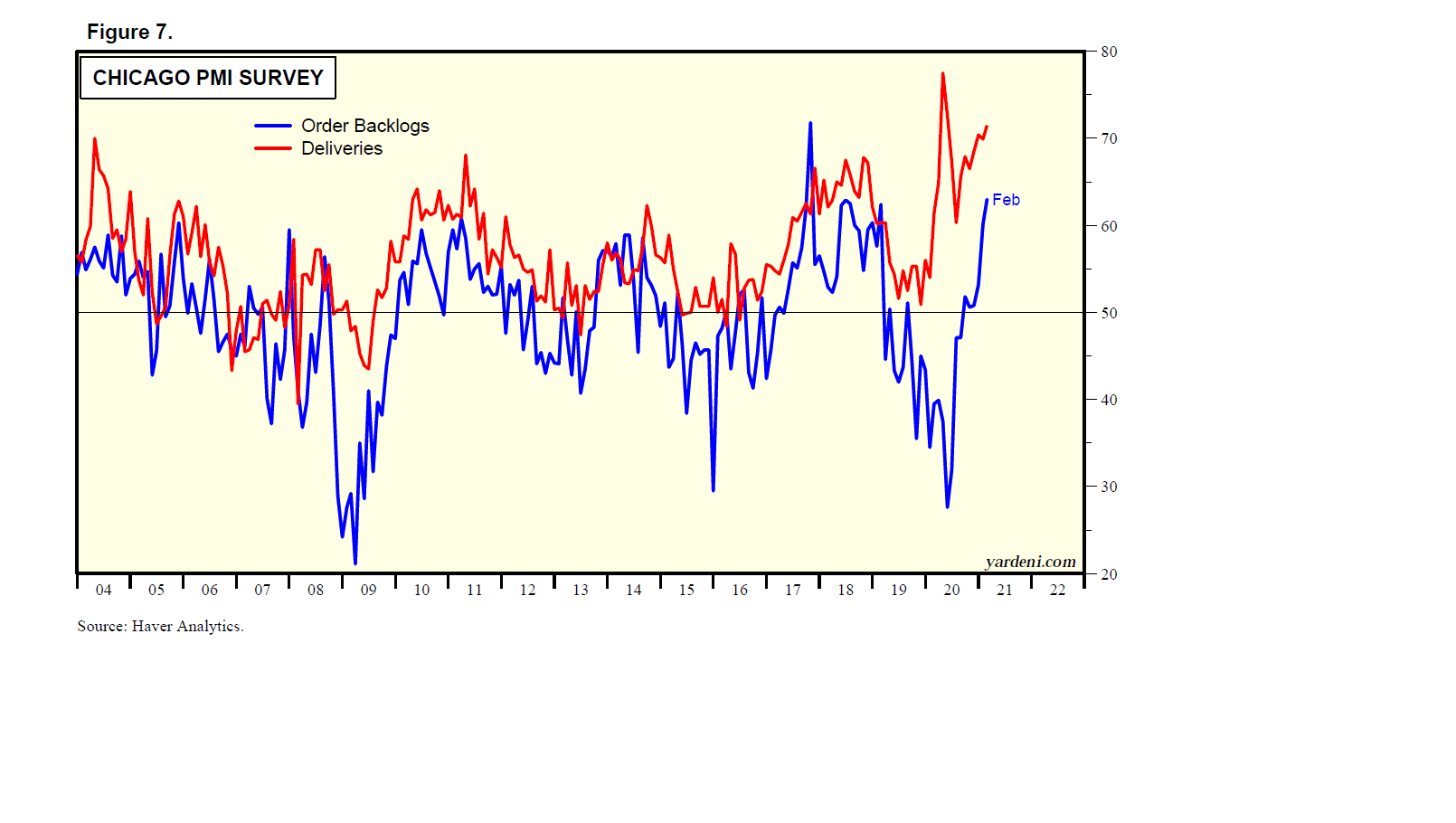

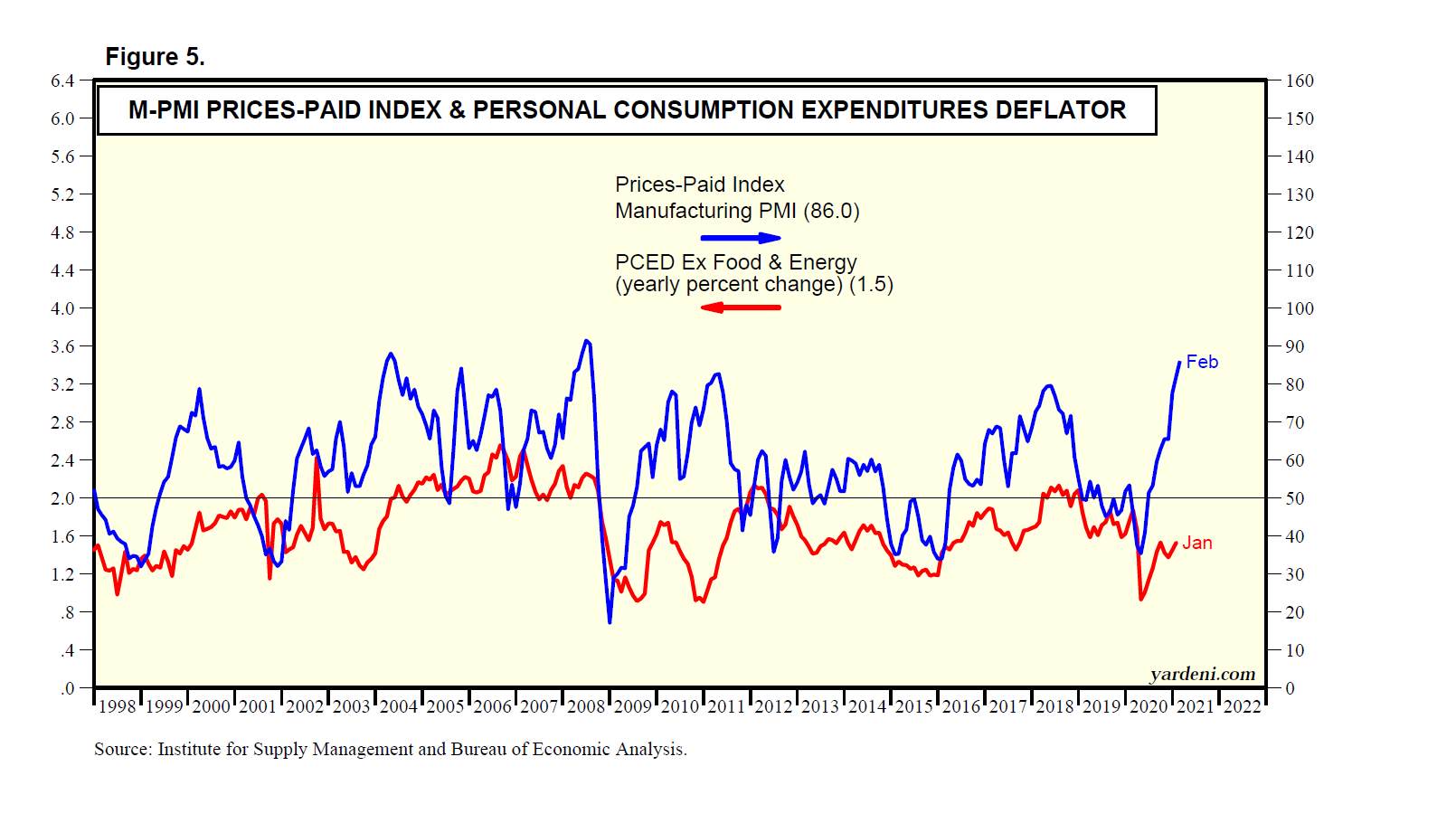

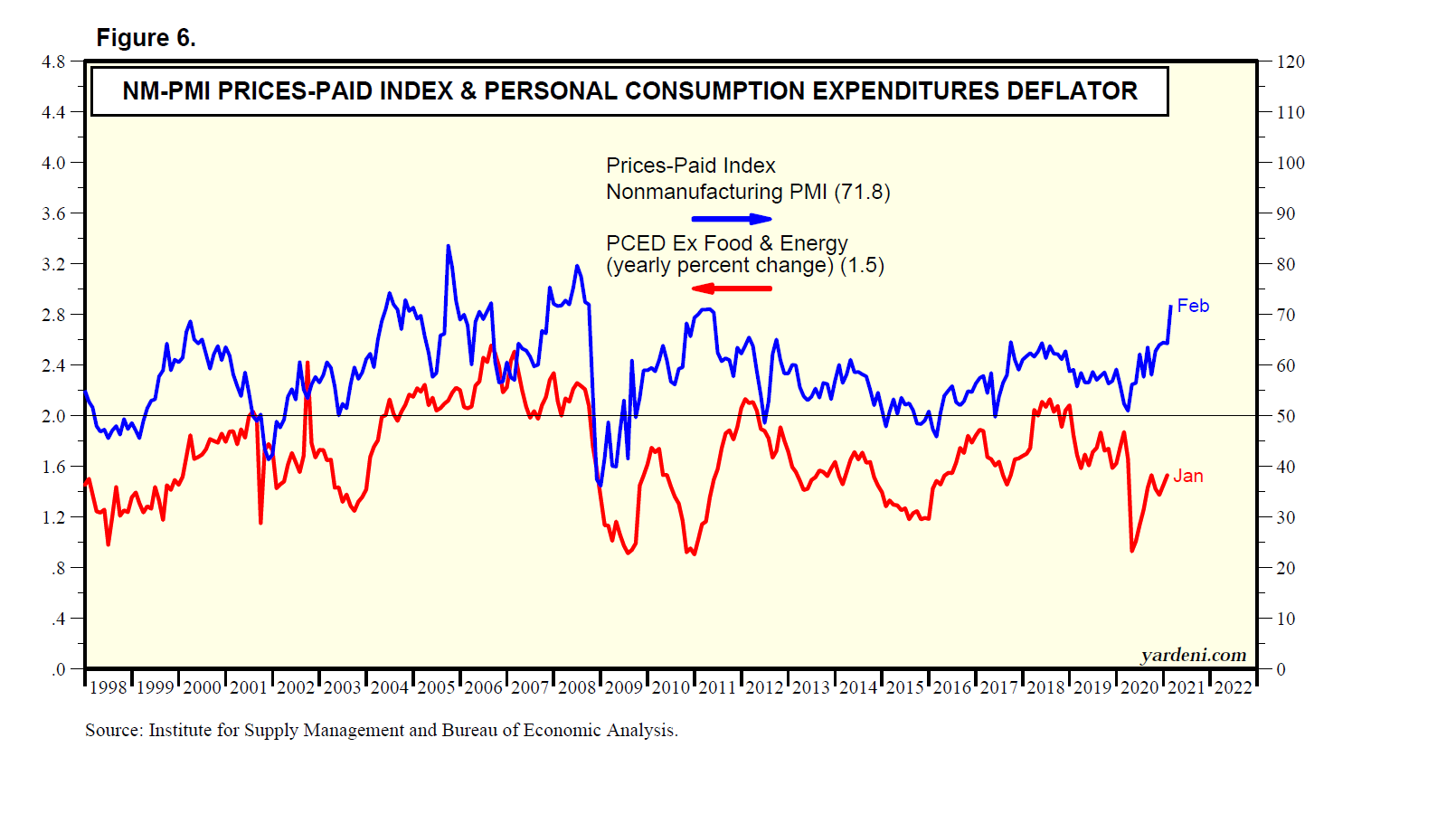

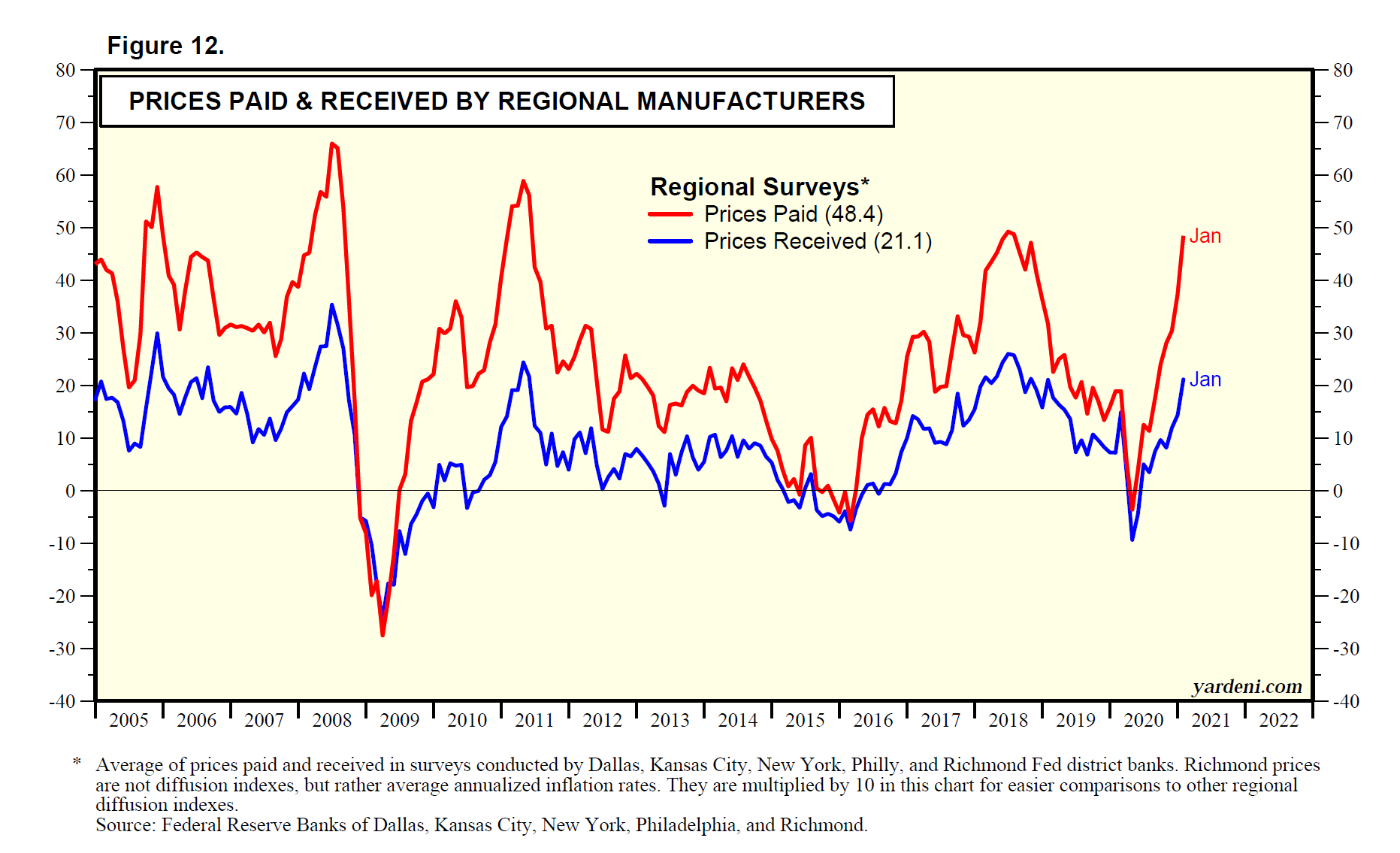

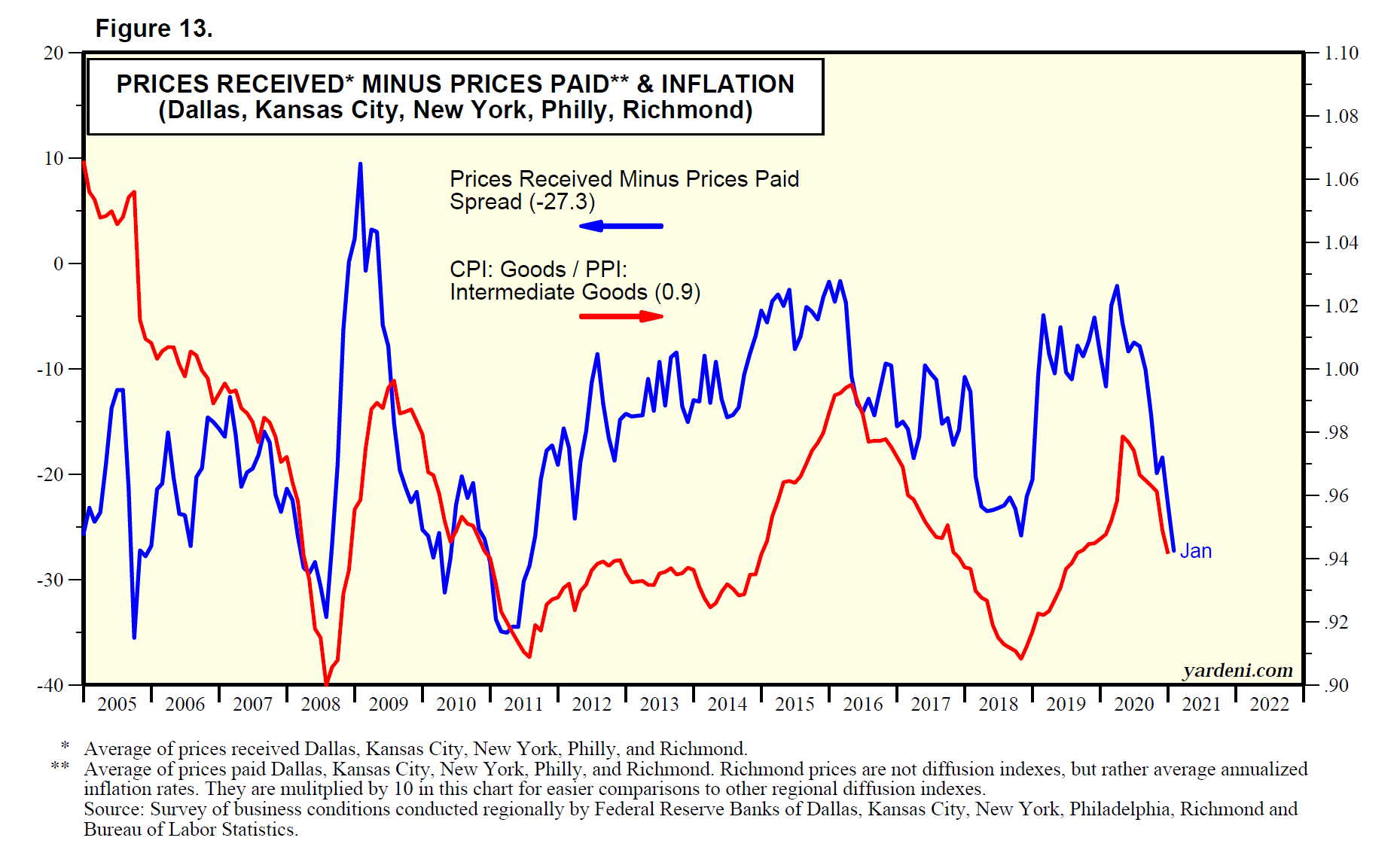

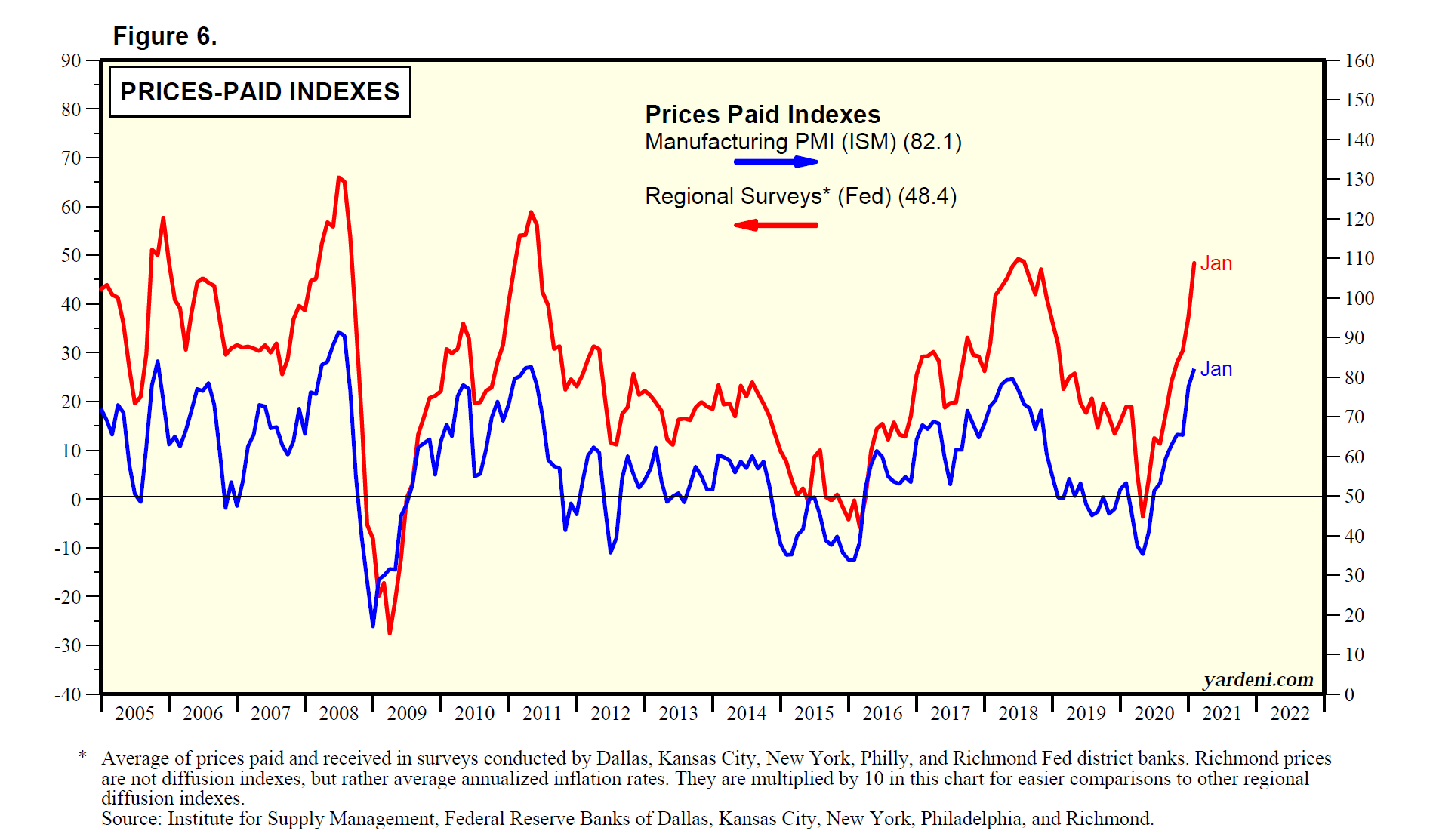

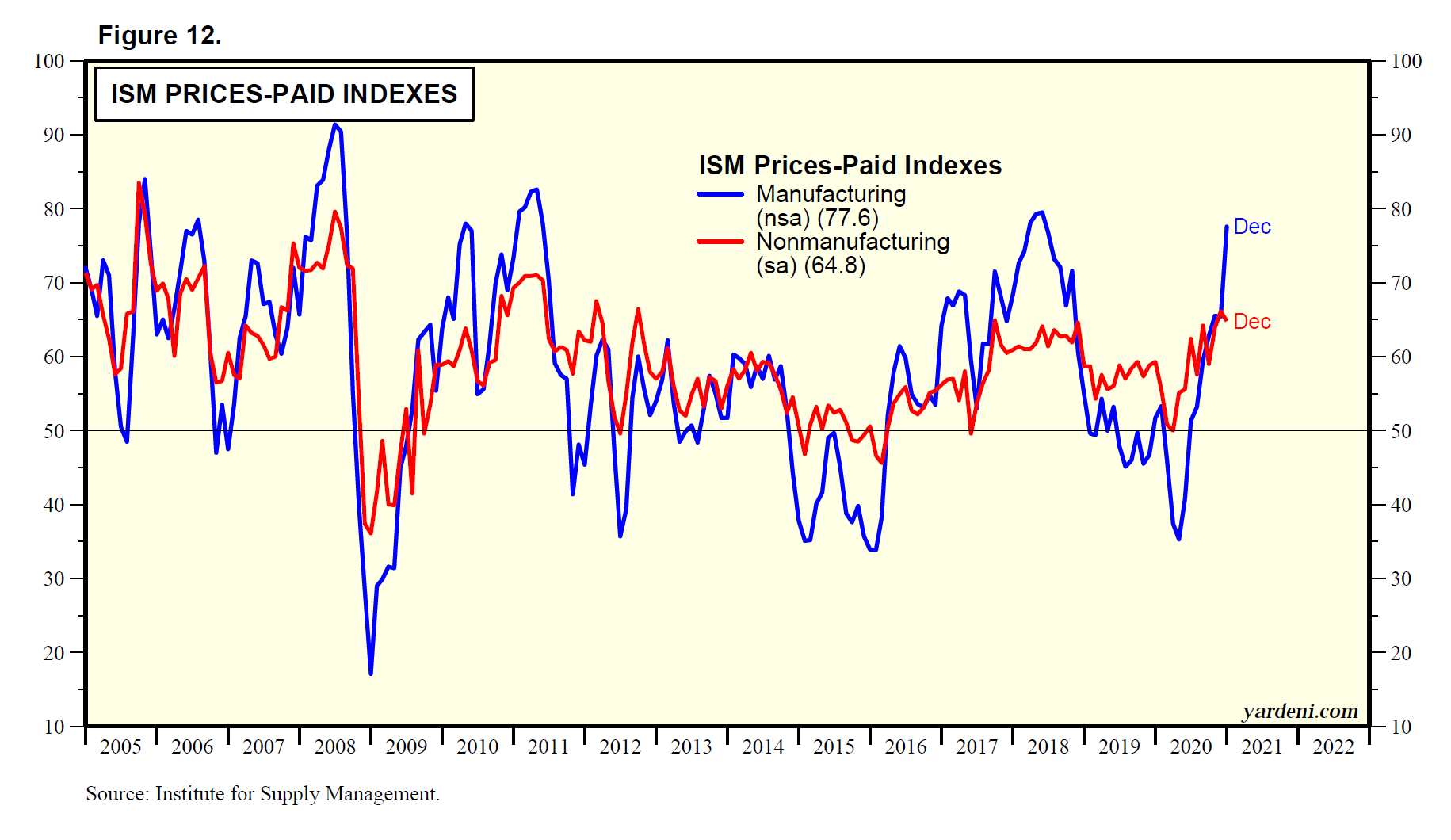

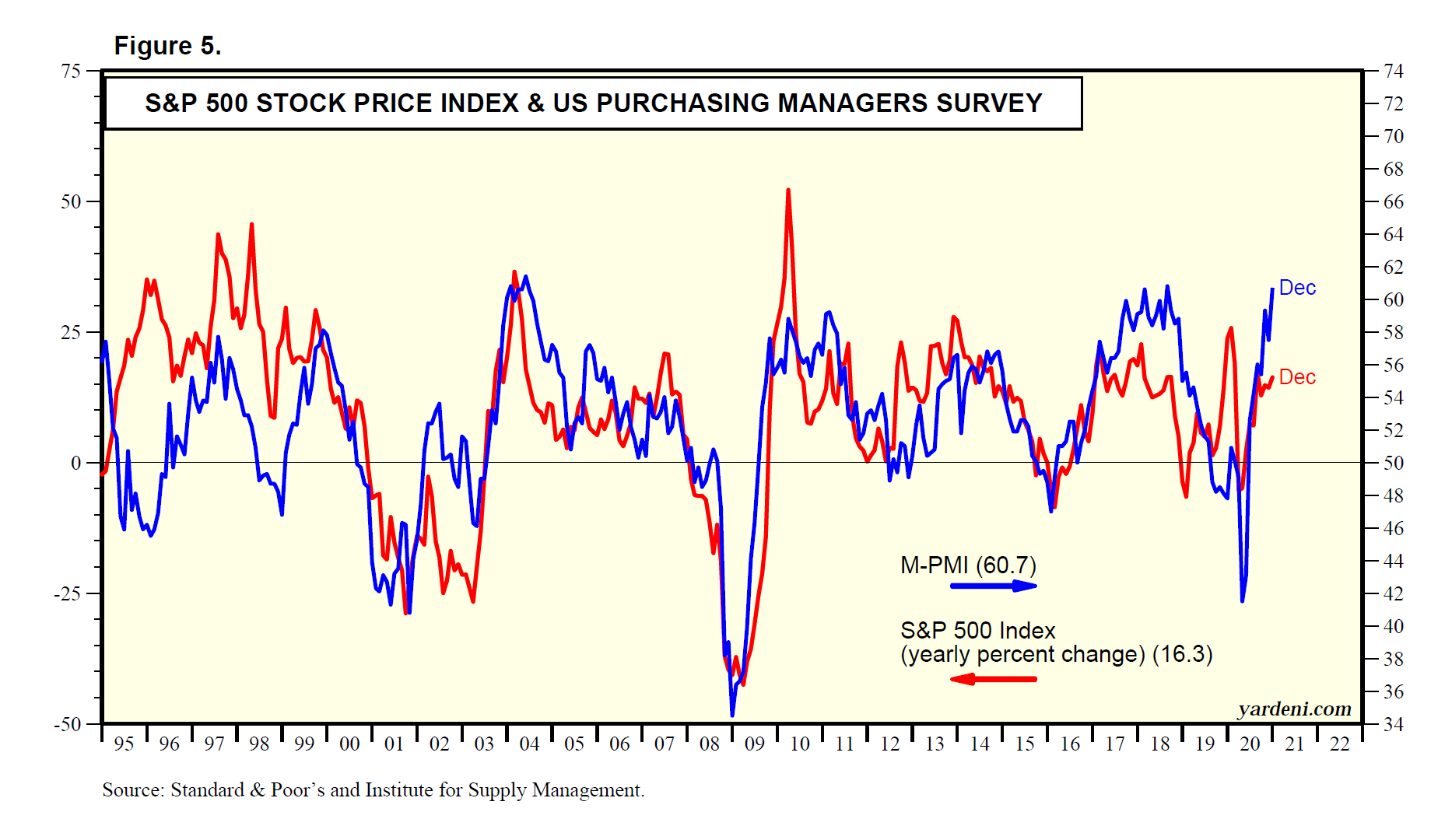

(1) Purchasing managers. The most recent survey of manufacturing purchasing managers showed that in recent months the new orders index has eased back toward the production index, with both at a robust reading of 61.5 (Fig. 13). The M-PMI supplier deliveries and backlog of orders remain elevated but continue to come down from their record highs during the early summer (Fig. 14). The M-PMI customer inventories index remains near recent record lows (Fig. 15).

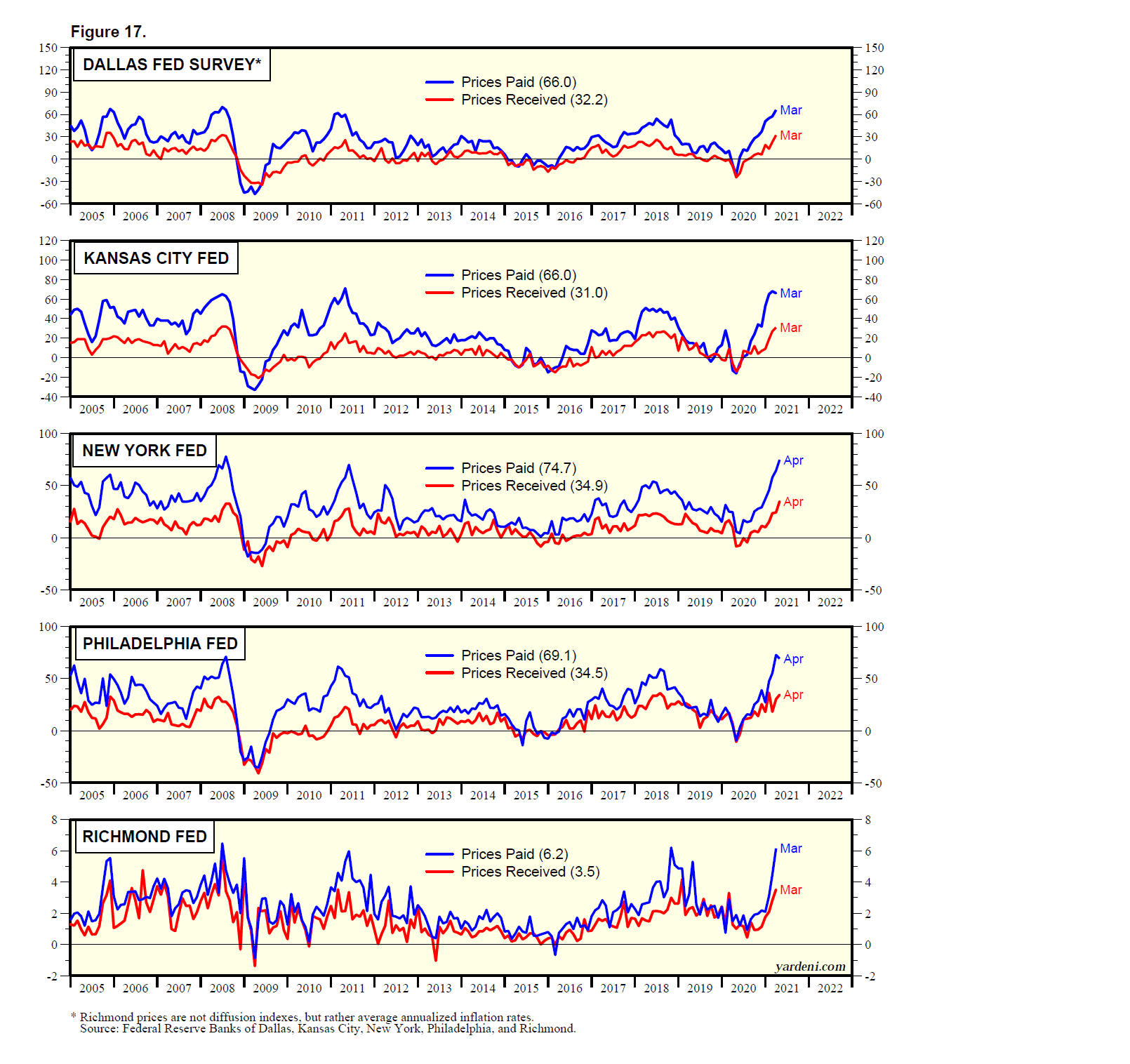

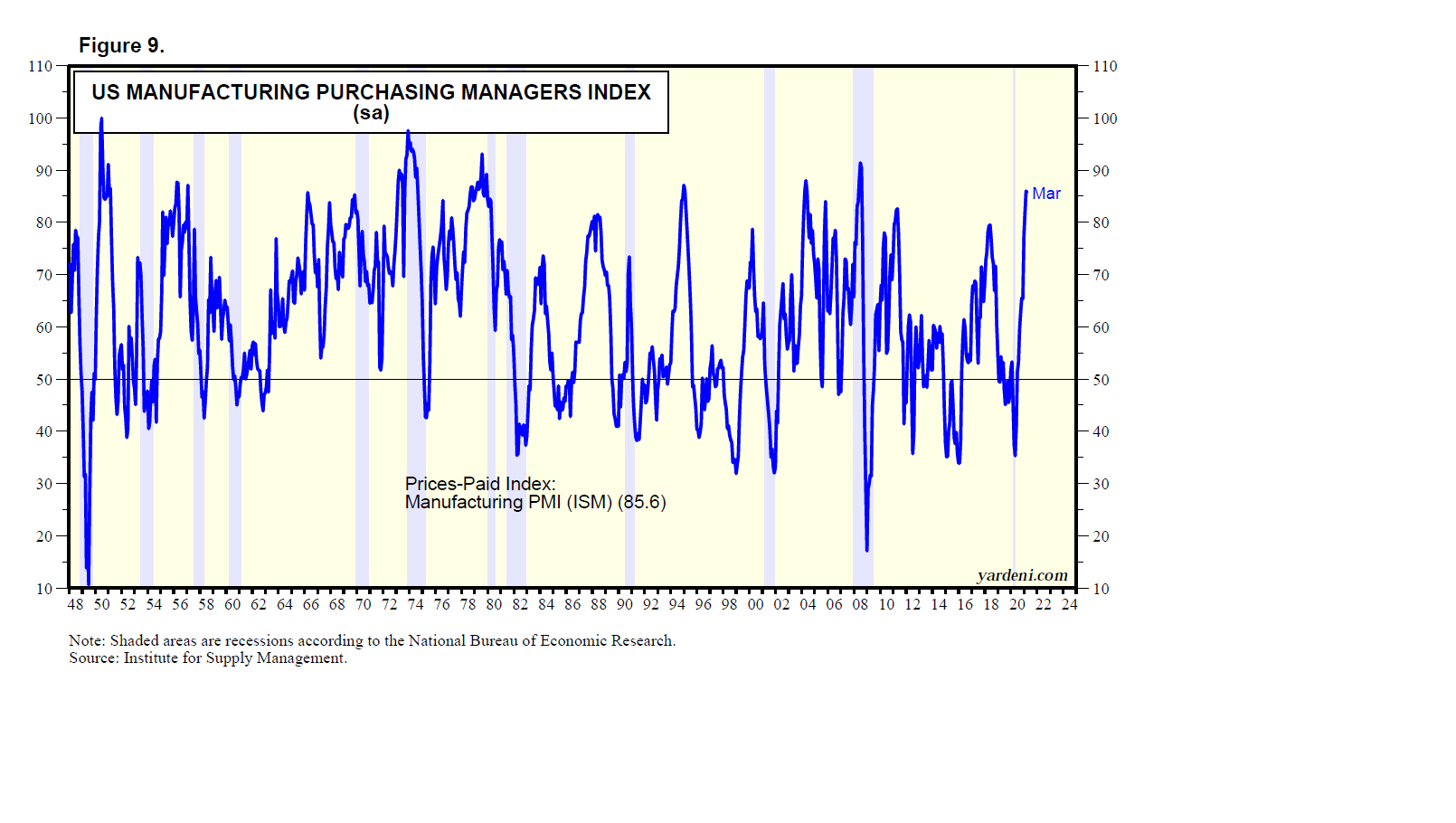

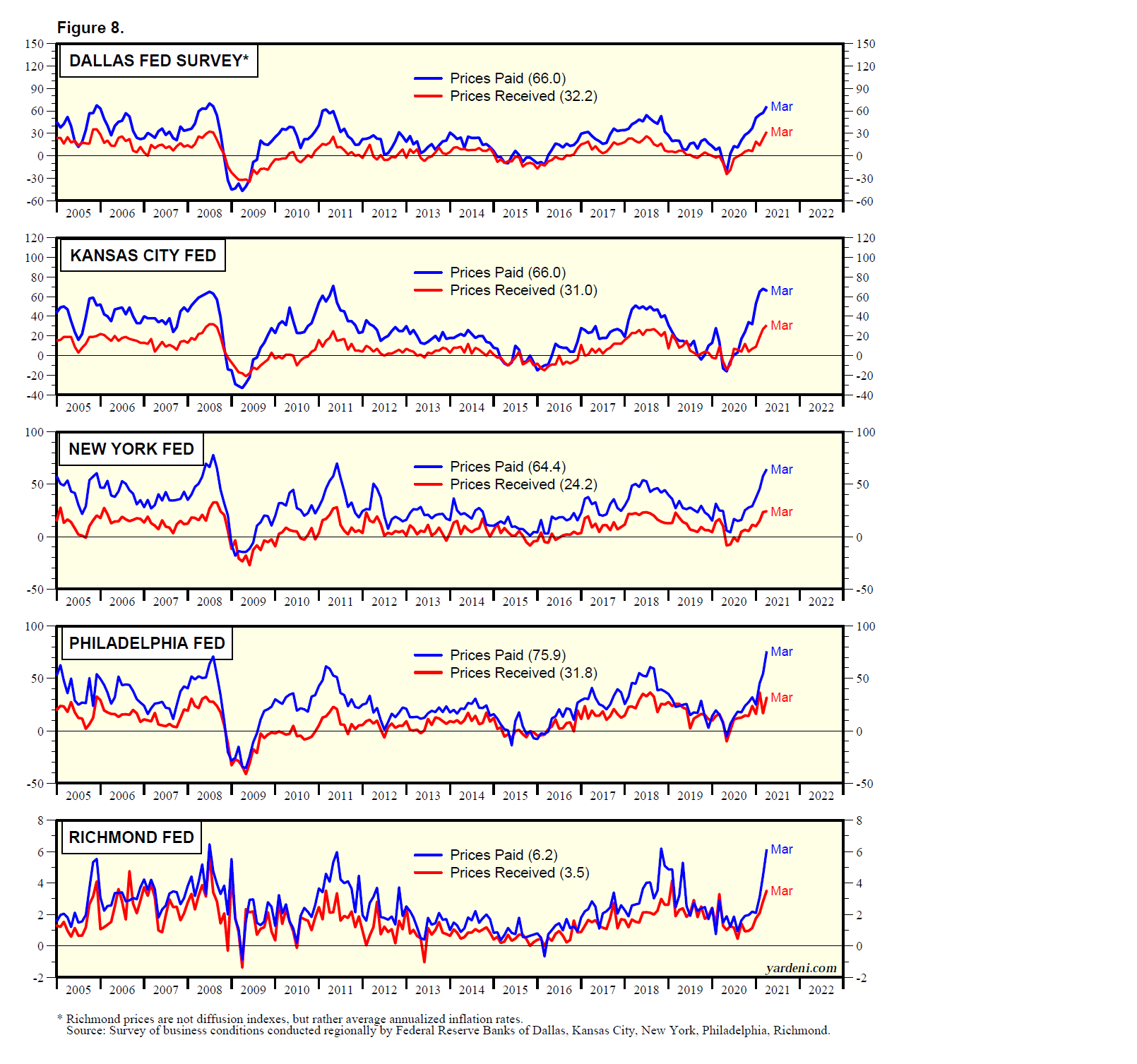

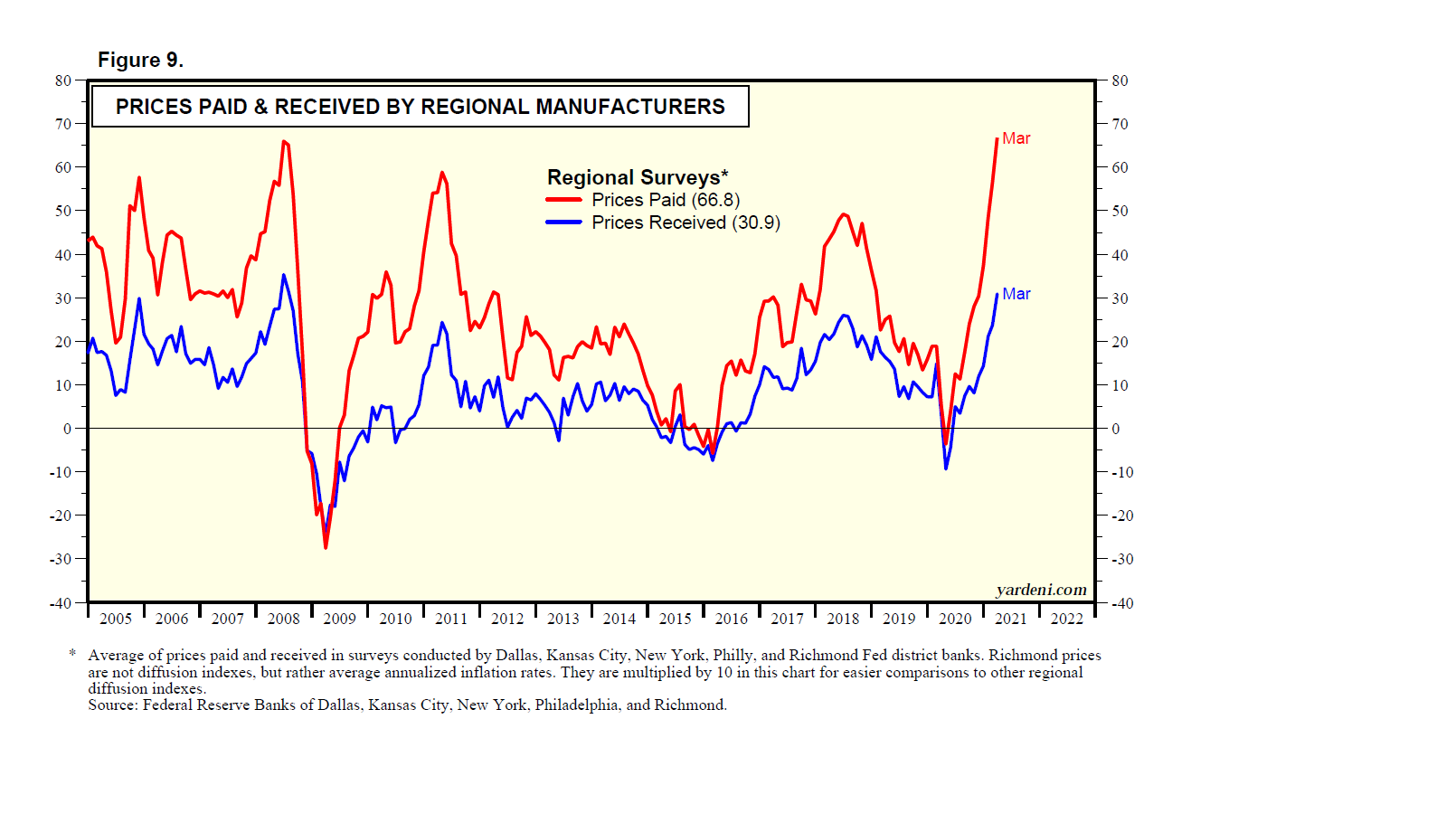

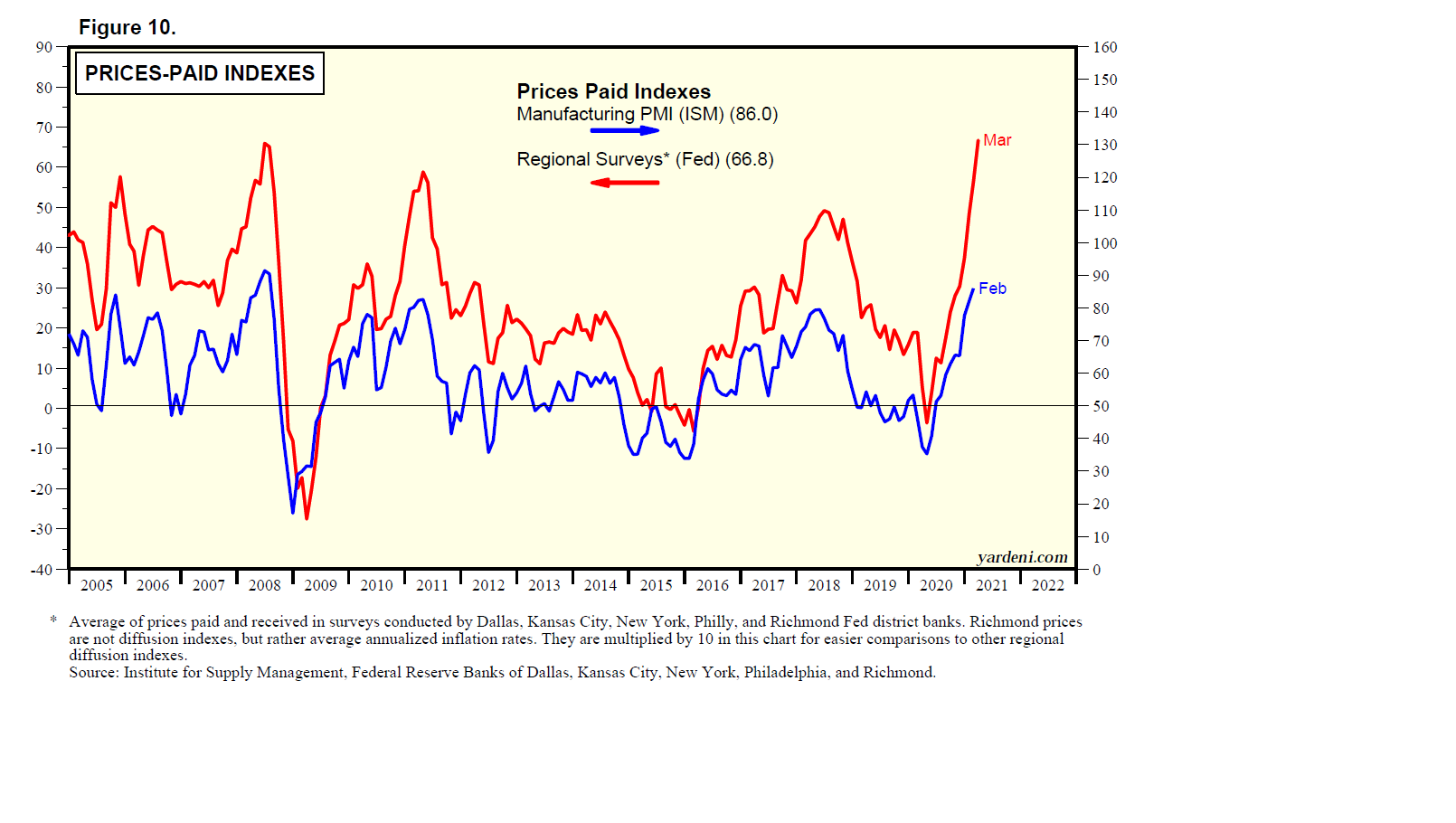

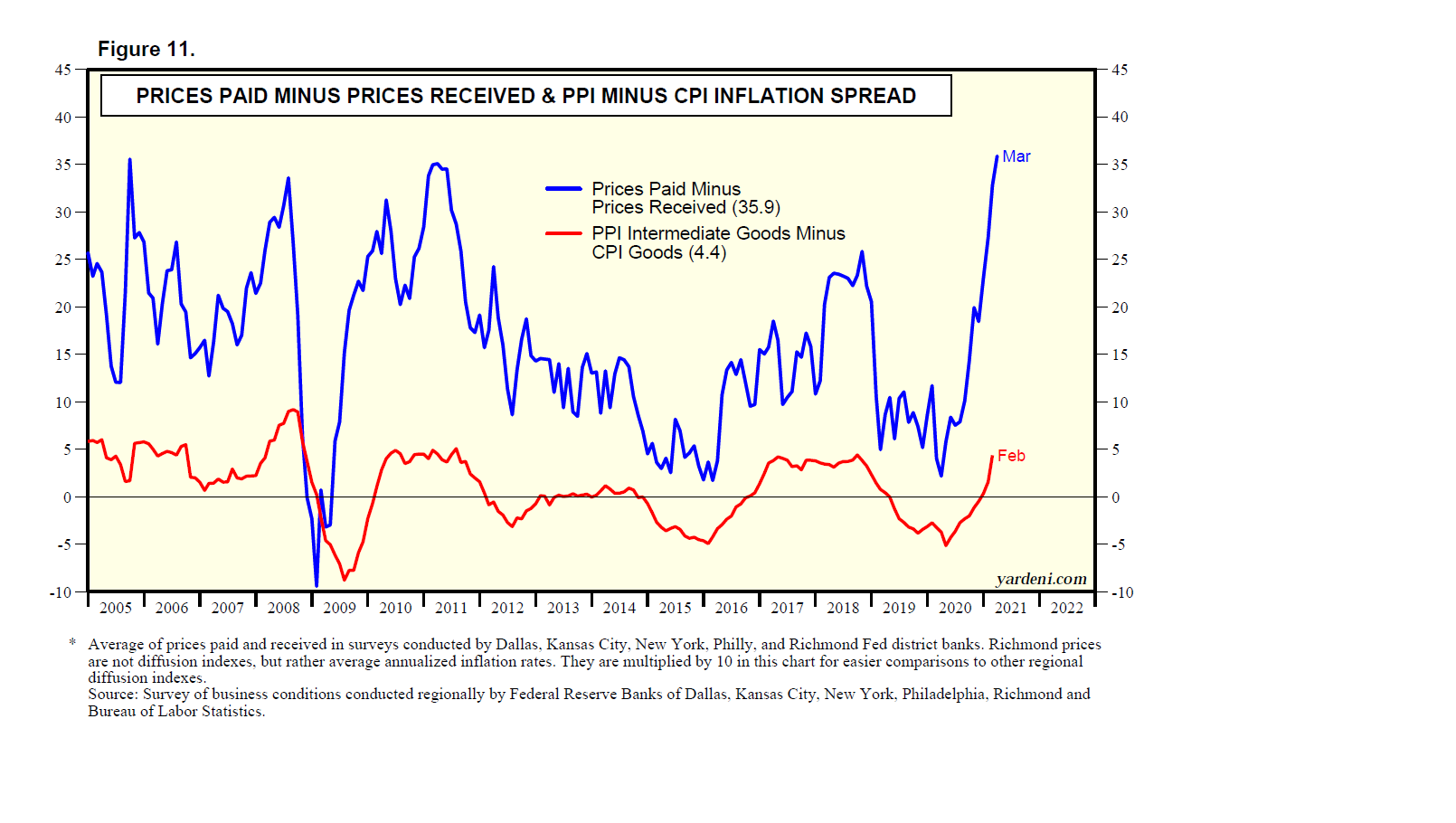

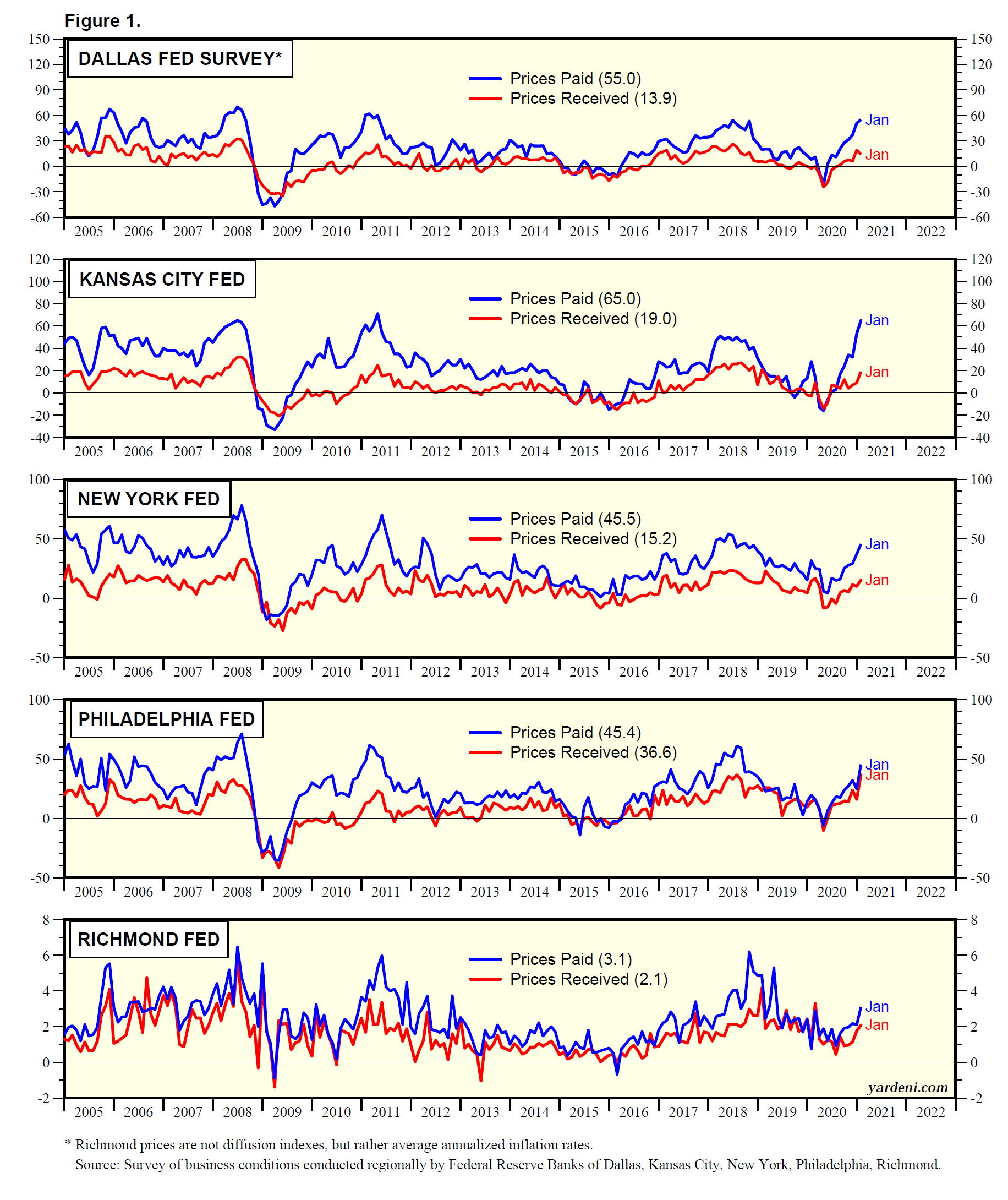

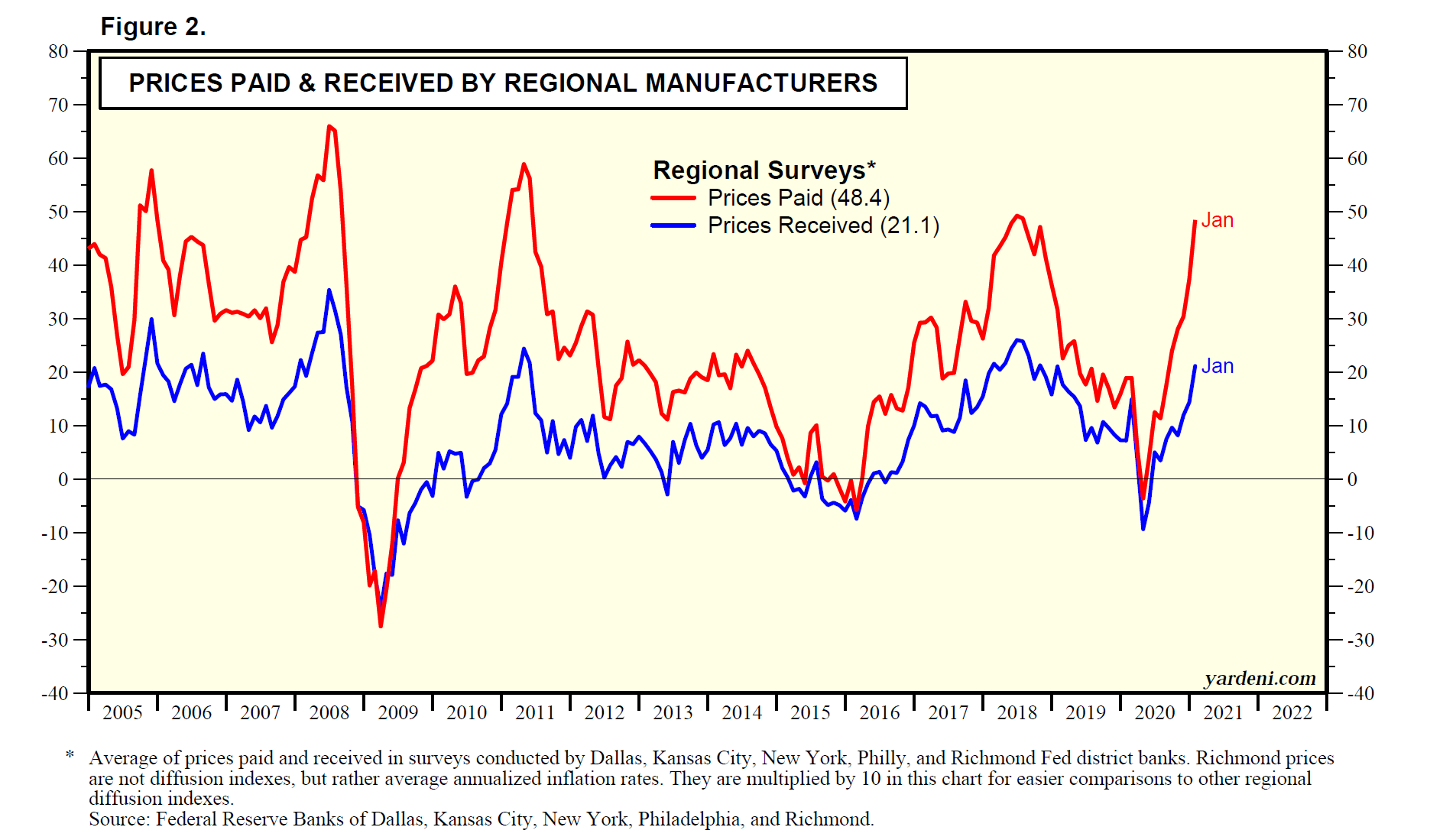

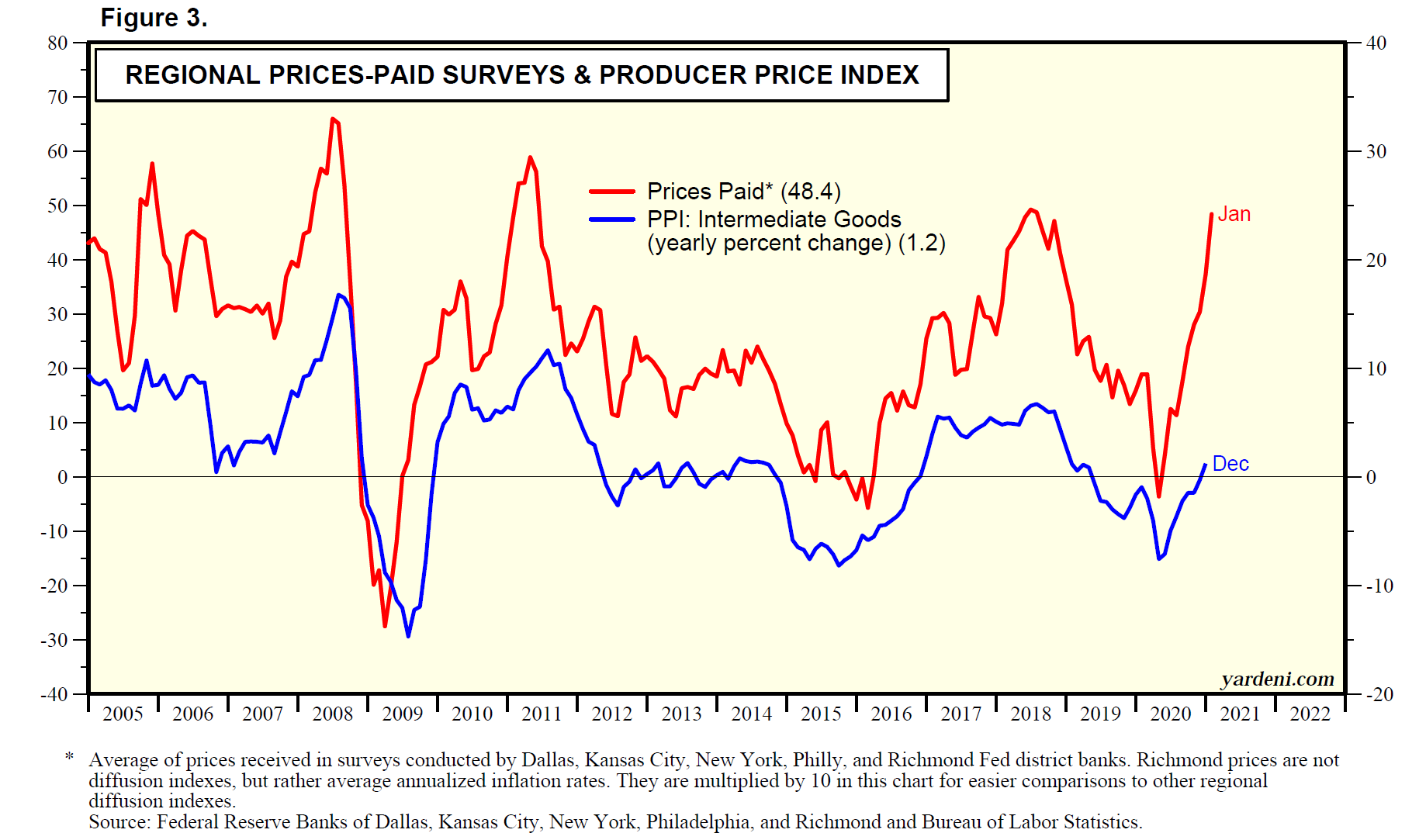

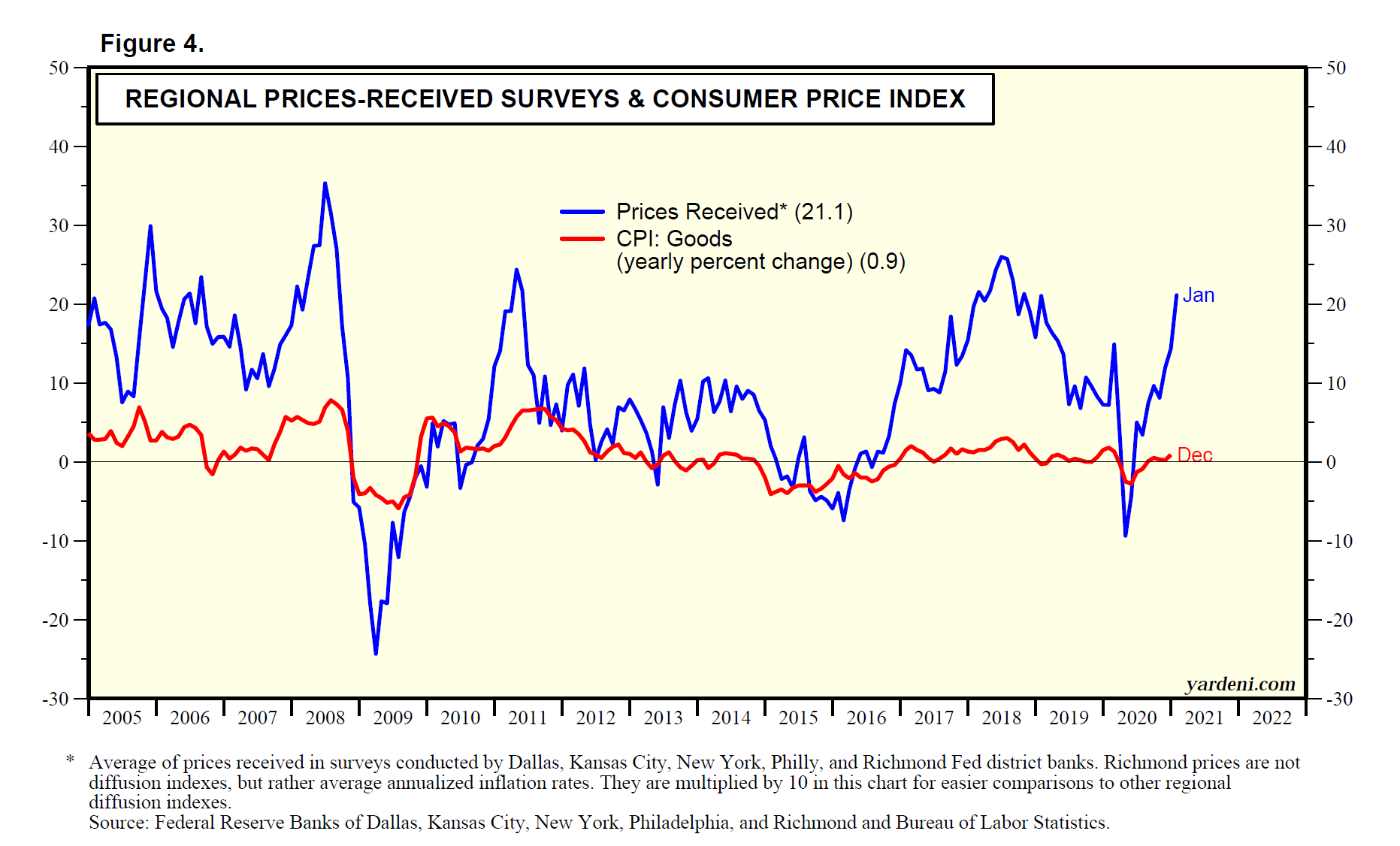

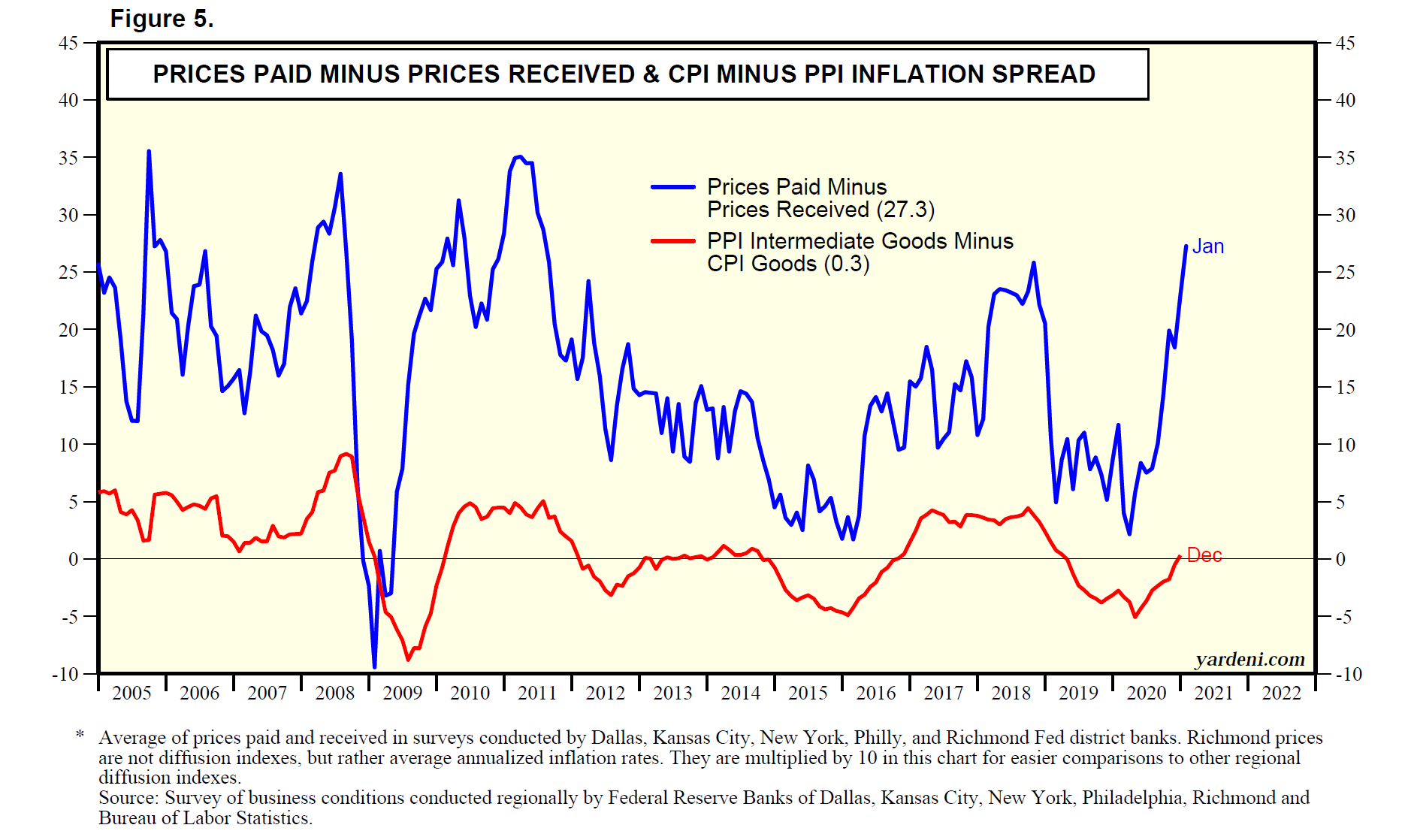

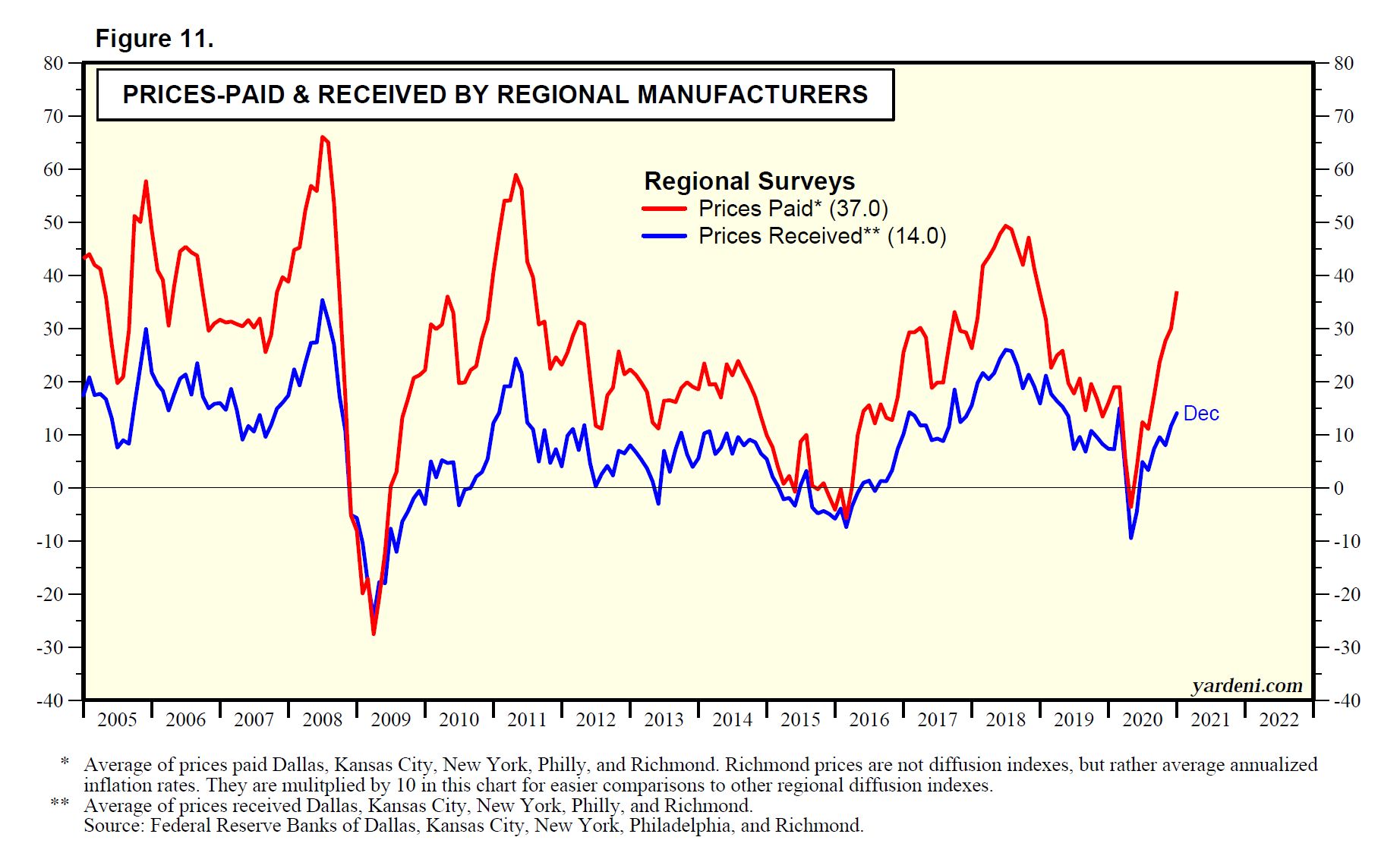

(2) Regional business surveys. Like the M-PMI, indexes of unfilled orders or delivery times in the five regional business surveys conducted by Federal Reserve Banks also remain elevated during November but down from recent highs (Fig. 16). Price pressures remain intense, with the prices-paid measure of the five districts at a new record high in November, while the prices-received measure held at record highs (Fig. 17).

Global Supply Chains III: How it Ends. Only time can fix the supply chain is the conclusion of logistics expert Michael Rentz in a December 6 essay for Law & Liberty. He says supply chains won’t normalize until demand finally tapers. Until then, the industry will be playing catch-up. “The system itself is overstressed. It is being asked to perform beyond its capacity with extreme constraints on space, equipment, and labor,” he says.

“What happened in 2020 was that the industry as a whole reduced capacity and shut down at the beginning of the pandemic. When the massive demand hit, the industry hadn’t started back up, and the capacity was already gone. The industry transitioned from a ‘Just-in-Time’ methodology to a ‘Just-in-Case’ one,” he writes. As a result, the Bullwhip Effect took place: Retailers realized that consumers were buying more goods than ever, so “they placed more orders than ever with wholesalers. When wholesalers received more orders than ever from retailers, they placed even more orders than ever with manufacturers.”

Suppliers couldn’t handle these unanticipated demand surges, Rentz explains, because supply-chain systems haven’t changed much since the container was invented in the mid-1950s. Consumer expectations have increased exponentially in all industries, but the supply chains in place to meet them have remained brittle.

Melissa and I think that problem is the reason that big money has been swooping in to revamp supply-chain systems with technology.

A December 2 article in Freight Waves was titled “Supply chain tech VC investment exceeds $7B for 3rd straight quarter.” That number—which is solely for the US and Europe—has dropped since a peak during Q1 but is still up more than 100% y/y. The article noted that median late-stage rounds are 94% larger compared to 2020. “At the same time that more capital is flowing to bigger companies, earlier-stage categories like drone logistics, augmented reality tech for warehousing, and ultrafast delivery are being populated with waves of new entrants.”

There’s another bright spot in the supply-chain story. As we wrote in our October 27 Morning Briefing, Amazon deliveries never skipped a beat as the rest of the world’s supply chains were shutting down. Why is that? A December 4 CNBC article explores how Amazon basically took control of its own supply network by “making its own containers and bypassing supply chain chaos with chartered ships and long-haul planes.”

Not unusually, Amazon started a trend: “This season, a handful of other major retailers—Walmart, Costco, Home Depot, Ikea and Target—are also chartering their own vessels to bypass the busiest ports and get their goods unloaded sooner.”

These trends are hopeful signs that broken supply chains will be fixed at some point with help from technology investment and retailers’ taking tighter control over the journey goods take from manufacturer to consumer. When that might happen is far from certain, but the good news is that passively waiting for supply-chain disruptions to end isn’t the only solution.

Does Covid = Y2K For Earnings?

December 14 (Tuesday)

Check out the accompanying pdf and chart collection.

(1) Technicians don’t like what they see in Nasdaq. (2) A replay of Y2K boom and bust for tech as a result of Covid? (3) Scramble to boost productivity should offset less pandemic-related tech demand. (4) Nasdaq 100 beating Nasdaq composite (2,500+ stocks). (5) S&P 500/400/600 Information Technology having a good year. (6) Mag-8 are in both S&P 500 and Nasdaq 100. (7) Mag-8 accounts for more than a quarter of S&P 500 market cap and is trading at a forward P/E of 34.8 on a free-float basis. (8) S&P 500 profit margins probably peaked during Q2 but should stay high, especially ex-Financials. (9) Lots of solid revenues and earnings growth rates among S&P 500 sectors.

Reminder. Check out a replay of Dr. Ed’s latest Monday morning webinar here.

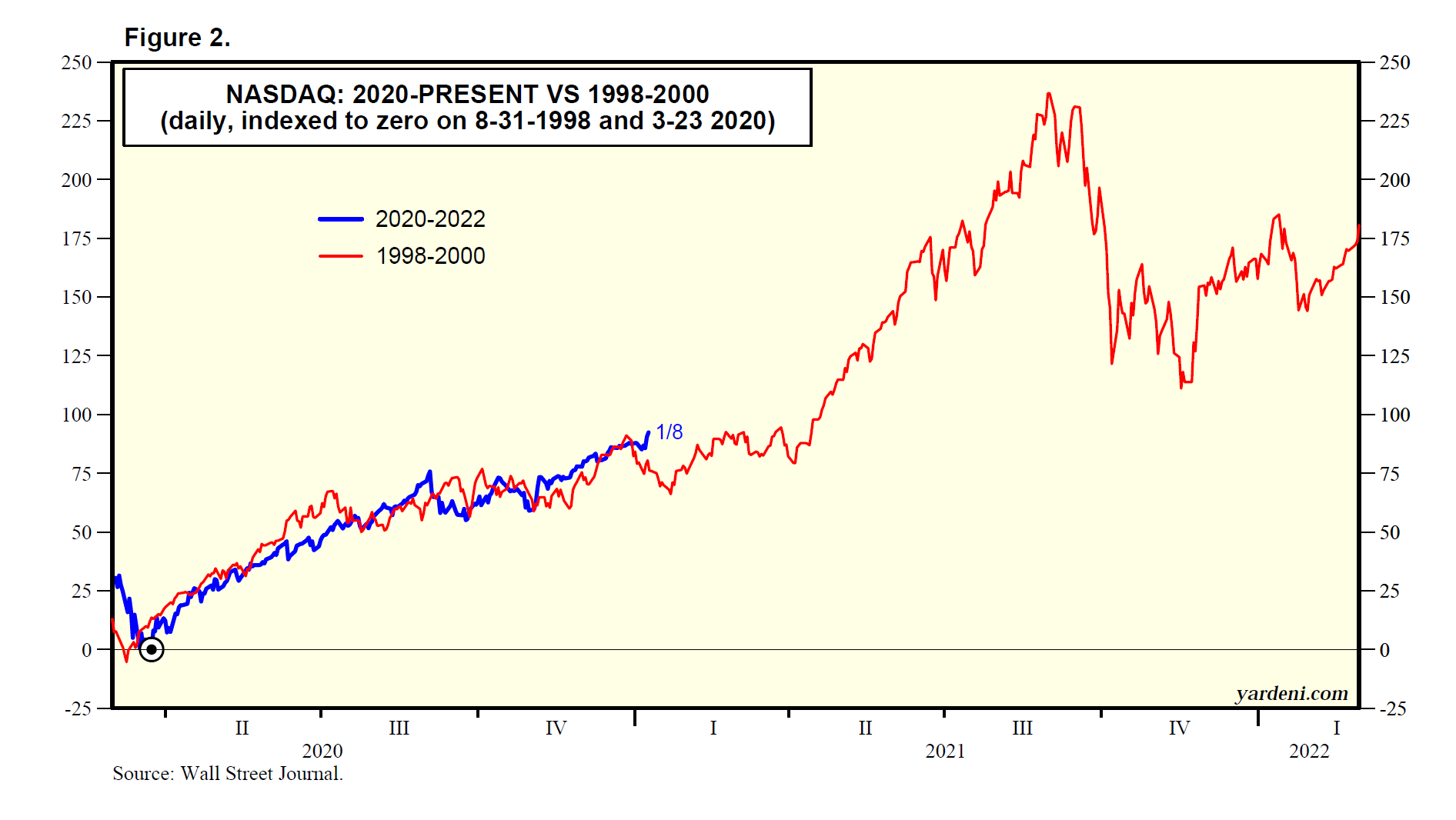

Strategy I: Nasdaq Has Bad Breadth. It has been widely reported that the Nasdaq’s technical picture has been deteriorating in recent weeks, with most of the index’s gains coming from just a handful of large-capitalization stocks. Some technical analysts see a similarity to the tech bubble of the late 1990s. A few have asked rhetorically whether Microsoft might be today’s Cisco. They warn that the Nasdaq’s technical deterioration could spell trouble for the broad stock market.

Joe and I disagree. We believe that the broad market as measured by the S&P 500 and Nasdaq 100 will continue to rally through at least 2022. However, we agree that certain areas of the Nasdaq that are already in a bear market may remain depressed through next year. That’s because the Nasdaq includes lots of unprofitable small tech and biotech companies that might have been viewed as pandemic plays and not very many that are viewed as re-opening ones.

During the late 1990s, technology companies received big earnings boosts from the widespread scramble to avert the Y2K problem by spending more on new technology hardware, communication equipment, and software. As a result, during the year 2000 such spending fell, sharply depressing tech earnings and stock prices.

Joe believes that the boom in tech spending during 2020 and 2021 in response to the pandemic might be followed by surprising weakness in earnings in 2022, whether the pandemic abates or we continue to live with it. That’s a good point and might explain why many Nasdaq stocks that attracted investors from the onset of the pandemic might now be stumbling as the prospects ahead look less propitious for them.

However, I believe that technology businesses will get an even bigger boost in their sales and earnings from companies that are scrambling to increase their productivity in the face of chronic labor shortages. By the way, the Nasdaq composite is up more than threefold from its 1999 peak. That’s mostly because Nasdaq companies are more profitable than ever, especially the larger ones.

Let’s take a deeper dive into this issue:

(1) Different strokes for different stock indexes. As we observed yesterday, the S&P 500 bottomed on December 1 at 4513.04, down 4.1% from its November 18 record high. On Friday, it was back up to a new record high of 4712.02 (Fig. 1). The equal weighted S&P 500 hit a record high on November 16 and subsequently declined 6.5% to its bottom on December 1. It’s still down 1.6% from its record, and has been underperforming the market-cap weighted S&P 500 since June 3 (Fig. 2).

The Nasdaq includes over 3,600 stocks currently (Fig. 3). This index hit a record high on November 19. It was 2.7% below that peak on Friday after falling as much as 6.1% by December 3 from its record. The Nasdaq 100 hit a record high on November 19 and was still down 1.5% from that peak on Friday. On December 3, it had been down 5.2% from its record. The Nasdaq price index relative to the Nasdaq 100 was at a record low again on Friday, and has been underperforming the Nasdaq 100 since March 12 (Fig. 4).

(2) Tech’s winners and losers. Admittedly, a wide swath of tech names has run into a buzz saw since March 2021, with some of the hottest names absolutely creamed. The ARKK Innovation ETF is a good proxy for those names—it’s down nearly 40% from the February top.

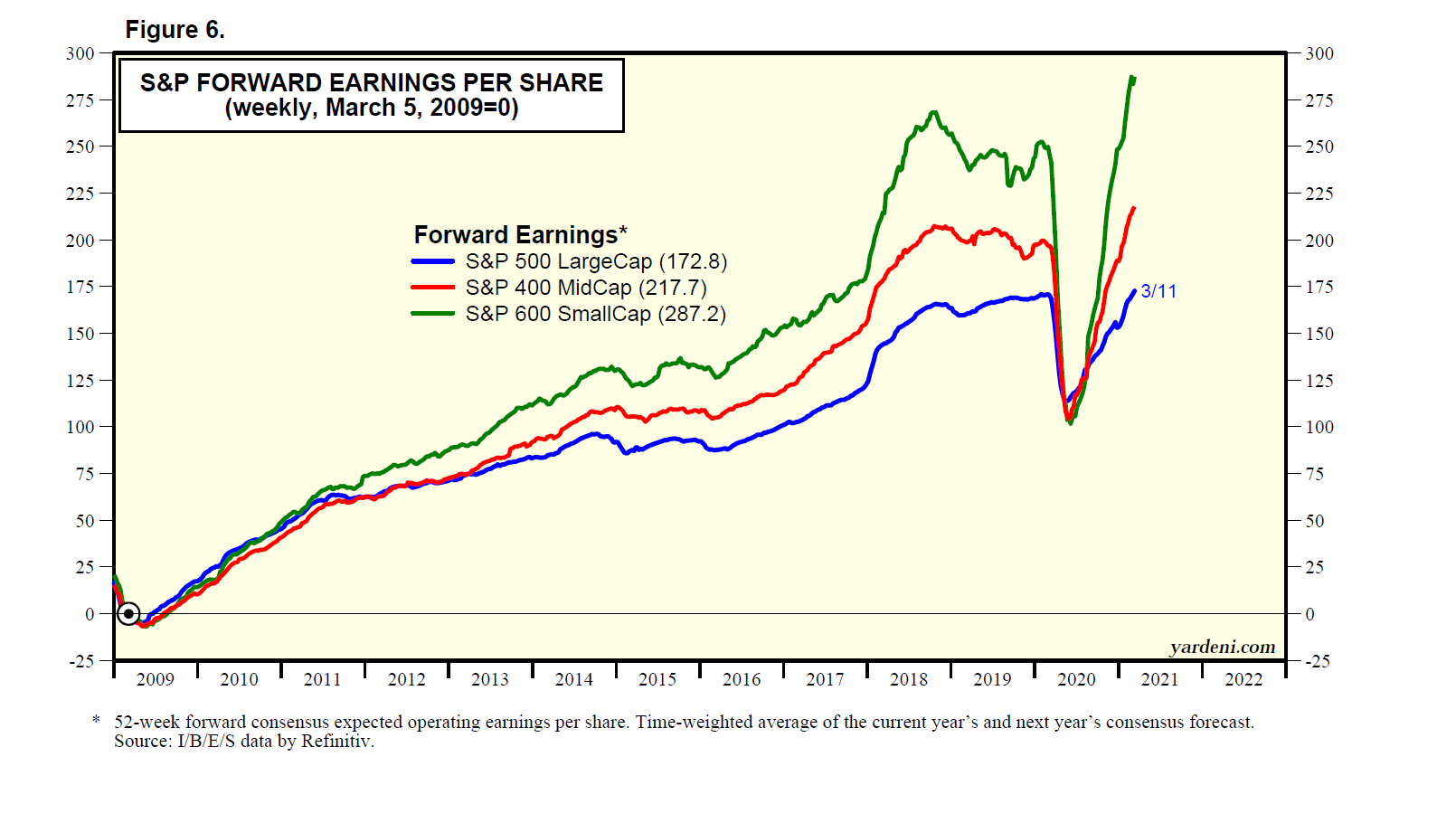

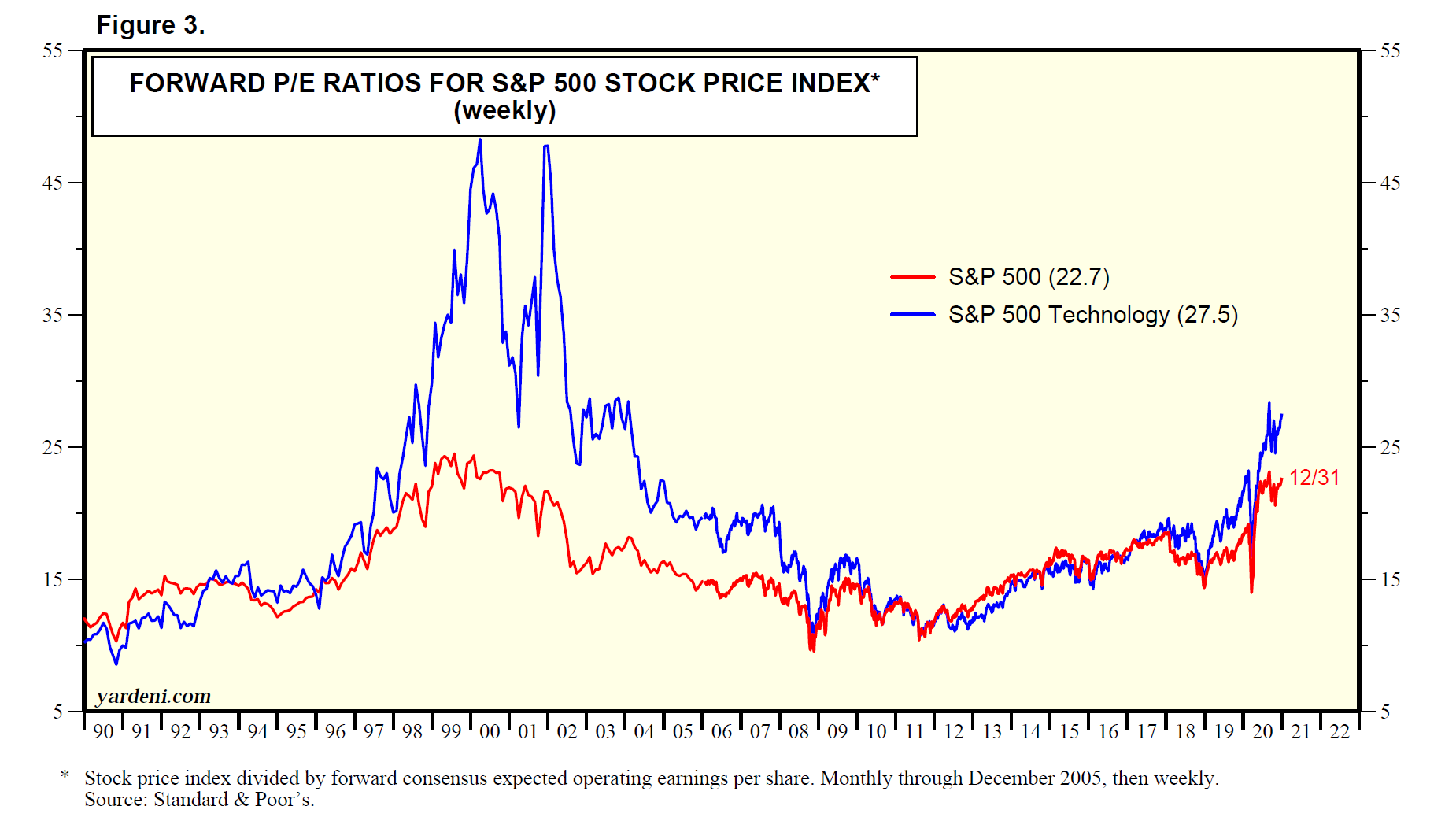

On the other hand, the S&P 500/400/600 Information Technology sectors are up 33.9%, 10.5%, and 22.8% ytd through Friday’s close (Fig. 5). The LargeCap sector rose to a new record high on Friday.

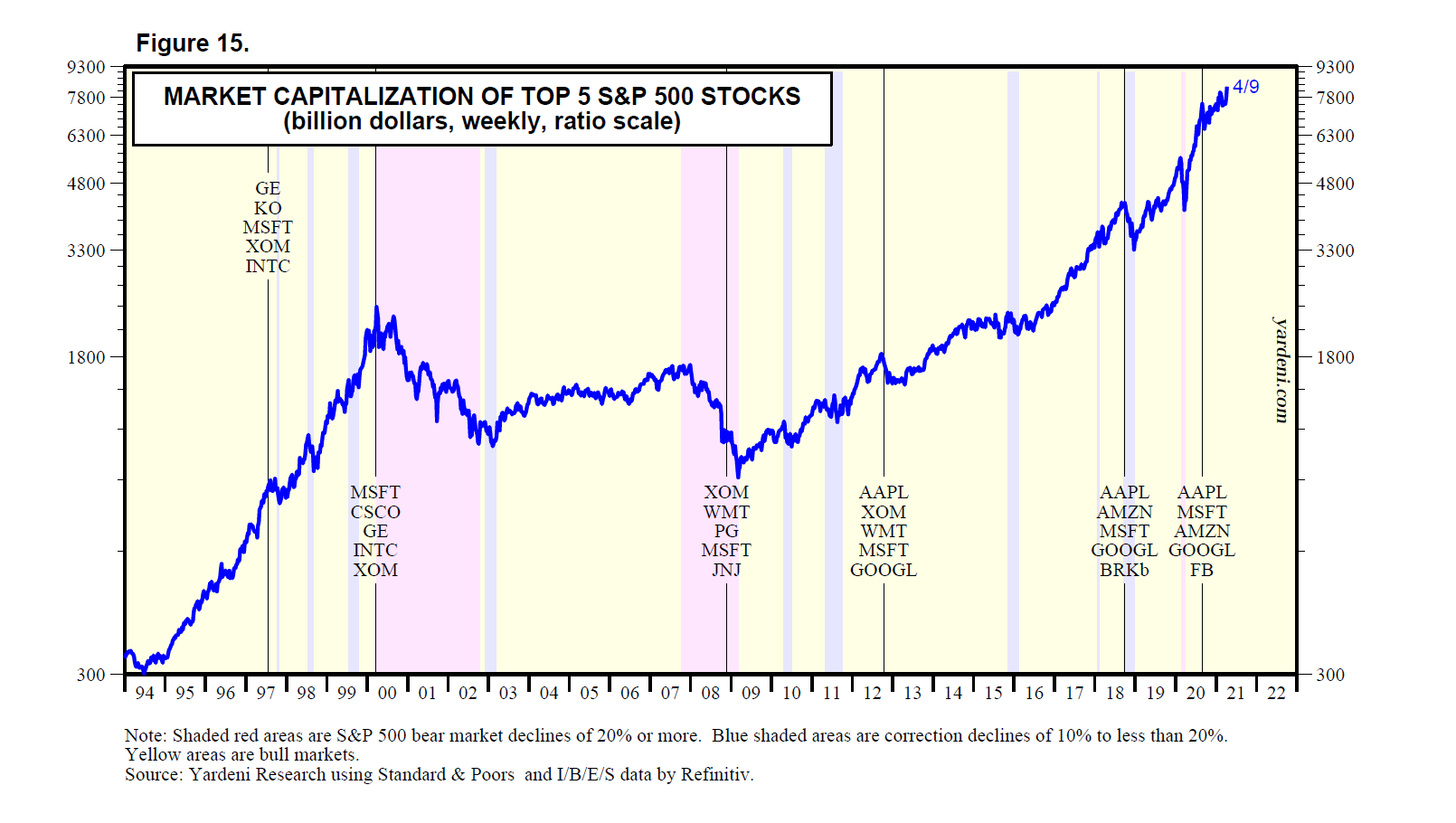

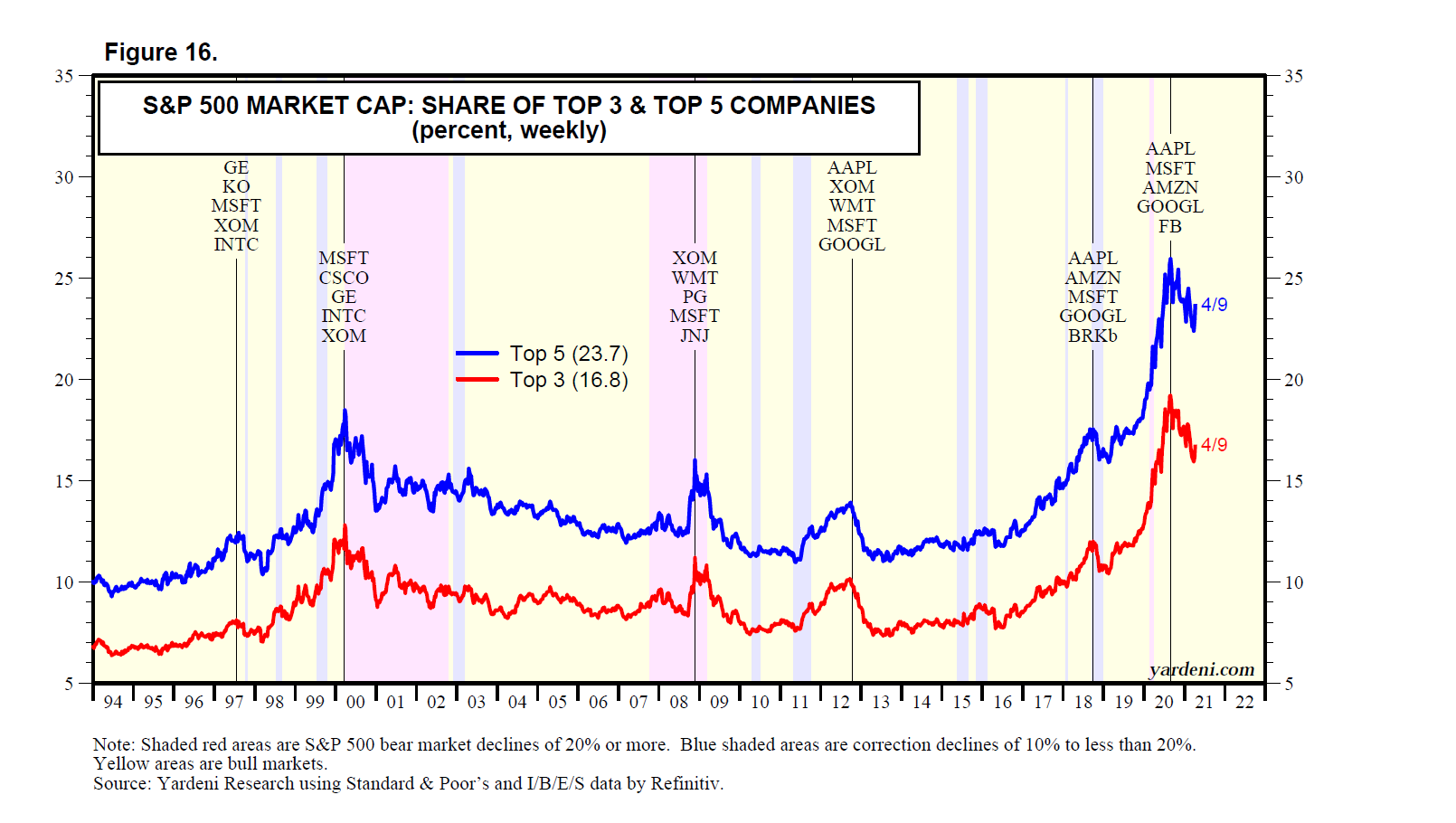

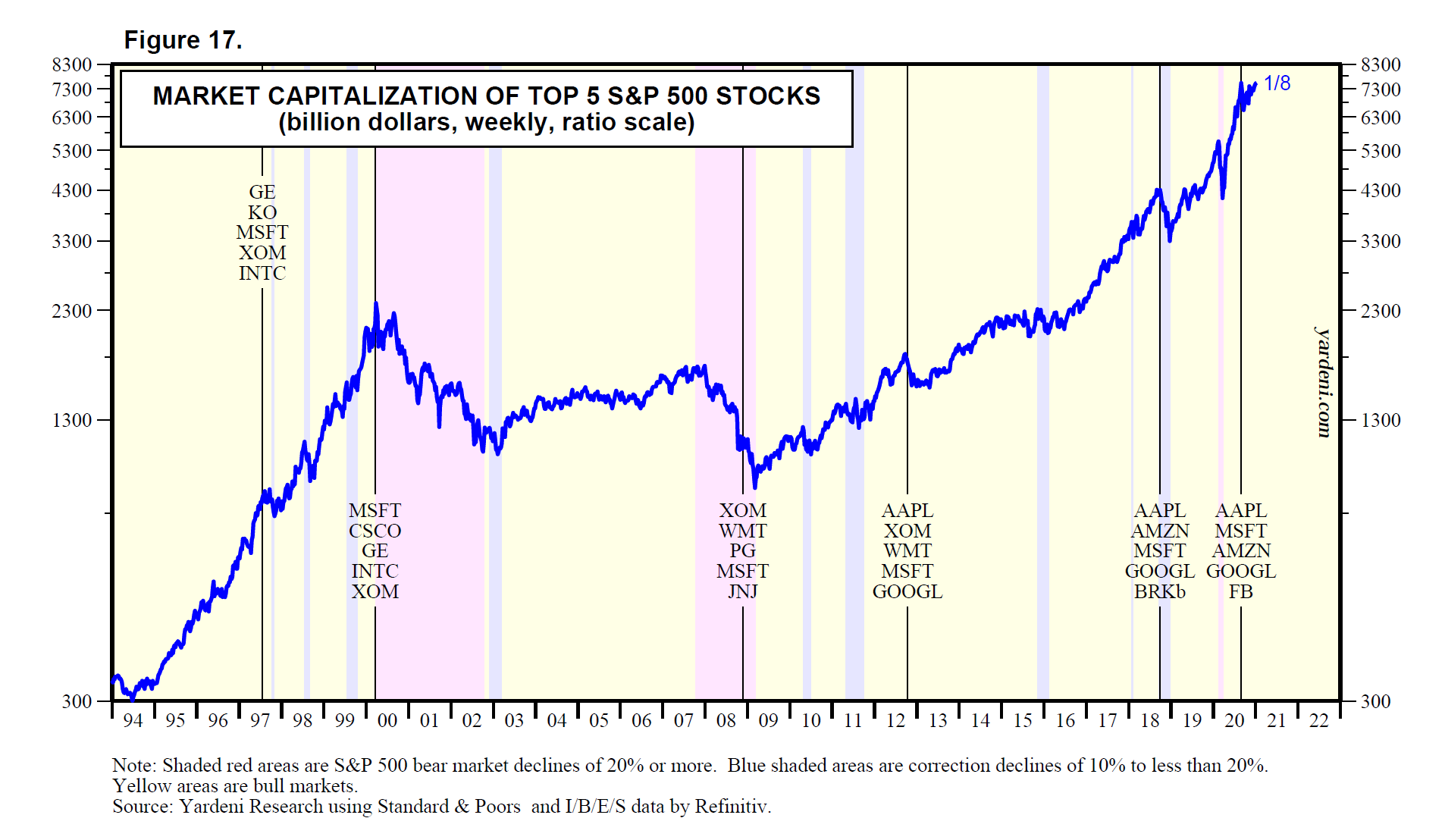

(3) The Magnificent 8. The Magnificent 8 represents Alphabet (Google), Amazon, Apple, Meta (Facebook), Microsoft, Netflix, NVIDIA, and Tesla. They are all in the S&P 500 and the Nasdaq 100. The Mag-8’s market-cap rose to $12.2 trillion on Friday, accounting for 26.3% of the market cap of the S&P 500 on a free-float basis (Fig. 6 and Fig. 7). On a ytd basis through Friday’s close, the former is up 38.7%, while the latter is up 25.5%. Excluding the Mag-8’s free-float market cap, the S&P 500’s market cap is up 22.4%.

The Mag-8’s collective forward P/E (i.e., based on forward earnings, which is the time weighted average of analysts’ consensus estimates for this year and next) was 34.8 on Friday (Fig. 8). Excluding the Mag-8, the forward P/E of the less magnificent 492 stocks in the S&P 500 is around 18.0.

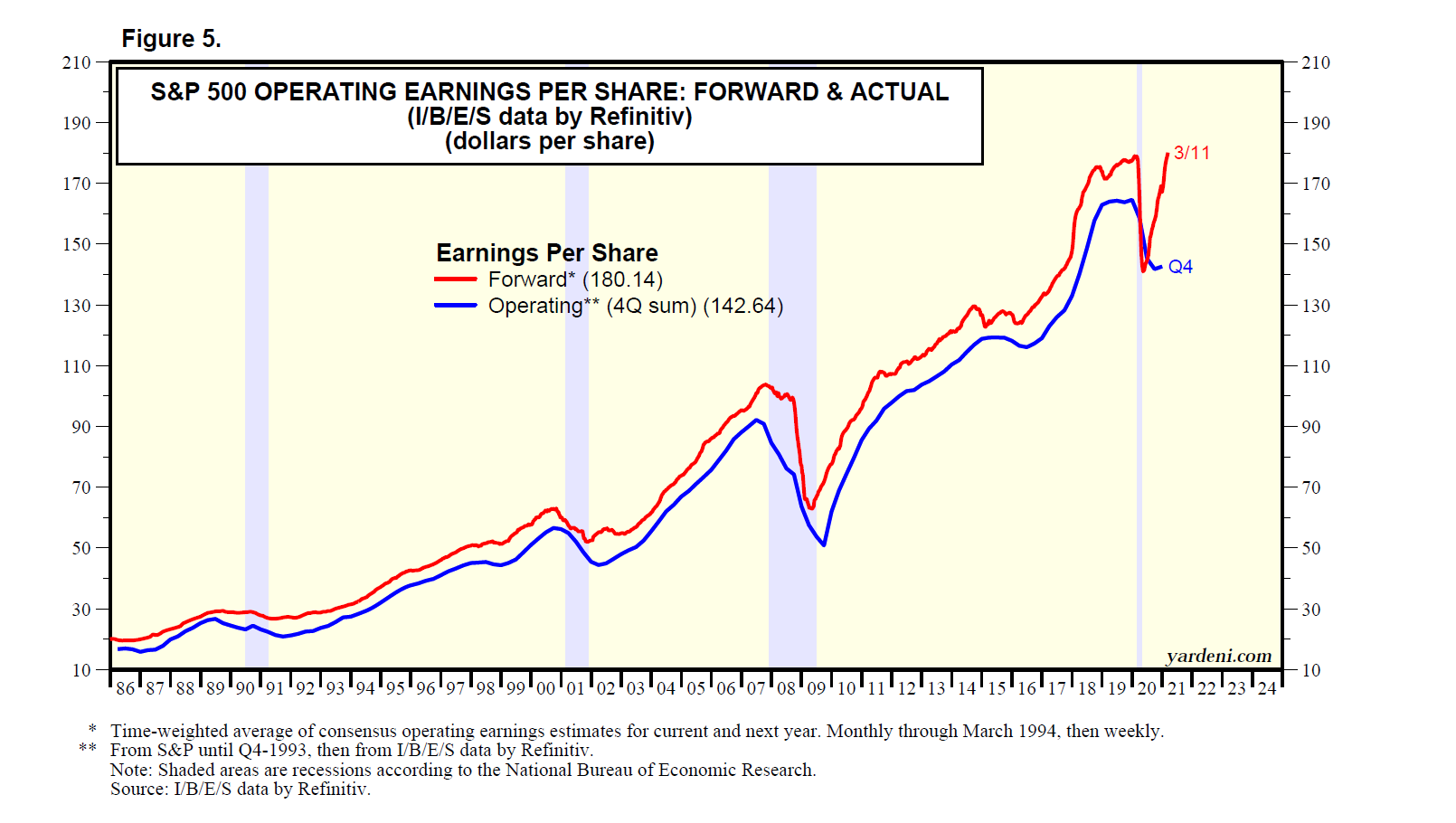

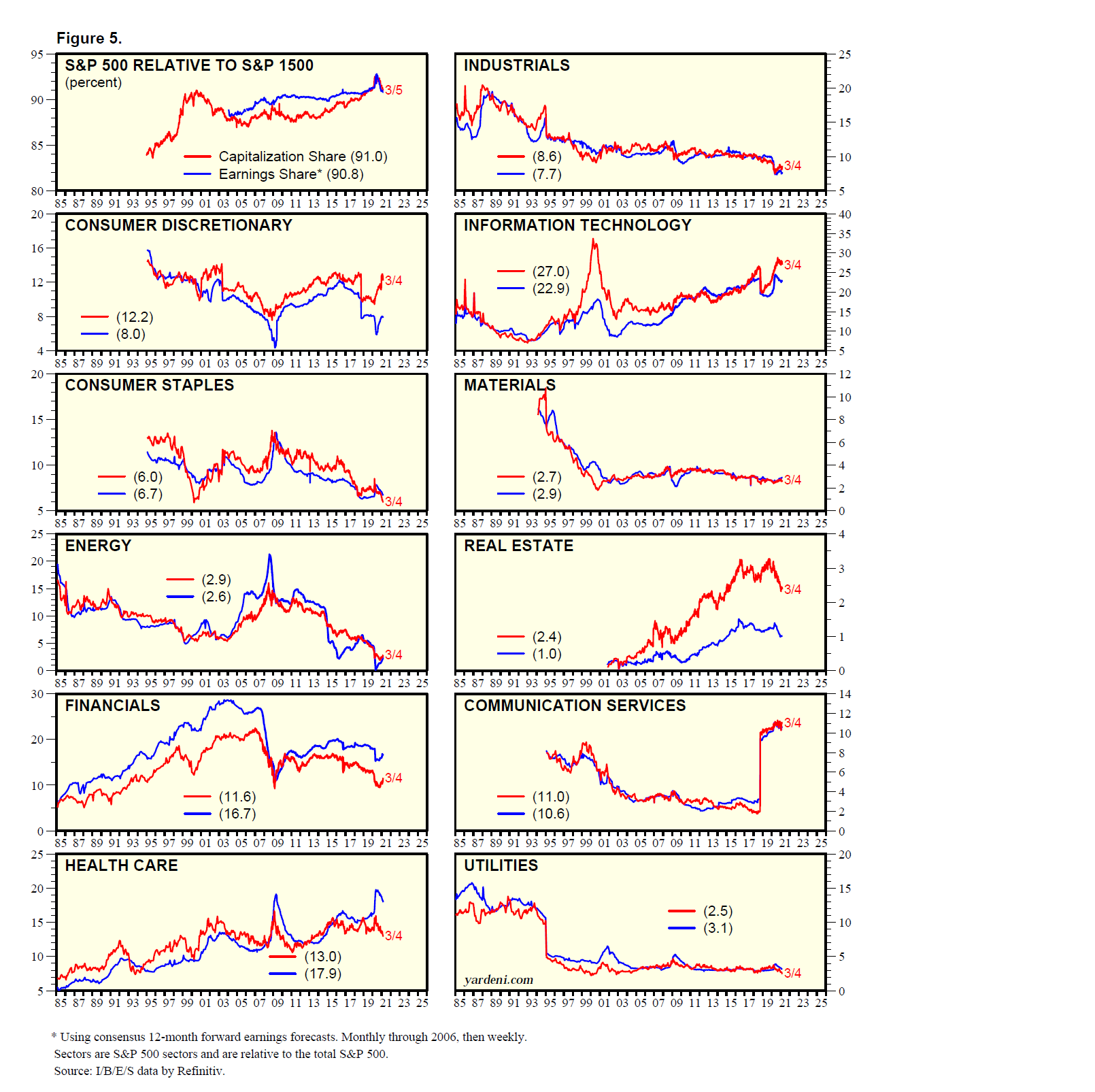

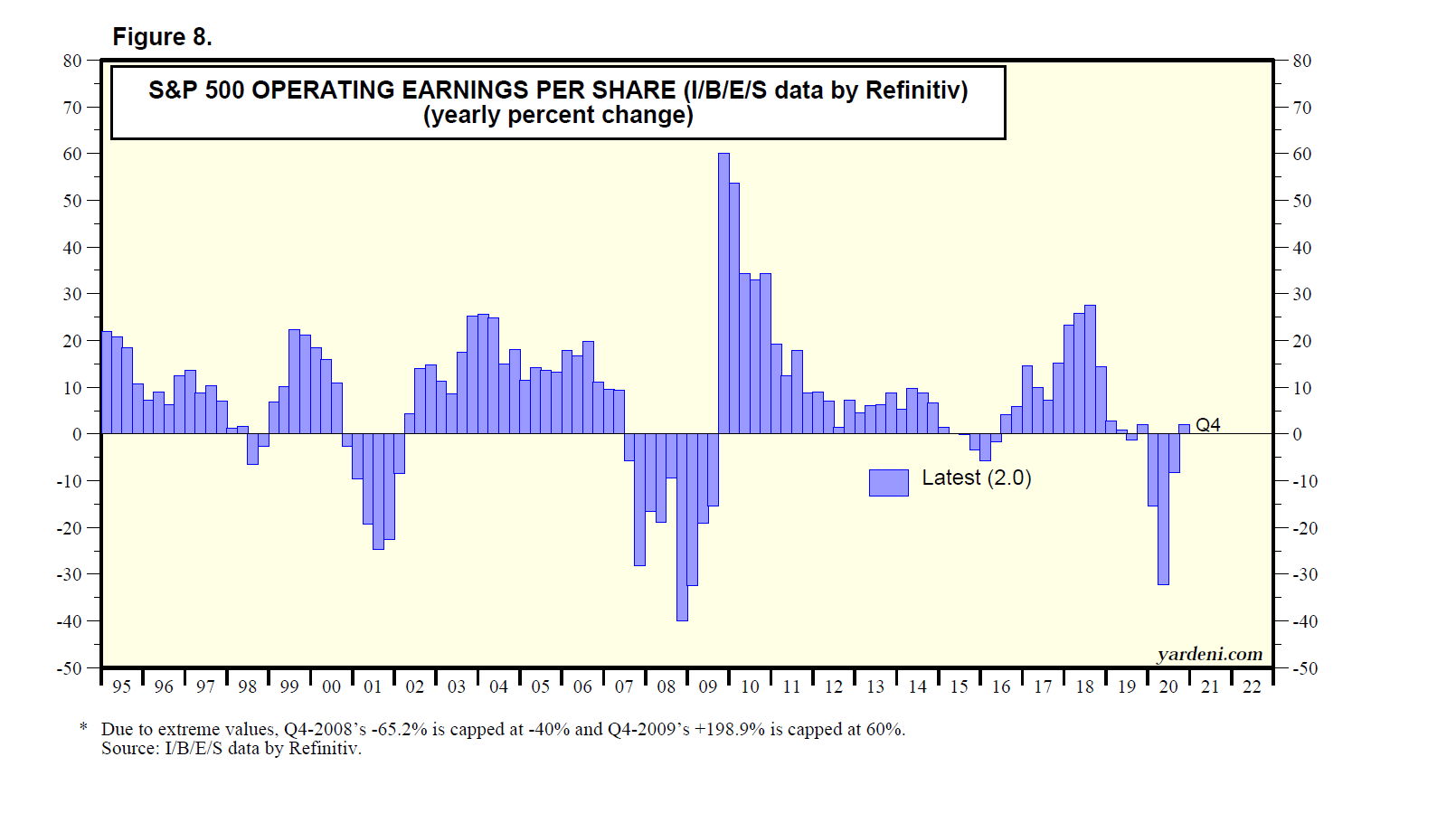

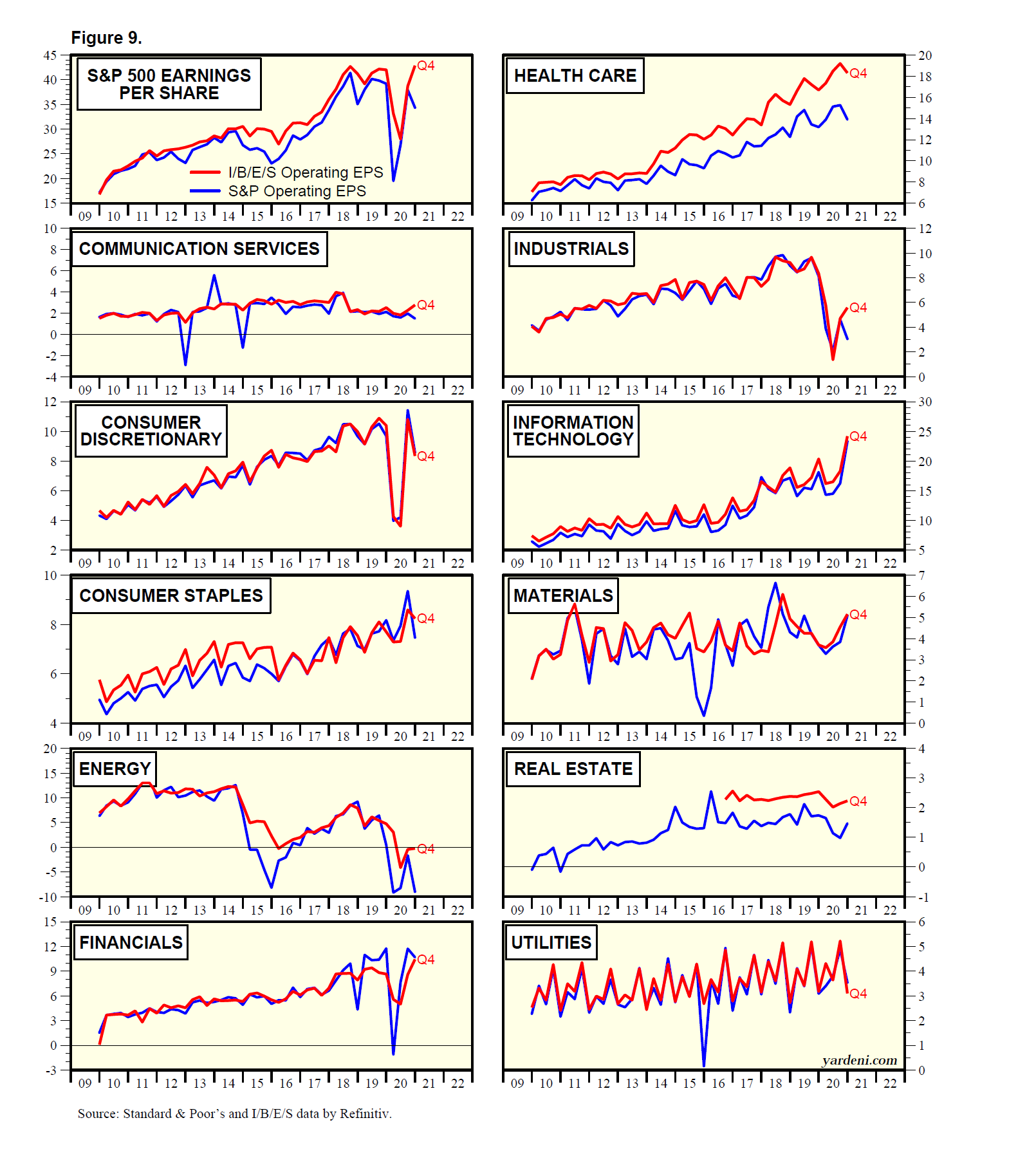

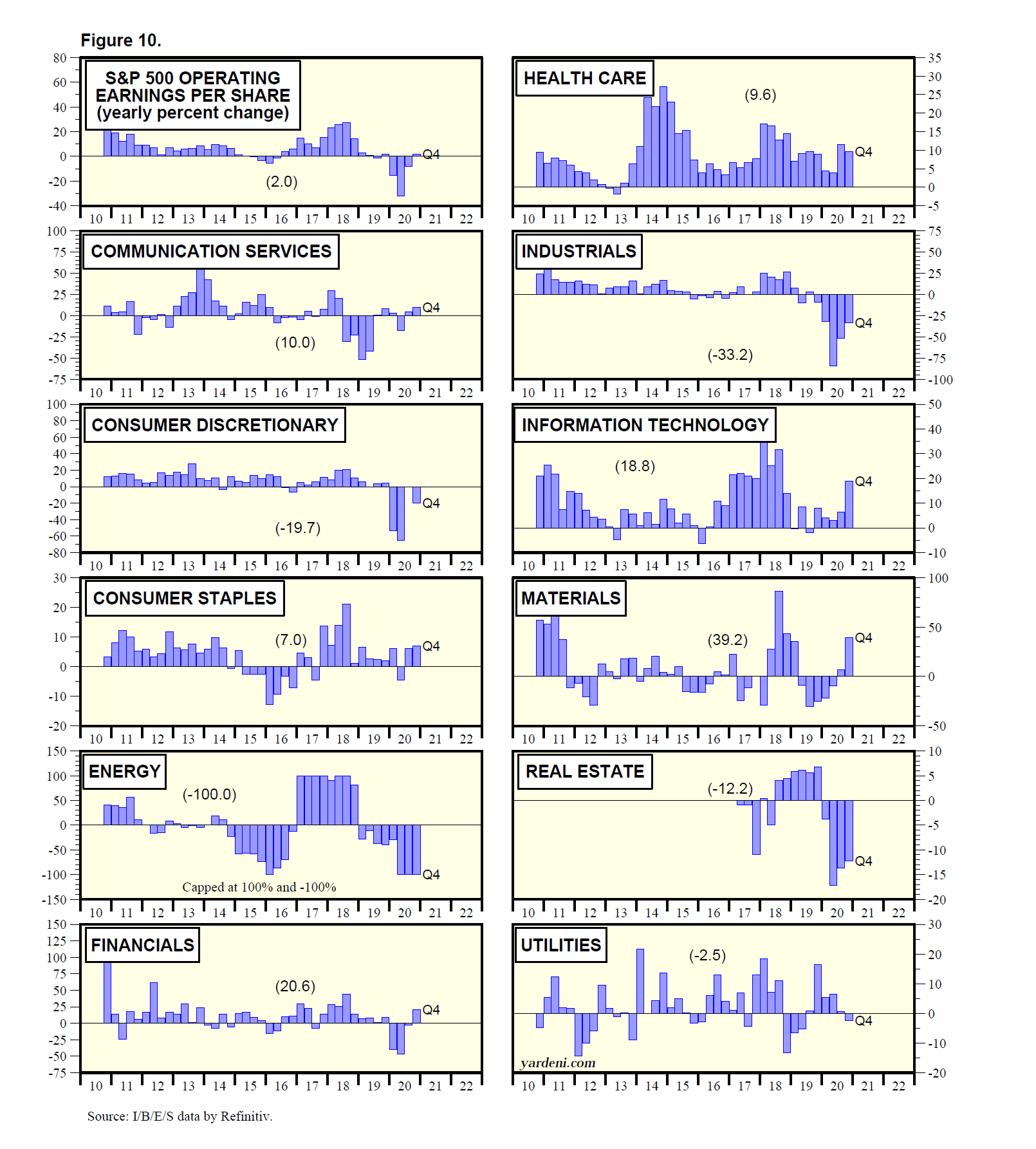

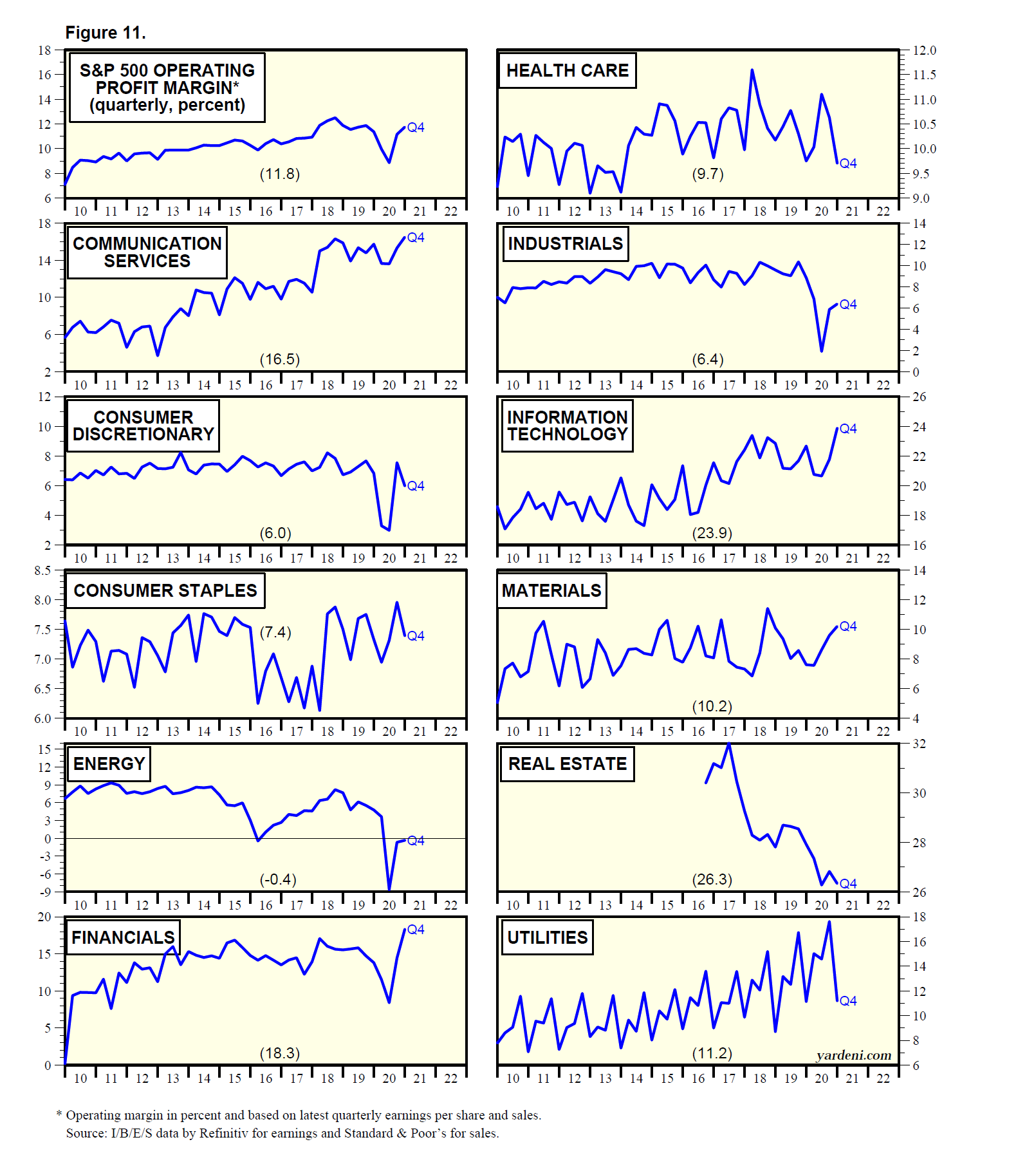

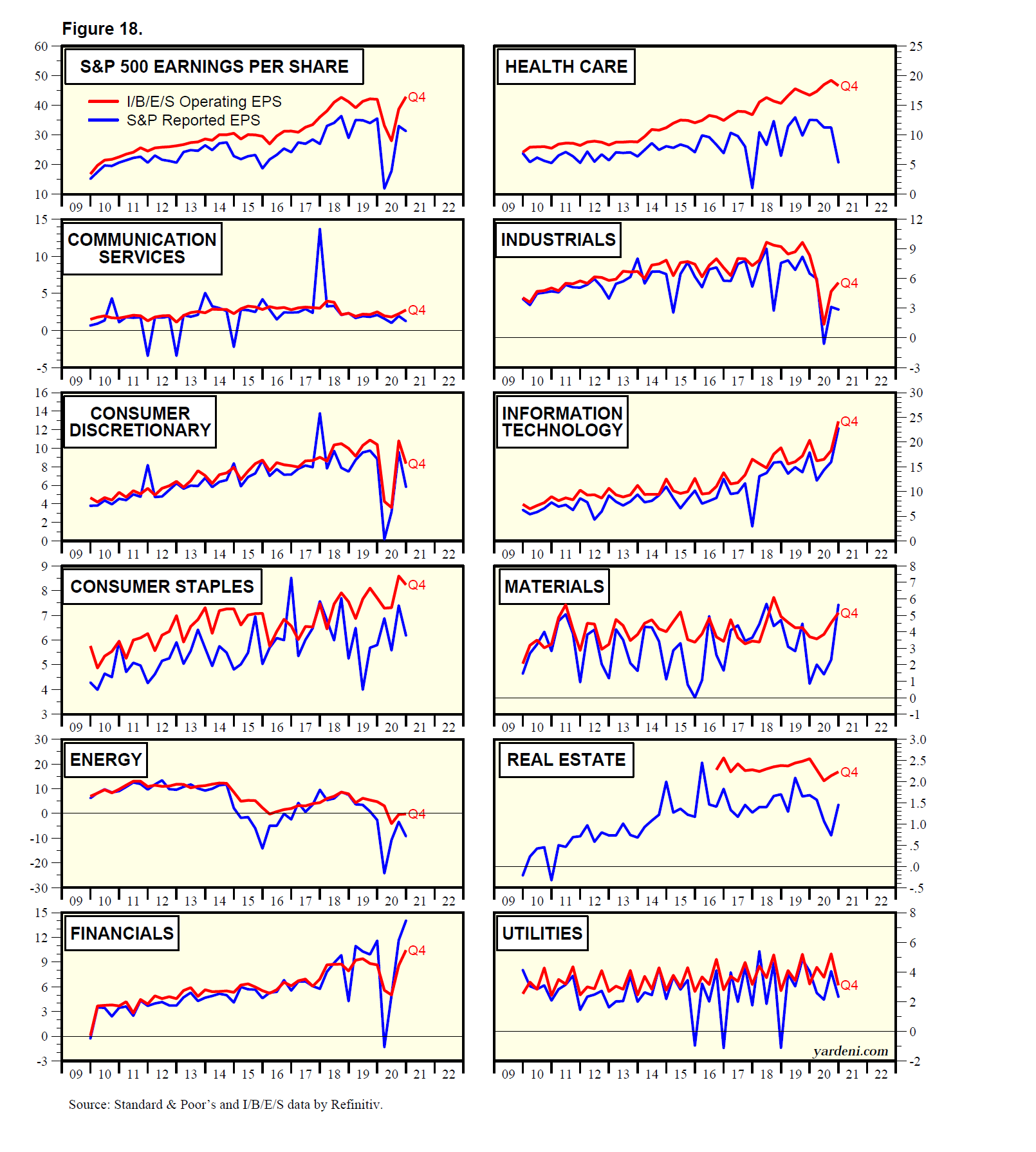

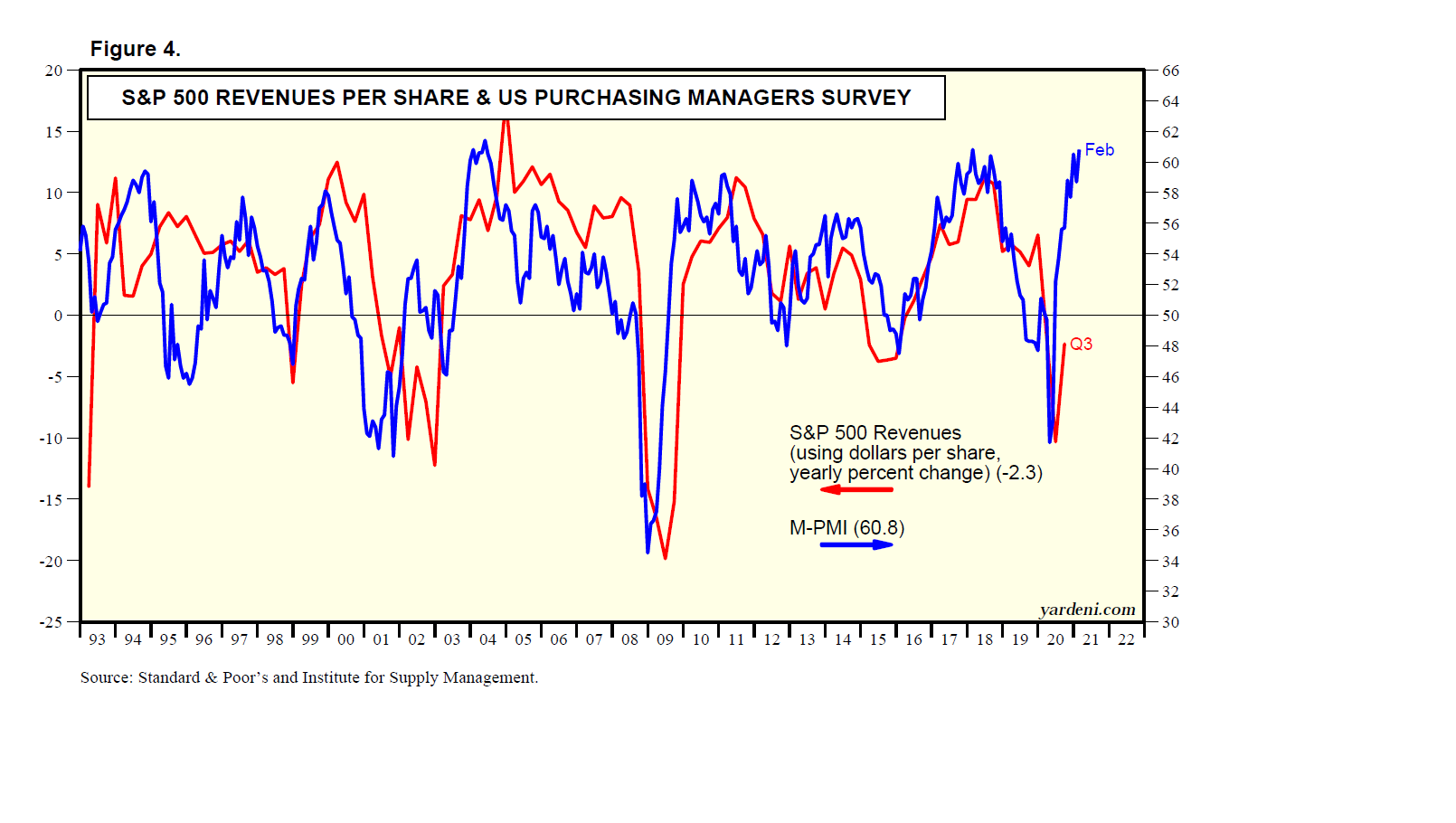

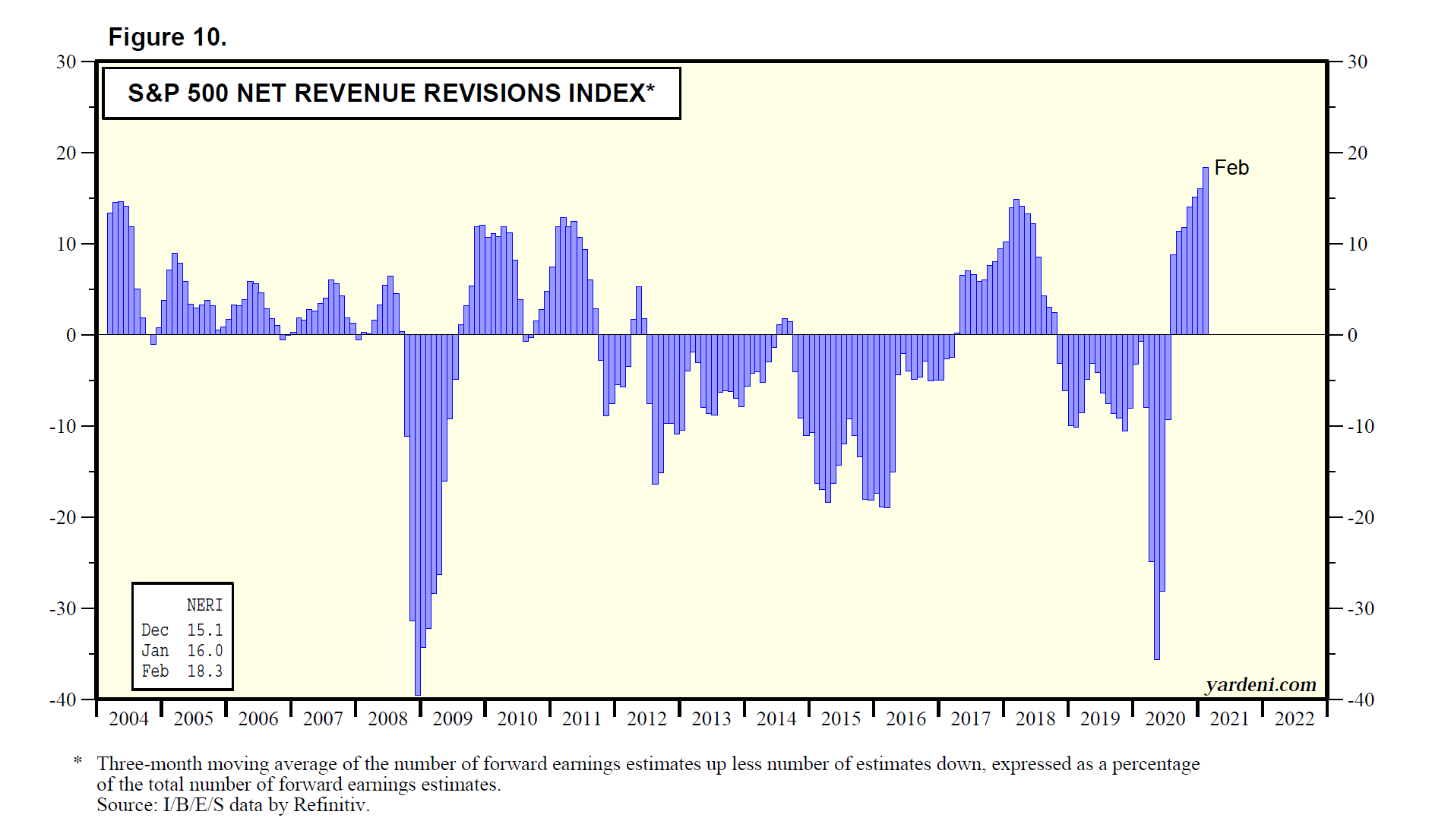

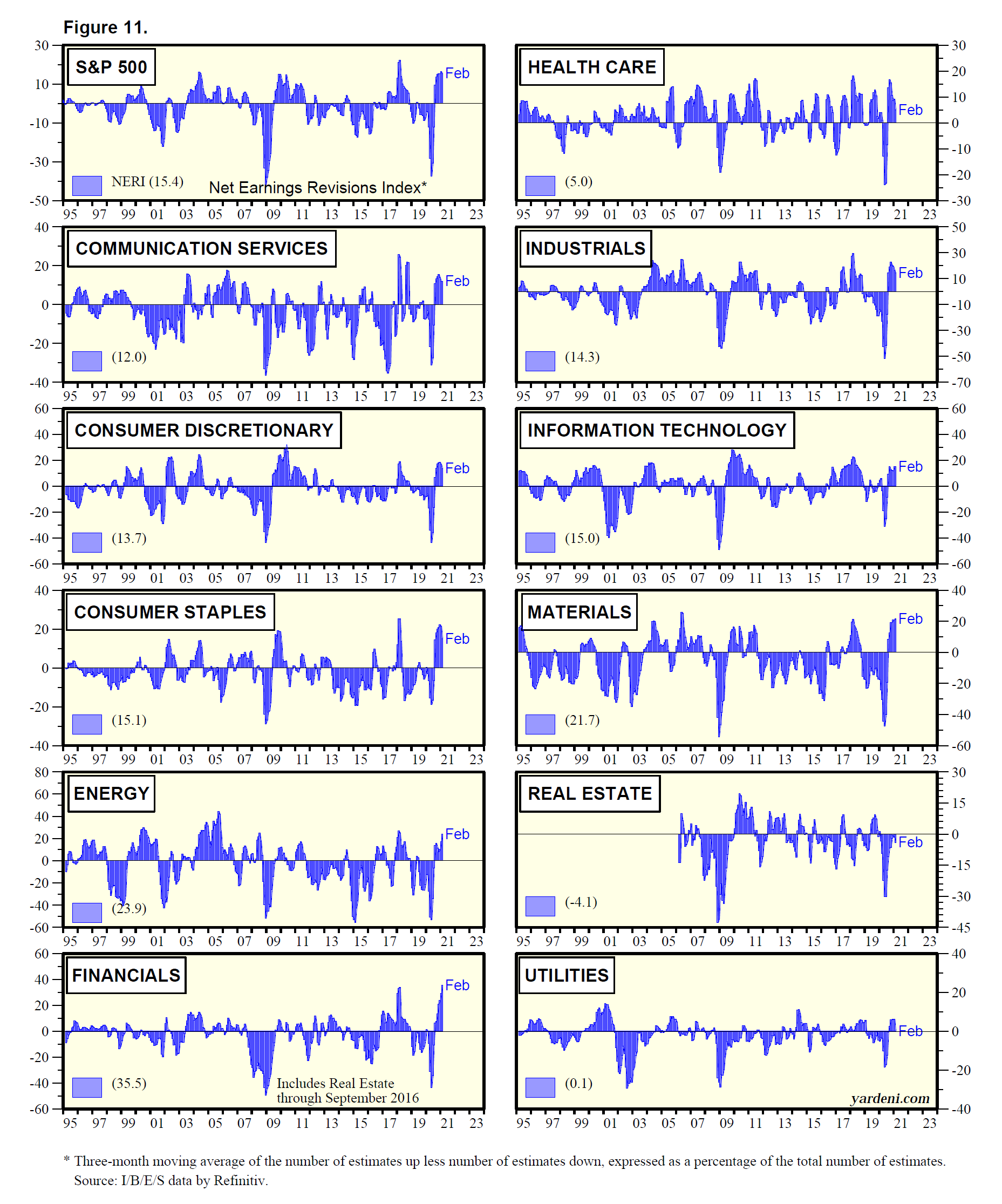

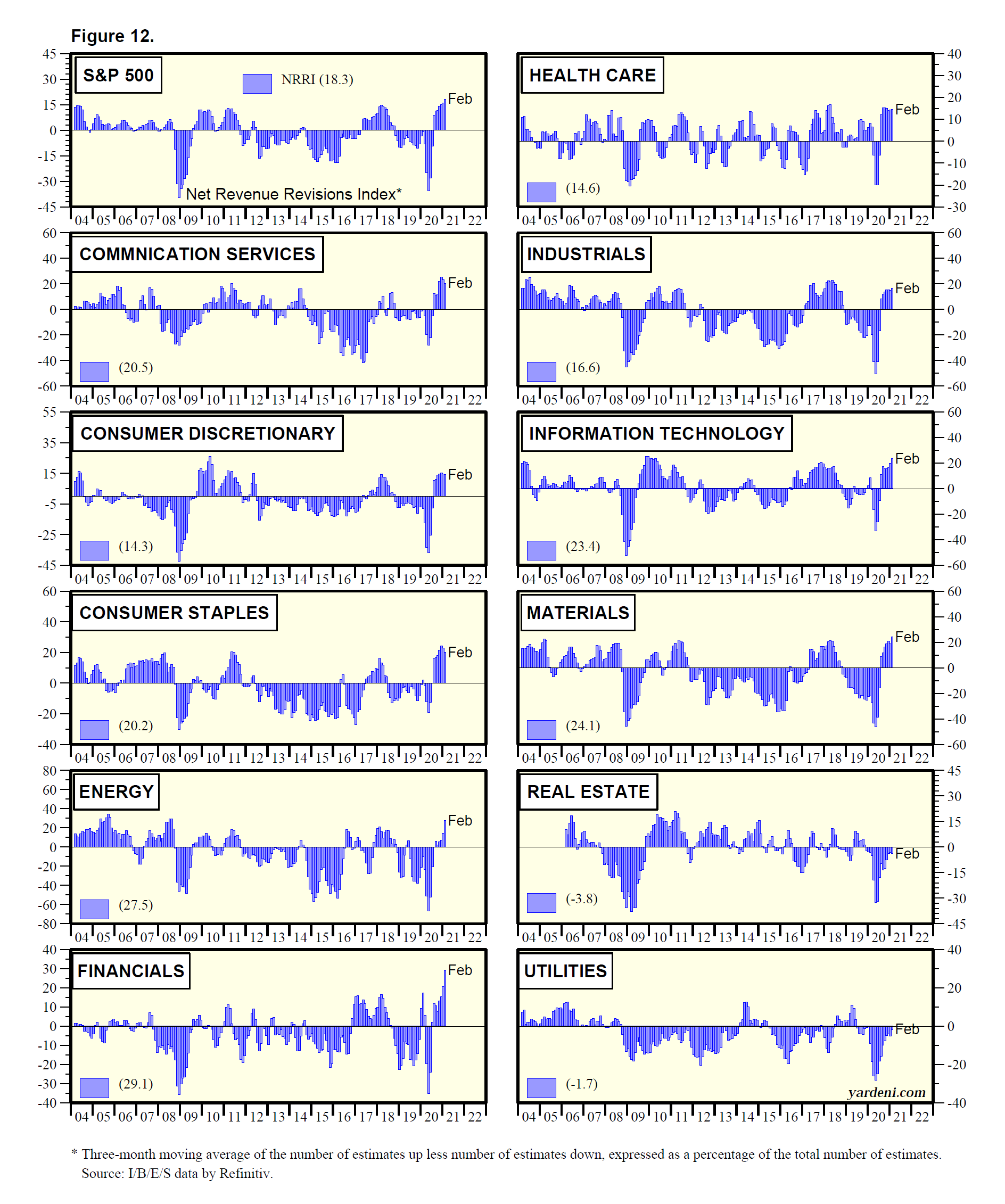

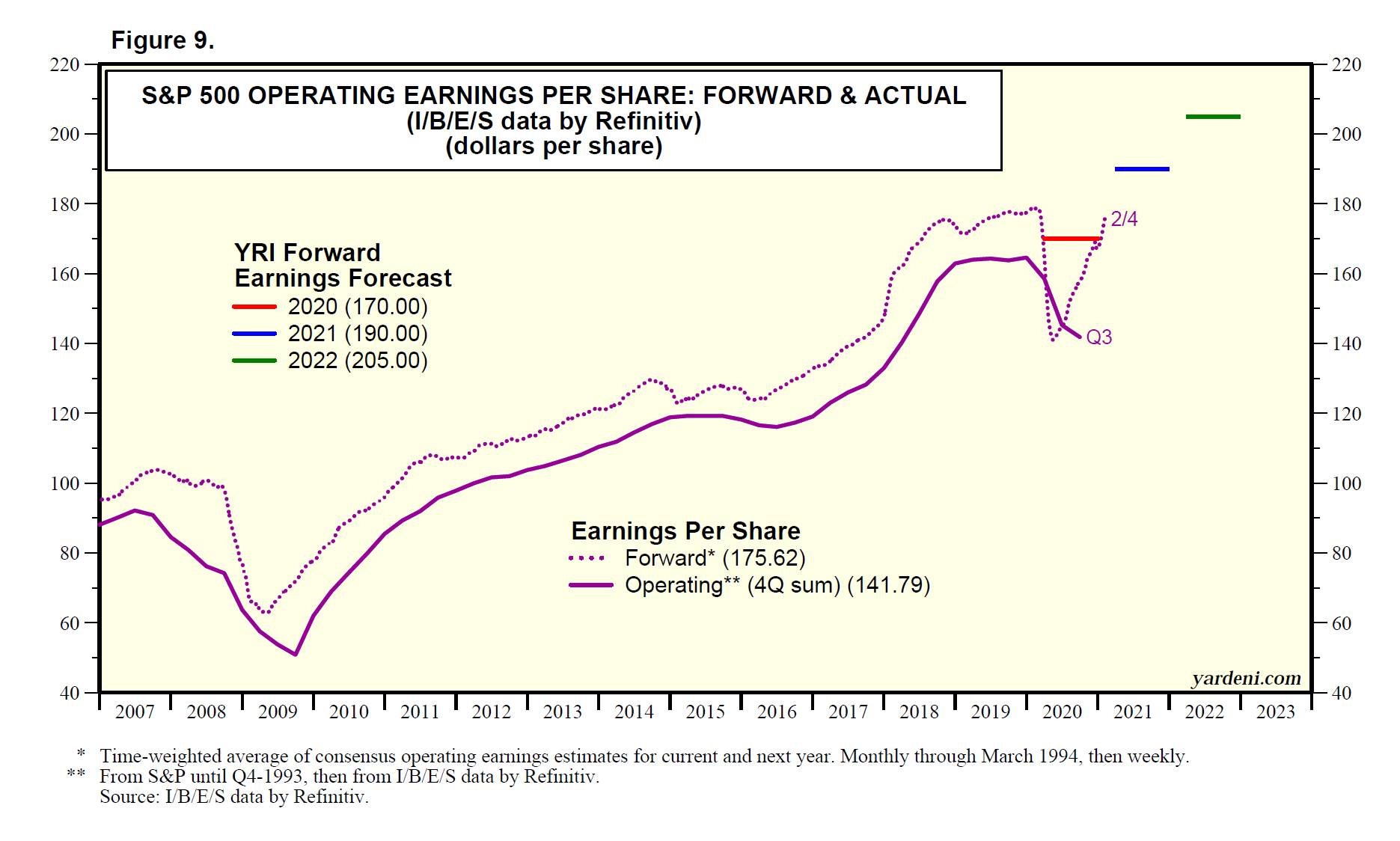

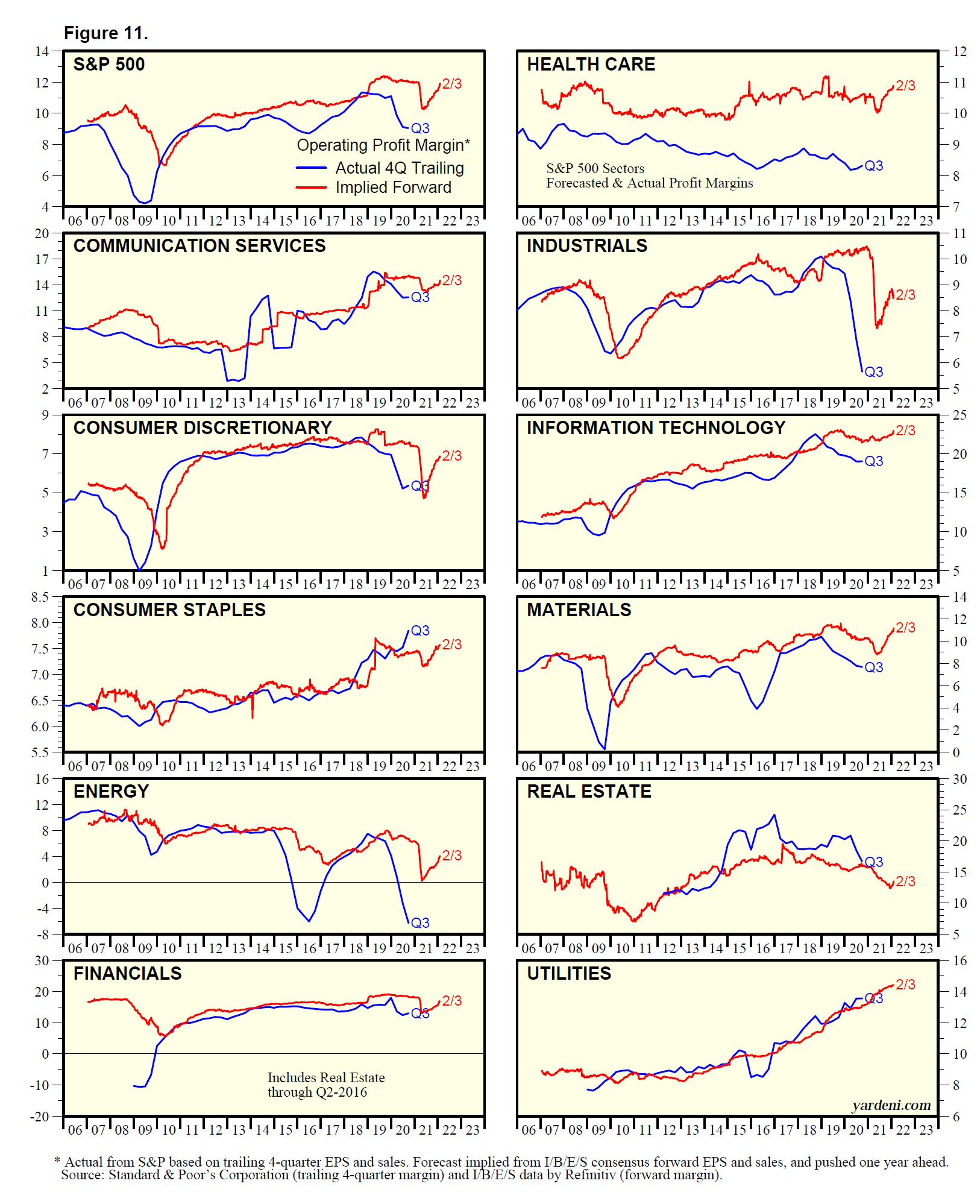

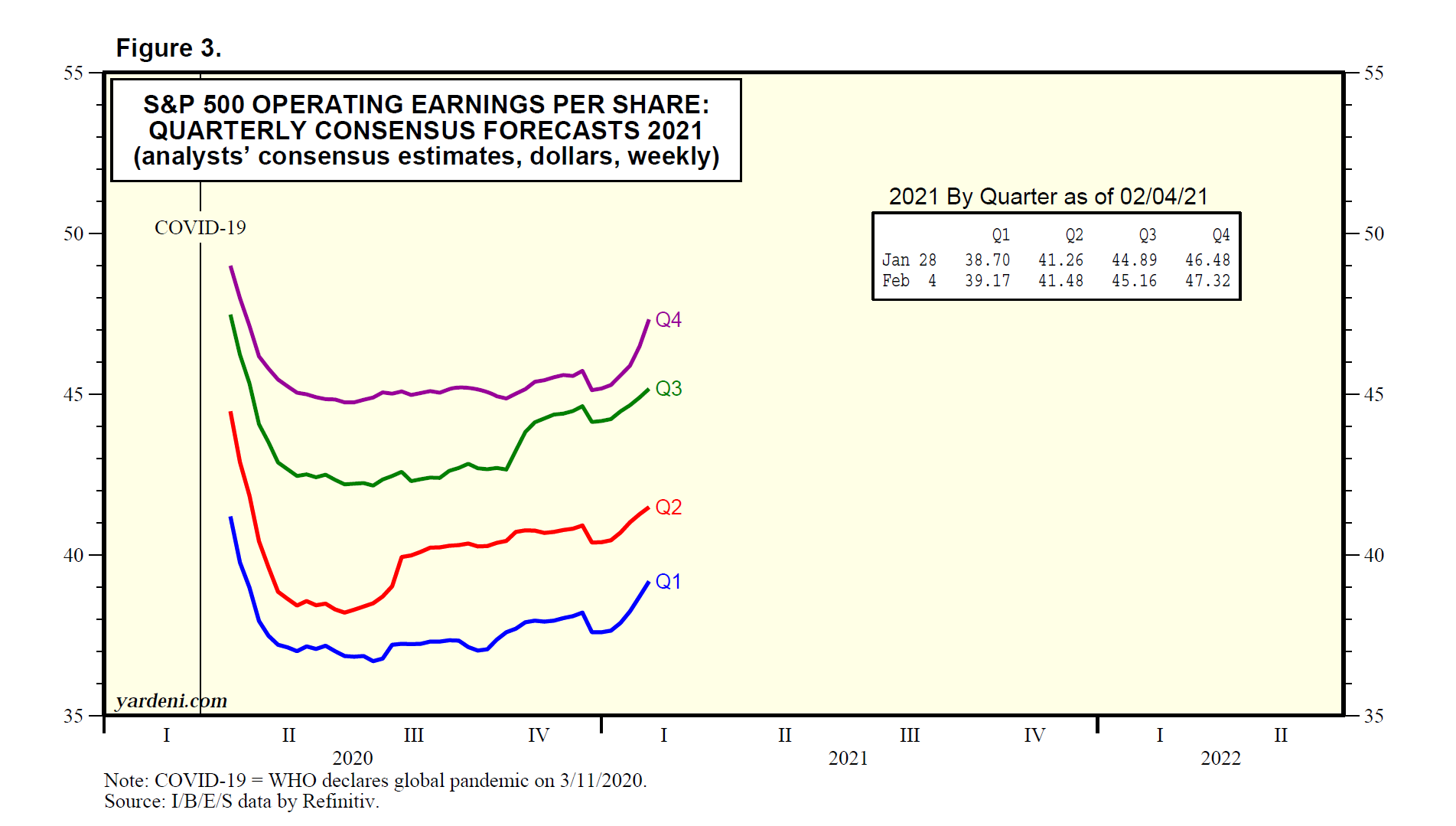

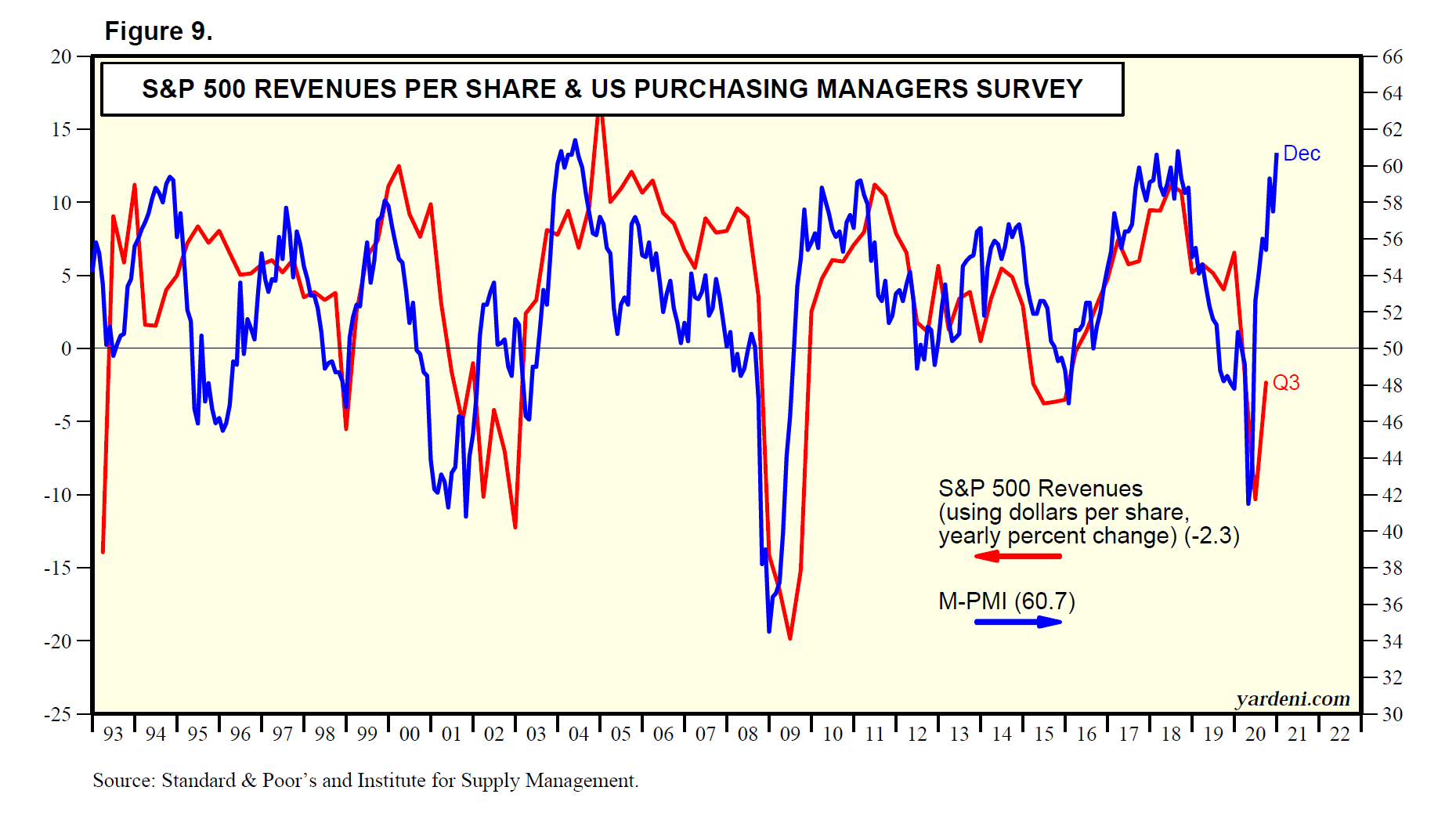

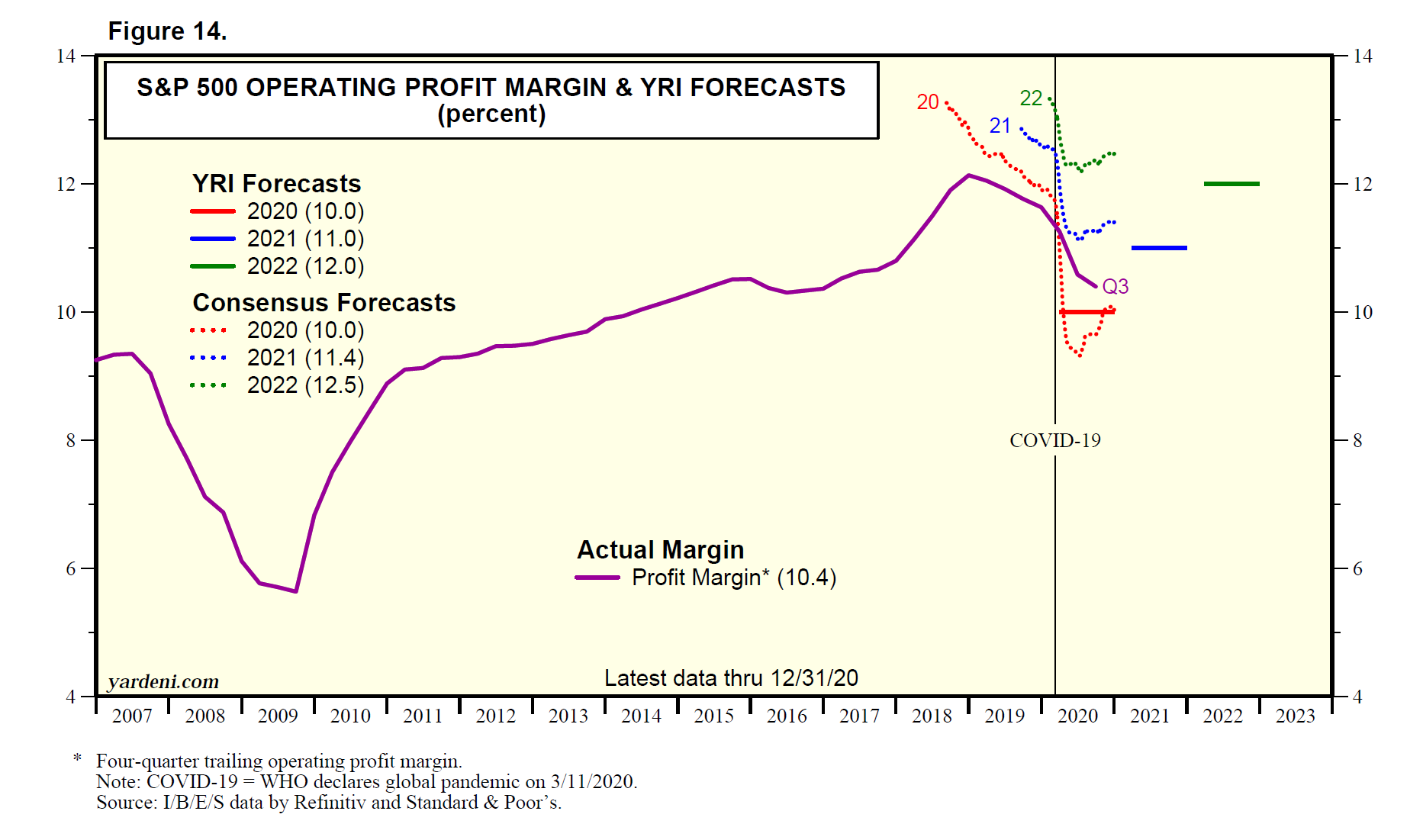

Strategy II: Profit Margins Peaking. Joe and I were impressed by Standard & Poor’s release recently of S&P 500 revenues per share and earnings per share. Both rose to record highs, but the y/y growth rates slowed from Q2’s latest peak rates. The former’s growth rate dropped to 13.9% y/y in Q3 from 21.8% y/y in Q2, while the latter fell to 39.3% from 88.6% (Fig. 9 and Fig. 10). Both of these growth rates are likely to decline further from their cyclical peaks in Q2 but should continue to grow through 2023. Here are our projected growth rates for S&P 500 revenues and earnings during 2021 (18%, 50%), 2022 (3, 5), and 2023 (3, 7). (See YRI S&P 500 Forecasts.)

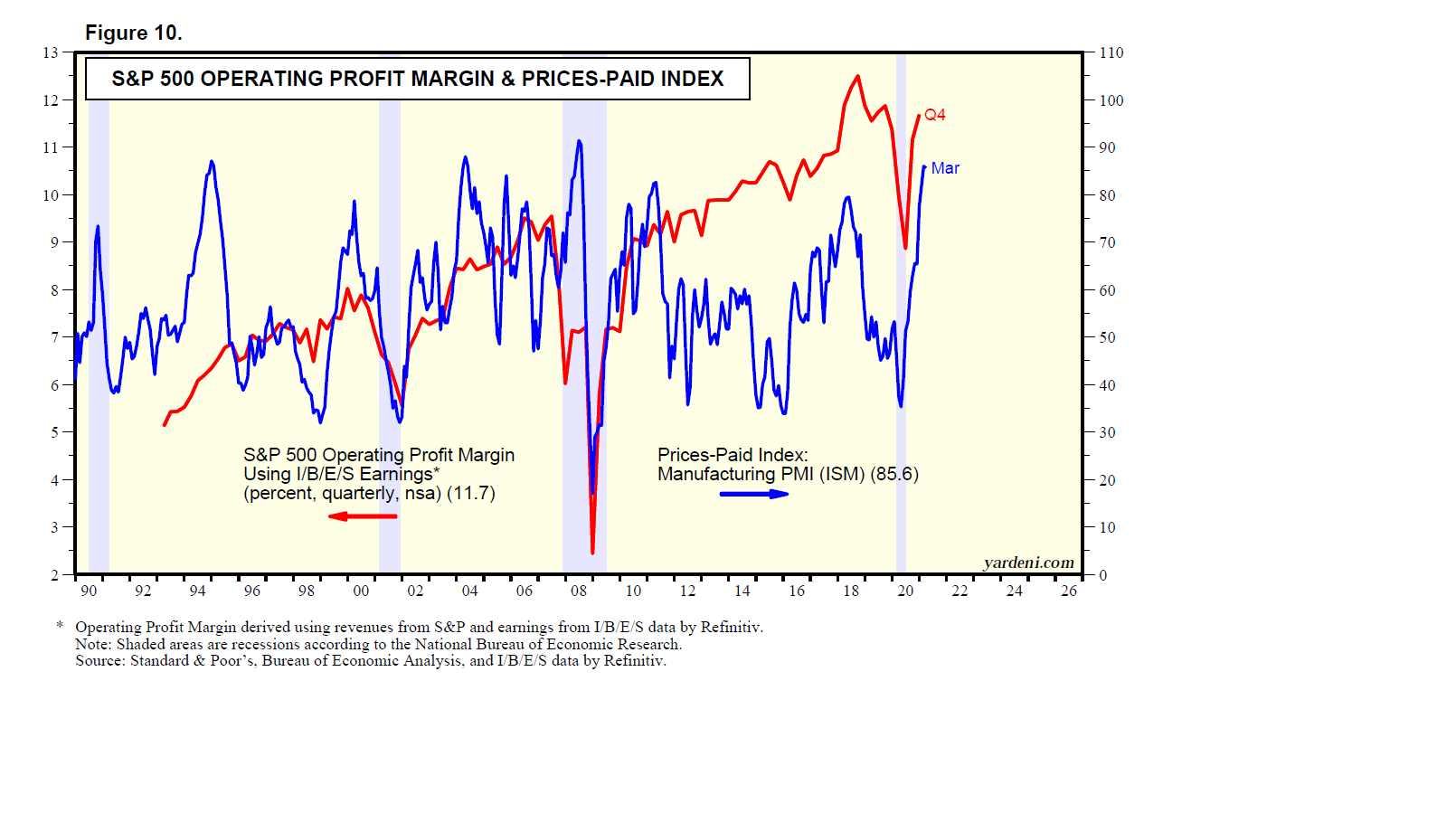

We can use the two series to calculate the profit margin of the S&P 500 (Fig. 11). Before the pandemic, the margin peaked at a then-record high of 12.5% during Q3-2018. President Donald Trump’s corporate tax cut was a big booster of the margin that year. As a result of the pandemic, the margin fell to 8.9% during Q2-2020, but that was well above the 2.4% low during the Great Financial Crisis. The margin rebounded from last year’s low to a record-high 13.7% during Q2 but ticked down to 13.6% during Q3.

The S&P 500 quarterly profit margin continues to impress us, but Q3’s slight decline from Q2’s record high was not surprising with labor and commodity costs continuing to rise. Another factor to consider is that the S&P 500 Financials sector saw less of a boost from loan-loss reversals in Q3 than it did in Q2. Using S&P’s operating earnings data, the S&P 500’s quarterly profit margin excluding Financials rose to a record-high 12.2% in Q3 from 11.8% in Q2 (Fig. 12).

Here are the latest developments for the S&P 500’s 11 sectors:

(1) Margins. Calculated using Refinitiv’s less conservative EBBS (earnings excluding bad stuff), otherwise known as operating earnings, the S&P 500 margin slipped in Q3 for the first time in five quarters even though the margins of seven sectors improved q/q, with two sectors, Information Technology and Utilities, reaching record highs. That was down from seven sectors’ margins improving q/q during Q2, when Materials’ and Tech’s margins were at record highs.

Here’s how the S&P 500 sectors’ margins stacked up during Q3 compared with their Q2 margins: Real Estate (30.7% [four-year high], 30.6%), Information Technology (25.5 [new record high], 24.7), Financials (18.7, 20.4), Communication Services (17.7, 18.5), Utilities (18.0 [new record high], 15.0), S&P 500 (13.6, 13.7), Materials (13.4, 14.7), Health Care (11.6, 11.4), Industrials (9.3 [two-year high], 9.1), Energy (9.2 [10-year high, 6.5), Consumer Staples (7.7, 7.7), and Consumer Discretionary (7.4, 7.8) (Fig. 13).

(2) Revenues. S&P 500 revenues per share hit a record-high $394.98 during Q3. Also hitting record highs were the revenues per share of Consumer Staples, Health Care, Materials, and the recently revamped Communication Services sector. Energy’s and Utilities’ revenues hit seven- and three-year highs, respectively, while Industrials’ was at a nine-quarter high. The revenues of Consumer Discretionary and Tech were at three-quarter highs, and those of the Financials and Real Estate sectors declined q/q from record highs in Q2 (Fig. 14).

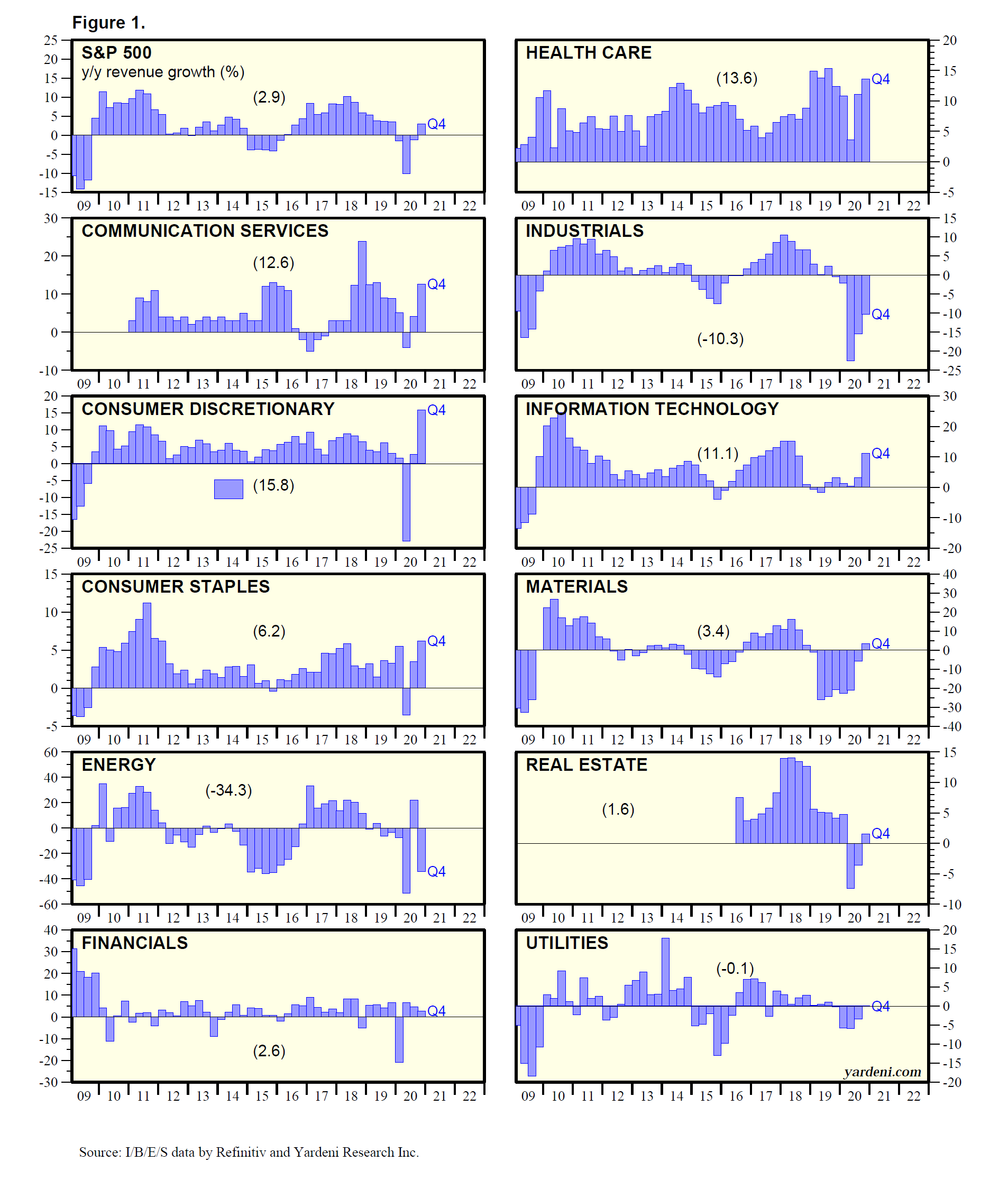

Looking at their y/y revenue growth rates in Q3, it appears that the S&P 500 and eight of its 11 sectors peaked during Q2. The three exceptions—Financials, Tech, and Utilities—did so during Q1. During Q3, just three sectors failed to post double-digit percentage y/y revenues growth.

Here are the sectors’ Q3 y/y revenue growth rates along with their Q2 readings: Energy (62.5%, 97.0%), Materials (31.9, 36.9), Information Technology (18.8, 22.1), Industrials (17.6, 28.6), Communication Services (16.6, 27.2), Real Estate (14.3, 18.7), S&P 500 (13.9, 21.8), Health Care (12.6, 19.0), Consumer Staples (10.7, 13.0), Utilities (8.5, 9.5), Financials (3.4, 5.9), and Consumer Discretionary (-2.6, 15.3).

However, Consumer Discretionary’s revenues didn’t really fall y/y. That’s because S&P’s index methodology does not adjust historical per-share data for index changes. Using Refinitiv’s pro forma data—which assumes that Tesla was in the Consumer Discretionary sector during both years although it wasn’t—the sector’s y/y revenues growth rate was 10.9% in Q3 instead of -2.6%, down from a peak of 35.2% during Q2 instead of 15.3%. Also according to Refinitiv, Energy boosted the S&P 500’s revenue growth rate by 3.4ppts to 17.0%.

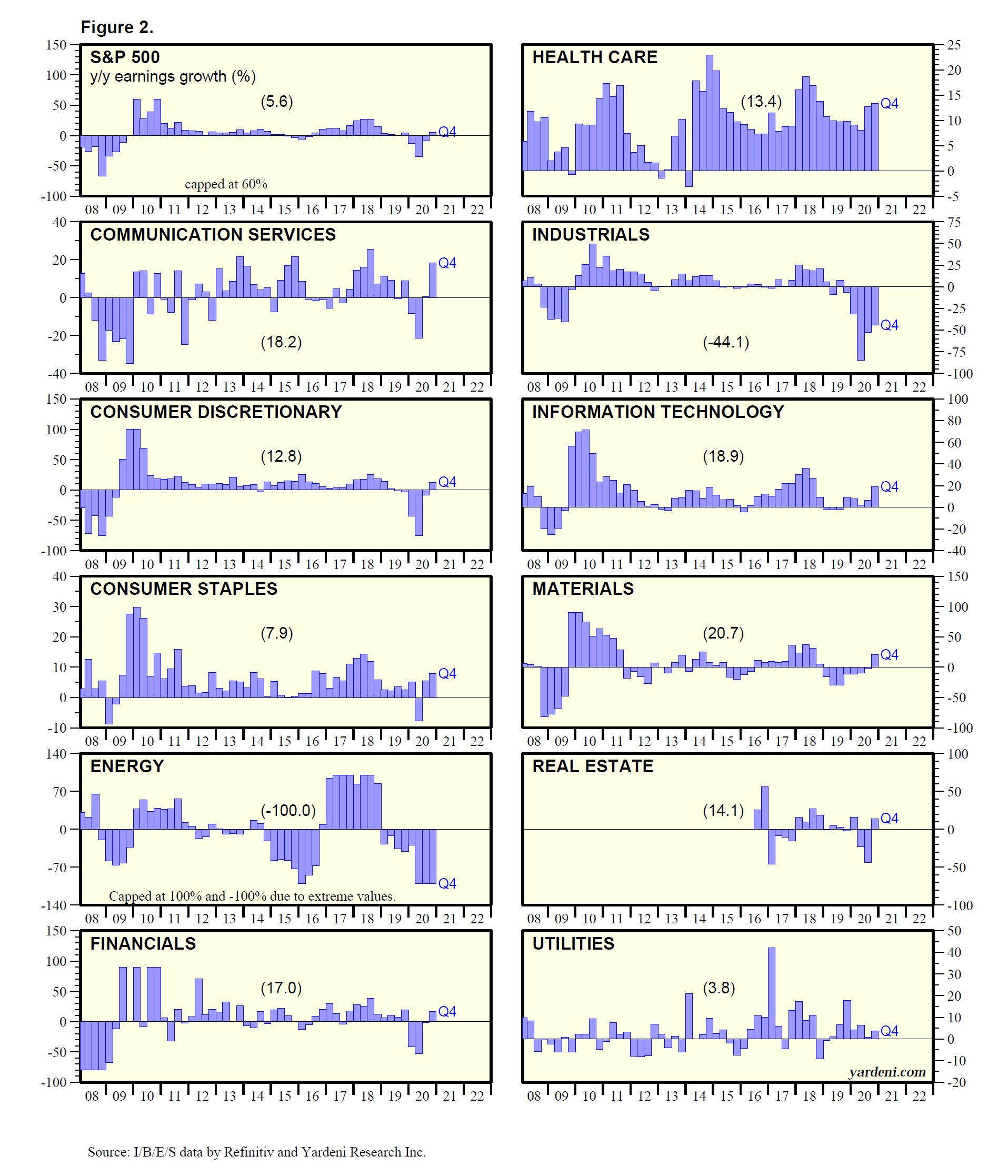

(3) Earnings. Earnings growth rates peaked during Q2 due to base-period effects in 2020 when the US economy was largely shut down. During Q3, the y/y earnings growth rates weakened q/q for the S&P 500 and seven of the 11 sectors. Energy’s rebounded from a year-earlier loss. The weakening was primarily due to base effects, as the US economy emerged from lockdown during Q3-2020.

Here’s how the Q3 y/y operating earnings-per-share growth rates of the S&P 500 and its sectors stacked up versus their Q2 growth rates: Energy (675.8%, 169.7%), Materials (109.1, 141.2), Real Estate (107.1, 86.0), Industrials (93.9, 316.8), S&P 500 (37.6, 94.3), Communication Services (56.9, 99.4), Information Technology (46.5, 51.0), Health Care (41.3, 25.5), Financials (6.5, 108.1), Consumer Staples (-0.5, 14.1), Utilities (-2.5, -17.4), and Consumer Discretionary (-10.8, 173.5) (Fig. 15). Notably, S&P’s version of Consumer Discretionary’s results were impacted by Tesla’s addition.

Refinitiv’s earnings measure shows similar slowdowns for the S&P 500 and most of its sectors (all but Energy). Here are Refinitiv’s y/y earnings growth rates for the index and its sectors during Q3 and Q2: Energy (2295.5%, 249.4%), Industrials (86.8, 522.1), Materials (84.4, 133.0), S&P 500 (39.3, 88.6), Information Technology (39.1, 46.3), Communication Services (34.7, 73.1), Financials (33.9, 157.4), Real Estate (30.8, 38.1), Health Care (22.4, 22.7), Utilities (10.9, 12.9), Consumer Staples (7.1, 18.7), and Consumer Discretionary (-3.9, 202.2).

According to Refintiv, Consumer Discretionary’s y/y earnings growth rate with Tesla in the sector during both years would have been 19.4% in Q3, down from 380.5% in Q2. Also according to Refinitiv, the S&P 500’s earnings growth rate without Energy would have dropped to 34.3%.

Santa’s Sleigh & Biden’s Helicopters

December 13 (Monday)

Check out the accompanying pdf and chart collection.

(1) Stocking stuffer idea. (2) Two Grinches: the Omicron variant and the hawkish Powell variant. (3) Believing in Santa. (4) S&P 500 makes another record high … Ho-Ho-Ho! (5) Good tidings for Tech. (6) A happy holiday yield-curve story. (7) Bidenflation: Dropping cash from helicopters works all too well. (8) Larry Summers was right. (9) Inflation likely to persist, but moderate later next year. (10) How real are S&P 500 earnings? (11) Real earnings yield says sell. We say don’t sell. (12) Movie review: “West Side Story” (+ +).

Great Stocking Stuffer. May I suggest the perfect gift for your family members and friends? Why not give them a copy of my new book, In Praise of Profits!? I wrote it for liberals, who may be surprised to find that I share some of their views and shed new light on others. Whether you are a liberal or a conservative, you will be praising profits and entrepreneurial capitalism more than ever. Complimentary downloads of the book are available here.

YRI Monday Webinar. Join Dr. Ed’s live Q&A webinar on Mondays at 11 a.m. EST. You will receive an email with the link to the webinar one hour before showtime. Replays are available here.

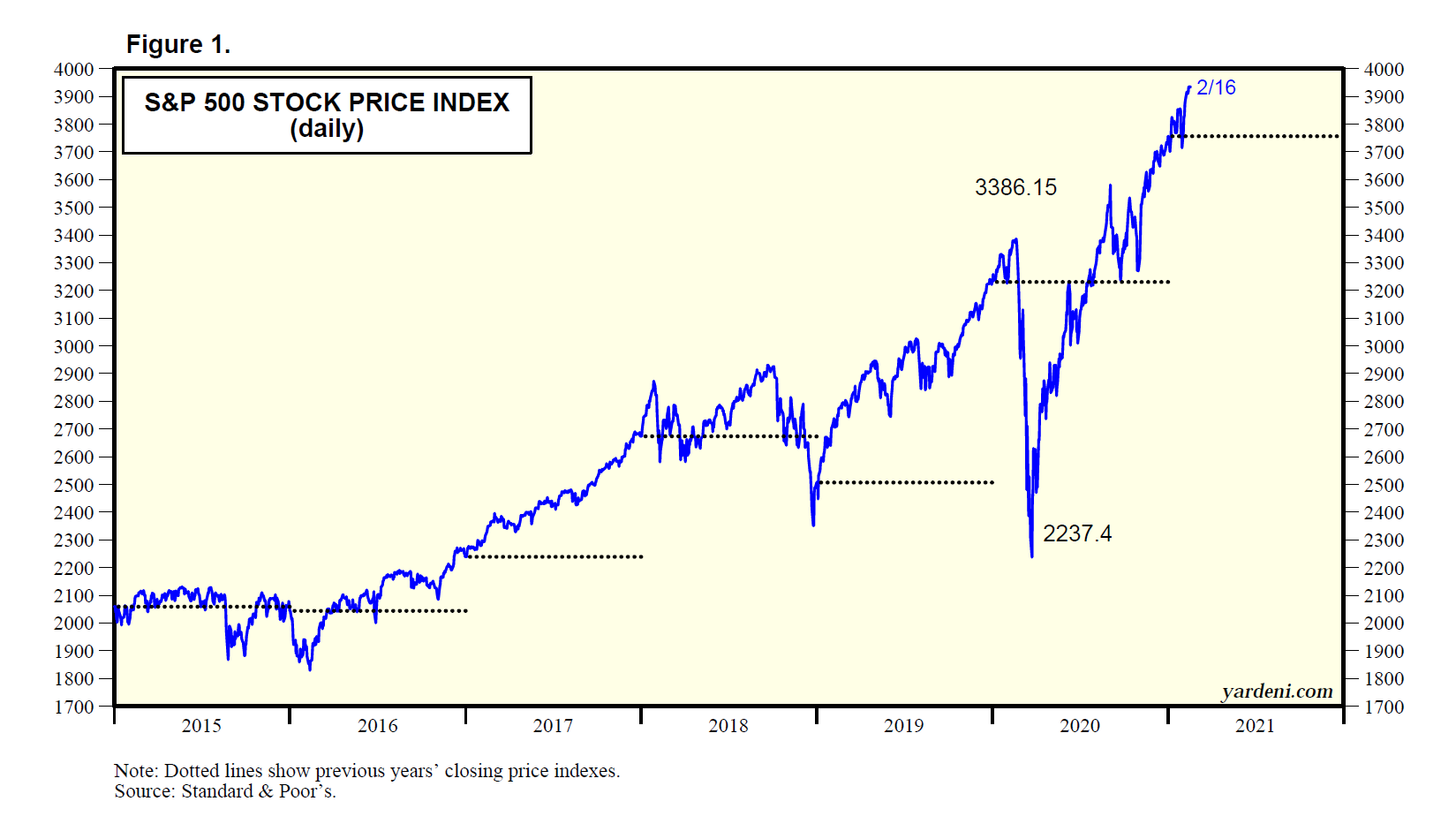

Santa Watch. Joe and I believe in Santa Claus. In our December 1 Morning Briefing, we wrote: “The Santa Claus rally started early this year. The question is whether it is over already.” The rally started on October 4 with the S&P rising 9.4% to a new record high on November 18. Just after Thanksgiving, investors started to worry that two Grinches were about to steal the Santa Claus rally, i.e., the Omicron variant of Covid-19 and the more hawkish variant of Fed Chair Jerome Powell. Like true believers, we wrote: “We aren’t giving up on Santa Claus.”

The S&P 500 bottomed on December 1 at 4513.04, down 4.1% from its recent high. Santa was back at the reins on Friday when the S&P 500 rose to a new record high of 4712.02 (Fig. 1). Ho-Ho-Ho!

Having the merriest time last week was the S&P 500 Tech sector, which rose 6.0% to a new record high (Fig. 2). Joe reports that it was the only sector to beat the S&P 500’s 3.8% gain. Looking at the available weekly data since 1991, that has happened only twice before, i.e., the weeks of February 4, 2000 and January 19, 2001. (Don’t spoil our merriment by reminding us that those years are associated with the bursting of the tech bubble.) Consider the following related developments:

(1) Performance derby. Here is the festive performance derby of the S&P 500 and its 11 sectors last week: Information Technology (6.0%), S&P 500 (3.8), Energy (3.7), Consumer Staples (3.5), Materials (3.5), Health Care (3.2), Industrials (3.0), Communication Services (2.9), Real Estate (2.7), Financials (2.6), Utilities (2.6), and Consumer Discretionary (2.5). (See table.) Besides Tech, the only other sector to hit a new record high on Friday was Consumer Staples.

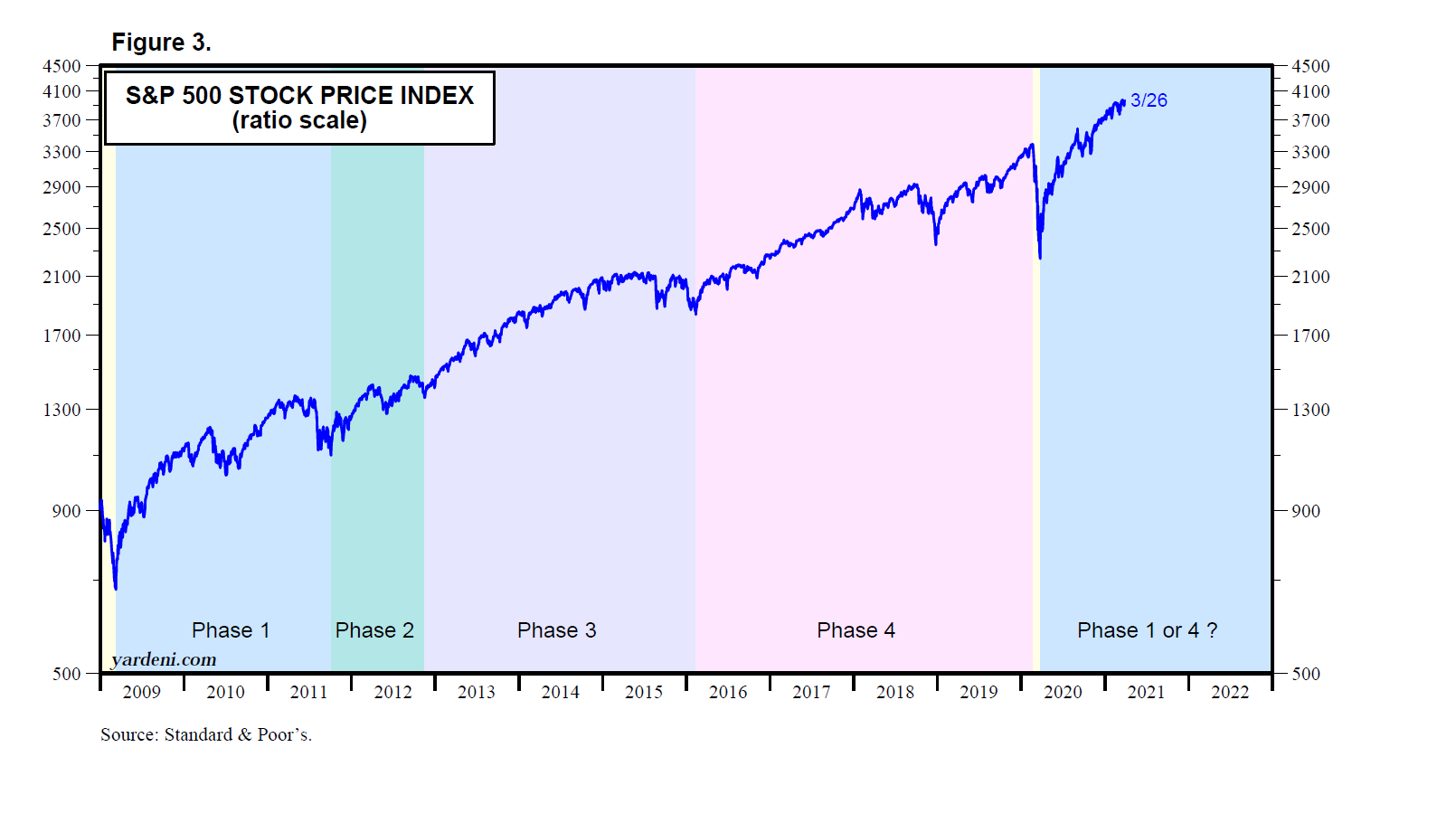

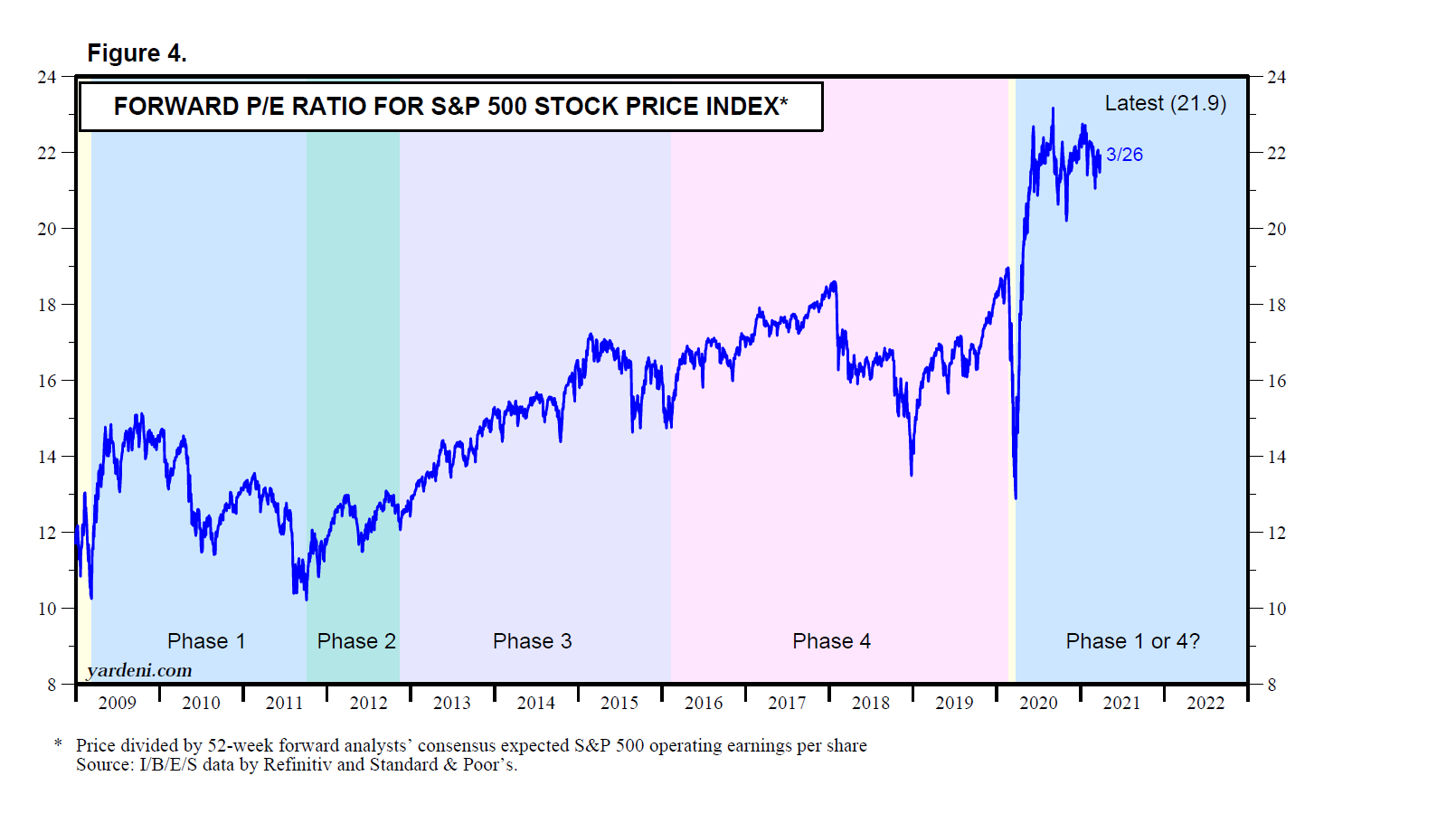

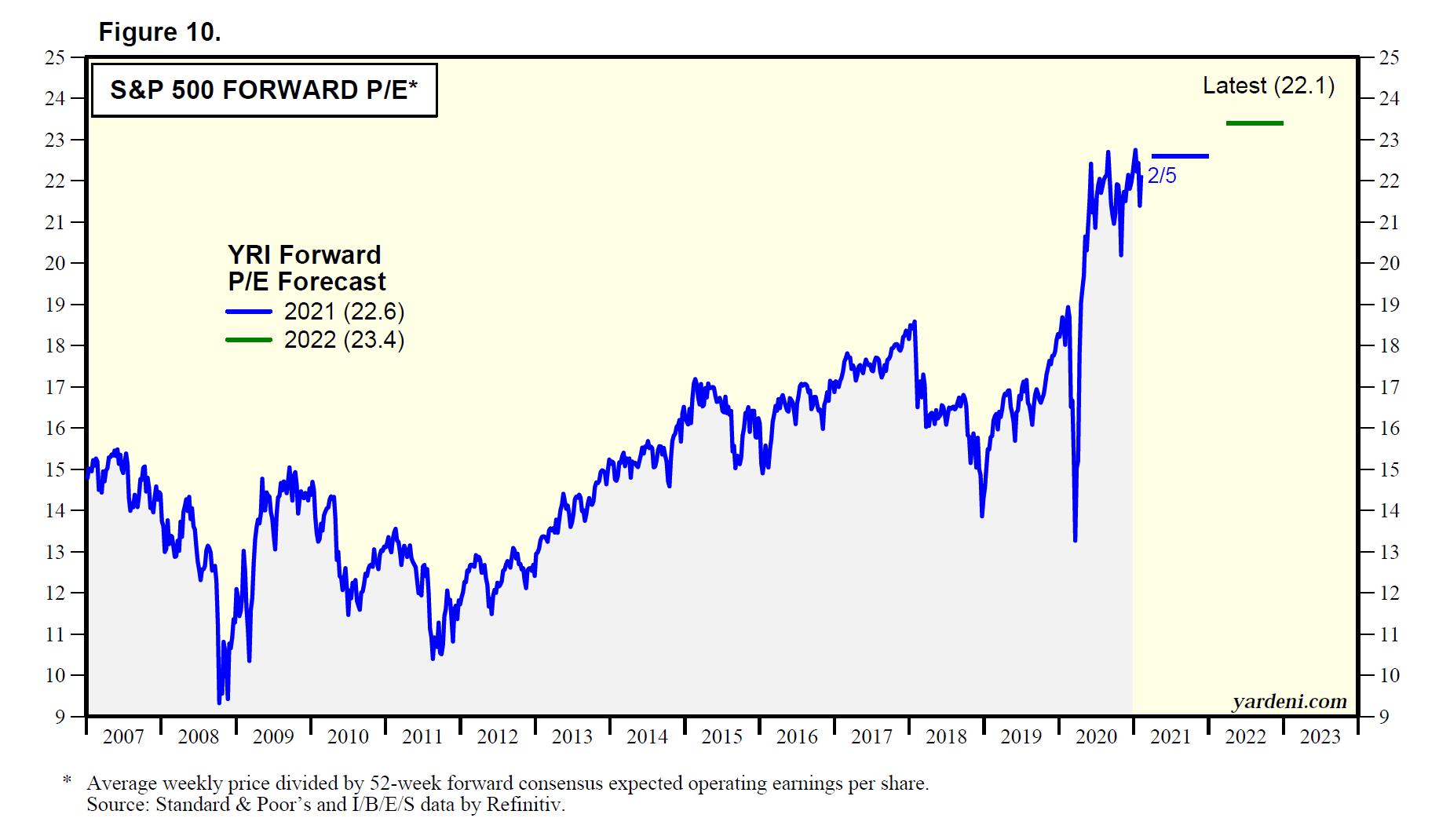

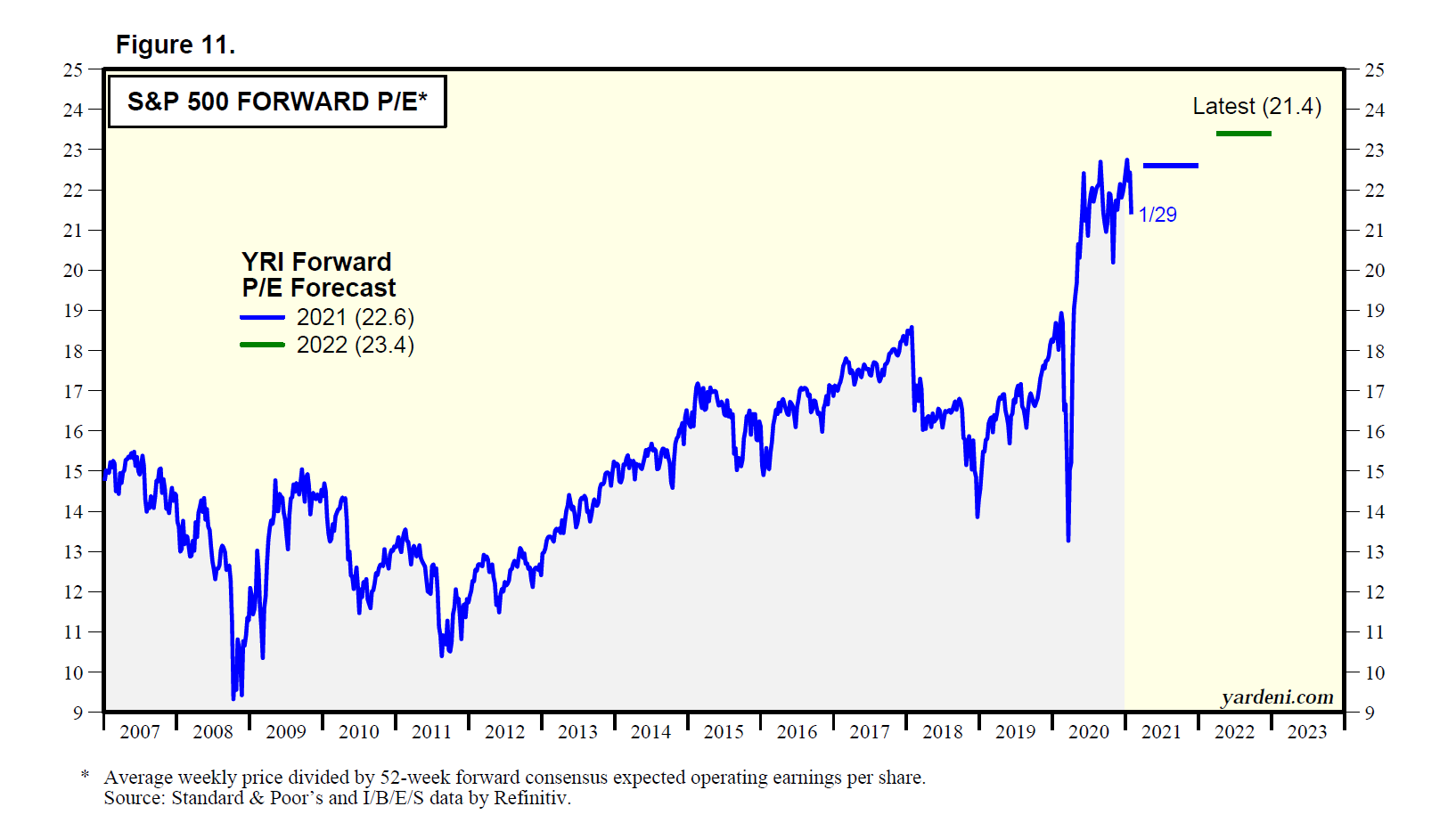

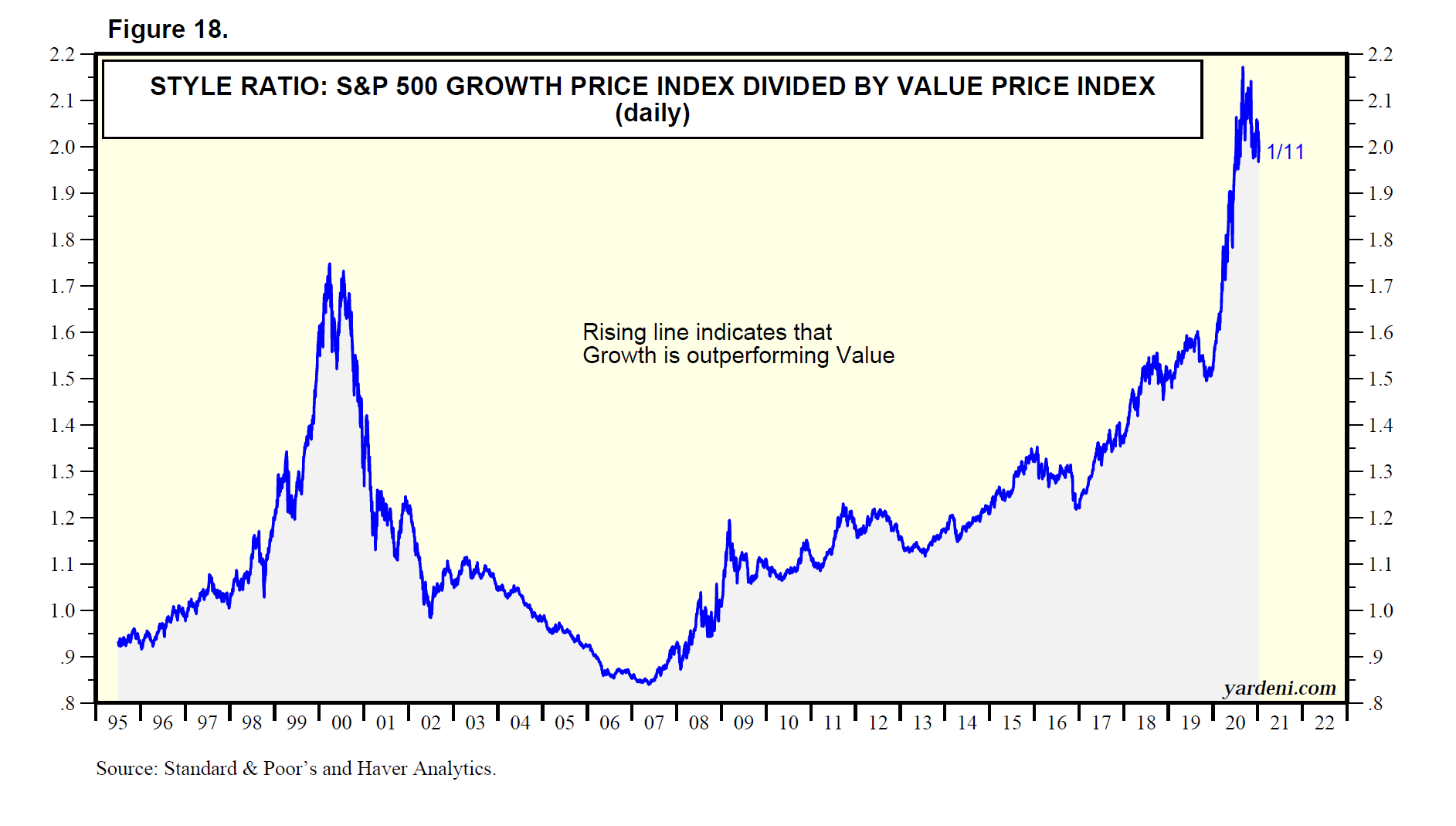

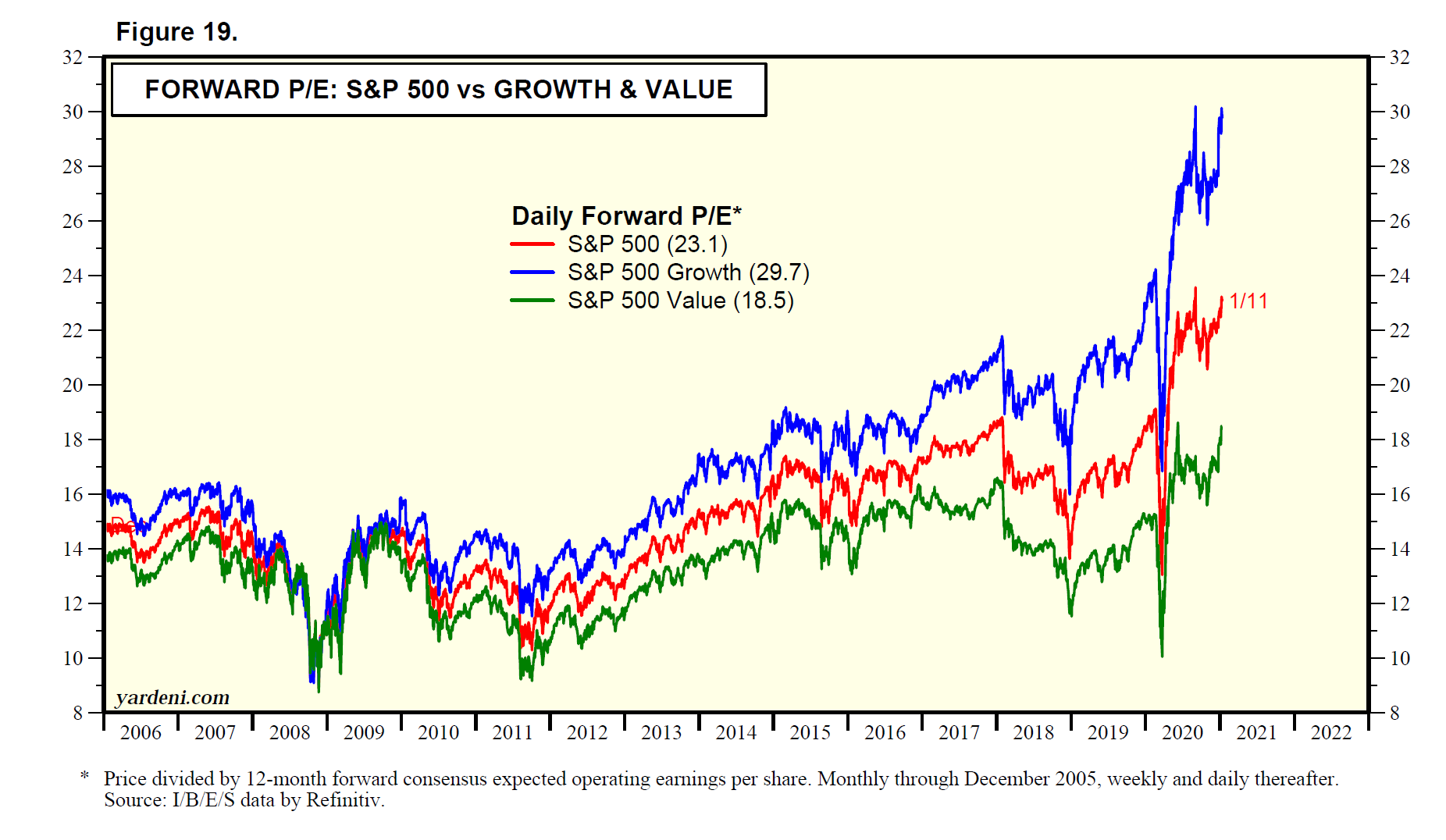

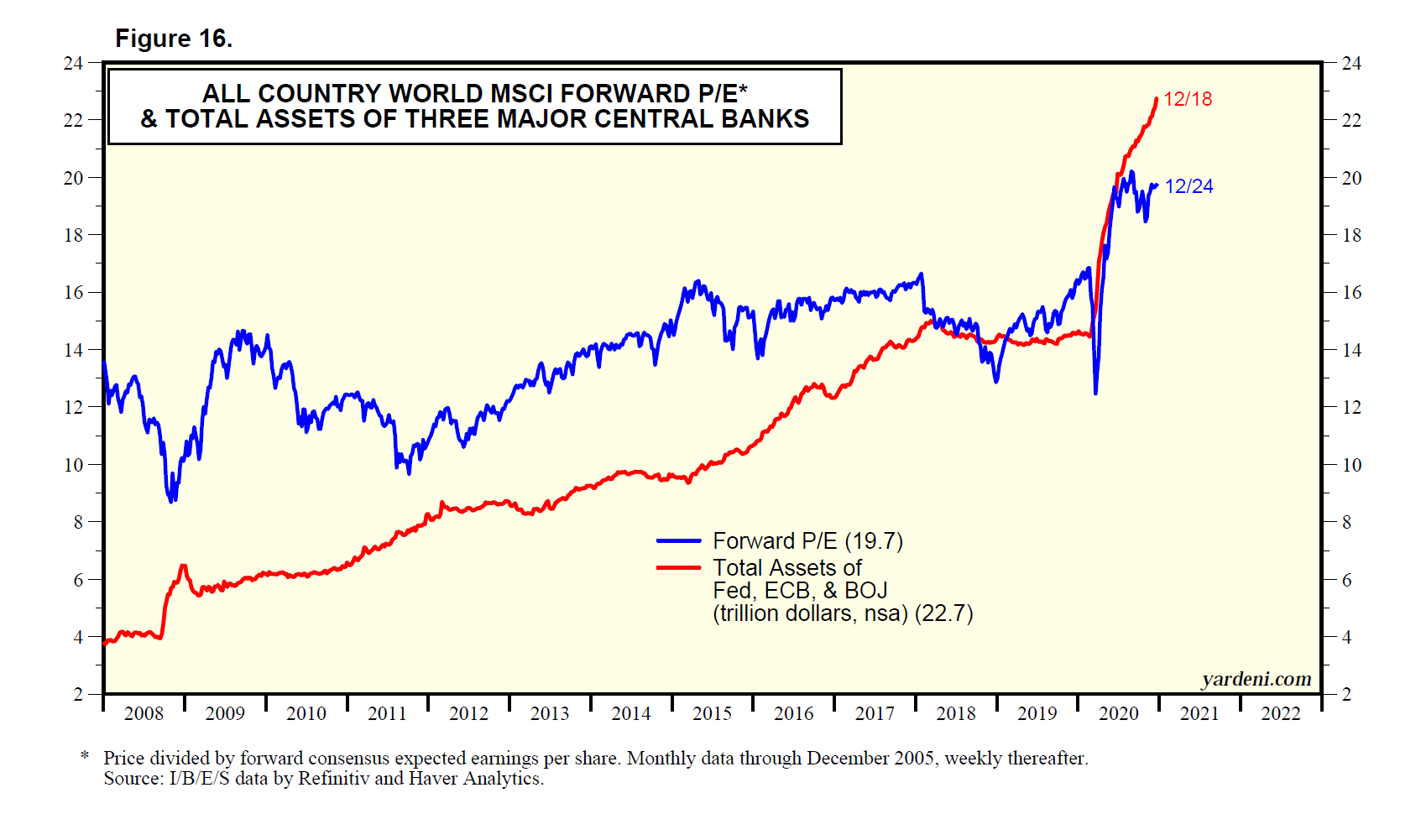

(2) Valuation multiples. The forward P/E of the S&P 500 remains above 20.0, bouncing back to 21.3 on Friday. The forward P/Es of the S&P 400/600 remained relatively depressed at 16.1 and 14.8 (Fig. 3). The forward P/Es of S&P 500 Growth and Value rose to 29.4 and 16.0 on Friday (Fig. 4).

(3) Yield curve. The Tech rally to a new record high is especially impressive given that the 2-year US Treasury yield rose to 0.67% last week, implying three 25-bps hikes in the federal funds rate next year (Fig. 5). However, the 10-year US Treasury bond yield remained below 1.50%. The “10-2” yield-curve spread has narrowed dramatically from a 2021 peak of 159bps on March 29 to 81 bps on Friday (Fig. 6).

The “5-2” yield-curve spread has been relatively flat around 70 bps over the same period. Both suggest that investors don’t expect the federal funds rate to rise by much more than the 75 bps currently expected for next year during the upcoming monetary tightening cycle. In other words, right or wrong, they expect that inflation will abate! That would be more “Ho-Ho-Ho!” for stocks!

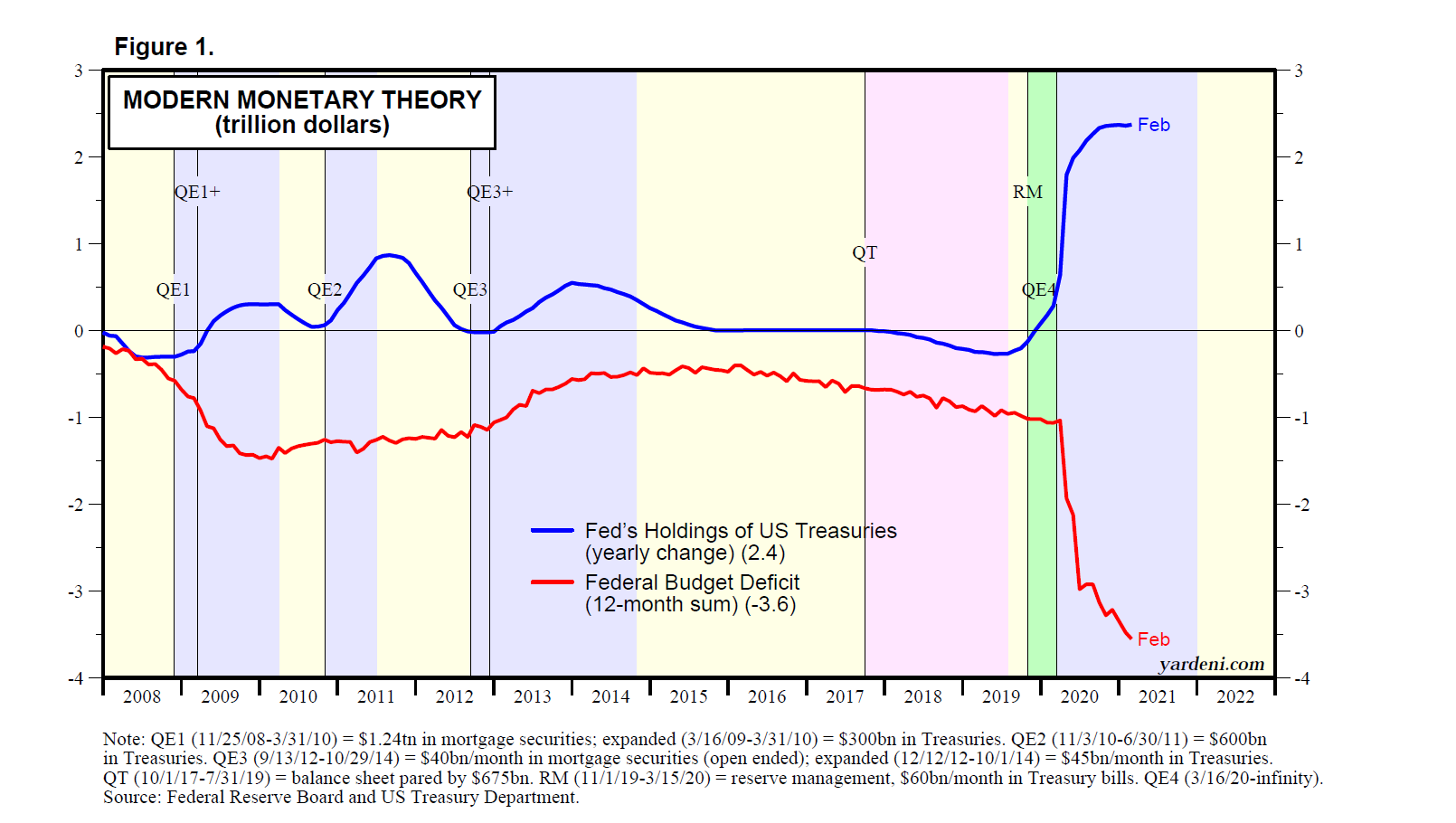

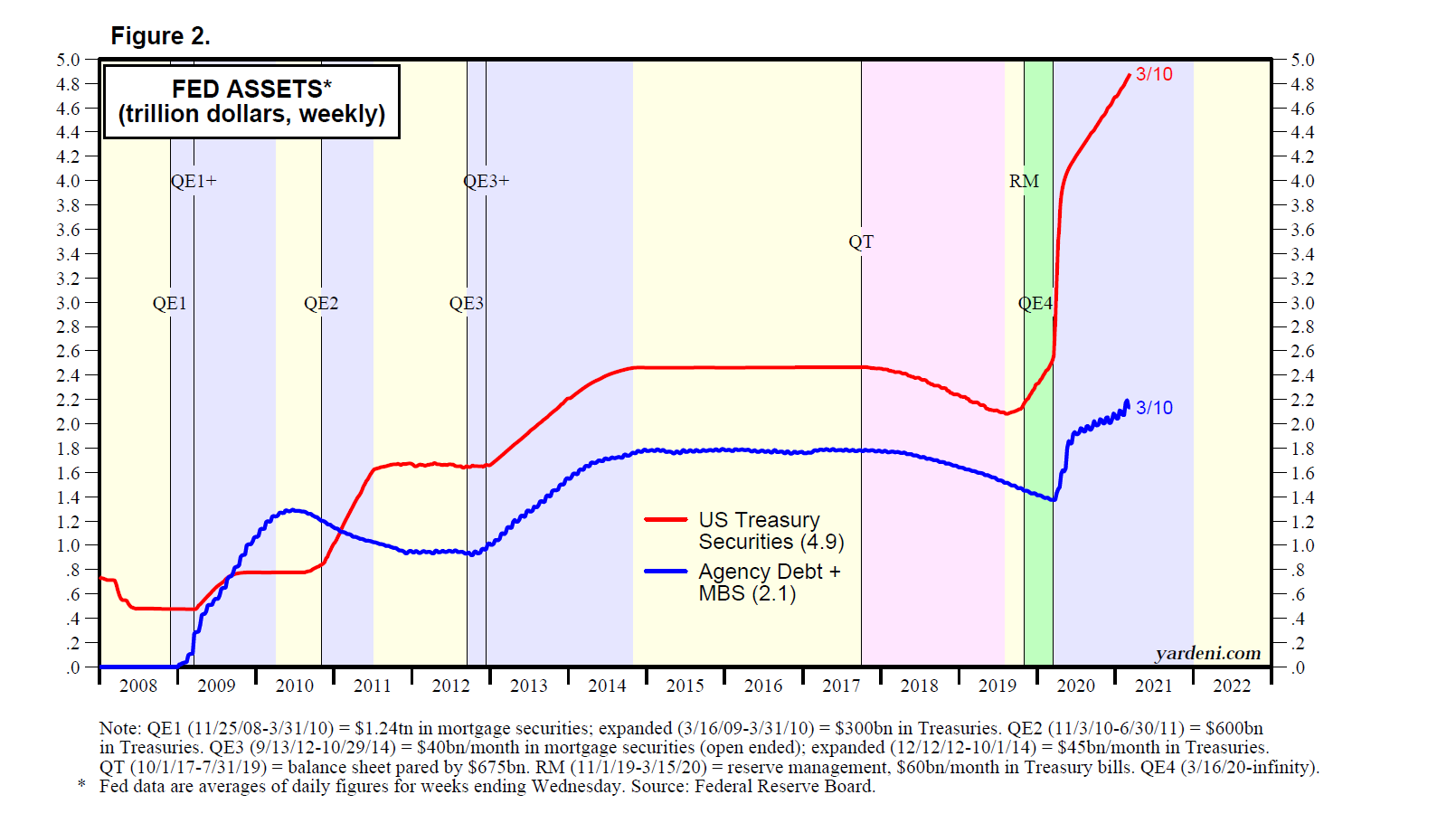

Inflation: Biden’s Helicopter Money. “Bidenflation” was unleashed by the $1.9 trillion American Rescue Plan (ARP), which was signed by President Joe Biden on March 11, 2021. It was passed in Congress by Democrats using the process of reconciliation, which did not require support from Republicans. In the House, all but one Democrat voted for the bill and all Republicans voted against the bill. In the Senate, the final vote was 50-49, with all Republicans voting against the measure and all members of the Senate Democratic caucus supporting it.

The ARP in combination with the Fed’s QE4 has been a textbook example of “helicopter money.” The ARP package provided direct stimulus payments of $1,400 to individuals, extended unemployment compensation, continued eviction and foreclosure moratoriums, and increased the Child Tax Credit while making it fully refundable. It provided $350 billion to state and local governments.

The ARP was entirely deficit financed. The Fed added to the inflationary consequences of the ARP by monetizing $80 billion per month of the federal government’s debt during the first 10 months of the year. The Fed continues to do so but at a slower pace since November.

In a February 4 Washington Post op-ed, economist Larry Summers, who served as a top economist in the Clinton and Obama administrations, trashed Biden’s plan. He said it’s too stimulative and too inflationary and includes overly generous unemployment benefits that would disincentivize the unemployed from taking jobs. Sure enough, the ARP created a demand shock that overwhelmed and disrupted the global supply chain. It exacerbated labor shortages, which clearly are structural. The ARP has been a major cause of the rebound in inflation in the US.

In congressional testimony on November 30, Fed Chair Jerome Powell pivoted by conceding that inflation isn’t transitory, but persistent. This increases the odds that the Fed will speed up the tapering of its asset purchases and start raising the federal funds rate before mid-2022. Surging inflation also increases the odds that Biden’s American Families Plan might not have enough votes to pass.

Debbie and I expect that tightening monetary policy and an amelioration of the supply-chain disruptions will reduce inflationary pressures by the second half of 2022. We also expect that businesses will respond to chronic labor shortages by spending more on technology to boost productivity. So we are predicting that the headline PCED inflation rate will hover between 4.0% and 5.0% through mid-2022 and then decline to 3.0%-4.0% during the second half of next year (Fig. 7). Now, consider the following related developments:

(1) Jobless claims and job openings. There now is mounting evidence, including the latest initial unemployment claims, that Summers was right about the ARP’s effect on the labor market. The federal jobless benefits provided by the plan, which was enacted on March 18, did provide a disincentive to work. The overly generous federal unemployment benefits (an extra $300 per week) did keep many of the unemployed from taking jobs. Initial unemployment claims fell below 300,000 in early October after the benefit was terminated. Jobless claims fell to 184,000 during the December 4 week (Fig. 8). That’s the lowest in 52 years!

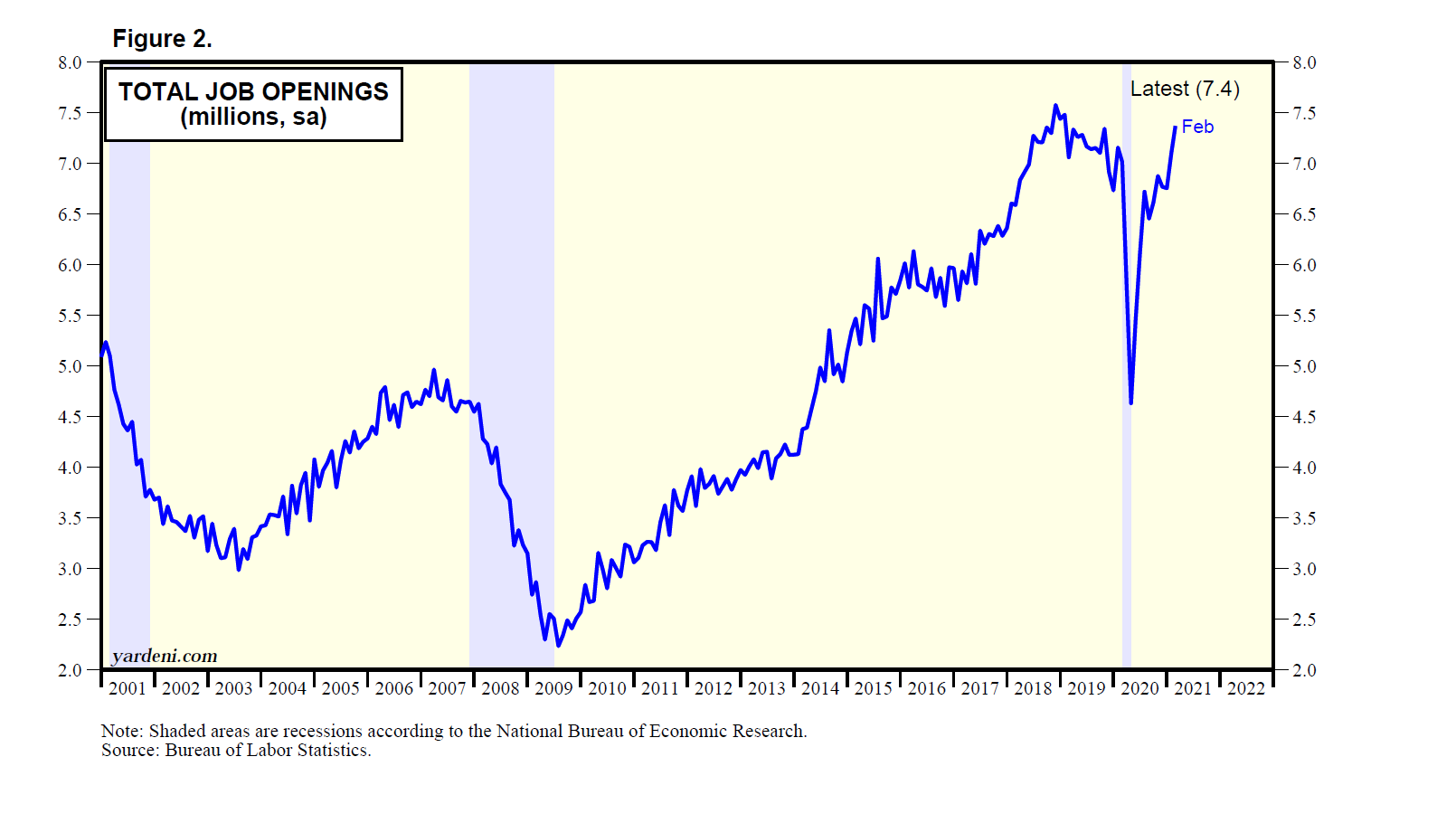

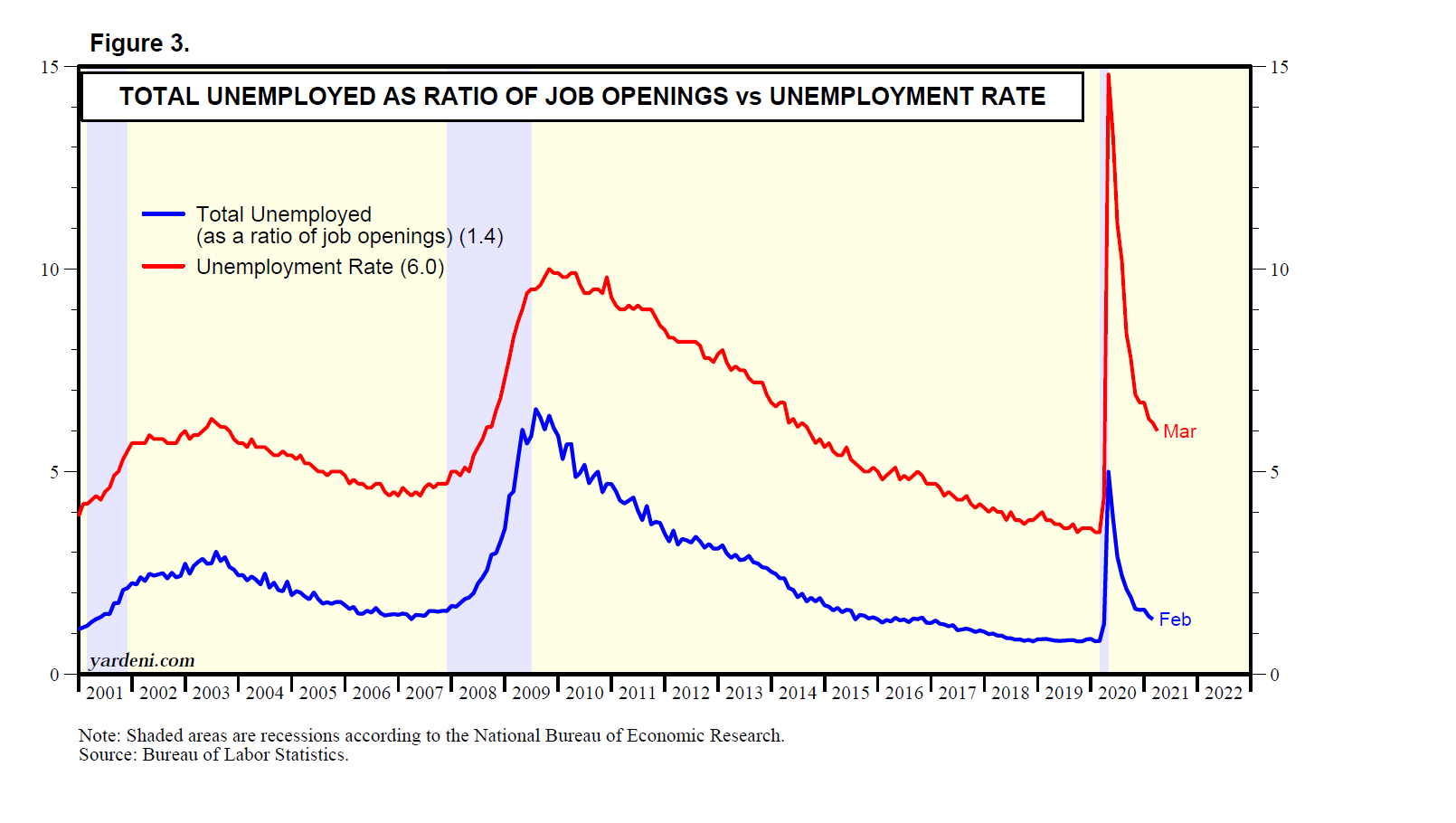

Total job openings remained in record-high territory at 11.0 million during October, while the number of unemployed fell to 6.9 million in November. Quits remained near September’s record high at 4.2 million during October.

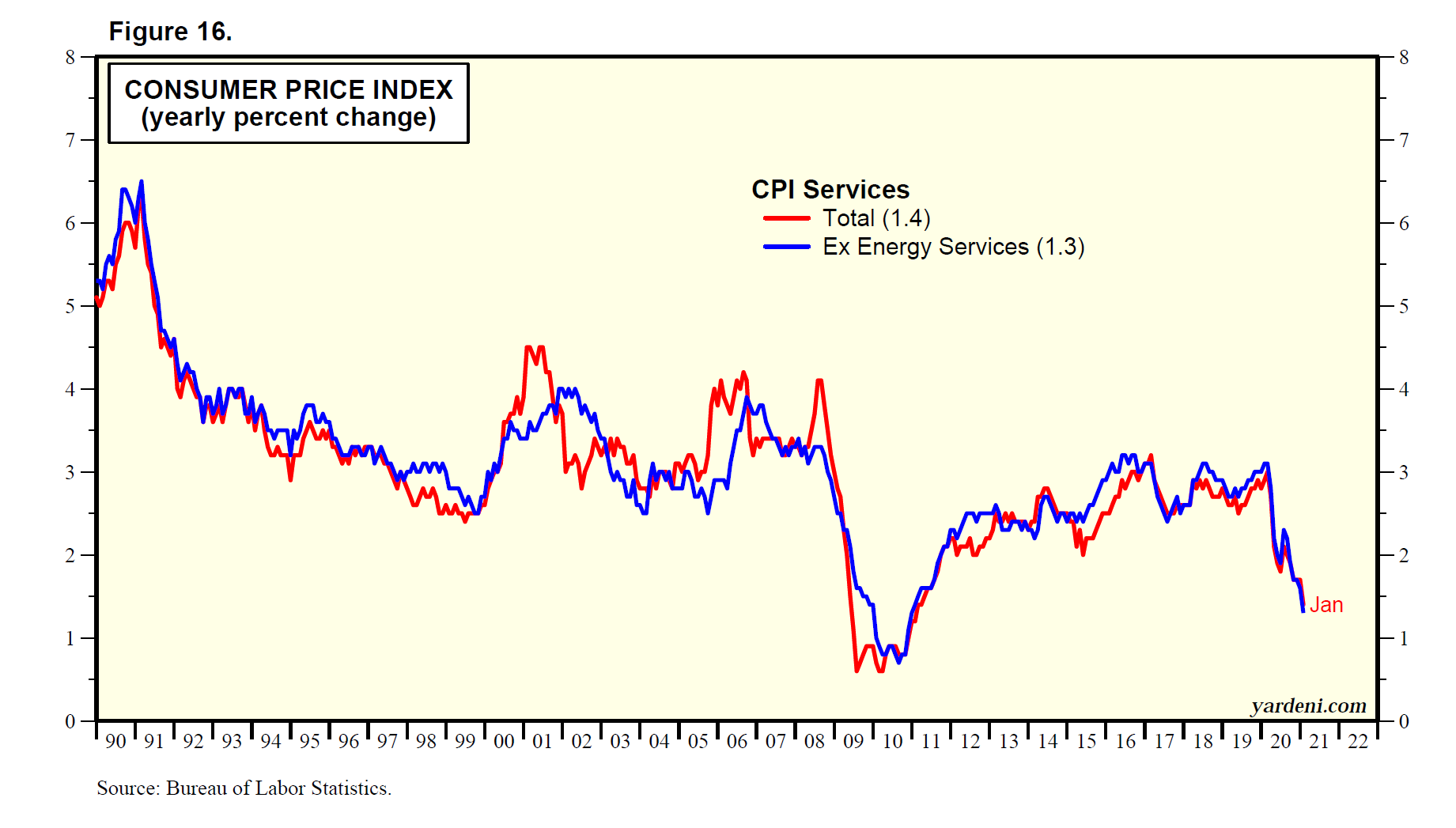

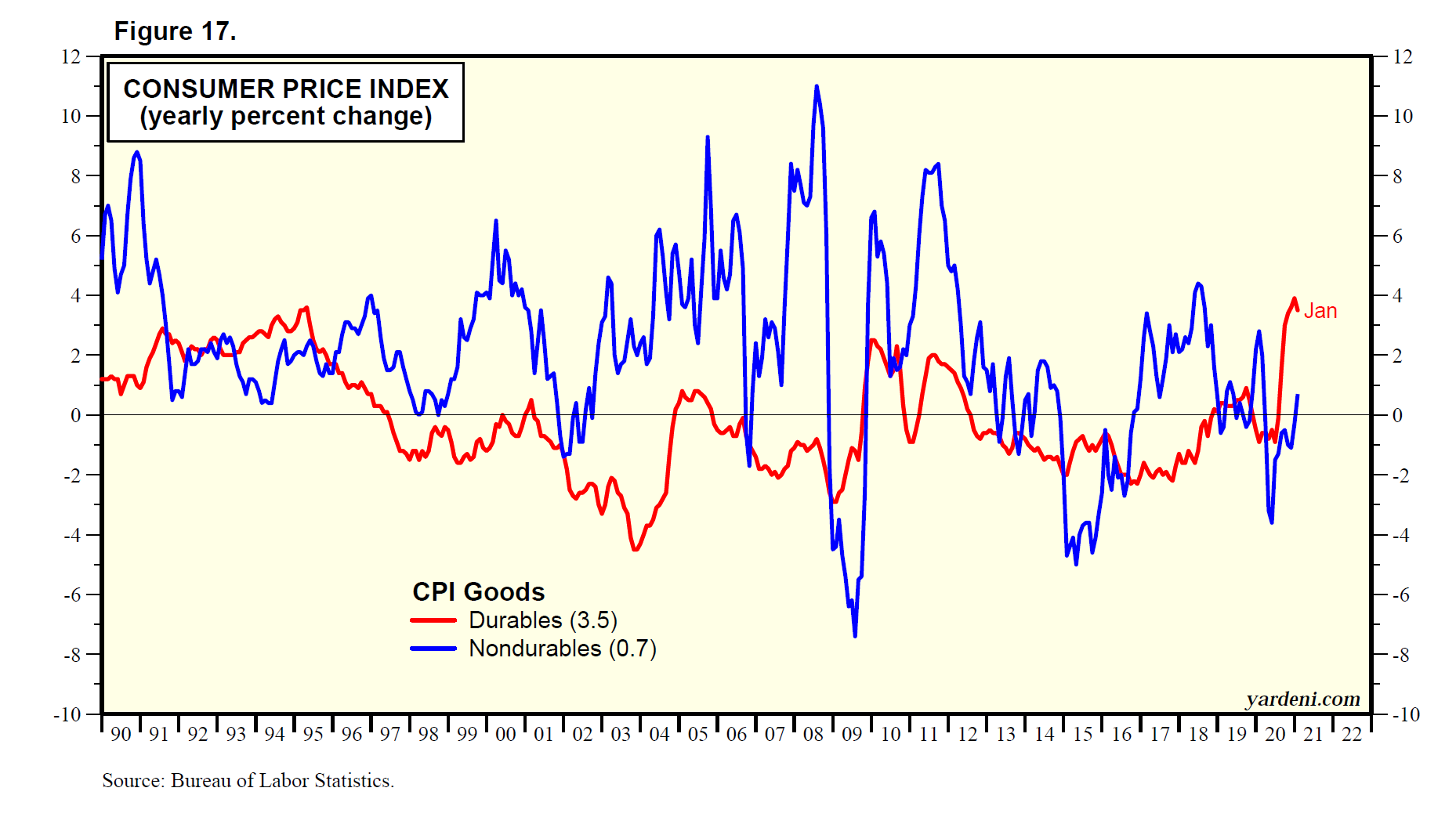

(2) Demand and supply shocks. November’s 6.8% y/y CPI reading was the highest in nearly 40 years (Fig. 9). Leading the way higher has been the CPI durable goods component, which was up 14.9% during November, while the CPI nondurable goods component rose 10.7% and the CPI services component rose 3.8% (Fig 10).

Durable goods prices have a long history of mostly deflating. This suggests that the rebound in inflation isn’t all Biden’s fault. The pandemic clearly disrupted global supply chains. Nevertheless, the ARP exacerbated inflationary pressures by boosting the demand for goods well above trend (Fig. 11). The demand shock overwhelmed the production and transportation systems for goods, thus causing the supply shock and boosting inflation.

As we noted above, improvements in the global supply chain, tighter monetary policy, less fiscal stimulus (assuming as we do that the American Families Plan doesn’t have enough votes to pass), and satiated pent-up demand collectively should moderate the pace of inflation by the second half of next year.

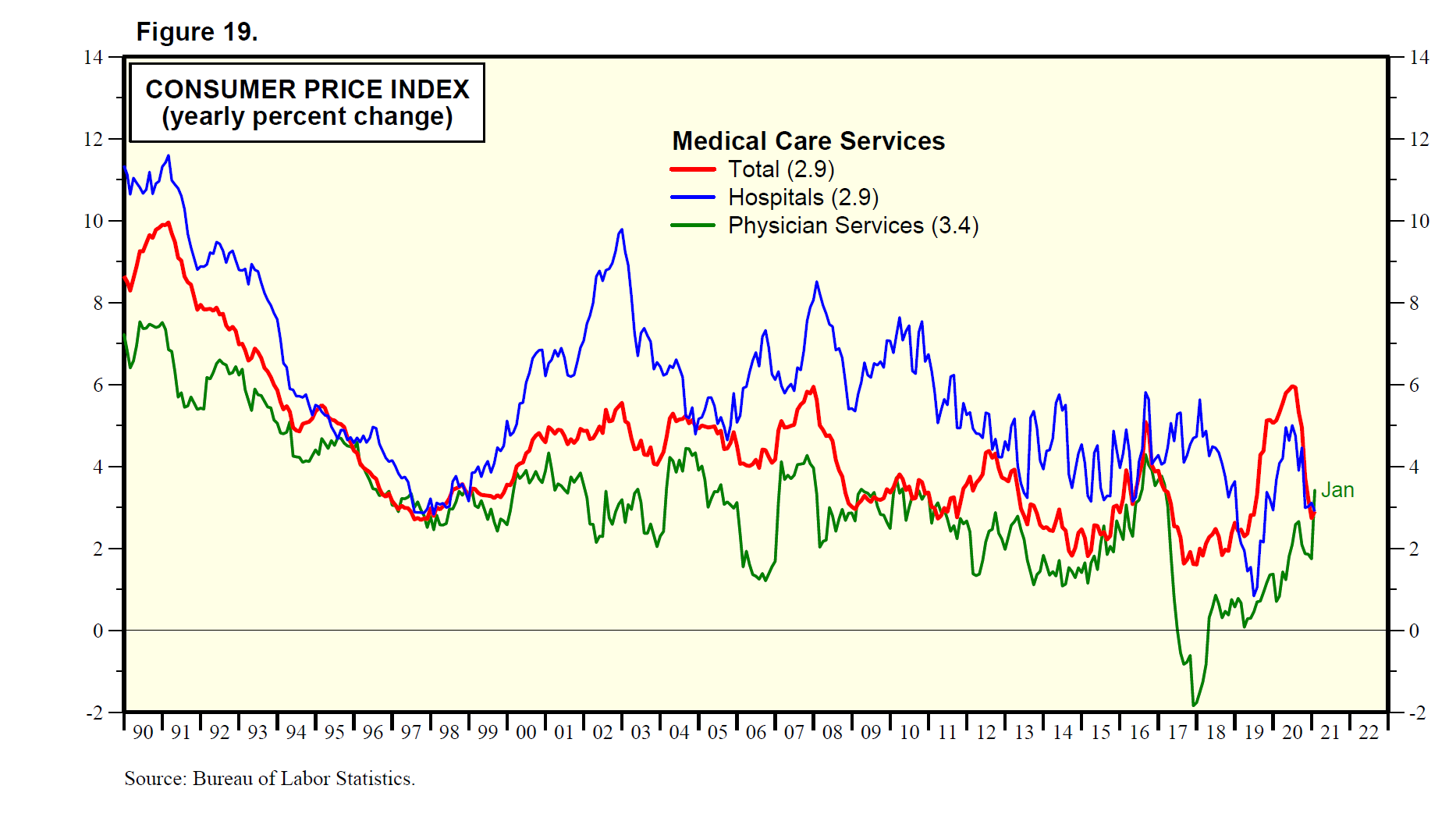

(3) Latest CPI and next PCED. The next important inflation data point will be November’s PCED inflation rate, which will be released on December 23 along with personal income and consumption. The core PCED inflation rate tends to be lower than the core CPI inflation rate (Fig. 12). That’s mostly because the PCED durable goods inflation rate and the medical care services inflation rate tend to be lower than the comparable CPI components (Fig. 13 and Fig. 14).

(4) Powell’s inflation. Again, Biden doesn’t deserve all the blame for the rebound in inflation. The Fed has made a major contribution with record-low mortgage rates that caused the median single-family existing home price to soar 30.3% from January 2020 (just before the pandemic) through October of this year. Many would-be home buyers have been priced out of the housing market and have boosted the demand for rental units. The CPI’s rent-of-shelter component was up 3.9% y/y during November, the highest since April 2007 (Fig. 15). It bottomed at 1.5% during February.

(5) Global inflation. Another reason that all the blame for the recent surge in inflation can’t be pinned on Biden is that other countries are also reflating. The OECD CPI inflation rate was 5.2% y/y through October, with the core rate at 3.5% (Fig. 16).

Here are the headline and core CPI inflation rates for some of the major Eurozone countries during November: Germany (6.0%, 4.1%), Eurozone (4.9, 2.6), Italy (4.0, 1.4), and France (3.4, 2.1). Policymakers in Germany haven’t provided as much fiscal and monetary stimulus as those in the US. Germany’s high inflation rate suggests that supply disruptions are contributing to global inflationary pressures.

(6) Yellen defends Build Back Better. Treasury Secretary Janet Yellen recently sent members of the US Senate a memo titled “Fiscal Responsibility and the Build Back Better Act.” She reassured them that the American Families Plan (AFP), if passed, won’t be fiscally irresponsible. On the contrary, it “will leave our nation’s budget in an improved position.” Moreover, AFP “will not add to near-term inflationary pressures.” Then again, she didn’t anticipate the near-term inflationary consequences of ARP.

By the way, a December 10 letter from the director of the Congressional Budget Office (CBO) responded to questions from a couple of members of Congress about BBB. They wondered what the impact would be if “specified modifications … would make various policies permanent rather than temporary.” The response stated that it would increase the deficit by $3.0 trillion over the 2022–31 period.

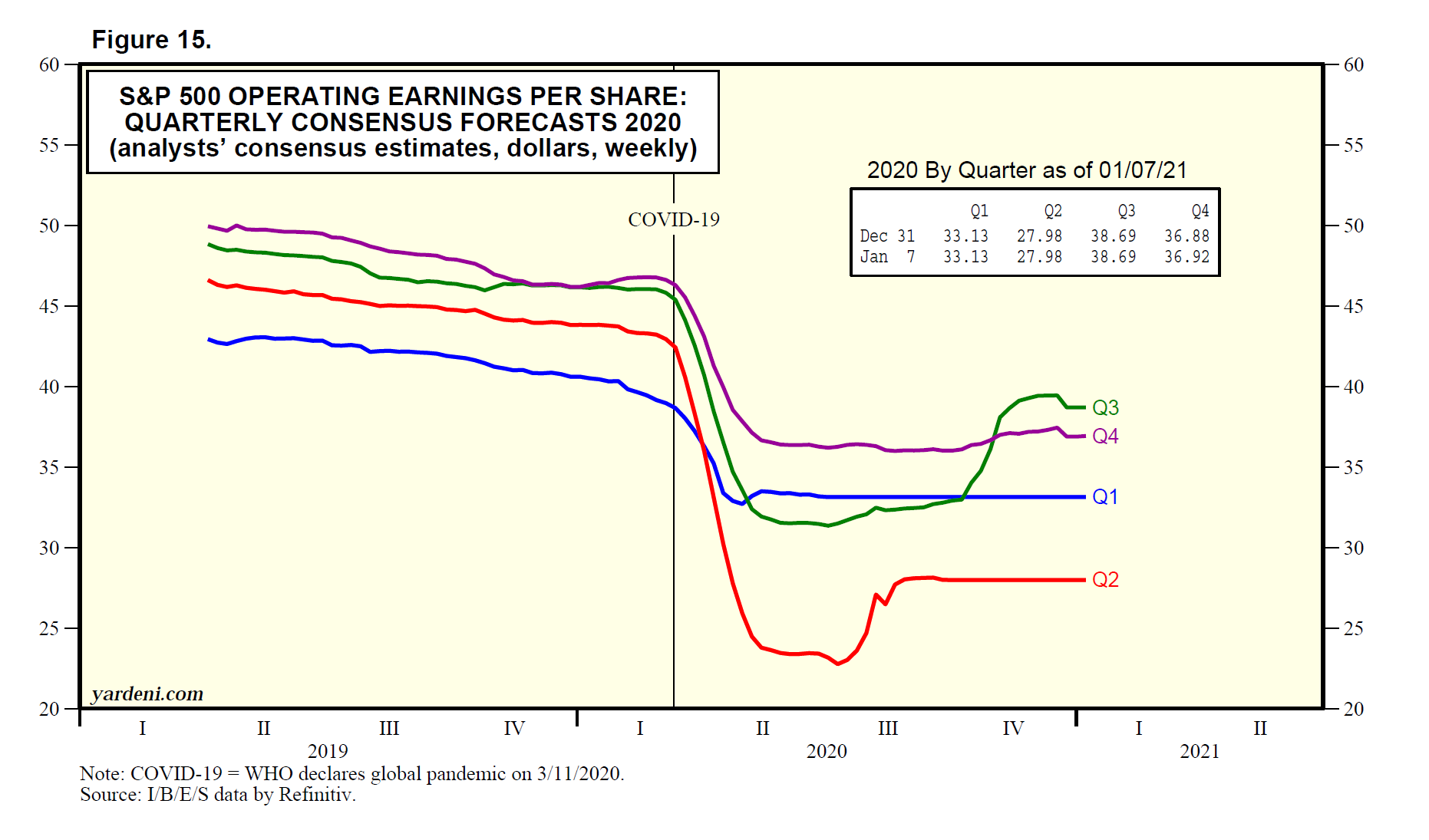

Strategy I: Real Earnings. Q3 revenues and earnings are out for the S&P 500. Joe and I will examine the data closely tomorrow. For now, we can report that revenues per share rose 13.9% y/y and earnings rose 39.3%. Most impressive is that the profit margin (which we calculate from the revenues and earnings data) ticked down only 0.1pt to 13.6% from Q2’s record high of 13.7% notwithstanding rapidly rising costs, labor shortages, and supply disruptions. That implies that companies overcame these problems by raising their prices and/or by boosting their productivity.

In other words, the increases in revenues and earnings are somewhat less impressive when adjusted for rapidly rising prices. During Q3, on a y/y basis, the CPI, PCED, and nonfarm business price deflator (NFBD) rose 5.3%, 4.3%, and 4.4%. We prefer the NFBD as a measure of the prices received by businesses, but it doesn’t differ much from the PCED (Fig. 17). We prefer not to use the CPI because it has a well recognized upward bias (Fig. 18).

In any event, using S&P 500 reported earnings-per-share data (which are available since 1935), we find that the series has tended to grow in a volatile fashion at a compound annual growth rate around 6.0% since 1947 (Fig. 19). Adjusting for inflation using the PCED (which is available since 1947), the rate tends to be around 3.0%.

While pricing power in an inflationary environment is a positive attribute for individual companies, collectively it tends to perpetuate wage-price spirals, creating a lose/lose/lose situation for companies, workers, and consumers.

Strategy II: Real Earnings Yield. Run for the hills! The real earnings yield turned negative during Q3 (Fig. 20). Since 1945, eight of the 11 bear markets in the S&P 500 were associated with declines in the real earnings yield (using reported earnings per share). It dropped to -0.84% during Q3. It is clearly something to add to investors’ worry list given its track record. However, Joe and I aren’t ready to give up on either the Santa Claus rally or a continuation of the bull market through 2022 and 2023.

Historically, the nominal earnings yield has always been positive with the exception of during Q4-2008. In other words, rising inflation has been the swing factor that caused the real rate to turn negative. In the past, rising inflation has also caused the Fed to tighten monetary policy in an effort to bring inflation down. That process won’t even start until the spring of next year, assuming that the FOMC ends QE4 by March of next year and votes to start raising interest rates during the May 3-4 meeting of the committee. It’s premature to conclude that the Fed’s next round of monetary tightening will end in tears and a recession.

Strategy III: Valuation and ETFs. There’s lots of controversy about the stock market’s valuation multiple. Everyone agrees that stocks aren’t cheap. The forward P/E of the S&P 500 is high. It has been hovering between 20 and 23 since the second half of 2020. On Friday, December 10, it was 21.3.

The debate is whether it is overdue for a fall. The question is: Why it has stayed so high in 2021 despite the surge in inflation and increasingly hawkish guidance from the Fed? There are many possible answers. The one that makes the most sense to us is that ultra-easy monetary and fiscal policies have produced at least $2 trillion of excess liquidity, which is boosting valuation multiples. (See the November 29 Morning Briefing.)

Some of that excess liquidity has been flowing into equity funds. They’ve attracted $385.5 billion over the past 12 months through October, with net inflows of $707.4 billion into ETFs and net outflows of 321.8 billion from mutual funds (Fig. 21). Buyers of equity ETFs tend to be much less focused on valuations than are mutual fund portfolio managers whose mandates force rebalancing out of stocks that gain too much market weight. This may explain why valuation multiples have been so high and might remain so in 2022 despite Fed tightening.

Movie. “West Side Story” (+ +) (link) is based on the classic 1957 musical conceived by Jerome Robbins with music by Leonard Bernstein and lyrics by Stephen Sondheim. This film is fondly directed by Steven Spielberg. I have fond memories of the play because it marked the beginning and end of my acting career. I played Chino in the 1967 production at New Rochelle High School. The music is eternally great, and the choreography is really wonderful in this remake of the original 1961 film starring Natalie Wood.

China, Wall Street, and the CIA

December 09 (Thursday)

Check out the accompanying pdf and chart collection.

(1) Evergrande’s restructuring looks likely. (2) It’s not alone. (3) Chinese economic growth slows, so its central bank boosts liquidity. (4) Hongkongers moving out. (5) Biden ires China by giving Taiwan a seat at the table and skipping the Olympics. (6) China building military outposts. (7) The little guys standing up to Xi might start a trend. (8) US financial giants see an opening in China and take it. (9) But are they hurting the US by developing China’s markets? (10) Taking a look at the venture capital firm that invests the CIA’s money. (11) Warning the US to up government research funding or risk losing our edge to China.

China: A Week of Headaches. We’ve always believed that actions speak louder than words. And no matter how often China’s leadership says all’s well, recent actions indicate otherwise. Evergrande, the country’s largest property developer, took one step closer to bankruptcy this week. Hong Kong residents are heading for the exits, and some external organizations have started to call out China’s tyranny. Let’s review what’s been a rough week for China’s leadership:

(1) Property sector unraveling. Evergrande failed to pay on Monday an $82.5 million debt payment that will likely result in an official default that pushes the large property developer to restructure its debt. The news is not a surprise, with the price of Evergrande’s dollar-denominated bonds below 20 cents on the dollar and the company’s shares each trading south of HK$2.

It’s widely known that Evergrande has roughly $300 billion in outstanding debt. Less understood are the guarantees the company has provided on other issuers’ debt. This week, the company unexpectedly revealed that “it has been asked to honor a debt guarantee of around $260 million, without providing further details,” a December 6 WSJ article reported.

Evergrande isn’t the only property developer in China having problems. There have been 11 defaults this year, land sales have fallen 55% y/y, and housing sales dropped 25% in October, according to JPMorgan data cited in a December 7 Reuters article.

Some of the specific companies in trouble were discussed in a December 6 Reuters article. Kaisa Group Holdings saw trading in its shares suspended Wednesday after it announced that bondholders rejected an exchange offer; Kaisa has $11.6 billion of dollar-denominated bonds outstanding. Sunshine 100 China Holdings defaulted on a $170 million dollar bond on Monday. And creditors of China Aoyuan Property Group have demanded repayment of $651.2 million in response to credit-rating downgrades—which it may be unable to pay due to a lack of liquidity.

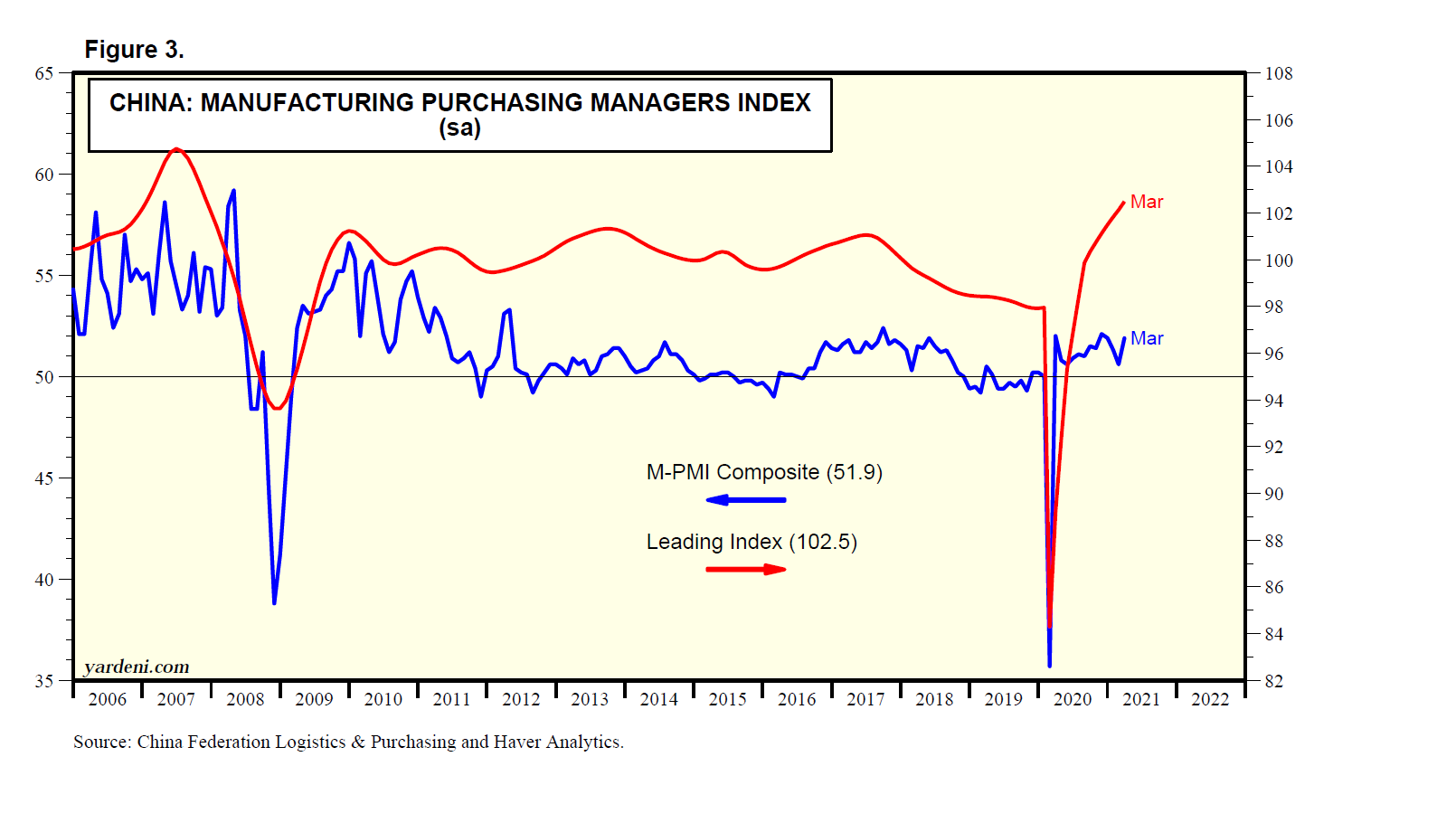

The property sector’s problems appear to be weighing on the economy. The November manufacturing purchasing managers index came in at 50.1, just barely above the 50.0 mark indicating expansion; but a number of the index’s components—including new orders (49.4) and employment (48.9)—were in contraction territory (Fig. 1). China’s central bank responded by cutting the bank reserve requirement on Monday by 50bps, its second cut this year (Fig. 2).

(2) Hongkongers hitting the road. The exodus from Hong Kong continues in the wake of the Chinese government’s changes to the city’s laws and clampdown on citizens’ freedoms. Nearly twice as many students and teachers have left 140 of Hong Kong’s secondary schools in the 2020-21 school year, a December 5 article in the South China Morning Post (SCMP) reported. Commenting readers blamed the lack of freedom and Internet censorship in Hong Kong now that the city is under Chinese control.

Separately, a survey by Oxford University’s Migration Observatory found that a third of British nationals living in Hong Kong are considering moving to the UK and 6% have already applied to do so. The survey polled 1,000 Hongkongers with British National (Overseas) status—which roughly 5.4 million of Hong Kong’s 7.5 million residents have, a December 3 SCMP article reported. Respondents wanted to move to the UK, then Taiwan, Australia, and Canada.

(3) US and China sparring. The US is not winning any friends inside China by inviting Taiwan to the Summit for Democracy, a virtual gathering this week of more than 100 democratic governments. The move counters China’s requirement that no country or company recognize the island as an independent nation. Zhao Lijian, a Chinese foreign ministry spokesman, warned: “Playing with the fire of ‘Taiwan independence,’ you will eventually get burned,” a November 24 WSJ article reported.

The Biden administration followed that jab by announcing that administration officials won’t be attending the Beijing Winter Olympics, citing the Chinese government’s “ongoing genocide and crimes against humanity,” referring to its treatment of Uyghur Muslims. Canada, the UK, and Australia followed the US’s lead and also announced a diplomatic boycott of the games. Athletes of the nations, however, will attend the Olympics. China’s Foreign Ministry said it would respond by taking “resolute countermeasures.”

The US is also working to thwart China’s attempts to expand its military presence around the world. Most recently, US diplomats have been trying to persuade Equatorial Guinea, on Africa’s west coast, not to allow China to build a military base there, according to a December 5 WSJ article, even though Equatorial Guinea already has a Chinese-built deep-water port. China already has a military base in Djibouti, on the east coast of Africa. And it has been building a military base at a Chinese-run commercial port in the United Arab Emirates (UAE), which the Biden administration has lobbied the UAE to halt.

(4) Finally taking a stand. Companies, organizations, and even basketball stars have been quick to ask for forgiveness whenever they’ve insulted or criticized China or supported Taiwan. But recently, some smaller entities have shown backbone, which may embarrass larger organizations into following their lead in the future.

The US Women’s Tennis Association (WTA) pulled all of its events out of China after it couldn’t confirm the wellbeing of Peng Shuai, a former doubles player ranked number one in the world and three-time Olympian. She posted an online message that said she was sexually assaulted by China’s former Vice Premier Zhang Gaoli and remains in China. Many elite tennis players supported both Peng and the WTA’s actions.